FEIE vs Foreign Tax Credit: Pick the Wrong One, Pay Thousands

Most US expats know about the Foreign Earned Income Exclusion. The FEIE versus Foreign Tax Credit decision isn't about which option sounds better.

Most US expats know about the Foreign Earned Income Exclusion. The FEIE versus Foreign Tax Credit decision isn't about which option sounds better.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Most US expats know about the Foreign Earned Income Exclusion. Fewer know it can cost them $14,000 a year they never see coming — while a different form sitting in the same tax code would have wiped out that bill entirely. The FEIE versus Foreign Tax Credit decision isn't about which option sounds better. It's about matching the right tool to your country, your income, and your long-term wealth goals. Pick wrong and you're either leaving serious money on the table or, worse, paying taxes you didn't have to.

This is a comparison post for people who've already heard the abbreviations. We're going to cut straight to the dollar math.

How Each Election Actually Works

The Foreign Earned Income Exclusion (FEIE) lets you exclude up to $130,000 of foreign earned income from your US taxable income in 2025 (up from $126,500 in 2024). You claim it on Form 2555. The excluded income simply doesn't appear as taxable on your 1040. Married couples where both spouses qualify can double it — $260,000 combined in 2025.

To qualify, you need to pass either the Bona Fide Residence Test (established residency in a foreign country for a full tax year) or the Physical Presence Test (330+ days outside the US in any consecutive 12-month period). FEIE only applies to earned income — wages, salaries, self-employment net profit. Dividends, capital gains, rental income, and passive income don't qualify.

The Foreign Tax Credit (FTC) works differently. Instead of removing income from your return, it lets you apply foreign taxes you've already paid as a dollar-for-dollar credit against whatever US tax you'd otherwise owe. Filed on Form 1116. Pay $28,000 in German income tax on $80,000 of wages? That $28,000 offsets up to $28,000 of US tax on the same income. Unused credits can carry back one year and forward ten.

FTC covers more income types than FEIE — you can claim it against foreign taxes on dividends, rental income, and capital gains using separate "baskets" on Form 1116. FEIE never touches passive income; FTC can.

