The Five-Flag Strategy: Pay Zero Tax Legally as an Expat

The five-flag strategy lets expats legally pay near-zero tax by splitting residency, business, banking, assets, and citizenship across multiple countries.

The five-flag strategy lets expats legally pay near-zero tax by splitting residency, business, banking, assets, and citizenship across multiple countries.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

A business owner earning $500,000 a year in Germany pays roughly $225,000 in taxes. The same person, after properly implementing the Five-Flag Strategy, can pay close to zero — legally, transparently, and with full disclosure to the relevant tax authorities. The setup costs around $220,000 upfront. It pays for itself in under 18 months. Over a decade, the savings top $2 million.

That's not a fantasy sold by offshore shysters. It's a strategy with a 50-year history, developed by serious financial thinkers, refined by generations of expats, and still fully viable in 2025 — with important caveats. The most important caveat, which we'll come back to repeatedly: if you're a US citizen, the rules are fundamentally different. The Five-Flag Strategy still works for Americans, but the mechanism is different, and the path is harder.

Here's everything you need to know about flag theory — what it is, what each flag does, what it actually costs, and whether it makes sense for you.

Related: territorial tax countries guide

What Is Flag Theory and Where Did It Come From?

The concept traces back to Harry Schultz, an American investment newsletter writer who in the 1970s wrote about what he called the "Three Flags Theory." His insight was simple but radical: you could legally reduce your tax exposure by spreading three key aspects of your life across three different countries — your citizenship, your tax domicile, and your money.

The concept was expanded by W.G. Hill (a pen name used by the UK-based publisher Scope International) in a series of books in the 1980s and 1990s. Hill fleshed out the five-flag framework that most people use today and coined the term "Flag Theory" itself. He also popularized the idea of the Perpetual Traveler (PT) — a person who, by keeping different life aspects in different countries, becomes a "guest everywhere, citizen of nowhere," with no single government holding complete jurisdiction over their economic life.

Modern advisory firms like Nomad Capitalist have since expanded the framework to six or even seven flags, adding digital presence and crypto/digital asset management as separate jurisdictional considerations. But the core five-flag structure remains the foundation of any serious international tax strategy.

The philosophical basis is this: governments claim the right to tax you based on where you live, where you work, and where you're a citizen. By strategically placing each of these in the most favorable jurisdiction, you can dramatically reduce — sometimes eliminate — your overall tax burden. The key word is strategically. This is not tax evasion. Every element is disclosed, legally structured, and maintained in full compliance.

The Five Flags, Explained

Each "flag" represents a specific aspect of your life that you deliberately plant in the most advantageous country:

| Flag | What It Controls | The Goal |

|---|---|---|

| Flag 1: Citizenship/Passport | Your legal nationality and travel document | A passport from a country that taxes on territorial or residence basis only — not worldwide |

| Flag 2: Tax Residency | Where you are legally considered a tax resident | A territorial tax country where foreign-sourced income is completely exempt |

| Flag 3: Business Base | Where your company is incorporated | A low or zero corporate tax jurisdiction with minimal operating restrictions |

| Flag 4: Asset Haven | Where your banking and investments are held | A stable, politically neutral jurisdiction with strong asset protection and zero capital gains tax |

| Flag 5: Lifestyle Playground | Where you actually live and spend time | Countries with high quality of life, low cost, and minimal consumption taxes |

The power comes from combining all five. Each flag on its own offers modest benefits. Together, they create a structure where income flows through a zero-tax business, gets sheltered in an asset-protection jurisdiction, while you live comfortably under a favorable tax residency — all while holding a passport that doesn't impose worldwide taxation on you.

Flag 1: Citizenship and the Second Passport

The passport you're born with determines your baseline tax situation. American and Eritrean citizens face worldwide taxation no matter where they live. Citizens of most other countries only get taxed where they're resident — and they can escape their home country's tax net by simply moving.

For Americans, getting a second passport from a territorial-tax country is the first step toward eventually exiting the US tax system entirely (through renunciation). For everyone else, getting a second passport is about optionality — travel access, banking options, and a backup plan.

