Territorial Tax Countries: Where Foreign Income Is Never Taxed

Countries like Panama, Costa Rica, Paraguay, and Georgia never tax foreign-source income. Full list with residency requirements, costs, and catches.

Countries like Panama, Costa Rica, Paraguay, and Georgia never tax foreign-source income. Full list with residency requirements, costs, and catches.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Here's a number that should make you furious: the average American pays an effective federal income tax rate of around 13–14% — but if you're earning $120,000 a year and living in the right country, you could pay zero to your country of residence. Not 3%. Not a flat 10%. Literally zero. And in many cases, you'll still dramatically reduce — or eliminate — your US tax bill at the same time.

This isn't some offshore shell company scheme from a 1980s James Bond villain. It's called territorial taxation, and it's the legal foundation on which dozens of sovereign countries have built their entire tax code. These countries have decided, as a matter of national policy, that income you earn outside their borders is none of their business.

For US expats, remote workers, digital nomads, and anyone building location-independent wealth, understanding territorial tax countries isn't a nice-to-have — it's the difference between keeping $29,000 more per year and handing it to governments that had nothing to do with your success.

Related: five-flag strategy guide

Let's break down exactly how it works, which countries do it best, what it costs to establish residency there, and — critically — how it interacts with your obligations as a US citizen.

What Is Territorial Taxation (And Why Most Countries Don't Use It)

The world's tax systems broadly fall into two camps:

Residence-based (worldwide) taxation: You pay tax on all income you earn anywhere on the planet, simply because you live in that country. The United States, Germany, France, Australia, and most Western nations use this approach. If you live in France and earn consulting income from US clients, France wants its cut.

Territorial taxation: You only pay tax on income earned within that country's borders. If you live in Panama and earn consulting income from US clients — income sourced outside Panama — Panama doesn't tax it. At all.

There's also a third category: zero personal income tax countries like the UAE and Bahrain, where there's simply no personal income tax on anything. These overlap heavily with territorial systems in their practical effect for expats.

Most high-income Western countries use worldwide taxation because it maximizes revenue and prevents wealthy residents from routing income through low-tax jurisdictions. Territorial systems are more common in developing economies and financial hubs that want to attract foreign capital and talent without creating barriers to international business.

The practical upshot for you: if you move to a territorial tax country and earn your income from outside that country (remote work, online business, foreign investments, foreign rental income), you owe that country nothing on that income.

The US Expat Catch: You Still Owe the IRS (But It Can Be Minimized)

Here's where Americans have to pay extra attention. The United States is one of only two countries in the world (the other being Eritrea) that taxes its citizens on worldwide income regardless of where they live. This means that even if you move to Panama and Panama owes you zero local taxes on your remote work income, the IRS still wants to hear from you.

That said, the US tax code provides two major tools that can dramatically reduce — or eliminate — that US tax liability:

1. The Foreign Earned Income Exclusion (FEIE): If you pass the bona fide residence or physical presence test (generally 330+ days outside the US), you can exclude up to approximately $130,000 of foreign earned income from your US taxable income. For many expats earning in the $80K–$130K range from remote work or freelancing, this exclusion effectively zeroes out their US income tax on that income.

2. The Foreign Tax Credit (FTC): If you do pay local income taxes in your country of residence, you can generally use those as a dollar-for-dollar credit against your US tax bill. The problem? In a territorial country where you pay zero local tax, there are no foreign taxes to credit — which is why the FEIE becomes so important for territorial-country residents.

The powerful combination: live in a territorial tax country + claim the FEIE = $0 local tax + near-zero US tax on the excluded amount. Many US expats in Panama, Paraguay, and Georgia are legally paying a few hundred to a few thousand dollars in total annual income tax on six-figure incomes.

For a deep dive into the FEIE mechanics, see our full guide: How to Pay Zero Federal Tax (Legally) as a US Expat.

The Best Territorial Tax Countries for US Expats

Not all territorial tax jurisdictions are created equal. Here's a detailed breakdown of the best options, ranked by accessibility and practical value for expats:

1. Paraguay — The Best-Kept Secret in Expat Finance

Paraguay has become the darling of the digital nomad tax optimization world, and for good reason: it may be the easiest and cheapest territorial tax residency available anywhere.

Tax system: Pure territorial. 0% income tax on all foreign-sourced income, period. Paraguay doesn't care if you deposit foreign earnings into a Paraguayan bank account — it's still not taxed. For locally-sourced income, a flat 10% rate applies.

