The 183-Day Tax Rule: What Expats Get Wrong

The 183-day rule is one of the most misunderstood rules in expat finance. Here is what it actually means—and where it will silently trap you.

Most expats misunderstand the 183-day tax rule. Learn how it actually works country by country and why it is irrelevant for US citizens abroad.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Most expats treat the 183-day rule like a magic password. Stay under 183 days in any given country, and you're free — no tax residency, no liability, no problem. That belief has cost people tens of thousands of dollars.

The 183-day figure appears in hundreds of tax treaties and domestic tax codes. But the number itself is almost never the whole story, and in some countries it's not relevant at all. For US citizens specifically, it's a complete red herring when it comes to US federal tax obligations. Here's what the rule actually means — and where it will quietly ambush you if you don't understand the fine print.

What the 183-Day Rule Actually Is

The 183-day rule is a threshold for tax residency — not tax liability. Crossing it in a country typically means that country claims the right to tax your worldwide income. Staying under it doesn't automatically mean you're not a tax resident; it just means you might qualify for a non-residency claim, depending on the country's other tests.

Where it originated: most modern tax treaties are based on the OECD Model Tax Convention, which uses 183 days as a standard reference point for determining whether a country can tax employment income earned by visiting workers. From there, individual countries adopted it — often incompletely, with their own modifications and additional tests layered on top.

The result is a patchwork of rules that share the same number but work completely differently. Understanding which version applies to you is one of the most important financial decisions you'll make as an expat.

US Citizens: The 183-Day Rule Is Irrelevant for Your US Taxes

If you're a US citizen or Green Card holder, no amount of careful day-counting protects you from US federal income tax. The United States is one of only two countries in the world (the other being Eritrea) that taxes based on citizenship rather than residency. You owe US taxes on your worldwide income regardless of where you live or how many days you spend outside the country.

The 183-day substantial presence test exists in the US tax code, but it's designed for foreign nationals — to determine when non-US citizens become US tax residents after spending time in the country. For US citizens already living abroad, it's irrelevant.

What offsets your US bill: the Foreign Earned Income Exclusion (FEIE), the Foreign Tax Credit, and bilateral tax treaties. These reduce or eliminate double taxation — but none of them remove the filing obligation. You still file a US return every year, regardless of days spent.

The IRS weighted formula for the substantial presence test (for foreign nationals) is also more complex than most realize. It counts all days in the current year, plus one-third of days in the prior year, plus one-sixth of days two years prior. A foreign national who spent 120 days in the US this year, 120 days last year, and 120 days the year before can still trigger US tax residency even though they were never present for 183 days in a single calendar year.

Country-by-Country: Where the 183-Day Rule Actually Applies

Here's where expats discover how fragmented this system really is. The same 183-day figure can mean completely different things depending on which country's tax code you're reading.

