US Tax Treaties: Why the Fine Print Kills Most Expat Benefits

The US has income tax treaties with more than 70 countries. This isn't a fringe technicality. This is the core quirk of US citizenship-based taxation.

The US has income tax treaties with more than 70 countries. This isn't a fringe technicality. This is the core quirk of US citizenship-based taxation.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

The US has income tax treaties with more than 70 countries. Most of those treaties include a single paragraph — usually buried in Article 1 — that quietly makes the entire agreement nearly worthless for American citizens living abroad. It's called the saving clause, and if you've been counting on a tax treaty to protect your income overseas, you need to read this first.

This isn't a fringe technicality. Tax professionals who specialize in expat returns consistently rank the saving clause as the single most misunderstood aspect of US international taxation. The consequences of getting it wrong — filing incorrectly, relying on treaty benefits you're not entitled to, or missing Form 8833 entirely — range from audit triggers to substantial penalties.

The Saving Clause: The Fine Print That Changes Everything

Here's what the saving clause says, in plain English: the United States reserves the right to tax its own citizens as if the treaty never existed.

That one sentence effectively neutralizes most of what's in a US tax treaty for American citizens abroad. While a German resident living in the US can use the US-Germany treaty to reduce withholding taxes and avoid double taxation, a US citizen living in Germany often cannot — because the saving clause lets the IRS treat them as a fully taxable American regardless of what the treaty says.

This is the core quirk of US citizenship-based taxation. The US is one of only two countries in the world (the other being Eritrea) that taxes based on citizenship rather than residence. You pay US taxes whether you live in Dallas or Dubai, Berlin or Bogotá. The saving clause is what enforces that system, and every comprehensive US tax treaty contains one.

What Treaty Benefits Actually Survive for US Citizens

Not everything is lost. Most treaties contain carve-outs — exceptions to the saving clause — that allow US citizens abroad to use certain provisions. These carve-outs vary by treaty and are rarely discussed in general expat tax guides.

The most consistently useful exceptions include:

- Foreign pension income: Many treaties exempt foreign pension benefits from US taxation. The US-Canada treaty specifies that Canadian Pension Plan and Old Age Security benefits are taxed only by Canada — meaning the US can't touch them for US citizens living there.

- Social security equivalents: Cross-border totalization agreements (separate from income tax treaties but often paired with them) prevent double taxation on social security contributions. The US has 30+ totalization agreements covering major destinations including Germany, France, Japan, Ireland, Australia, and Canada.

- Government employment income: US government employees abroad can often claim treaty benefits on specific income categories.

- Students and researchers: Short-term scholars and students are frequently carved out of the saving clause entirely, getting full treaty protection.