What makes Paraguay unique:

- No minimum stay requirement to maintain residency. You can get Paraguayan residency and never live there if you choose — you just need to visit once every three years.

- Not a CRS participant. The Common Reporting Standard (CRS) is the OECD's global framework for automatic exchange of financial information between tax authorities. Paraguay doesn't participate, meaning your Paraguayan bank accounts won't be automatically reported to your home country. (Note: US citizens still have FBAR/FATCA obligations regardless.)

- Low residency cost: approximately $2,290 in legal fees and government processing costs, with no mandatory investment or bank deposit requirement.

- Permanent residency in under 3 years: After 21–24 months of temporary residency, you can upgrade to permanent status, then a path to Paraguayan citizenship opens after 3 years of permanent residency.

How to get residency: The most accessible route is the "independent means" visa. You need to show proof of income (approximately $1,300/month) and submit standard documents (apostilled birth certificate, criminal background check, passport). A short visit to Asunción — typically 2–5 days — is required to submit your application in person. Many expats use a local lawyer to handle the paperwork for $1,500–$3,000 total.

Cost of living: Asunción is genuinely cheap — $800–$1,500/month covers a comfortable expat lifestyle. You're not obligated to live there, but those who do find it surprisingly livable with a growing international community.

The catch: Paraguay is not a glamorous destination. It's landlocked, relatively undeveloped compared to other expat hubs, and English is not widely spoken. Most people use it as a tax residency base, not a primary lifestyle destination.

2. Panama — The Original Expat Tax Haven

Panama has been attracting wealth-conscious expats for decades, and its territorial tax system is the bedrock reason. The country has deliberately positioned itself as a financial and business hub, and its tax code reflects that ambition.

Related: FEIE zero tax guide

Tax system: Pure territorial. 0% income tax on all foreign-sourced income. Panamanian-sourced income is taxed at progressive rates up to 25%. Capital gains on real estate are generally taxed at 10%.

Key visa options for expats:

- Digital Nomad Visa: Requires proof of minimum $36,000/year in foreign income ($3,000/month). Grants 9 months initially, renewable for another 9 months. Not a path to permanent residency, but excellent for testing the lifestyle.

- Friendly Nations Visa: Available to citizens of 50+ countries (including the US). Requires establishing economic ties — either a Panamanian company, property purchase, or employment. More permanent solution with a path to residency.

- Pensionado Visa: For retirees with $1,000/month or more in permanent income (pension, Social Security, etc.). One of the world's best retiree visa programs, with extensive discounts on everything from airfare to medical bills.

Cost of living: Panama City is the most expensive option (approximately $1,800–$2,800/month for a comfortable lifestyle), but smaller cities and beach towns run $1,200–$1,800/month. See our Geographic Arbitrage Playbook for detailed Panama cost breakdowns.

Practical advantage: The US dollar is Panama's currency. Zero currency risk, no forex fees on USD transactions, and US banking works seamlessly. Panama is also a 3-hour flight from Miami — you're never truly far from home.

Banking: Mercury works well as your US business banking anchor while you maintain a local Panamanian account for expenses. The two-account approach is standard practice for Panama-based expats.

3. Georgia — The 1% Tax Rate That Broke the Internet

The country of Georgia (not the US state) has become one of the hottest expat destinations on earth, and not just because of the wine and the mountains. Georgia's tax system offers two genuinely exceptional options for remote workers and online business owners.

Option A — Territorial Tax Residency: Foreign-sourced income is taxed at 0% if you establish tax residency and your income originates outside Georgia. To qualify as a tax resident, you need to spend 183 or more days per year in Georgia.

Option B — Small Business Status (SBS): This is Georgia's hidden gem. If you register as an Individual Entrepreneur and obtain Small Business Status, you pay just 1% tax on your total turnover (not profit — turnover) up to 500,000 GEL per year, which is approximately $180,000 USD. On income above that threshold, the rate rises to 3%. This applies even if your income is sourced from Georgia itself.

To put that in perspective: a US expat earning $120,000/year through a Georgian IE business structure pays about $1,200 in local taxes annually. Combined with the FEIE, total tax burden can fall under $5,000/year on $120,000 of income.

Residency requirements: Georgian citizens of most Western countries can stay visa-free for up to 365 days. After 183 days, you can apply for tax residency status. Setting up as an Individual Entrepreneur typically costs $500–$1,500 in legal fees and can be done in a week in Tbilisi.