The fastest and most accessible second passports come from Caribbean Citizenship by Investment (CBI) programs:

| Country | Minimum Investment | Processing Time | Visa-Free Access | Notes |

|---|---|---|---|---|

| Vanuatu | ~$130,000 donation | 1–2 months | 95+ countries | Fastest globally; fully remote process |

| Dominica | $200,000 donation | 3–6 months | 140+ countries | Cheapest Caribbean option |

| Grenada | $235,000 donation | 3–4 months | 140+ countries | Only Caribbean passport eligible for US E-2 visa |

| St. Kitts & Nevis | $250,000 donation | 45–60 days | 155+ countries | Oldest CBI program (1984) |

| Malta | €600,000+ | 12–36 months | 185+ countries (EU) | The gold standard; full EU citizenship |

| Paraguay | ~$5,000 legal fees | 3–5 years residency then citizenship | 140+ countries | Cheapest natural path to citizenship |

The Caribbean CBI programs are the fastest route — you donate to a government fund or buy approved real estate, and you get a full passport with no residency requirement. They're not cheap, but for someone earning $500K+ in a 45% tax country, the math is obvious. A $200,000 passport investment that reduces your annual tax bill by $200,000 is a one-year payback.

For non-Americans, getting the passport and the tax residency in the same country (like Paraguay or Panama) is often the most efficient approach — two flags in one move.

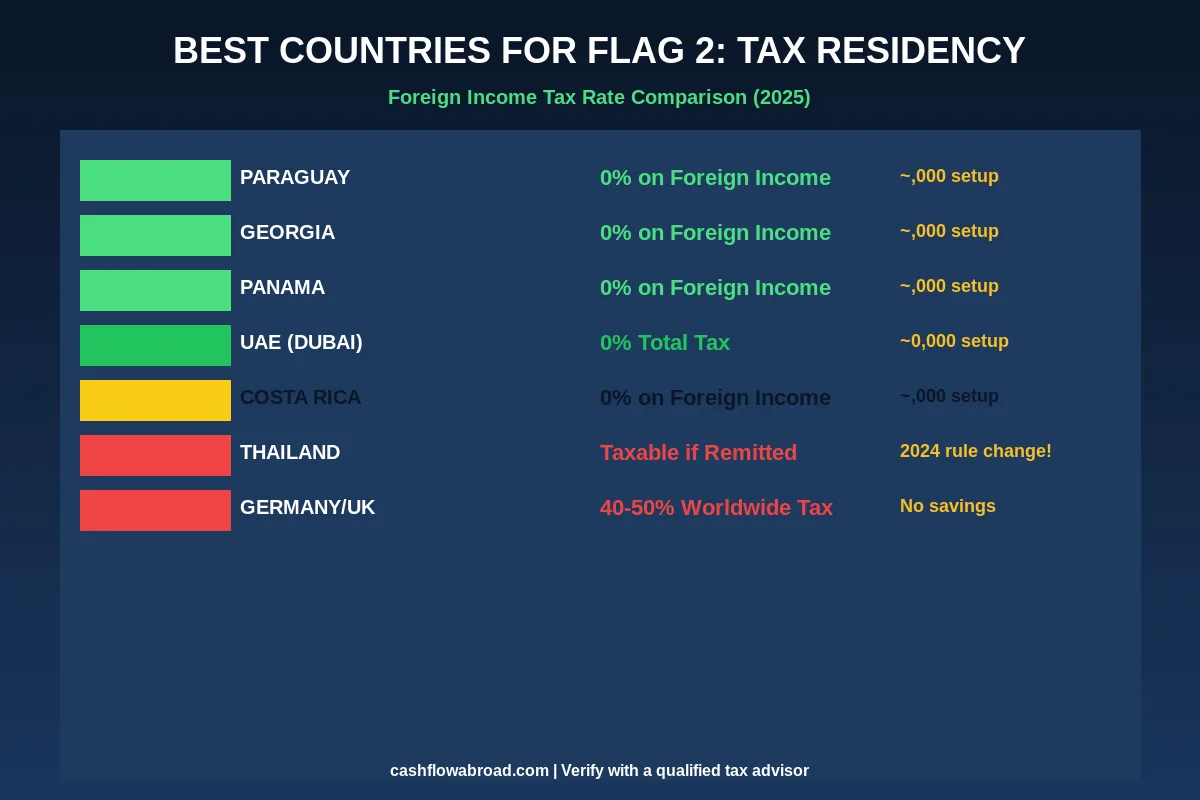

Flag 2: Establishing Tax Residency in a Territorial Tax Country

This is arguably the most important flag of all. Territorial taxation means a country only taxes income earned within its borders. If you run an online business, consult for foreign clients, or earn investment income from overseas — all of it can be completely exempt from local tax.