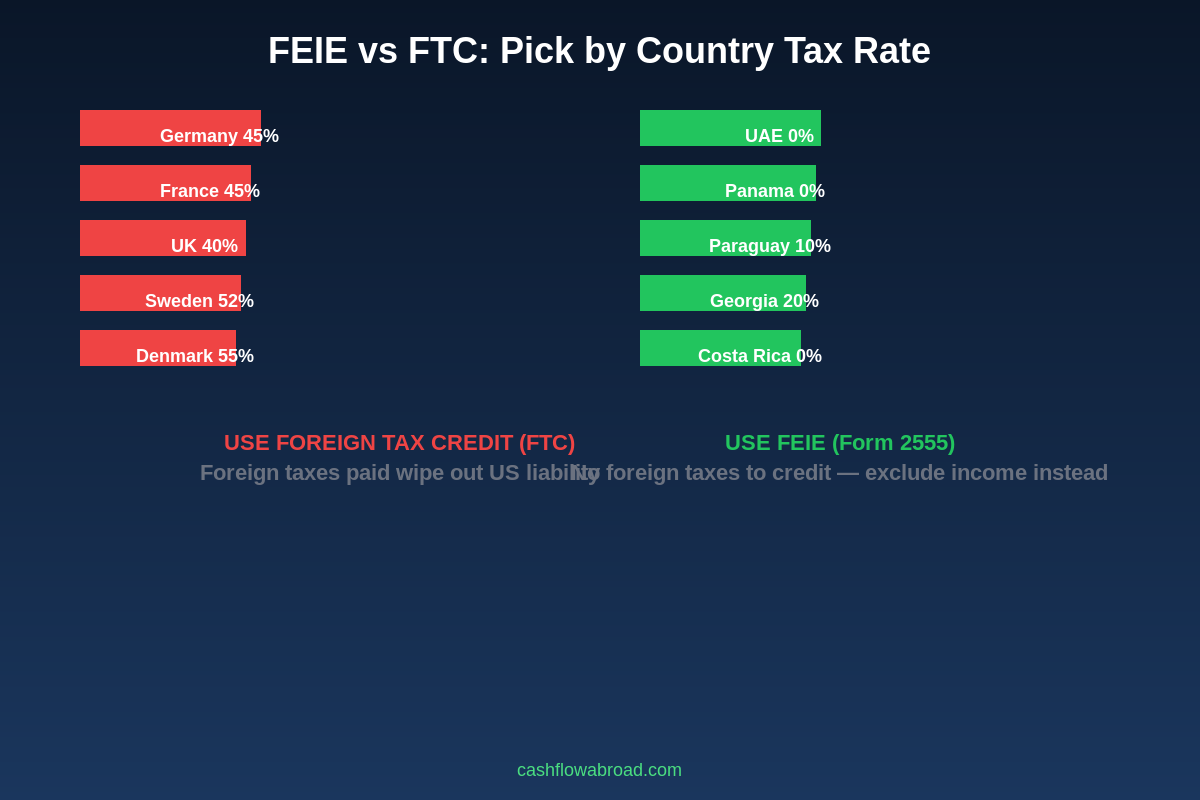

The Country You're In Largely Decides This

This one rule covers the majority of cases: if your host country taxes you at rates close to or above US rates, use the FTC. If your host country barely taxes you (or doesn't at all), use FEIE.

The logic is mechanical. The FTC's power is proportional to what you actually paid abroad. If Germany took 42% of your income, that's a massive credit to deploy against a US bill that tops out at 37%. The credit exceeds your US liability — you owe nothing, and the leftover carries forward. But if you live in Dubai where the income tax rate is zero, the FTC gives you nothing because you have zero foreign taxes to credit. FEIE is the only lever you have.

| Country | Top Income Tax Rate | Best Election | Reason |

|---|---|---|---|

| Germany | 45% + solidarity surcharge (~47%) | FTC | Foreign taxes exceed US rates — credit wipes liability |

| France | 45% + social charges (~55%) | FTC | Massive credit surplus, often generates carryforward |

| UK | 40–45% | FTC | High earners see complete US offset |

| Sweden / Denmark | 52–55% | FTC | Highest tax burden in the table |

| UAE / Qatar / Bahrain | 0% | FEIE | No foreign taxes exist — FTC useless |

| Panama | 0% on foreign-source income | FEIE | Territorial system: foreign income exempt locally |

| Paraguay | 10% on local income / 0% foreign | FEIE | Low FTC credit — FEIE exclusion more powerful |

| Georgia | 20% flat (1% micro-business) | Usually FEIE | FTC credit too small to zero out US liability alone |

| Mexico / Colombia | 15–35% / 0–39% | Evaluate case by case | Mid-range rates — run the numbers both ways |

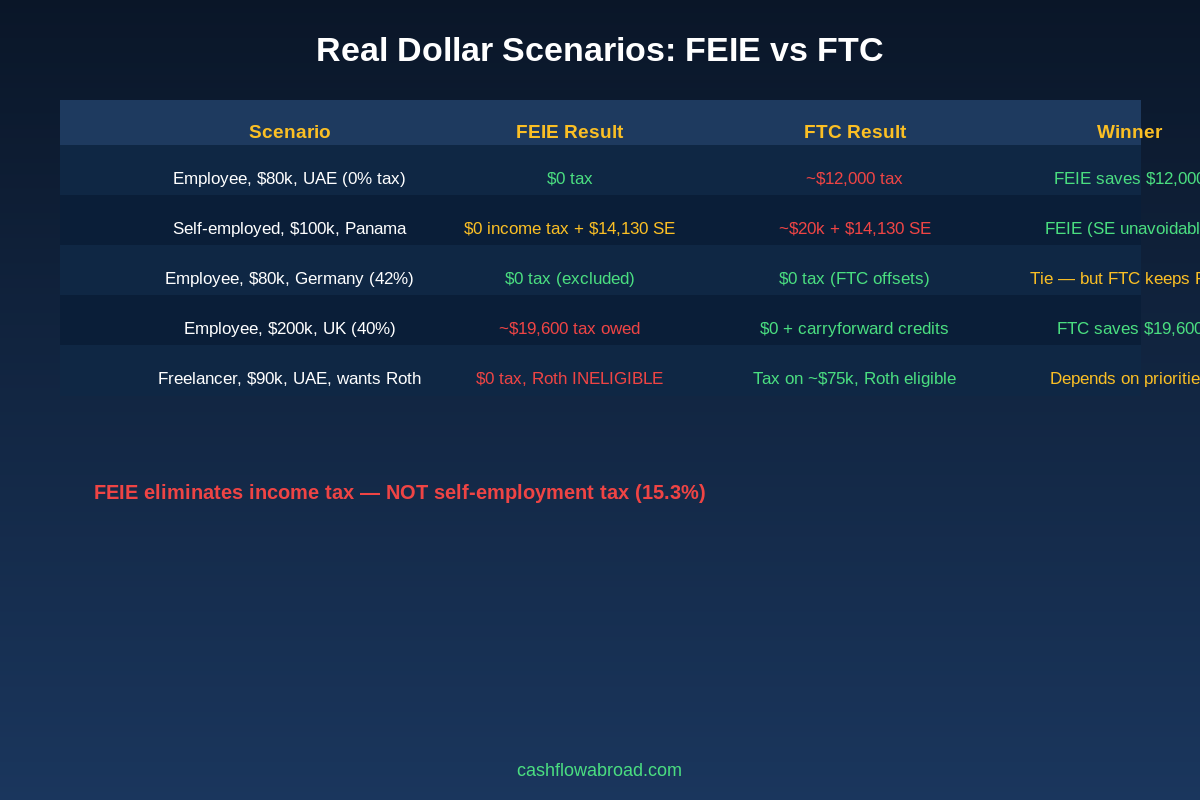

What This Looks Like in Real Dollars

Scenario A — Employee, $80,000 salary, Dubai, 0% local tax:

