Self-Employment Tax: The Expat Freelancer’s Hidden Bill

The FEIE eliminates US income tax—but not self-employment tax. Here’s what expat freelancers actually owe and the legal routes to reduce or wipe it out.

FEIE zeroes your income tax abroad—but SE tax still applies. See the exact numbers and legal ways to reduce your bill as a US expat freelancer.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

You moved abroad. You claimed the Foreign Earned Income Exclusion. Your US federal income tax bill dropped to zero. Then your accountant sent you a number that made your stomach drop: $16,956. Still owed. To the IRS. Every year.

That number is your self-employment tax — and the FEIE doesn't touch it. Not one dollar. While the FEIE is genuinely one of the best provisions in the US tax code, it was designed to eliminate income tax, not Social Security and Medicare contributions. The distinction costs the average US freelancer abroad between $7,000 and $19,000 per year, and most don't find out until they're already behind.

Here's the full breakdown: how SE tax works, what it actually costs at different income levels, the legal routes to reduce or eliminate it, and the S-Corp math that's more complicated than it looks in expat Facebook groups.

How Self-Employment Tax Actually Works

Self-employment tax is the mechanism by which self-employed people fund Social Security and Medicare. When you're a W-2 employee, your employer splits this cost — 7.65% comes out of your paycheck and your employer quietly pays another 7.65%. As a freelancer or independent contractor, you pay both halves: 15.3% total.

The breakdown: 12.4% goes to Social Security (capped at the annual wage base — $176,100 for 2025) and 2.9% goes to Medicare on all net earnings. If your net self-employment income exceeds $200,000 as a single filer or $250,000 married filing jointly, an additional 0.9% Medicare surtax applies on top of that.

There's one semi-saving grace: SE tax applies to 92.35% of your net self-employment income, not 100%. This is because the IRS lets you treat the employer-half of SE tax as a deductible business expense before calculating the tax itself. So the actual math is: Net Self-Employment Income × 92.35% × 15.3%.

The filing threshold is just $400 in net self-employment income. Earn $401 freelancing abroad and you owe SE tax — regardless of how much the FEIE saved you on income taxes. The IRS's position, stated explicitly in Publication 54: "The foreign earned income exclusion will reduce your regular income tax but will not reduce your self-employment tax."