Here are the strongest territorial tax jurisdictions available to expats today:

Paraguay: The Hidden Gem

Paraguay stands out as the most underrated option. The country only taxes income earned within Paraguay — foreign income is completely exempt, no matter what. Residency requires approximately one day per year to maintain, and the entire setup costs roughly $2,000–$5,000 in legal fees. Corporate tax on local income is just 10% flat. This is why Paraguay has become the preferred option for online entrepreneurs and investors who want a simple, cheap, low-drama tax residency. You can check out our deep-dive on the Geographic Arbitrage Playbook for more on LATAM options.

Related: FEIE zero tax guide

Georgia: 1% Tax for Small Business Owners

Georgia (the country, not the US state) offers something extraordinary: a "Small Business Status" that allows qualifying entrepreneurs to pay just 1% tax on turnover up to roughly GEL 500,000 (~$185,000). Foreign income is completely exempt from Georgian tax. Residency requires 183+ days per year. Tbilisi offers an exceptionally high quality of life at $800–$1,500/month all-in, and banking at TBC Bank or Bank of Georgia is straightforward to establish without high minimums.

Panama: The Classic

Panama has been the flagship territorial tax destination for decades. The Friendly Nations Visa — available to citizens of about 50 countries — allows you to establish residency quickly with approximately $5,000 in a Panamanian bank account plus legal fees of $2,000–$3,000. Panama City has excellent infrastructure, strong rule of law by regional standards, a dollarized economy, and a sophisticated financial sector. It's pricier than Georgia or Paraguay, but it's more established and has better banking infrastructure.

For those interested in Panama's neighbor and a broader LATAM comparison, ColombiaMove.com has an excellent guide to Colombia's own residency and banking options — Colombia is not a territorial tax country, but it offers remarkable cost-of-living arbitrage for those who've already established their tax residency elsewhere.

UAE (Dubai): Zero Everything

Dubai is the nuclear option. There is zero personal income tax on all income — foreign or domestic. There's a 9% corporate tax introduced in 2023, but it only kicks in on profits above AED 375,000 (~$102,000) from mainland UAE operations. Free zone businesses remain exempt for qualifying activities. The cost to establish UAE residency via a freelancer visa or free zone company runs $3,500–$15,000. No minimum days required to maintain residency (though you must use your visa). The trade-off: Dubai itself is expensive to live in — a comfortable lifestyle runs $4,000–$7,000/month.

Thailand: A Warning

Thailand used to be a favorite for digital nomads and retirees as a de facto territorial tax country — foreign income brought into Thailand in a later year was tax-exempt. In 2024, that changed. The Thai Revenue Department now taxes foreign income remitted to Thailand regardless of when it was earned. This blindsided thousands of expats who had structured their finances around the old rules. Thailand is worth watching, but it's no longer the reliable territorial haven it once was.

Flag 3: Where to Incorporate Your Business

If you run any kind of business — consulting, e-commerce, SaaS, content, trading — the country where it's incorporated determines how much corporate tax you pay. Most successful flag theorists incorporate in a zero-tax offshore jurisdiction while maintaining tax residency in a territorial country.