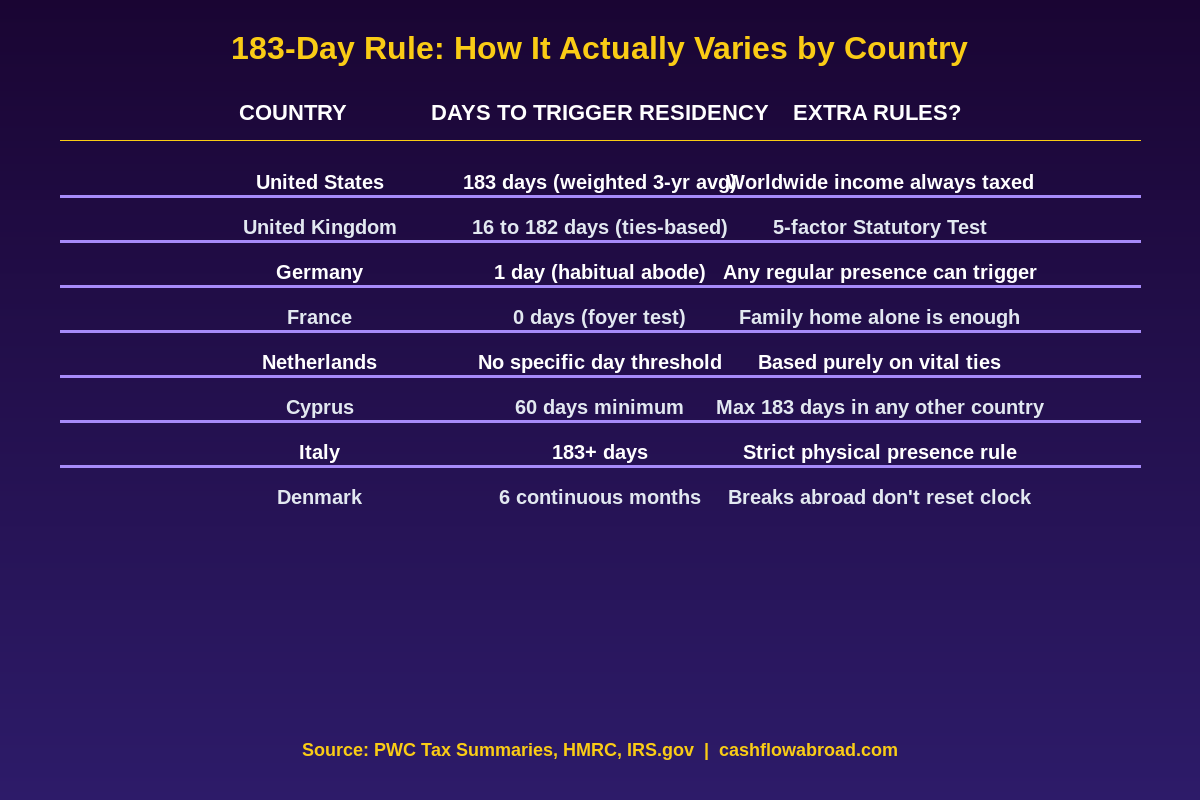

| Country | Day Threshold | Additional Tests | Key Risk |

|---|---|---|---|

| United States | N/A for citizens; weighted 3-yr formula for foreign nationals | Citizenship-based taxation | US citizens always file regardless of days |

| United Kingdom | 16–182 days depending on ties | 5-factor Statutory Residence Test | 4 UK ties + 16 days = resident |

| Germany | No fixed threshold | Habitual abode / dwelling test | Any regular presence + home = resident |

| France | 0 days (foyer test) | 4 independent triggers | Family home alone triggers residency |

| Netherlands | No day threshold | Durable ties and vital interests | Connections, not days, determine status |

| Italy | 183+ days | Civil Registry registration also triggers | Registering as resident = worldwide taxation |

| Cyprus | Minimum 60 days | Max 183 days in any other single country | Unique 60-day non-domicile rule |

| Denmark | 6 continuous months | Short breaks don't reset the clock | A single long stay can trap you |

| Thailand | 180+ days | 2024 rule change taxes foreign remittances | New rule caught many existing expats off guard |

The UK's Statutory Residence Test: The Most Dangerous Trap

The UK Statutory Residence Test (SRT), introduced in 2013, replaced a simple 183-day rule with a multi-factor matrix that turns otherwise non-resident expats into UK taxpayers. Most people who fail it had no idea they were at risk.

The SRT counts five types of "UK ties": a family tie (spouse or minor children living in the UK), an accommodation tie (any property you can use, including a parent's spare room), a work tie (more than 40 days of UK work per year), a 90-day tie (spending more than 90 days in the UK in either of the two preceding tax years), and a country tie (the UK being the country where you spent the most days that year).

The key table:

| Number of UK Ties | Days in UK Before You Become Resident |

|---|---|

| 4 ties | 16 days |

| 3 ties | 46 days |

| 2 ties | 91 days |

| 1 tie | 121 days |

| 0 ties | 183 days |

A former UK resident who still has a parent's house they occasionally use, a child in school in London, and who visited more than 90 days in the prior year may have three ties. At just 46 days — less than seven weeks — they become a UK tax resident with worldwide income obligations. Many expats who moved to Dubai or Portugal specifically for their low-tax regimes have been caught by HMRC enquiries on exactly this pattern.

Germany and France: Where Days Don't Matter Much

Germany's tax residency rules don't fix a day-based threshold. Residency is triggered by having a "dwelling" (Wohnsitz) or "habitual abode" (gewöhnlicher Aufenthalt) in Germany. A dwelling is any place you maintain as a home on a more than temporary basis — even if you only use it occasionally.