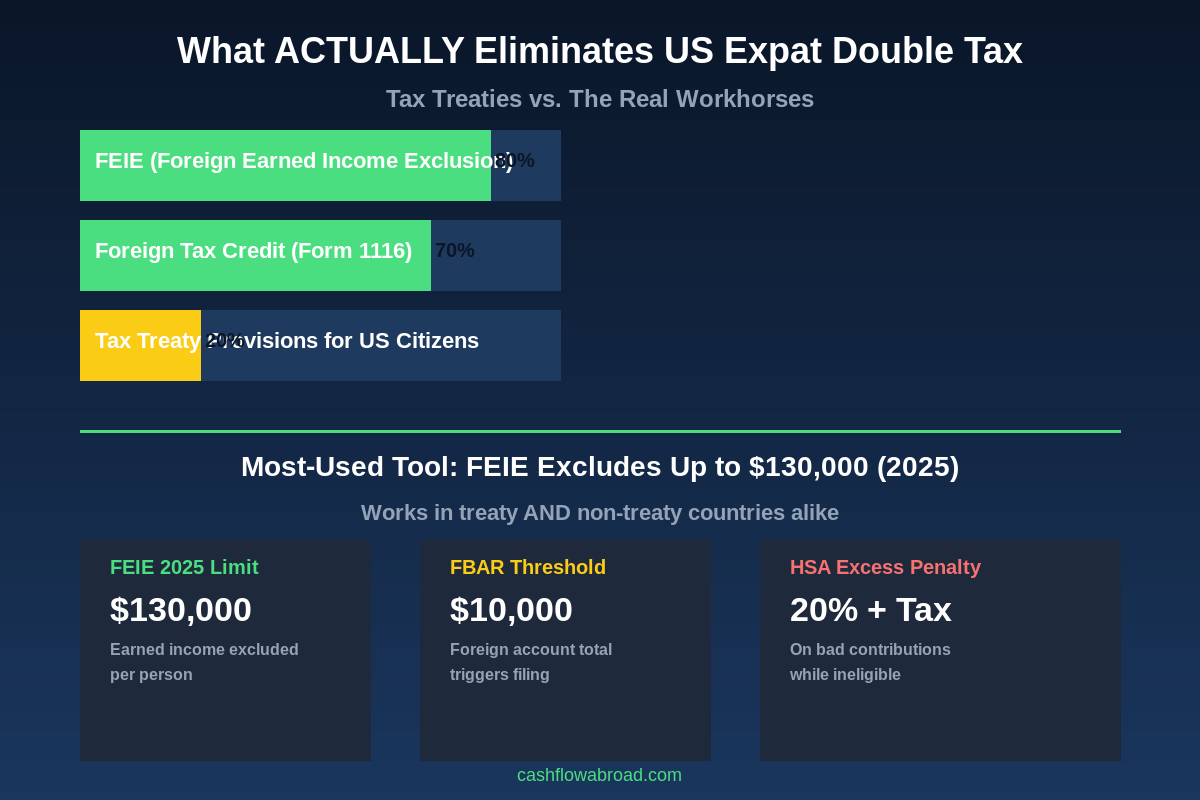

For most working expats, those carve-outs are limited. The real tax-elimination tools aren't in the treaties at all.

FEIE and the Foreign Tax Credit: The Actual Workhorses

Two provisions in the US tax code do far more to eliminate double taxation than any treaty — and neither one requires a treaty to work.

The Foreign Earned Income Exclusion (FEIE) lets you exclude up to $130,000 of foreign earned income from US taxes in 2025 (up from $126,500 in 2024, rising with inflation annually). You qualify by passing either the bona fide residence test (you're a legal resident of a foreign country) or the physical presence test (you're outside the US at least 330 days in any 12-month period).

The FEIE works in every country on earth — treaty or not. Whether you're in the UAE (no treaty) or Germany (comprehensive treaty), the exclusion applies the same way.

The Foreign Tax Credit (FTC) gives you a dollar-for-dollar credit against your US tax bill for taxes paid to foreign governments. If you pay 25% income tax in Germany, you get a $0.25 US credit per dollar of foreign-taxed income. In high-tax countries, this effectively eliminates your US tax liability entirely — often more completely than any treaty provision would.

One critical note: you can't use both FEIE and FTC on the same income. You choose one or the other per dollar of foreign earned income. For low-tax or zero-tax countries, FEIE usually wins. For high-tax countries like Germany, France, or Canada, the FTC often makes more sense. The math gets complicated fast — run your numbers with a qualified expat CPA before filing. The zero-federal-tax expat guide covers the choice in more detail.

Treaty Countries vs. No-Treaty Hotspots: The Full Picture

Here's the counterintuitive part: many of the most popular expat destinations for Americans have no US income tax treaty at all. And yet tens of thousands of Americans move to these countries every year without any meaningful tax disadvantage compared to treaty countries.