| Jurisdiction | Corporate Tax | Setup Cost | Annual Maintenance | Best For |

|---|---|---|---|---|

| BVI (British Virgin Islands) | 0% | $1,500–$3,000 | $800–$1,500/yr | Most popular; general business, holding companies |

| Cayman Islands | 0% | $3,000–$6,000 | $2,000–$4,000/yr | Investment funds, financial structures |

| UAE Free Zones | 0% (qualifying) | $3,500–$15,000 | $3,000–$8,000/yr | Includes UAE residency visa; physical presence available |

| Estonia e-Residency | 0% retained / 20% distributed | ~€200 card | €1,000–€2,000/yr | EU-based operations; 33,000+ companies formed since 2014 |

| Singapore | 17% (exemptions for startups) | $2,000–$5,000 | $2,000–$4,000/yr | Asia-Pacific operations; prestigious; strong treaty network |

| Paraguay | 10% (local income only) | $1,500–$3,000 | $500–$1,500/yr | Cheapest option for those with Paraguay residency |

The BVI remains the most popular offshore incorporation destination globally, with hundreds of thousands of active companies. The key advantage is confidentiality and flexibility. The key watch-out: since 2018, economic substance rules require that offshore companies demonstrate genuine business activity in their jurisdiction — local employees, locally-made decisions, actual operations. Pure shell companies with no local activity increasingly face scrutiny and reclassification by tax authorities. This is the OECD's response to the era of empty offshore structures.

Estonia's e-Residency program is worth a mention for the tech-savvy: 120,000+ entrepreneurs from 170+ countries have used it to set up EU-based companies entirely online. You don't need to live in Estonia. Tax is deferred as long as profits stay in the company — only 20% when you distribute dividends. For online businesses that can reinvest earnings, this is an elegant structure.

If you're running an online business from anywhere in the world, you'll want solid US banking access for your company. Mercury is the go-to banking solution for remote business owners — it's a US-based fintech that handles international founders, offers free business checking, and plays well with offshore corporate structures.

Flag 4: Banking and Asset Protection

Where you hold your money matters as much as where you earn it. The fourth flag is about placing your banking, investments, and assets in a jurisdiction with three qualities: political stability, zero capital gains tax, and strong asset protection laws.

The era of true banking secrecy is effectively over. The OECD's Common Reporting Standard (CRS) — now adopted by over 100 countries — requires banks to automatically report account information of foreign nationals to their home tax authorities. Switzerland, Singapore, UAE, and most traditional banking havens now share data under CRS. The days of hiding money offshore are gone. But tax-efficient asset structuring and protection are very much alive.

Jurisdictions with zero capital gains tax:

- UAE: 0% capital gains on all asset types

- Singapore: 0% capital gains (on most assets; not professional traders)

- Cayman Islands: 0% on everything

- BVI: 0% on everything

- Panama: 0% on foreign-sourced gains

- New Zealand: 0% (currently — under political debate)

- Switzerland: 0% capital gains on private assets (not professional traders)

- Hong Kong: 0% capital gains

For practical banking as an expat investor, Charles Schwab International remains one of the best-kept secrets in the space. It offers a brokerage and checking account combo with zero foreign transaction fees, free ATM withdrawals worldwide, and full access to the Schwab brokerage platform including international ETFs and US securities. For someone managing assets across multiple flag jurisdictions, this is a practical backbone for the portfolio layer.

For Latin American residents operating in Colombia, Mexico, Argentina, or Brazil, ARQ Finance fills an interesting niche — it holds balances in USDc/EURc stablecoins, lets you swap to local currencies (MXN/COP/ARS/BRL), earn up to 4% on dollar balances, and comes with a Mastercard. It's not a bank, but for LATAM-based expats who need reliable dollar access without traditional banking friction, it's a legitimate tool worth knowing.

Related: second passport guide

Flag 5: Where You Actually Live (The Lifestyle Flag)

The fifth flag is where you spend your time — your home base, your travel circuits, your day-to-day life. The goal here is maximizing quality of life per dollar spent while staying compliant with your Flag 2 tax residency (which may require a minimum number of days in-country per year).

The most practical Flag 5 locations share these characteristics: low cost of living, high quality of life, low or no VAT/sales tax, and no income tax on foreign-sourced earnings (even if they're not your formal tax residency). Some top picks:

- Tbilisi, Georgia: $800–$1,500/month comfortable living. Vibrant expat scene. Fast internet. Excellent food and wine. Combined Flag 2 + Flag 5 option — possibly the best single-country two-flag play available.

- Asuncion, Paraguay: One of the cheapest capitals in the Americas. Simple life. No drama. Strong combined Flag 2 + Flag 5 play for those who prioritize savings over sophistication.