The Numbers That Surprise Every Expat Freelancer

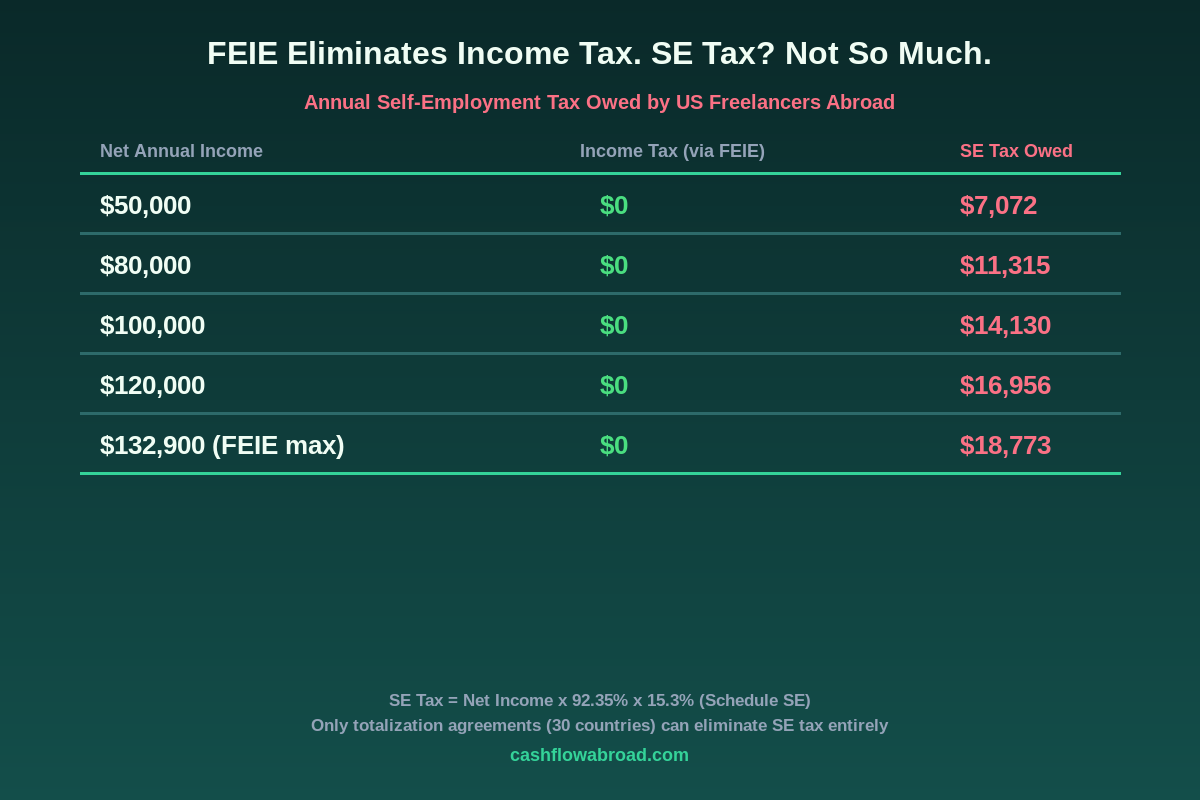

For 2025, the FEIE ceiling is $130,000. For 2026 it rises to $132,900 due to inflation indexing. Use the exclusion in full and your federal income tax on qualifying foreign earned income drops to zero. Your SE tax calculation ignores the exclusion entirely — it's computed on gross net self-employment income before the FEIE applies.

A freelance consultant netting $100,000 from a co-working space in Chiang Mai or Lisbon or Medellín owes the IRS $14,130 in SE tax. At $120,000 net income, that number is $16,956. These figures don't budge based on which country you're in, how long you've lived abroad, what tax treaties exist, or whether your income tax is zero via the FEIE. The only factors that change the SE tax calculation are totalization agreements and business entity structure — both addressed below.

The 30 Countries That Can Wipe the Bill Entirely

The US has Social Security totalization agreements with 30 countries. Under these agreements, you can't be taxed by both countries for the same social security benefit — so if you're actively paying into your host country's pension system, you're exempt from US self-employment tax. For a freelancer earning $120,000 in Germany or Portugal, this exemption is worth $16,956/year. That's a number worth building your country choice around.

To claim the exemption, you need a Certificate of Coverage from your host country confirming you're paying into their system — submitted with Form 4029 and Schedule SE. The certificate is free to obtain from the host country's social security authority; the actual enrollment requirements and costs vary by country.

| Has Totalization Agreement (SE Tax Exempt) | No Agreement (Full SE Tax Applies) |

|---|---|

| Australia, Austria, Belgium | Thailand, Indonesia/Bali |

| Brazil, Canada, Chile | UAE, Vietnam, Cambodia |

| Czech Republic, Denmark, Finland | Colombia, Panama, Costa Rica |

| France, Germany, Greece | Paraguay, Ecuador, Georgia |

| Hungary, Iceland, Ireland, Italy | Malaysia, Philippines, Argentina |

| Japan, Luxembourg, Netherlands | Mexico, Dubai/UAE, Turkey |

| Norway, Poland, Portugal, Slovakia | Taiwan, Morocco, Montenegro |

| Slovenia, South Korea, Spain, Sweden | Most of Southeast Asia |

| Switzerland, United Kingdom, Uruguay | Most of Latin America & Africa |

Notice the pattern: the countries freelancers flock to for geographic arbitrage — Thailand, Bali, Colombia, Panama, UAE, Georgia, Vietnam — are almost entirely outside the totalization agreement network. The countries that do have agreements tend to be higher-cost Western nations where the income arbitrage advantage is smaller.