| Country | US Treaty? | Local Income Tax | FEIE Applies? | Monthly Budget (USD) |

|---|---|---|---|---|

| UAE / Dubai | No | 0% | Yes | $3,000–$6,000 |

| Panama | No | 0–20% (local income only) | Yes | $1,500–$2,500 |

| Costa Rica | No | 0–25% (local income only) | Yes | $1,400–$2,000 |

| Thailand | No | 5–35% (foreign income if remitted) | Yes | $1,000–$1,800 |

| Singapore | No | 0–24% | Yes | $4,000–$6,000 |

| Mexico | Yes | 1.92–35% | Yes | $1,200–$2,000 |

| Portugal (NHR) | Yes | 0% foreign income for 10 years | Yes | $1,650–$2,200 |

| Canada | Yes | 20–33% federal + provincial | Yes | $2,500–$4,000 |

| UK | Yes | 20–45% | Yes | $2,500–$4,500 |

| Colombia | No | 0–39% (after 183 days) | Yes | $1,200–$2,200 |

The FEIE and FTC apply across the board. For most Americans earning under $130,000 from foreign sources, the presence or absence of a tax treaty changes very little in practice. The geographic arbitrage playbook runs the full cost-of-living comparison for the top destinations.

When Treaties Actually Matter: Pensions, Dividends, and Withholding

Strip away the saving clause frustration, and there are real scenarios where a US tax treaty delivers value — particularly for retirees with cross-border income and investors holding foreign securities directly.

Foreign Pensions and Social Security

This is where treaties earn their keep. If you spent years working in a treaty country and accrued a local pension, the treaty often determines whether the US gets a cut.

Canada: The US-Canada treaty explicitly excludes Canadian CPP and OAS benefits from US taxation. American retirees who've built up CPP credits receive those benefits US-tax-free. US Social Security is generally taxable only by the US — Canada can't double-tax it.

UK: The US-UK treaty allows UK pension lump sums of up to £1,073,100 (roughly $1.35 million at current rates) to be paid out with favorable tax treatment. The treaty also reduces withholding on dividends to 5% for qualifying shareholders and 0% on interest payments.

Germany: Pensions from the German statutory pension insurance (Deutsche Rentenversicherung) are taxable only in Germany for German residents, even if the recipient is a US citizen. One of the cleaner cross-border pension arrangements available.

Withholding Taxes on Foreign Investments

Foreign companies withhold tax on dividends before the check reaches you. Without a treaty, the standard rate is often 25–30%. With a treaty, it frequently drops to 5–15%.

| Country | Standard Dividend Withholding | Treaty Rate (Qualified) | Interest Rate (Treaty) |

|---|---|---|---|

| Canada | 25% | 5–15% | 0% |

| United Kingdom | 0% (UK doesn't withhold) | 5% | 0% |

| Germany | 26.4% | 5–15% | 0% |

| France | 30% | 5–15% | 0% |

| Netherlands | 25% | 5–15% | 0% |

| Switzerland | 35% | 5–15% | 0% |

These reduced withholding rates survive the saving clause — one of the few areas where treaties deliver tangible value on investment income. If you're holding foreign stocks directly or investing through a foreign brokerage, this matters. Expats who keep their primary brokerage at a US institution like Charles Schwab International — which also refunds ATM fees worldwide and keeps your US banking intact abroad — often have treaty withholding elections handled automatically.

Why No-Treaty Countries Often Work Better

Panama and Costa Rica tax only locally-sourced income. If you're working remotely for a US company or running an online business from Medellín or San José, your income isn't sourced in those countries. They don't tax it. The US taxes it, but the FEIE exclusion eliminates the first $130,000. Net result: often zero tax on both sides, with no treaty required.

The UAE has zero income tax entirely. No withholding, no local tax, no treaty needed. You still file US taxes and use FEIE or FTC to zero out the bill — but there's no foreign tax to complicate the picture.

Thailand's situation deserves a specific warning. Thailand moved in 2024 to tax all foreign-sourced income remitted into the country, regardless of when it was earned. For digital nomads depositing US client payments into a Thai bank account, that creates a local tax liability — and with no US-Thailand treaty, there's no fallback. The FTC would still apply to the extent you pay Thai income tax, but navigating it without a treaty means less certainty. Read the expat investing playbook before moving significant income streams to a no-treaty country with shifting rules.

The State Tax Problem Nobody Warns You About

Federal treaties operate at the federal level. States set their own rules — and some states don't honor federal treaty provisions at all.

