US Expat Banking & Taxes: The Complete FBAR, FATCA, FEIE Guide

The United States is one of only two countries on Earth that taxes its citizens based on citizenship rather than residency.

The United States is one of only two countries on Earth that taxes its citizens based on citizenship rather than residency.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

The US Citizenship-Based Taxation Problem

Let's get the foundational absurdity out of the way: if you hold a US passport (or a Green Card), you are required to file a US tax return every single year and report your worldwide income — no matter where you live, where you earn, or how long you've been gone. You could be a dual citizen who was born in Paris, lived your entire life in France, never set foot in the US, and the IRS still expects you to file. This system dates back to the Civil War in 1864, when it was implemented to tax Americans who fled to Europe to avoid the conflict. Over 160 years later, it's still on the books. Every other developed nation on the planet uses residency-based taxation. You live there, you pay taxes there. You leave, you stop. Simple. Not the US. This creates a cascading set of problems:- Double taxation risk on every dollar you earn

- Complex reporting requirements for foreign accounts and assets

- Banking discrimination — foreign banks increasingly refuse American clients

- Eye-watering penalties for mistakes you didn't even know you were making

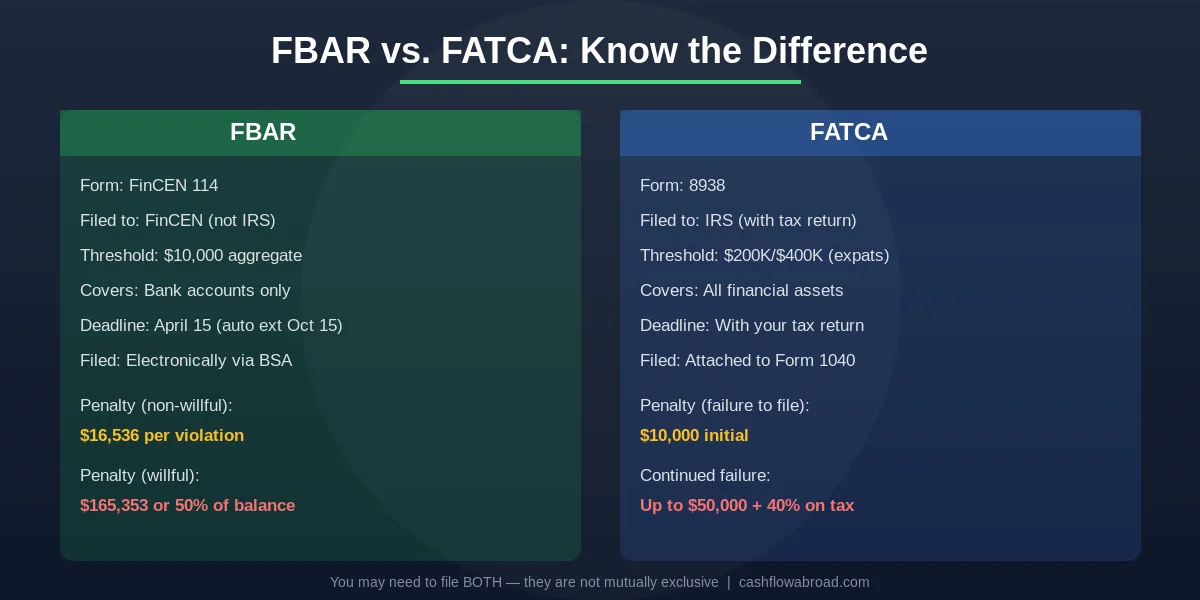

FBAR: The $10,000 Reporting Threshold Everyone Misses

The Report of Foreign Bank and Financial Accounts (FBAR, officially FinCEN Form 114) is one of the most commonly missed filing requirements for expats — and one of the most expensive mistakes you can make.Who Must File