- Panama City: Higher cost (~$2,500–$4,000/month), but excellent infrastructure, first-world healthcare, and Tocumen airport makes it one of the most connected cities in Latin America.

- Bali, Indonesia: The Instagram favorite. ~$1,200–$2,000/month for a genuinely excellent lifestyle. Indonesia's new Digital Nomad Visa offers tax-free foreign income for up to 5 years.

- Medellin, Colombia: The most talked-about geographic arbitrage city in the world. $1,500–$2,500/month buys a genuinely premium lifestyle. Not a territorial tax country, but an excellent Flag 5 lifestyle hub for those with their tax residency established elsewhere. See the full Medellin monthly budget breakdown at ColombiaMove.com.

- Dubai: Combines Flag 2 (zero tax) and Flag 5 (luxury lifestyle), but expensive — budget $5,000–$10,000/month for genuine comfort.

Our full Geographic Arbitrage Playbook covers 10 countries where $2,000/month gets you a $6,000/month lifestyle — essential reading for Flag 5 planning.

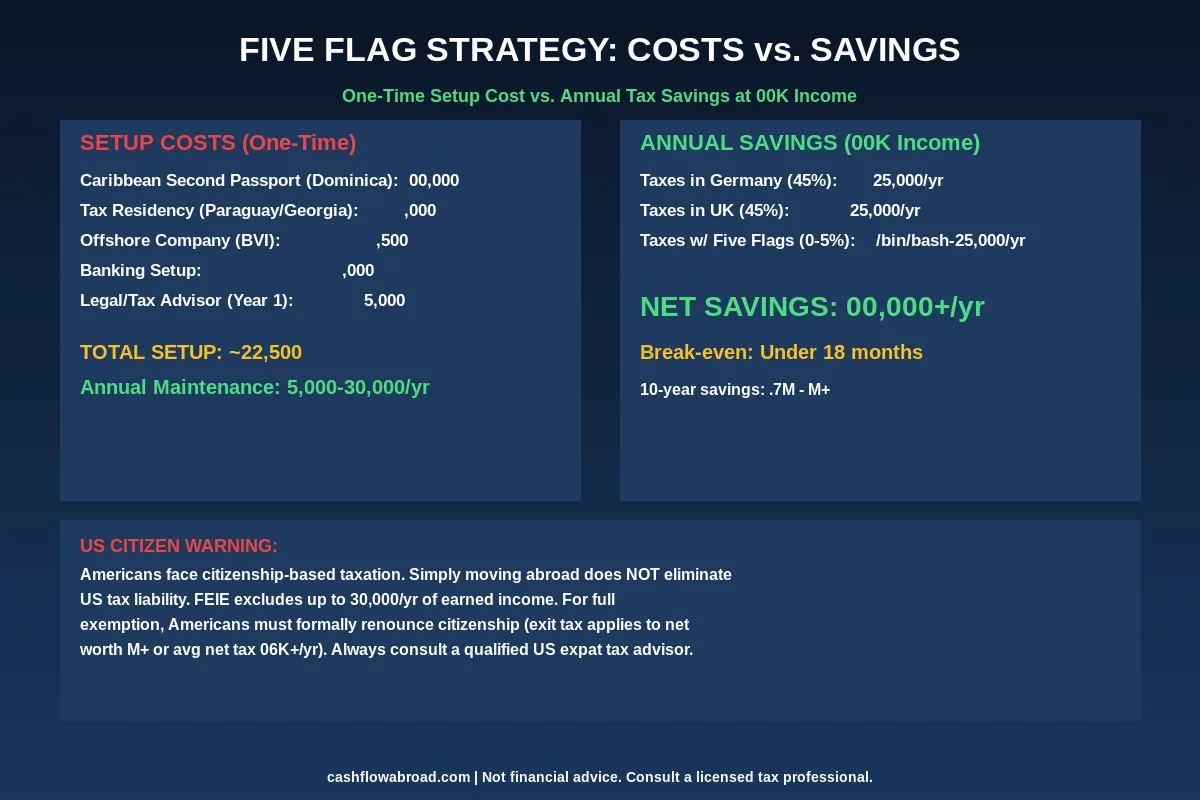

What Does It Actually Cost, and How Much Do You Save?