California and Virginia are the notorious examples. If you're a California domiciliary who moves to Germany, California may continue to tax you as a state resident, and it does not have to recognize the US-Germany treaty in computing your state bill. This problem has nothing to do with federal double taxation — it's a third layer entirely.

This is one of the strongest arguments for establishing domicile in a no-income-tax state before going abroad. Florida, Texas, Nevada, Wyoming, and South Dakota have no state income tax — and no treaty question to navigate at the state level. Changing your state domicile before departing eliminates this entire problem, treaty or not.

A Traveling Mailbox virtual address in a no-income-tax state ($15/month, real US street address in 50+ cities, mail scanning, check deposits) gives you the IRS correspondence address and state domicile documentation you need without actually requiring you to live there. It's also essential for maintaining US banking while abroad — most US banks won't keep your account open without a US address on file. Our virtual mailbox guide covers the full setup.

How to Claim Treaty Benefits: Form 8833

Treaty benefits are not automatic. If you're claiming a treaty-based tax position on your US return — a reduced withholding rate, a pension exclusion, a specific income exemption — you must file Form 8833 (Treaty-Based Return Position Disclosure) with your return.

Failing to file Form 8833 when required isn't just losing the treaty benefit. It's a separate $1,000 penalty per unreported position. Claim multiple treaty provisions across multiple years without the form and those penalties compound quickly.

Form 8833 requires identifying the specific treaty article you're relying on, explaining the position, and quantifying the tax benefit. Most expat tax software prompts you to complete it; if you're using generic US tax software or filing manually, it's easy to miss entirely.

The HSA Angle: A Tax Tool Treaties Can't Touch

While tax treaties consume significant mental real estate for expats, one of the most effective US tax-advantaged accounts gets almost no attention abroad: the Health Savings Account.

Your existing HSA balance can be spent on qualified medical expenses anywhere in the world, tax-free. Foreign doctors, foreign hospitals, foreign pharmacies — all qualify as long as the service would be a qualified medical expense under IRS rules. The HSA doesn't care what country you're in.

The catch: you can only contribute to an HSA while enrolled in a qualifying High-Deductible Health Plan (HDHP). Foreign national health insurance — including plans from countries with universal healthcare — does not qualify as an HDHP under IRS rules. The moment you enroll in a local foreign health plan, you lose contribution eligibility. Violate this and you face a 20% excise tax on excess contributions plus ordinary income tax on the same amount — a double hit that adds up fast.

The 2025 HSA contribution limits are $4,300 (individual) and $8,550 (family), with an additional $1,000 catch-up for those 55 and older. For 2026, those limits rise to $4,400 and $8,750. Expats still covered by a US-based HDHP through an employer can keep contributing. Many max out their HSA before leaving and let the balance grow invested tax-free indefinitely — then use it as a tax-advantaged medical fund abroad, where the money goes further anyway. After age 65, non-medical HSA withdrawals are taxed as ordinary income only (no 20% penalty), making the HSA function as a supplemental traditional IRA.

For expat health coverage that maintains HDHP status, options narrow considerably. SafetyWing is widely used among digital nomads abroad — but it's not an HDHP, so enrolling ends your HSA contribution eligibility. See the expat health insurance guide for a full breakdown of options and HSA compatibility.

Filing Requirements That Apply Regardless of Treaties

Whether or not a tax treaty applies, these obligations exist independently — and missing them carries penalties that dwarf most tax bills:

- FBAR (FinCEN 114): Required if your foreign financial accounts exceeded $10,000 in aggregate at any point during the year. Due April 15, extended automatically to October 15. Penalty for willful non-filing: up to $100,000 or 50% of account balance per violation.

- Form 8938 (FATCA): Required for expats with foreign financial assets exceeding $200,000 at year-end or $300,000 at any point. Penalty for failure: $10,000 plus continuation penalties.

- Form 2555 (FEIE): How you claim the Foreign Earned Income Exclusion. Filed with your Form 1040.

- Form 1116 (FTC): How you claim the Foreign Tax Credit. Can be used in combination with Form 2555 for different income categories.