Important update: Georgia has been refining its rules around the SBS regime. Eligible businesses include IT, digital marketing, consulting, design, and most remote work categories. It excludes gambling, licensed activities, and staffing agencies. Verify current eligibility with a local accountant before restructuring your affairs around this regime.

Cost of living: Tbilisi is exceptionally affordable — $1,000–$1,600/month covers a genuinely good lifestyle with quality restaurants, fast internet (100Mbps+ fiber is widely available), and a thriving expat community. Georgia consistently ranks among the top 3 digital nomad destinations globally for value.

4. UAE — Zero Tax, World-Class Infrastructure

The United Arab Emirates has no personal income tax. Full stop. Not territorial, not conditional on income source — there is simply no personal income tax in the UAE. This applies to all residents, including the hundreds of thousands of expats who've made Dubai and Abu Dhabi their home.

What makes the UAE different:

- No personal income tax of any kind on employment income, business income, dividends, rental income, or capital gains for individuals.

- Free Zones: The UAE has dozens of economic free zones (DIFC, ADGM, IFZA, and many others) where you can establish a company with 100% foreign ownership, near-zero corporate tax on qualifying activities, and simplified banking. Setup costs run $3,000–$8,000 depending on the free zone and license type.

- Digital Nomad Visa: Allows remote workers to live in the UAE for up to one year, renewable. Requires proof of employment with a non-UAE company and minimum monthly income of $3,500.

- Golden Visa: Long-term 10-year residency for investors, entrepreneurs, specialists, and high achievers. Real estate investment of AED 2 million (approximately $545,000) is the most straightforward qualification path.

The trade-offs: The UAE is expensive. Dubai lifestyle costs run $3,000–$5,000/month or more for a comfortable expat setup. Summer temperatures regularly hit 45°C (June through September). The cultural environment is more conservative than most Western expats are accustomed to.

US expat note: The UAE's strength for US citizens is primarily as a lifestyle base combined with the FEIE. Since there's no local income tax, you can't use foreign tax credits — so the FEIE becomes the essential mechanism to offset your residual US tax liability on foreign earned income.

5. Costa Rica — Territorial Tax in Paradise

Costa Rica operates a pure territorial tax system and has been attracting North American expats for 40 or more years. If you earn income from outside Costa Rica — a US-based online business, foreign investments, remote employment with a US company — that income is not taxed in Costa Rica.

Visa options:

- Rentista Visa: Requires $2,500/month in stable foreign income. Valid for 2 years, renewable, with a path to permanent residency after 3 years.

- Pensionado Visa: For retirees with $1,000/month or more in pension income. Comes with 20% discounts on utilities, 15% on restaurant bills, and various medical exemptions.

- Digital Nomad Visa: Requires $3,000/month income ($4,000 if applying with a family). Valid for 2 years.

Cost of living: San José runs $1,500–$2,200/month for a comfortable expat lifestyle. Beach areas like Tamarindo or Jacó cost more ($2,000–$3,000). The Central Valley is the sweet spot — excellent infrastructure, top-tier medical care, and a massive US expat community makes the transition easy.

For comprehensive health insurance options while abroad, our Expat Health Insurance Guide covers plans including SafetyWing, which starts at $45–$85/month and covers most of Latin America.

6. Belize — English-Speaking Territorial Tax

Belize is the only English-speaking country in Central America with a pure territorial tax system. Foreign-sourced income is completely exempt from Belizean taxation for residents.

Related: golden visa guide

The Qualified Retired Persons (QRP) program is Belize's flagship expat visa: it requires $2,000/month in foreign pension or retirement income and grants immediate permanent residency status with import duty exemptions on household goods, a vehicle, and a boat or small aircraft.

Cost of living in Belize City is modest ($1,200–$1,800/month), and popular expat areas like San Ignacio or Placencia run lower. The trade-offs: Belize lacks the infrastructure, medical facilities, and amenity level of Panama or Costa Rica, and internet reliability outside major towns can be inconsistent.

7. Malaysia — Foreign Income Exemption Extended to 2036

Malaysia made a significant pro-expat move when it extended its foreign-sourced income exemption for individual residents through December 31, 2036. This means Malaysian tax residents pay 0% on income earned from abroad for the next decade — a uniquely long runway of tax certainty that no other country on this list can match.