Let's run the real numbers. Here's what a mid-range Five Flag setup looks like:

| Component | One-Time Cost | Annual Maintenance |

|---|---|---|

| Caribbean second passport (Dominica) | $200,000 | ~$36/yr (renewal every 10 years) |

| Tax residency setup (Paraguay or Georgia) | $2,000–$5,000 | $1,000–$3,000/yr compliance |

| Offshore company (BVI) | $1,500–$3,000 | $800–$1,500/yr |

| Banking setup | $0–$5,000 | $0–$2,000/yr |

| Legal and tax advisor (Year 1) | $10,000–$20,000 | $5,000–$20,000/yr ongoing |

| Total (mid-range) | ~$215,000–$235,000 | ~$10,000–$30,000/yr |

Now the savings for someone earning $500,000/year in a 45% tax country (UK or Germany):

- Current annual tax bill: $225,000/year

- After Five Flag setup: $0–$25,000/year (depending on structure)

- Net annual savings: $200,000+/year

- Break-even: 13–18 months

- 10-year net benefit (after ongoing compliance costs): $1.7 million to $2 million

The break-even math improves dramatically for lower-cost residency options. Skip the CBI passport and instead pursue residency in Paraguay or Georgia through normal channels ($3,000–$5,000 in legal fees), and your entire setup cost drops to $20,000–$30,000. For a $300,000/year earner in a 40% tax country, that's a 2–3 month payback period. One of the fastest financial decisions you'll ever make.

The US Citizen Problem: Why This Is Different for Americans

Here's the section most flag theory guides bury or gloss over. If you hold a US passport, the Five Flag Strategy works differently for you — and in some ways, significantly harder.

The United States is one of only two countries in the world (the other is Eritrea) that taxes its citizens on worldwide income regardless of where they live. Moving to Panama, Georgia, or Dubai does not eliminate your US tax liability. You remain a US taxpayer as long as you hold US citizenship.

What US expats can legitimately do:

- Foreign Earned Income Exclusion (FEIE): Excludes up to $130,000 of earned income (wages, self-employment) from US tax in 2025. Requires 330+ days outside the US per year (Physical Presence Test) or bona fide foreign residence (Bona Fide Residence Test). Critically, the FEIE does not cover passive income — dividends, capital gains, rental income, and interest are still fully taxable to Americans regardless of where they live.

- Foreign Tax Credit (FTC): Credits taxes paid to foreign governments against your US tax bill. Highly useful if you're living in a high-tax country like Germany (which taxes income at ~45%). Essentially worthless if you're in UAE or Paraguay, because there's no foreign tax to credit — your US bill remains in full.

- Foreign Housing Exclusion: Additional exclusion for housing costs above a base amount; varies by city. Useful in expensive expat hubs like Singapore or Zurich.

Americans also face two compliance requirements with teeth: FBAR (FinCEN Form 114) and FATCA (Form 8938). FBAR is required if your combined foreign account balances exceed $10,000 at any point during the year — and penalties for willful non-filing run up to 50% of account balance per account per year, plus potential criminal charges with up to 5 years imprisonment. FATCA penalties start at $10,000 for failure to file, with up to $50,000 in additional penalties for continued non-filing.

Our comprehensive guide to US expat banking, FBAR, FATCA, and FEIE is required reading before you open any foreign account.

For US citizens, the Five Flag Strategy's primary legitimate benefits are: business structure efficiency up to the FEIE limit, asset protection diversification, banking resilience, lifestyle optimization, and building the infrastructure for eventual renunciation if and when it makes financial sense.

The Nuclear Option: Renouncing US Citizenship

For high earners, formal renunciation of US citizenship is the only way to fully exit US worldwide taxation. The mechanics in 2025:

- Renunciation fee: $2,350 at a US consulate abroad (up from $450 before 2014 — a 422% increase)

- Exit tax: The IRS treats you as having sold all worldwide assets on the day before renunciation. All unrealized gains are deemed realized and taxed.