You must file an FBAR if you are a US person (citizen, resident, Green Card holder) and the aggregate value of all your foreign financial accounts exceeded $10,000 at any point during the year. That's the combined total across every foreign account you have. If you have 5 bank accounts in different countries, each holding $2,001, your aggregate is $10,005 — and you must file. This includes checking accounts, savings accounts, investment accounts, and even accounts where you have signature authority but no financial interest.The Penalties Are Brutal

This is where it gets scary:- Non-willful violation: Up to $16,536 per violation (2025, adjusted annually for inflation)

- Willful violation: Up to $165,353 or 50% of the account balance — whichever is greater

- Criminal penalties: Up to $500,000 in fines and 10 years in prison

How and When to File

The FBAR is filed electronically through the FinCEN BSA E-Filing System — not with your tax return. The deadline is April 15, with an automatic extension to October 15 (no form required).FATCA: Why Foreign Banks Keep Rejecting Americans

The Foreign Account Tax Compliance Act (FATCA), enacted in 2010, is the reason your life as a US expat is significantly harder than it needs to be. FATCA requires every foreign financial institution in the world to identify US account holders and report their details to the IRS. Banks that don't comply face a 30% withholding tax on their US-source income. The result? Many foreign banks have decided it's simply not worth the compliance cost to accept American customers. An estimated 340,000 accounts were closed in 2025 alone for Americans living abroad.Your Reporting Obligation: Form 8938

In addition to FATCA's burden on banks, it created a reporting obligation for you: Form 8938 (Statement of Specified Foreign Financial Assets), filed with your tax return. Thresholds for expats living abroad:| Filing Status | End of Year | Any Time During Year |

|---|---|---|

| Single | >$200,000 | >$300,000 |

| Married Filing Jointly | >$400,000 | >$600,000 |

FBAR vs. FATCA: What's the Difference?

This is one of the most confusing areas for expats because both deal with reporting foreign accounts. Here's the critical distinction: The key takeaway: you may need to file BOTH. They are not mutually exclusive. The FBAR has a much lower threshold ($10,000) but only covers bank accounts. Form 8938 has a higher threshold but covers a wider range of financial assets including securities, financial instruments, and interests in foreign entities.

The key takeaway: you may need to file BOTH. They are not mutually exclusive. The FBAR has a much lower threshold ($10,000) but only covers bank accounts. Form 8938 has a higher threshold but covers a wider range of financial assets including securities, financial instruments, and interests in foreign entities.