The Malaysia My Second Home (MM2H) program was relaunched with revised requirements. The current Silver Tier requires MYR 500,000 (approximately $110,000) in liquid assets and MYR 40,000/month (approximately $8,800) in offshore income — significantly higher than the old program. The DE Rantau digital nomad pass is more accessible: it requires $24,000/year (approximately $2,000/month) in income and 60+ days in Malaysia during the validity period.

Why Malaysia anyway? Kuala Lumpur offers exceptional quality of life at $1,200–$1,800/month. World-class healthcare, outstanding food, strong English proficiency throughout the professional class, and direct flights to essentially everywhere in Asia make it a serious lifestyle contender.

8. Croatia — The EU Territorial Option

Croatia is one of the few EU member states that specifically exempts digital nomad visa holders from local income tax on foreign income. The Croatian digital nomad visa (technically a temporary stay permit) allows up to 1 year of residence with a minimum income requirement of approximately €2,300/month. No local income tax applies to your foreign earnings during this period.

The limitation: it's capped at 1 year and is not a path to permanent EU residency or citizenship. But for someone who wants to spend a year in Split or Dubrovnik without a local tax headache, the lifestyle value is hard to overstate.

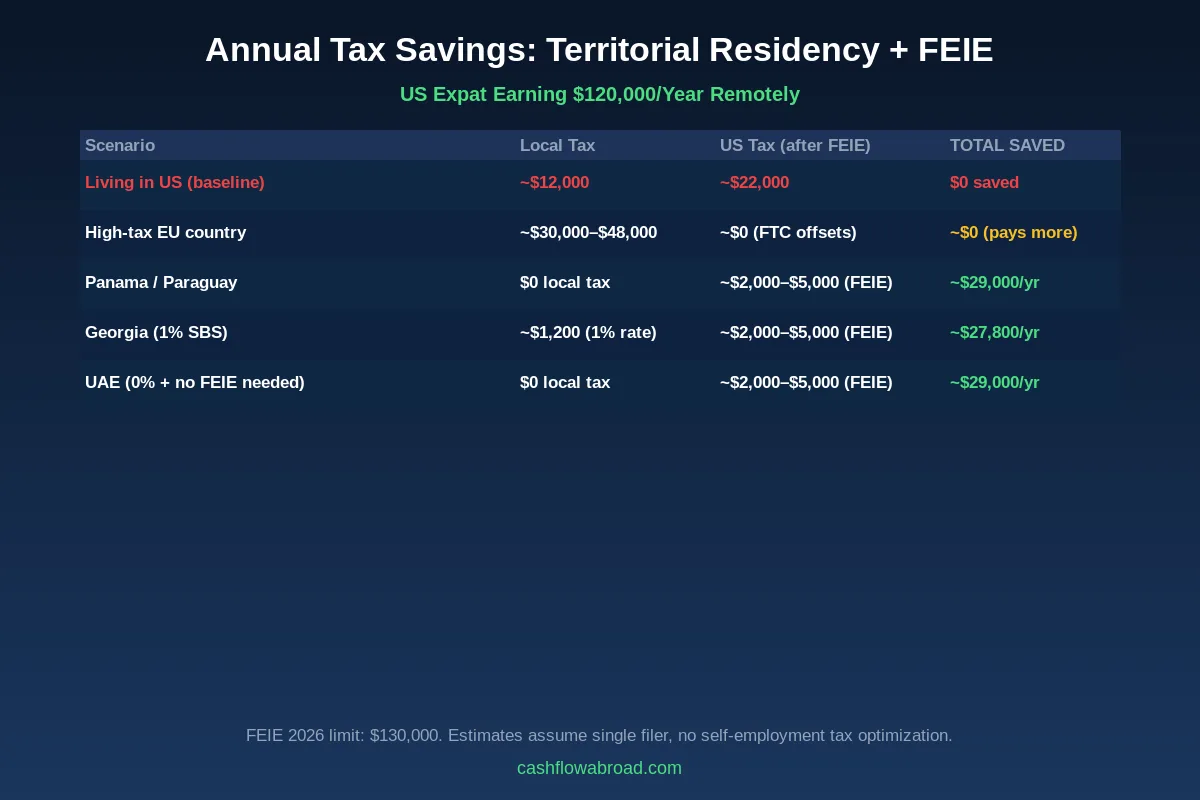

The Math: What This Actually Saves You

Let's run the actual numbers for a US expat earning $120,000/year from remote work or an online business:

| Location | Local Income Tax | US Tax (after FEIE ~$130K) | Total Annual Tax | vs. Living in US |