There's one crucial nuance: the totalization agreement works only if you're actively enrolled in and contributing to the host country's social security system. Many expat freelancers opt out of local social security entirely — which means they're covered under neither system and owe US SE tax in full. If eliminating SE tax via totalization is your goal, active enrollment in the local scheme is a prerequisite, not optional.

When the S-Corp Play Actually Makes Sense

The advice in expat communities tends to be binary: "Convert your LLC to an S-Corp and eliminate self-employment tax." The advice is directionally correct but leaves out the math that determines whether it's actually worth it — and the expat-specific complication that can create new income tax liability where none existed before.

With a standard single-member LLC, 100% of your net profit flows to Schedule SE. Every dollar of net income is subject to the 15.3% calculation. With an S-Corp, you pay yourself a "reasonable salary" (subject to payroll taxes) and take the remaining profit as a distribution — which is not subject to self-employment tax. The savings come from what you don't label as salary.

Concrete example: $120,000 net consulting income, living abroad:

| Structure | Salary (Payroll Tax) | Distribution (No SE Tax) | SE / Payroll Tax | Compliance Cost | Net Cost |

|---|---|---|---|---|---|

| Single-member LLC | $120,000 | — | $16,956 | ~$500/year | $17,456 |

| S-Corp ($60K salary) | $60,000 | $60,000 | $8,478 | ~$3,000–4,000/year | $11,478–12,478 |

| S-Corp net savings | — | — | $8,478 saved | — | ~$5,000–6,000/year |

The compliance cost isn't trivial. Running an S-Corp requires payroll processing (even for a solo owner), quarterly payroll tax deposits, W-2 filing, and a separate entity tax return (Form 1120-S). Add payroll software, a bookkeeper, and increased CPA fees and you're realistically looking at $2,500–4,000/year in extra overhead. Below roughly $85,000–90,000 in net self-employment income, the gross savings don't cover the compliance costs.

The expat-specific wrinkle: FEIE applies only to earned income — wages and net self-employment income from active work. S-Corp distributions are not earned income, so they don't qualify for the FEIE. If your S-Corp pays you a $60,000 salary and $60,000 in distributions, only the salary portion is excludable under the FEIE. The $60,000 in distributions is taxable as ordinary income at regular US rates.

For some earners, this creates a scenario where the S-Corp structure saves $8,478 in SE tax but creates $8,000–12,000 in new income tax liability on the distributions — a wash or worse. Run the full tax model before converting. This is one of those situations where the advice that sounds smart in a forum can cost you real money if you don't model it for your specific situation.

If you're operating a US LLC or S-Corp while abroad, keeping a valid US mailing address is non-negotiable for IRS correspondence, payroll records, and state compliance. Traveling Mailbox provides a real US street address in 50+ cities, with digital mail scanning and remote check deposit for about $15/month — the cleanest solution most expat business owners use for this. For US business banking, Mercury is built for remote-operated businesses and handles both LLC and S-Corp accounts with no minimums, free wires, and solid ACH infrastructure for payroll.

For a fuller breakdown of entity structures, state compliance, and the full cost-benefit of running a US business from abroad, the expat business structure guide covers the mechanics across different scenarios.

The Half-SE Deduction: Partial Help, Widely Misunderstood

The IRS allows you to deduct half of your self-employment tax as an above-the-line adjustment to gross income. On a $16,956 SE tax bill, that's an $8,478 deduction — sounds significant. For most expats using the FEIE, it's largely irrelevant.

The half-SE deduction reduces adjusted gross income, which reduces federal income tax liability. If the FEIE has already zeroed out your income tax, there's no income tax left to reduce. The deduction only generates real savings if you have income above the FEIE ceiling — US-source income, rental income, capital gains, S-Corp distributions — that would otherwise be taxable at ordinary rates.

Don't let accountants use the half-SE deduction to soften the blow of a large SE tax bill when your income tax is already zero. It doesn't reduce the SE tax itself — only potential income tax that may not exist in your situation.