This means a German national who keeps an apartment in Berlin for 30 or 40 days a year can still be classified as a German tax resident. The Federal Finance Court has consistently held that maintaining a readily available home constitutes a dwelling under §8 of the German Tax Code, regardless of how many days are actually spent there. The habitual abode test can also apply to furnished holiday apartments used repeatedly, even those that aren't owned or formally leased.

France is even more sweeping. Under Article 4B of the French General Tax Code, you're a French tax resident if any of the following four conditions are met independently:

- Your foyer (habitual household) is in France — your family lives there

- Your principal place of activity is in France

- Your principal place of professional activity is in France

- Your center of economic interests is in France

None of these require you to spend a single day in France. An executive whose family remains in Paris while they work abroad becomes a French tax resident purely on the foyer test, regardless of how many days they're physically in the country. The French tax authority (Direction Générale des Finances Publiques) has enforced this aggressively against expatriates who relocated for work but left families behind.

The Digital Nomad's Specific Problem

The rise of digital nomad visas has created a new category of taxpayer especially vulnerable to the 183-day misconception. Nomads who deliberately stay under 183 days in every country, believing this keeps them tax-resident nowhere except their home country, often run into several hard problems:

You may become tax-resident by default. When you have no clear tax domicile, some countries can claim you by default. The US still claims you as a citizen. Your former home country may claim you never properly deregistered. A country where you spent four months may claim habitual presence. Legally "living nowhere" is harder to achieve than it sounds — and the consequences of getting it wrong are expensive.

FBAR and FATCA don't disappear. US citizens who open foreign accounts while nomading still face FBAR reporting if those accounts exceed $10,000 at any point during the calendar year. FBAR penalties for "willful" violations can reach the greater of $100,000 or 50% of the account balance per year — and the IRS's AI-driven cross-referencing with FATCA data now detects unreported foreign accounts with dramatically higher accuracy than it did five years ago.

Maintaining a US address matters more than most nomads realize. For banking, brokerage accounts, IRS correspondence, and state domicile purposes, a legitimate US physical address is essential. A virtual mailbox service like Traveling Mailbox gives you a real US street address in 50+ cities, handles mail scanning, and costs around $15/month — far less than losing access to US banking infrastructure while abroad. For the full breakdown on maintaining your US financial presence from abroad, see the expat virtual mailbox guide.

The five-flag strategy requires real legal structuring. Legitimately reducing global tax exposure through second residency and territorial tax jurisdictions isn't about casual day-counting. It requires formal establishment of tax domicile, banking relationships, and often physical presence documentation — all of it defensible under audit.

The Dual Residency Trap

What happens when two countries both claim you as a tax resident simultaneously? This is more common than most expats expect. A US citizen spending eight months a year in Germany may trigger German tax residency under the habitual abode test while remaining a US tax resident by citizenship. Both countries want to tax worldwide income.

Tax treaties are supposed to resolve these conflicts via tiebreaker rules, running through a hierarchy: first, where do you have a permanent home? If both, where is your center of vital interests? If still unclear, where do you habitually reside? Then nationality, then mutual agreement between tax authorities.

Two things make these tiebreakers fail:

- The saving clause. Most US tax treaties contain a saving clause explicitly preserving the US's right to tax its own citizens regardless of treaty provisions. Claiming treaty benefits to avoid US tax rarely works for US citizens — the saving clause blocks it in almost every case.

- No treaty exists. The US has income tax treaties with about 68 countries. Living outside that list — Thailand, Cambodia, Argentina, Vietnam — means you rely entirely on unilateral relief like the Foreign Tax Credit, which may not fully offset double taxation depending on the type of income.

How to Count Your Days (It's More Nuanced Than You Think)

Even when you know a day-threshold applies, counting correctly is non-trivial.

The IRS counts any day you are physically present in the US as a full day, even if you arrive at 11:55 PM. The day you depart is generally not counted as a US day. Transit days — changing planes in a US airport — count as US days unless you never leave the international zone, which isn't possible in most US airports because there is no separate international zone.

The UK's SRT counts any day present in the UK at midnight as a UK day. A short UK visit that doesn't extend past midnight doesn't count — but a stopover that runs past midnight does. Exceptional circumstances (medical emergencies, natural disasters) can allow up to 60 additional days without them counting toward the tie-breaker totals.