|---|---|---|---|---|

| Living in the US | N/A | ~$22,000–$24,000 | ~$22,000–$24,000 | Baseline |

| High-tax EU (Germany, France) | ~$36,000–$48,000 | ~$0 (FTC offsets US tax) | ~$36,000–$48,000 | Pay more |

| Panama or Paraguay | $0 | ~$2,000–$5,000 (SE tax) | ~$2,000–$5,000 | Save ~$19,000–$22,000/yr |

| Georgia (1% SBS) | ~$1,200 | ~$2,000–$5,000 (FEIE + SE tax) | ~$3,200–$6,200 | Save ~$17,800–$20,800/yr |

| UAE | $0 | ~$2,000–$5,000 (FEIE + SE tax) | ~$2,000–$5,000 | Save ~$19,000–$22,000/yr |

Estimates assume single filer, self-employed income, FEIE exclusion of approximately $130,000. "SE tax" refers to self-employment tax (Social Security and Medicare, 15.3% on net self-employment income) which the FEIE does not eliminate. Proper business structuring can further reduce SE tax exposure. Consult a qualified expat CPA.

Over a 10-year career abroad in a territorial tax country, combined with proper US tax optimization, a $120K earner could accumulate $190,000–$220,000 in additional compounding capital compared to living in the US — simply from not paying that money in taxes. That's a down payment on investment property. That's a decade of maxed-out retirement accounts. That's what geographic arbitrage looks like in real numbers.

For investment strategies to deploy those savings, see our Expat Investor's Playbook.

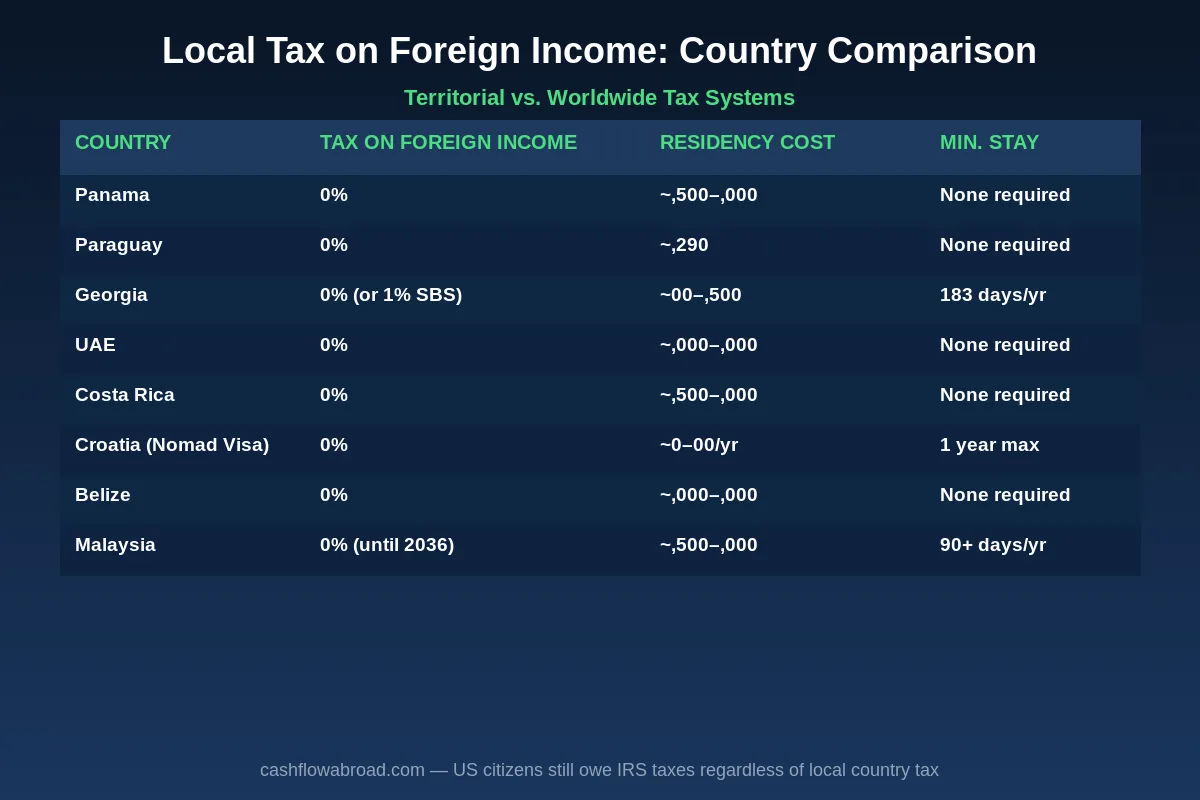

Full Country Comparison: Territorial Tax Jurisdictions

| Country | Foreign Income Tax | Min. Income Req. | Residency Cost | CRS Member | Path to PR |