- "Covered expatriate" thresholds (2025): Full exit tax applies if your average annual net income tax for the prior 5 years exceeds $206,000, OR your net worth is $2 million or more, OR you failed to certify 5 years of full tax compliance.

- Exit tax exclusion (2025): First $890,000 of deemed gains is excluded. Gains above that are taxed at capital gains rates.

- After renunciation: No more FBAR, no more FATCA, no more worldwide taxation. The Five Flag Strategy then works in full.

Renunciation records hit approximately 5,315 in the first half of 2023 alone — a near-record pace that reflects growing awareness of citizenship-based taxation and its consequences. This is a significant, irreversible decision that requires careful legal planning, but for the right individual, it's the move that makes the full flag theory math work.

Related: cheapest countries guide

For a complete breakdown of your options as an American expat, see our detailed guide on how to legally pay zero federal income tax as a US expat.

What's Changed: 2024–2025 Enforcement Trends

The landscape for international tax planning has shifted significantly. Anyone entering this space needs to understand these developments:

The Death of Banking Secrecy

The OECD's Common Reporting Standard is now operational in 100+ countries. Banks in Switzerland, Singapore, UAE, Cayman, BVI, and essentially everywhere that matters now automatically report account holder information to the account holder's home tax authority. Banking secrecy as practiced in the 20th century is functionally dead. This doesn't make the strategy illegal — it makes it transparent. Everything must be disclosed and properly filed. That's not a bug; it's the feature. The Five Flag Strategy has always been about legal optimization, not hiding.

Economic Substance Rules

BVI, Cayman Islands, Bahamas, and other offshore centers now require companies to demonstrate real economic activity locally — local employees, directors actually making decisions locally, genuine operations. Post-2018, the shell company era is effectively over. A BVI company with no actual activities in the BVI increasingly faces reclassification by tax authorities using "look-through" rules. Your offshore structure needs genuine substance.

UK Non-Dom Abolition (April 2025)

The UK's non-domicile tax status — which had allowed wealthy foreign residents to avoid UK tax on overseas income — was substantially curtailed in April 2025. This disrupted thousands of high-net-worth individuals based in London and has accelerated the migration of wealthy individuals to Dubai, Switzerland, and other lower-tax jurisdictions. It's one of the most dramatic flag theory driving events in years.

Thailand's 2024 Rule Change

Worth repeating: Thailand's 2024 change — taxing foreign income remitted to Thailand regardless of which year it was earned — caught thousands of expats off guard. This is a perfect example of how territorial tax regimes can change without warning, and why annual monitoring of your residency country's rules is non-negotiable. We covered the broader data-sharing enforcement trend in our post on AI audits, CARF, and global data sharing.

Common Mistakes That Will Wreck Your Strategy

The Five Flag Strategy fails — sometimes catastrophically — when people cut corners. Here are the most common ways it goes wrong:

- Thinking the 183-day rule is the only test. Many countries use "center of life" or "habitual abode" tests. If your family stays in Germany while you "live" in Paraguay, German tax authorities may deem you still resident. Physical presence must be genuine and well-documented.

- Not disclosing offshore accounts. With CRS and FATCA operating globally, the probability of detection for undisclosed foreign accounts is higher than it's ever been. The penalties are criminal-level severe. This isn't a risk to take.

- Forgetting US state taxes. California, New York, Virginia, and South Carolina aggressively assert continuing state tax residency even after you physically move abroad. California in particular requires documented, formal departure with severed domicile ties. Moving internationally while your family and home remain in California does not solve the California tax problem. Establish domicile in a no-tax state and use a virtual mailbox like Traveling Mailbox (from $15/month) for banking and IRS correspondence at a real street address.

- Building a shell company with no substance. Post-2018 economic substance rules require that offshore companies have real local operations, or they risk being disregarded for tax purposes by multiple jurisdictions simultaneously.

- Underestimating compliance costs. A properly maintained multi-jurisdictional structure costs $10,000–$30,000/year in legal and accounting fees. The strategy only makes financial sense above roughly $200,000–$300,000/year in income. Below that, the compliance tail wags the strategy dog.

- Choosing Thailand for tax residency post-2024. The rule change makes it an unreliable choice until the regulatory environment stabilizes.