What to Do Based on Your Situation

The right path depends on income level, country of residence, and how much complexity you're willing to manage:

Under $60,000/year net SE income: The S-Corp structure costs more than it saves at this level. Focus on whether your host country has a totalization agreement and whether enrolling in their pension system is practical. If not, budget the SE tax and optimize elsewhere. Charles Schwab International remains the standard for holding and investing savings as an expat — no foreign transaction fees and worldwide ATM reimbursements.

$60,000–$100,000/year: Run the S-Corp math with a CPA who specializes in expat taxation. Factor in your state of domicile — if you're still legally domiciled in California or New York, those states impose additional entity-level taxes and requirements that affect the S-Corp calculation. No-income-tax states (Wyoming, South Dakota, Nevada, Florida, Texas) make the structure cleaner.

Over $100,000/year: The S-Corp structure almost certainly saves money, even accounting for full compliance costs — but the FEIE interaction must be modeled carefully. The "reasonable compensation" salary you pay yourself should be defensible: IRS scrutiny increases when S-Corp owners pay themselves salaries well below industry norms. Most tax practitioners recommend 40–60% of net profit as salary for service businesses, with clear documentation justifying the figure.

If you're choosing a country: A totalization agreement country can legally eliminate $15,000+/year in SE tax on a $120,000 income. That factor is worth incorporating into your country analysis alongside income tax rates, cost of living, and quality of life. Germany, Portugal, Spain, Ireland, and Australia all have agreements. Most of Southeast Asia and Latin America do not. For a full US expat tax guide covering how FEIE, Foreign Tax Credit, FBAR, and SE tax interact across different residency scenarios, that's the next read.

Everyone: File Schedule SE every year regardless of income tax outcome. The $400 threshold is extremely low, and SE tax underpayment is a common correspondence-audit trigger for expats. The IRS cross-references 1099s and foreign income disclosures — omitting Schedule SE when you have self-employment income creates a paper trail problem that's expensive to unwind. For comprehensive tax compliance planning including how SE tax fits into the larger expat picture, the FEIE guide and the expat estate planning guide cover the adjacent obligations most people overlook.

The Bottom Line

The FEIE is a genuine windfall. At $130,000 for tax year 2025 and $132,900 for 2026, it eliminates most or all US income tax for the average expat freelancer. What it doesn't do — and has never done — is touch self-employment tax. That 15.3% on 92.35% of your net earnings moves straight to the IRS regardless of where you live, where you earned the money, or what exclusion you claim.

Three legitimate paths exist to reduce or eliminate it: move to one of the 30 totalization agreement countries and enroll in their social security system, restructure as an S-Corp above the ~$90,000 income threshold (after carefully modeling the FEIE interaction on distributions), or accept the bill and plan around it. None of these paths require exotic structures. They require knowing the rules before the surprise invoice arrives — which most expats learn too late.

Financial Disclaimer: This article is for informational purposes only and does not constitute tax or legal advice. Self-employment tax rules, totalization agreement eligibility, S-Corp requirements, and FEIE mechanics involve fact-specific analysis that varies by individual circumstances. Consult a qualified CPA or enrolled agent specializing in US expat taxation before making any structural decisions. Tax laws and treaty provisions change; verify current figures with the IRS or a licensed tax professional.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 11, 2026

Expat Tax & FinanceMay 11, 2026

The FEIE Self-Employment Tax Trap for Expat Freelancers

FEIE won't save expat freelancers from SE tax. Learn what you actually owe, which countries offer exemptions, and 3 strategies to reduce the bill.

Expat Tax & FinanceJuly 14, 2026

Expat Tax & FinanceJuly 14, 2026

Expat State Taxes: Which US States Won't Let You Go

Move abroad and California may still tax you 13.3%. Learn which five states chase expats, how domicile works, and how to sever state ties legally.

Expat Tax & FinanceJuly 2, 2026

Expat Tax & FinanceJuly 2, 2026

S-Corp vs LLC for US Expats: SE Tax Savings Compared

US expats pay 15.3% SE tax on LLC profits even with FEIE. Learn when an S-corp election saves tax, how GILTI affects foreign corps, and when to use a