|---|---|---|---|---|---|

| Paraguay | 0% | ~$1,300/month | ~$2,290 | No | Yes (2 years) |

| Panama | 0% | $3,000/month (nomad) | ~$3,500–$7,000 | Yes | Yes (multiple paths) |

| Georgia | 0% or 1% SBS | None required | ~$500–$1,500 | Yes | Yes (6+ years) |

| UAE | 0% | $3,500/month (nomad) | ~$3,000–$8,000 | Yes | Yes (Golden Visa) |

| Costa Rica | 0% | $2,500–$3,000/month | ~$2,500–$4,000 | Yes | Yes (3 years) |

| Belize | 0% | $2,000/month (QRP) | ~$1,000–$2,000 | Yes | Yes (QRP = permanent) |

| Malaysia | 0% (until 2036) | $2,000/month (DE Rantau) | ~$1,000–$3,000 | Yes | Yes (MM2H) |

| Croatia | 0% (nomad visa) | ~$2,300/month | ~$100–$200 | Yes | No (nomad only) |

| Hong Kong | 0% foreign income | None required | ~$5,000–$10,000 | Yes | Yes (7 years) |

| Singapore | 0% foreign income (generally) | Varies by visa | High | Yes | Yes (professional paths) |

What Changed Recently: The Tax Landscape Is Shifting

Territorial tax residency has grown in popularity — which means some countries are tightening the rules. Here's what's changed that you need to know before making a move:

Thailand Closed Its Remittance Loophole

Thailand used to be a popular hack: it technically taxed foreign income, but only if you remitted it to Thailand in the same tax year you earned it. Expats would earn income, park it offshore, then bring it in the following year — legally tax-free. Thailand eliminated this strategy for all income earned after January 1, 2024. Any foreign income earned after that date is now taxable when remitted to Thailand, regardless of timing or the year it was earned. Thailand is no longer a reliable territorial tax option for planning purposes.

The UK's Non-Dom Regime Is Gone

The UK ended its centuries-old non-domicile tax regime. The replacement Foreign Income and Gains (FIG) regime offers only 4 years of foreign income exemption for new arrivals — down from potentially unlimited duration under the old system. The UK is no longer a viable territorial tax base for long-term planning.

Portugal's NHR Regime Was Replaced

Portugal's famous Non-Habitual Resident (NHR) regime — which gave expats 10 years of 0% tax on most foreign income — was abolished at the end of 2023. The replacement "IFICI" incentive regime is more limited, primarily targeting tech workers, scientific researchers, and specific skilled professions. Portugal remains an excellent expat lifestyle destination, but the broad territorial tax play no longer exists there.

Paraguay Remains Stable

While other jurisdictions have been retreating from favorable expat tax treatment, Paraguay has maintained its no-CRS, pure territorial tax framework without announced changes. It's currently one of the most stable territorial tax residencies available globally.

How to Set Up Territorial Tax Residency: The Practical Steps

This process is more straightforward than it sounds, but it requires methodical execution. Here's the general framework:

Step 1: Choose Your Country Based on Lifestyle and Tax Goals

The best territorial tax country for you depends on factors beyond the headline tax rate:

- Do you want to actually live there, or just maintain residency while traveling freely?

- What are your income levels? Georgia's 1% SBS is exceptional at $80K–$180K; Paraguay is better for passive income or situations where you need a very low physical presence requirement.

- Do you have dependents? Some programs have generous family extension provisions; others are designed for individuals.

- Do you need a path to citizenship or a second passport? Some territorial countries offer citizenship in 3–5 years of residency.

Step 2: Hire a Local Immigration Lawyer

Every country on this list has a well-developed ecosystem of expat-specialist immigration lawyers. Budget $1,500–$4,000 for legal support. The paperwork requirements — apostilled documents, certified translations, notarizations — are tedious and highly variable by jurisdiction. A qualified local lawyer typically saves weeks of frustration and reduces the risk of costly application errors.