- Getting de-banked. Many traditional banks refuse to service accounts connected to offshore structures. Use specialist providers — international banks, fintech-forward institutions, offshore-friendly banks — from the start, not as an afterthought.

- Confusing legal optimization with tax evasion. The strategy is entirely legal when properly structured and disclosed. The moment you hide assets or fail to file required forms, you're committing a crime, not doing tax planning.

Is the Five-Flag Strategy Worth It?

For the right person, the answer is clearly yes. The break-even math on a properly structured Five Flag setup is compelling for anyone earning $300,000+ in a high-tax jurisdiction. Over 10 years, the wealth preservation difference between a 45% tax regime and a near-zero one can easily exceed $2 million.

For digital entrepreneurs, consultants, investors, and remote workers with genuine geographic flexibility, the strategy is more accessible than it's ever been. Paraguay and Georgia offer residency for under $5,000 in legal fees — no $200,000 passport required. Combined with an offshore company structure and the right banking setup, you can be operational within a few months.

For US citizens, the path is harder but not closed. The FEIE protects the first $130,000 of earned income. Building the infrastructure now — second passport, offshore company, proper banking — positions you for the eventual renunciation decision if and when it makes financial sense. And if you're planning to hold significant investment assets abroad, the combination of PFIC-compliant investment strategies with a properly structured offshore holding company can mean the difference between genuine wealth accumulation and watching gains taxed away at punitive rates.

For international money movement throughout any of this, Remitly gives you transparent exchange rates and no hidden markup fees — useful when you're regularly moving money between multiple flag jurisdictions.

And wherever you plant your flags, keep your health covered. SafetyWing's Nomad Insurance starts at approximately $45/month and provides global coverage — practical for the early stages of building your flag structure before you settle into a full expat health plan.

The Bottom Line

Flag theory is not a gimmick, a loophole, or a conspiracy. It's a 50-year-old framework for legally optimizing your relationship with multiple tax systems by taking geographic freedom seriously. Wealthy individuals and international business owners have used it quietly for decades. The internet and remote work explosion have made it accessible to a vastly larger group of people.

The strategy works best for: high-income earners in high-tax countries who have genuine location flexibility; online entrepreneurs with international clients; serious investors seeking both asset protection and tax efficiency; and US citizens planning a long-term exit from citizenship-based taxation.

It requires real commitment: actual physical residency in your chosen country, genuine corporate substance in your offshore entity, real banking relationships, and ongoing compliance with multiple jurisdictions. Done right, it's one of the highest-ROI financial decisions you can make over a 10-year horizon. Done wrong — especially by Americans who think simply moving to Dubai eliminates their US tax bill — it's expensive and potentially criminal.

Get qualified advice. Use specialists who understand multi-jurisdictional tax structures. Move deliberately. The flags you plant today determine the tax map you'll live under for the next decade.

Financial Disclaimer: This article is for informational and educational purposes only and does not constitute legal, tax, or financial advice. Tax laws vary significantly by jurisdiction and change frequently. The strategies discussed involve complex legal and regulatory considerations that differ based on your individual circumstances, citizenship, residency, and income sources. Always consult with a qualified international tax attorney and certified public accountant before making any decisions related to offshore structures, citizenship, residency changes, or tax planning. Nothing in this post should be construed as a recommendation to take any specific action.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageJune 30, 2026

Geographic ArbitrageJune 30, 2026

Moving Abroad with Kids: School Costs and Family Budget

International school fees change the whole geographic arbitrage math for families. Compare real costs in Medellín, Chiang Mai, Mexico, and Lisbon for

Geographic ArbitrageJune 29, 2026

Geographic ArbitrageJune 29, 2026

Bali for US Expats: Monthly Costs and Permit Guide

How much Bali costs, which Indonesian stay permit suits long-term stays, and what US citizens owe the IRS while living there in 2025.

Geographic ArbitrageJune 26, 2026

Geographic ArbitrageJune 26, 2026

Colombia Type V Visa: The Remote Worker's Guide

Colombia's Type V digital nomad visa requires ~$1,400/month foreign income, $315 in fees, and 2–6 weeks processing. Step-by-step application guide for