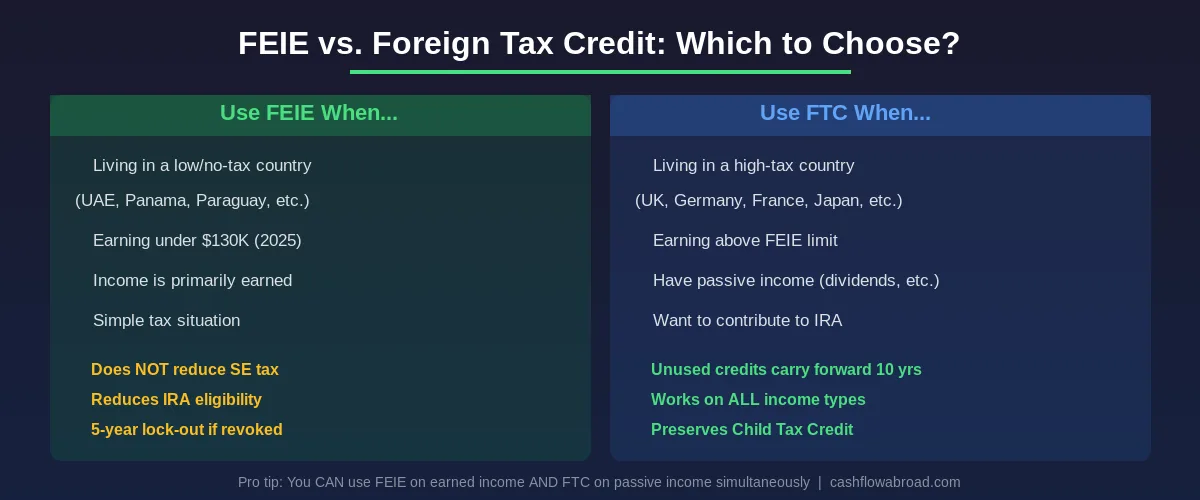

Foreign Earned Income Exclusion (FEIE): Exclude Up to $130,000

The Foreign Earned Income Exclusion is the single most powerful tax tool available to US expats. It allows you to exclude up to $130,000 (2025) or $132,900 (2026) of foreign earned income from US federal taxation. That means if you're earning $100,000 while living in Bangkok, and you qualify, your US federal tax on that income is $0.How to Qualify: Two Tests

You must meet one of two tests: 1. Physical Presence Test- Be physically present in a foreign country for 330 full days during any 12 consecutive months

- Days don't need to be consecutive

- The 12-month period doesn't have to align with the calendar year

- Travel days between foreign countries count; days in the US do not

- Pro tip: Keep a detailed travel log with dates, passport stamps, and boarding passes

- Be a bona fide resident of a foreign country for an uninterrupted period that includes an entire tax year (January 1–December 31)

- Must be a US citizen (Green Card holders generally can't use this unless they're citizens of a treaty country)

- The IRS looks at intent — did you genuinely establish a life abroad?

The Housing Exclusion Bonus

On top of the FEIE, you can claim the Foreign Housing Exclusion for qualifying housing expenses above a base amount. For 2025:- Base housing amount: $20,800

- Standard cap: $39,000

- High-cost city adjustments: Hong Kong ($114,300), Geneva ($102,600), Singapore ($82,900), Tokyo ($67,700), London ($67,000)

Critical Limitations

- Only applies to earned income (wages, salary, self-employment) — NOT investment income, dividends, or capital gains

- Does NOT reduce self-employment tax (more on this below — it's a big one)

- If you revoke the FEIE election, you cannot re-elect it for 5 years without IRS approval

- Excluded income cannot be used for IRA contributions

- Reduces your eligibility for the Child Tax Credit

Foreign Tax Credit (FTC): The Dollar-for-Dollar Offset

The Foreign Tax Credit (Form 1116) is the FEIE's more sophisticated sibling. Instead of excluding income, it provides a dollar-for-dollar credit against your US tax for income taxes you've already paid to a foreign government. Living in Germany and paid 35% in German income tax? Since Germany's rate exceeds the US rate, the FTC can potentially eliminate your entire US tax liability — and the excess credits carry forward for up to 10 years (or back 1 year).Why Many Expats Should Choose FTC Over FEIE

- Works on all income types, including passive income (dividends, interest, rental income)

- Doesn't reduce IRA contribution eligibility

- Preserves Child Tax Credit eligibility

- No lock-out period — you can switch strategies freely (but revoking FEIE triggers its 5-year lock-out)

- Unused credits carry forward 10 years

FEIE vs. FTC: Which One Should You Use?

This is the million-dollar question (sometimes literally). The right answer depends entirely on your situation: The general rule of thumb:

The general rule of thumb:

- Low/no-tax country (UAE, Panama, Paraguay, Cayman Islands) → FEIE

- High-tax country (UK, Germany, France, Japan, Scandinavia) → FTC

- Earning above $130K → Use FEIE on the first $130K, FTC on the rest

- Significant investment income → FTC (FEIE can't touch passive income)

Best Banks for US Expats (And Which Ones Will Close Your Account)

Banking as a US expat is a minefield. Thanks to FATCA compliance costs, many domestic banks will close your account when they discover you've moved abroad, and many foreign banks will refuse to open one. Here's what actually works:Best US Bank: Charles Schwab International