Step 3: Prepare Your Documents Early

Standard requirements across most territorial residency applications include:

- Valid passport (usually with 1+ year of remaining validity)

- Apostilled birth certificate

- FBI background check (apostilled for use in the destination country)

- Proof of income (bank statements, employment letter, tax returns)

- Medical certificate (required by some countries)

- Passport-style photos

Processing the FBI background check takes 3–8 weeks for the standard channel (faster with a third-party channeler). Start this first — it's the most common timeline bottleneck.

Related: digital nomad visa rankings

Step 4: Establish Your FEIE Eligibility Correctly

Moving to a territorial tax country doesn't automatically fix your US taxes. You need to qualify for the FEIE through either the Bona Fide Residence Test (you must be a bona fide resident of a foreign country for an entire tax year) or the Physical Presence Test (330 or more days outside the US in any 12-month period).

Critically: you need to actually change your tax home. Maintaining your primary home in the US while spending time abroad doesn't qualify you. Work with an expat-specialist CPA — not a generalist accountant who does a few international returns — before your first overseas tax year. The cost of that professional guidance is trivial compared to the tax savings at stake.

Step 5: Set Up Your Banking Structure

The three-account structure most expats use:

- US business banking (Mercury is the standard choice for LLC or S-Corp structures) — receives client payments and holds USD reserves

- US personal banking with global ATM access — Charles Schwab International is the gold standard, with unlimited ATM fee reimbursements worldwide and no foreign transaction fees on any withdrawal

- Local bank account in your country of residence — for paying rent, utilities, and local expenses in local currency

For sending larger sums internationally (funding investment accounts, property deposits, moving capital between jurisdictions), Remitly offers competitive rates for common currency corridors. For a comprehensive breakdown of how to move money internationally without losing a significant slice to fees, see our Expat Money Transfer Bible.

What to Watch Out For: The Traps Expats Fall Into

Self-Employment Tax Is Not Eliminated by the FEIE

This is the single most common misconception about expat tax optimization. The FEIE excludes foreign earned income from US income tax, but self-employment tax (Social Security and Medicare, totaling 15.3% on net self-employment income up to approximately $168,600) still applies. For a freelancer earning $120,000, that's potentially $18,000+ in SE tax even after claiming the full FEIE.

The solution: structure your business as an S-Corp (which allows you to take a "reasonable salary" and distribute the rest as dividends not subject to SE tax) or use a properly structured foreign corporation. This is not a DIY project — get professional advice before you go.

Substance Requirements Are Getting Stricter Globally

Tax authorities — both the IRS and foreign governments — are increasingly scrutinizing "paper residencies" where someone claims tax residency in a low-tax country but clearly doesn't actually live there. The FEIE's Bona Fide Residence Test was designed specifically to require real, substantive residency. If you're claiming Panama tax residency while living 300 days a year in New York, you have a serious compliance problem.

Don't Forget State Taxes

Some US states — California, New York, Virginia, and a handful of others — are particularly aggressive about maintaining that you're still a state resident for income tax purposes, even after establishing foreign residency. Before you leave, you need to legally establish domicile elsewhere (typically in a state with no income tax like Texas, Florida, or Nevada, or properly terminate your existing state residency). Set up a virtual mailbox like Traveling Mailbox in your new domicile state to anchor your address for banking and IRS correspondence. Our Complete US Expat Banking and Taxes Guide covers the state tax departure process in detail.

CRS and FATCA: Your Accounts Are Not Invisible

Most territorial tax countries — Panama, Georgia, UAE, Costa Rica, Malaysia — participate in the Common Reporting Standard. This means your local bank accounts will be automatically reported to your country's tax authority. For US citizens, FATCA creates additional reporting requirements on top of CRS: foreign financial accounts over $10,000 aggregate require an annual FBAR filing, and significant foreign holdings trigger Form 8938 on your US tax return. Non-compliance is extraordinarily expensive — FBAR penalties start at $10,000 per unreported account per year for non-willful violations.

Paraguay is unusual in not participating in CRS, but US citizens there are still bound by FBAR and FATCA obligations regardless of where they bank.

The AI Audit Wave Is Coming

Global tax enforcement is entering a new era. The OECD's Crypto-Asset Reporting Framework (CARF) and increasingly sophisticated AI-driven audit tools mean that inconsistencies between your lifestyle (social media, flight records, credit card usage) and your declared tax residency are easier to detect than ever. If your claimed residency doesn't match your actual life pattern, authorities will eventually find it. See our full analysis: The End of Expat Invisibility.