- Form 8833: Required when claiming any treaty-based position on your return.

The filing stack for a US expat with foreign accounts, investment income, and potential treaty positions can involve six or more forms that most domestic tax preparers have never seen. The complete US expat banking and tax guide covers the full FBAR/FATCA/FEIE requirements.

Banking Setup That Survives the No-Treaty Problem

One practical consequence of the no-treaty landscape: US financial institutions are spooked by FATCA compliance burdens, and foreign banks in non-treaty countries are sometimes reluctant to open accounts for Americans. The solution most experienced expats use is keeping a solid US banking foundation regardless of where they live.

Mercury works well for the business banking side — US-based, FDIC-insured, no monthly fees, and accessible globally. For personal banking with the widest ATM access abroad, Charles Schwab's checking account reimburses all ATM fees worldwide with no foreign transaction fees — essential if you're moving between no-treaty countries without established local banking. For international transfers when you need to move money across borders, Remitly covers 170+ countries with competitive rates and same-day delivery on most corridors.

The Residence-Based Taxation Push

For years, expat advocacy groups have pushed for a shift from citizenship-based taxation (CBT) to residence-based taxation (RBT) — the system every other developed country uses. Under RBT, you'd only owe US taxes while actually living in the US. No saving clause problem, no double-filing burden, no treaties needed to patch the gaps.

Multiple legislative proposals in 2025 targeted this shift. None passed into law. The Taiwan Double-Tax Relief Act — addressing the fact that Taiwan has no comprehensive US tax treaty despite being a major tech and business hub — passed the House in January 2025. The US also withdrew from UN global minimum tax negotiations in early 2025, signaling a continued preference for bilateral arrangements over multilateral frameworks.

Until something changes legislatively, the operating reality remains: treaties help at the margins, mostly for pensions and dividend withholding rates. The FEIE and FTC are doing the heavy lifting. Choosing where to live based primarily on treaty status is at best a secondary factor — the cost of living differential between a $1,500/month lifestyle in Panama and a $3,500/month lifestyle in a treaty country dwarfs anything the treaty saves.

Bottom Line

US tax treaties are valuable for retirees collecting foreign pensions, investors receiving dividends directly from foreign companies, and workers in high-tax countries who need to clarify which government gets priority on specific income categories. For those scenarios, hire a qualified expat CPA, identify the relevant treaty article, and file Form 8833.

For everyone else — the remote worker in Bali, the freelancer in Medellín, the digital nomad hopping between Bangkok and Panama City — the saving clause means the treaty isn't doing much anyway. The FEIE eliminates the first $130,000 of foreign earned income. The FTC handles taxes paid to high-tax foreign governments. Both work everywhere, in every country, with or without a treaty. The expats choosing no-treaty destinations aren't making a mistake. They've correctly figured out that the treaty wasn't going to save them much — and that the real arbitrage is in the cost of living, not the treaty map.

Financial Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. US international tax law is complex and fact-specific. Consult a qualified CPA or tax attorney with expertise in US expat taxation before making decisions about treaty positions, FEIE elections, FTC strategy, or HSA contributions. The author is not a licensed tax professional. Laws and limits referenced reflect information available as of early 2026 and are subject to change.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJuly 4, 2026

Expat Tax & FinanceJuly 4, 2026

Canadian TFSA and US Taxes: The Reporting Trap

US citizens holding a Canadian TFSA owe tax on all annual growth and must file Form 3520 — PFIC rules apply to Canadian mutual funds inside the

Expat Tax & FinanceJuly 4, 2026

Expat Tax & FinanceJuly 4, 2026

State Income Tax for Expats: Which States Follow You

California, New York, and Virginia keep taxing Americans abroad. Learn which states follow you, what triggers audits, and how to exit cleanly.

Expat Tax & FinanceJuly 3, 2026

Expat Tax & FinanceJuly 3, 2026

FBAR: The $10,000 Expat Rule Most People Get Wrong

FBAR: when any foreign account aggregate hits $10,000 during the year, all accounts must be reported. Penalties, Bittner ruling, and catch-up