This is the gold standard for expat banking:- No foreign transaction fees

- Unlimited worldwide ATM fee rebates — use any ATM anywhere, fees refunded

- No monthly fees, no minimum balance

- Full US routing and account number (critical for IRS direct deposit, ACH transfers)

- Must apply through Schwab International if already abroad

👉 Open a Schwab International Account

HSBC Premier

- Global banking network in 60+ countries

- Multi-currency accounts and free intra-HSBC transfers worldwide

- In-person branch access globally

- Caveat: Requires $75,000+ combined balance to waive monthly fees

Digital Banking (Essential for Every Expat)

Remitly (formerly TransferWise): The best option for international transfers. Multi-currency account holding 40+ currencies, local bank details in 8+ currencies, and the mid-market exchange rate with no markup. Fees start at 0.41%. For frequent smaller transfers (rent, support payments), Remitly is another excellent choice with fees as low as $1.49. Revolut: Best for daily spending abroad. Supports 45+ million customers globally with competitive FX rates, crypto, and stock trading. The winning combination: Most savvy expats use Schwab as their US base account, Remitly for international transfers and receiving payments, and Revolut for daily foreign spending. If you run a US business from abroad, add Mercury — it is purpose-built for online businesses and works seamlessly from any country without branch visits. This stack covers virtually every banking need. One more essential: switch your financial email to Proton Mail. With FBAR and FATCA reporting requirements, your email contains sensitive financial data that Gmail happily scans and indexes. Proton is end-to-end encrypted and based in Switzerland — outside US jurisdiction.Banks That Will Close Your Account

Many mainstream US banks and brokerages routinely close accounts when they discover a client has moved abroad. This includes some major names citing SEC/FINRA regulations. Before you move:- Open accounts at expat-friendly institutions before leaving

- Don't update your address abroad at banks that aren't expat-friendly

- Keep a US mailing address (family member or Traveling Mailbox for a real street address from $15/month)

- Set up Schwab and Remitly before your departure — it's much harder from abroad

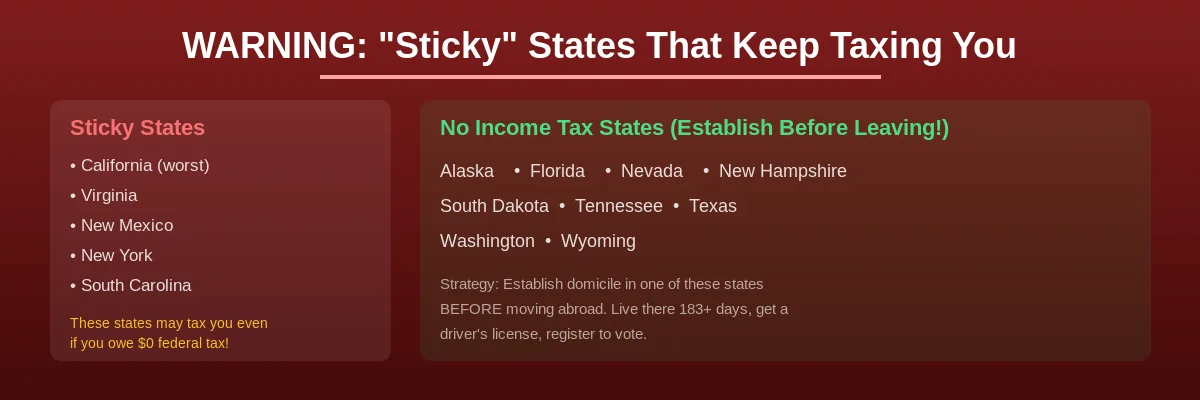

State Taxes: The Trap Nobody Warns You About

Here's a nightmare scenario that catches thousands of expats: you successfully eliminate your federal tax using the FEIE, only to discover you still owe thousands in state taxes. Why? Because most states do not recognize the FEIE at the state level. And several states will continue to claim you as a tax resident long after you've left the country.