Germany counts continuous stays without a fixed daily limit for the dwelling test, but for the "habitual abode" standard, continuous presence of more than six months anywhere in Germany — including repeated stays in vacation rentals — can trigger residency regardless of total annual count.

Practical implication: if you're managing days carefully, maintain a contemporaneous travel log with flight records, accommodation receipts, and boarding passes. This is what you produce if a tax authority challenges your non-residency claim. Without contemporaneous documentation, their presumption will stand.

What to Actually Do About It

Establish tax domicile formally before you leave. If you're pursuing a territorial tax country strategy, formally register in your target jurisdiction — set up a local bank account, sign a lease, and document the relocation. Some countries require formal deregistration from your home country. Germany and the Netherlands have explicit deregistration processes; skipping them keeps you in the tax system.

Audit your ties before moving. If you're leaving the UK, France, or Germany, count your ties before departure. Keeping a property available, leaving a family member behind, or maintaining a UK company directorship can keep you tied to a tax system you believe you've escaped.

Don't confuse visa rules with tax rules. A digital nomad visa lets you legally work in a country. It says nothing about tax obligations. Some visa programs explicitly grant tax exemptions — Paraguay's zero-tax on foreign income is a genuine exemption — but others don't, and assuming a visa confers tax benefits without reading the actual tax code is a costly mistake.

Use the right financial infrastructure. A brokerage that works globally — like Charles Schwab International with its fee-free ATM access worldwide — avoids the PFIC problems that come with buying foreign mutual funds. For international money transfers, Remitly consistently offers better rates than traditional bank wires with faster settlement.

File even if you owe nothing. Information returns (FBAR, Form 8938, Form 5471) carry penalties entirely independent of your tax liability. With the IRS's 2026 AI cross-referencing against FATCA data, the probability of detection for unreported foreign accounts is higher than it's ever been. At a 7% annual interest rate on underpayments plus failure-to-file penalties of up to 25% of unpaid tax, the cost of non-compliance compounds fast.

The Bottom Line

The 183-day rule isn't wrong — it's just dangerously incomplete. It's a starting point in some tax systems, irrelevant in others, and completely beside the point for US citizens managing their federal filing obligations. The expats who navigate this successfully understand that tax residency is a legal status determined by multiple overlapping tests — physical presence, vital interests, domicile, citizenship, and treaty provisions all interacting simultaneously.

Counting days is necessary but never sufficient. Building a defensible tax position requires understanding which tests apply where you live and where you're from, and then satisfying each one systematically — with documentation. The good news: this is entirely achievable. Thousands of US expats legitimately minimize their global tax burden through careful, legal planning. But it starts with ditching the idea that one number — 183 — unlocks the whole system.

For a comprehensive look at how the full US expat tax framework fits together, including FEIE, the Foreign Tax Credit, FBAR, and expat banking strategy, the US expat banking and taxes guide is the right starting point before making any major international moves.

Financial Disclaimer: This article is for informational and educational purposes only. It does not constitute legal, tax, or financial advice. Tax laws vary by country and individual circumstances change frequently. The rules described here are subject to change by legislation, treaty, or administrative guidance. Always consult a qualified international tax attorney or CPA before making decisions about tax residency, foreign financial accounts, or cross-border financial planning.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 29, 2026

Expat Tax & FinanceMay 29, 2026

Self-Employment Tax: The Expat Freelancer’s Hidden Bill

FEIE zeroes your income tax abroad—but SE tax still applies. See the exact numbers and legal ways to reduce your bill as a US expat freelancer.

Expat Tax & FinanceMay 26, 2026

Expat Tax & FinanceMay 26, 2026

Portugal IFICI: Is the NHR Replacement Worth It?

NHR ended in 2025. Portugal's IFICI replacement gives tech workers and researchers a 20% flat tax for 10 years — but retirees and passive investors.

Digital Nomad & Visa GuidesMay 25, 2026

Digital Nomad & Visa GuidesMay 25, 2026

Bali's $130K Visa and the Tax Trap Most Nomads Miss

Indonesia's $130K Second Home Visa sounds ideal — but the 183-day tax rule could expose your worldwide income. Here's what nomads need to know.