Is Territorial Tax Residency Right for You?

Territorial tax residency is not for everyone. It requires you to actually restructure your life — legally, physically, and logistically — around a different home base. Here's a quick self-assessment:

You're a strong candidate if:

- You earn $60,000 or more per year in location-independent income (remote work, online business, freelancing, foreign investments)

- You're comfortable spending meaningful time abroad — or are excited to live abroad full-time

- You're willing to invest 3–6 months in the setup process (legal, banking, IRS compliance)

- You have the discipline to maintain proper records and work with qualified professionals annually

You're a poor candidate if:

- Your income is primarily US-sourced employment and you plan to live in the US

- You're not willing to physically spend enough time abroad to qualify for the FEIE

- Your earnings are below $40K/year (the savings may not justify the setup complexity)

- You're looking for a way to hide income — this is legal tax optimization through genuine residency change, not evasion

If you're building an online business specifically structured for location independence, see our guide to building a $100K/year online business from anywhere — it covers the business structures that pair best with expat tax strategies.

For those considering Latin America as a base, it's worth noting that while Colombia itself isn't a territorial tax system (it taxes residents on worldwide income after 5 years of residency), many expats use it as a lifestyle hub while maintaining legal tax residency in Paraguay or Panama. If you want to understand what life in Colombia actually looks like for an American, ColombiaMove.com's guide to moving to Colombia is the most detailed resource available. The Medellín cost of living breakdown is particularly useful for modeling what your dollars actually buy.

For tracking crypto gains across multiple jurisdictions — a genuine complexity for expats with digital asset holdings — CoinTracking handles multi-country cost basis tracking and generates reports compatible with both US and local tax filings. The full picture of crypto obligations for US expats is in our dedicated guide: Crypto and Taxes as a US Expat.

The Bottom Line

Territorial taxation isn't a loophole. It's a sovereign nation's deliberate choice about how to structure its economy. Paraguay, Panama, Georgia, the UAE, and dozens of other countries have decided — as a matter of considered national policy — that income you earn from outside their borders is yours to keep. They want your presence, your local spending, and your economic participation. They're not trying to tax income they had no role in creating.

The math is unambiguous: a US expat earning $120,000/year can move from a $22,000+ annual tax bill to $2,000–$5,000 through a combination of territorial residency and the FEIE. Over a decade, that's $170,000–$200,000 in additional compounding capital that stays in your hands instead of disappearing into government coffers. Invested at even a modest 7% return, that extra $20,000/year compounds to over $276,000 in additional wealth over 10 years.

The setup takes 3–6 months, costs $2,000–$7,000 in legal and administrative fees depending on the country, and requires working with a qualified expat CPA for as long as you maintain the structure. That's a one-time investment that pays itself back in the first year, then continues paying every year thereafter.

The only people not taking advantage of this are people who don't know it exists — or people who've consciously decided that the convenience of staying put is worth $20,000 or more per year. That's a perfectly valid choice. It just needs to be a conscious one.

Financial Disclaimer: This article is for informational and educational purposes only and does not constitute tax, legal, or financial advice. Tax laws are complex, vary significantly by individual circumstances, and change frequently. Every reader's situation is different. Always consult a qualified expat CPA or international tax attorney before making decisions about your tax residency, business structure, or financial accounts. US citizens are subject to worldwide income reporting requirements regardless of where they live, including FBAR and FATCA obligations. Non-compliance with these reporting requirements can result in severe civil and criminal penalties. Nothing in this article should be construed as encouraging tax evasion or illegal activity.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJuly 4, 2026

Expat Tax & FinanceJuly 4, 2026

Canadian TFSA and US Taxes: The Reporting Trap

US citizens holding a Canadian TFSA owe tax on all annual growth and must file Form 3520 — PFIC rules apply to Canadian mutual funds inside the

Expat Tax & FinanceJuly 4, 2026

Expat Tax & FinanceJuly 4, 2026

State Income Tax for Expats: Which States Follow You

California, New York, and Virginia keep taxing Americans abroad. Learn which states follow you, what triggers audits, and how to exit cleanly.

Expat Tax & FinanceJuly 3, 2026

Expat Tax & FinanceJuly 3, 2026

FBAR: The $10,000 Expat Rule Most People Get Wrong

FBAR: when any foreign account aggregate hits $10,000 during the year, all accounts must be reported. Penalties, Bittner ruling, and catch-up