The Worst Offender: California

California is the most aggressive state for expat taxation:- Uses a "closest connections" test — maintaining property, bank accounts, a driver's license, or voter registration can keep you on the hook

- Taxes all worldwide income of residents

- Does NOT recognize the FEIE at the state level

- Can and will audit you years after you've left

Virginia's Dirty Trick

Virginia considers overseas moves "temporary" unless you provide overwhelming evidence of permanence. The state explicitly requires you to establish domicile in another US state to terminate Virginia domicile. Moving directly abroad without passing through another state? Virginia says you're still theirs.The Solution: Establish Residency in a No-Tax State Before Leaving

The nine states with no income tax: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. To properly establish domicile before moving abroad:- Live in the state for at least 183 days

- Get a driver's license

- Register to vote

- Open bank accounts there

- File a final state tax return in your old state marking it as your last

Self-Employment Tax: The FEIE Won't Save You

If you're a freelancer, consultant, or run your own business abroad, brace yourself for the single biggest tax surprise most expat entrepreneurs face: the Foreign Earned Income Exclusion does not reduce self-employment tax. Even if you exclude your entire income from federal income tax using the FEIE, you still owe:- 12.4% Social Security tax (on earnings up to $176,100 in 2025)

- 2.9% Medicare tax (on all earnings, no cap)

- 0.9% additional Medicare surtax on earnings over $200,000 (single)

Totalization Agreements: Your Potential Escape

The US has totalization agreements with 30 countries that eliminate dual Social Security taxation. If you're paying into the social security system of a partner country, you may be exempt from US self-employment tax. Countries with agreements: Australia, Austria, Belgium, Brazil, Canada, Chile, Czech Republic, Denmark, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Japan, Luxembourg, Netherlands, Norway, Poland, Portugal, Slovak Republic, Slovenia, South Korea, Spain, Sweden, Switzerland, United Kingdom, and Uruguay. Important: You need a Certificate of Coverage from the country where you ARE paying social security. Without this document, both countries may demand payment. Notable countries WITHOUT agreements: China, India, Mexico, Thailand, Vietnam, Colombia, and most of Southeast Asia and Latin America. If you're self-employed in these countries, you're paying US self-employment tax — period.Tax Treaties: The Savings Clause Nobody Reads

The US has tax treaties with 61 countries. Many expats assume this means they're protected from double taxation. They're mostly wrong.The Savings Clause Problem

Nearly every US tax treaty contains a savings clause — a provision that reserves the US government's right to tax its citizens and residents as if the treaty didn't exist. This is unique to US treaties and it effectively neutralizes most treaty benefits for American expats.Common Misconceptions

- "Living in a treaty country means no US tax" — False. The savings clause preserves the US right to tax you.

- "Treaties automatically eliminate double taxation" — False. Most expats rely on the FEIE and FTC, not treaty provisions.

- "Treaties are the primary tool for avoiding double taxation" — False. The credit system (FTC) is usually more important.

Where Treaties Actually Help

Treaties aren't useless — they just don't do what most people think:- Reducing withholding rates on passive income (dividends, interest, royalties)

- Specific provisions for pensions and retirement income

- Special rules for teachers, researchers, and students

- They work alongside the FEIE and FTC as complementary tools

Renouncing Citizenship: The Nuclear Option

With renunciations surging — from an average of 200–400 per year before 2009 to nearly 5,000 in 2024 — it's clear that many Americans abroad are reaching their breaking point with the tax and banking burden. Starting April 13, 2026, the State Department fee drops to $450 (down from $2,350 — an 80% reduction). But the financial implications go far beyond the filing fee.The Exit Tax

If you're classified as a "covered expatriate" — meeting ANY one of three tests — you face an exit tax: You're covered if:- Your net worth is $2 million or more

- Your average annual net income tax over the past 5 years exceeds $211,000 (2026)

- You cannot certify 5 years of full tax compliance on Form 8854

Key Deadlines and Extensions for Expats

| Deadline | What | Notes |

|---|---|---|

| April 15 | Standard filing + payment deadline | Taxes owed are due regardless of extensions |

| June 15 | Automatic 2-month extension for expats | No form needed if tax home + abode are outside the US on April 15. Interest still accrues from April 15. |

| October 15 | Extended filing deadline | Must file Form 4868 before June 15. Also the FBAR automatic extension deadline. |

Your Expat Tax Action Plan

Whether you're already abroad or planning your move, here's what to do:Before You Leave

- Open expat-friendly bank accounts — Schwab International, Remitly, and Revolut at minimum. SoFi is another strong option for combined banking and investing with zero commissions.

- Establish domicile in a no-tax state if coming from a "sticky" state (CA, VA, NM, NY, SC)

- File a final state tax return in your old state

- Get a mail forwarding address in your new domicile state — Traveling Mailbox gives you a real US street address with mail scanning from $15/month

Once You're Abroad

- Keep a travel log — dates in and out of every country for the Physical Presence Test

- File your federal return every year, even if you owe $0 (failure-to-file penalties apply)

- File FBAR if foreign accounts exceed $10,000 aggregate

- File Form 8938 if foreign assets exceed reporting thresholds

- Choose FEIE or FTC (or the combination strategy) based on your tax situation

- Check totalization agreements if self-employed

- Hire an expat tax specialist — this is not DIY territory for most people

Recommended Expat Tax Services

- MyExpatTaxes — Most affordable DIY software built specifically for expats

- Taxes for Expats (TFX) — 25+ years of expat-only focus

- Greenback Tax Services — Transparent pricing starting at $250 with CPAs and Enrolled Agents

The bottom line: The US makes it unnecessarily complicated to live abroad and manage your finances. But with the right knowledge, the right bank accounts, and the right tax strategy, you can legally minimize your burden to near-zero in many cases. The key is being proactive — set things up correctly before problems arise, and never, ever skip a filing. Have questions about your specific situation? Drop a comment below or reach out — this is exactly the kind of thing we help people navigate at Cash Flow Abroad.

Living in Latin America and need dollar access? ARQ Finance holds your balance in USDc and EURc stablecoins, lets you swap to local currency (MXN, COP, ARS, BRL) at real market rates, deposit USDC/USDT from external wallets, and earn up to 4% on dollar balances. No US bank account needed.

Related: zero-fee banking stack

Moving money internationally? Before you wire a single dollar through your bank, read our Expat Money Transfer Bible — it breaks down how banks charge 4-6% in hidden fees and which services cut that to under 1%.

Related: crypto tax guide for expats

Related: FEIE zero tax guide

Ready to start investing from abroad? Our Expat Investor's Playbook covers how to avoid the PFIC trap, the best brokerages for US expats in 2026, and three portfolio models built specifically for Americans living overseas.

Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently. Consult with a qualified tax professional for advice specific to your situation.This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJune 8, 2026

Expat Tax & FinanceJune 8, 2026

FBAR Explained: Which Expats Must File FinCEN 114

Who must file FinCEN Form 114 (FBAR), the $10,000 aggregate threshold, what accounts count, and how to avoid the $16,000+ non-willful penalty.

Expat Tax & FinanceJune 23, 2026

Expat Tax & FinanceJune 23, 2026

FBAR vs Form 8938: Expat Reporting Guide

US expats with foreign accounts over $10,000 must file FBAR. Learn how Form 8938 differs, current penalty amounts, and how to catch up.

Expat Tax & FinanceJune 14, 2026

Expat Tax & FinanceJune 14, 2026

FBAR: The $10,000 Trap Every Expat Must Understand

The $10,000 FBAR threshold is aggregate across all foreign accounts, not per account. Who must file, what counts, and the penalty math after Bittner.