FEIE excludes the full $80,000. Federal income tax: $0. FTC option: $0 foreign taxes paid means zero credit; US tax on $80,000 (single, after standard deduction ~$15,000) runs roughly $12,000–$14,000. FEIE wins by $12,000+.

Scenario B — Employee, $200,000 salary, UK (paid ~$72,000 in UK income tax):

With FEIE alone: exclude $130,000, leave $70,000 taxable — pushed to a higher bracket by the stacking rule (more below), owing roughly $19,600. With FTC: $72,000 UK taxes paid against ~$40,000 US tax liability = zero US tax owed, plus $32,000 in carryforward credits. FTC saves $19,600 and generates carryforward surplus.

Scenario C — Freelancer, $100,000, Panama, 0% local tax:

FEIE excludes the $100,000 from federal income tax. Federal income tax: $0. Self-employment tax at 15.3% on $92,350 (net of the SE deduction): $14,130 — still owed regardless. FTC option: $0 credits available, income tax bill of roughly $14,000–$16,000 on top of the same $14,130 SE tax. FEIE still wins on income tax, but the SE tax is unavoidable either way.

The SE Tax Trap Nobody Tells You About

This is where a lot of expat freelancers get blindsided. The FEIE eliminates your income tax liability on excluded earnings. It does absolutely nothing for self-employment tax — the 15.3% payroll tax covering Social Security (12.4%) and Medicare (2.9%).

The SE tax base for 2025 runs up to the Social Security wage base of $176,100, with 2.9% Medicare continuing above that. On $100,000 of net freelance income in a zero-tax country:

- FEIE exclusion reduces federal income tax to $0 ✓

- SE tax on $100,000 × 92.35% × 15.3% = $14,130 still owed ✗

The FTC doesn't fix this either. The only clean escape is a US Totalization Agreement with your host country — these redirect social security contributions to one system only. The US has agreements with roughly 30 countries including Germany, the UK, France, Australia, Canada, and Japan. Notable gaps: UAE, Panama, Paraguay, and Georgia all lack totalization agreements. If you're self-employed in one of those countries, SE tax is the cost of doing business, no matter which election you pick.

Our guide on the expat investor's playbook covers how entity structure interacts with these elections for high earners.

FEIE's Hidden Roth IRA Problem

This one costs expats six figures in retirement wealth without them realizing it until years later.

IRA contributions — Roth or Traditional — require taxable earned income equal to or exceeding the contribution amount. When you use FEIE to exclude all your foreign earned income, that income disappears from your US return. The IRS treats your "compensation" for IRA eligibility as $0. With $0 compensation, you cannot contribute to a Roth IRA that year. If you already contributed, you've made an excess contribution — subject to a 6% annual excise tax until corrected on Form 5329.

The math on this over a career is stark:

- $7,000/year Roth IRA contribution (2025 limit)

- 8% average annual return over 30 years

- Missed compounding: roughly $793,000 in tax-free retirement assets

- Miss just 10 of those years: ~$265,000 in lost wealth

The FTC avoids this problem entirely. Because FTC keeps income on your return (it reduces tax owed, not income reported), your compensation figure stays intact and you remain IRA-eligible.

There is one counterintuitive silver lining if you're all-in on FEIE: if the exclusion zeros out your US taxable income, you can convert Traditional IRA funds to a Roth at a 0% federal tax rate that year. It's a legitimate strategy for expats with existing pre-tax retirement accounts. But it's a one-time conversion opportunity, not a substitute for ongoing Roth contributions.

When You Can Use Both: The Stacking Rule

If you earn above the FEIE ceiling — $130,000 in 2025 — you can combine both elections. Apply FEIE to exclude the first $130,000, then use FTC to offset foreign taxes on earnings above the cap. The rule: you can't claim a credit for taxes on income you've already excluded. But you can apply the proportional foreign taxes on the above-cap portion.

The catch: under IRC §911(f), the IRS doesn't let the excluded FEIE income occupy your lower tax brackets. Your above-cap income gets taxed as if the excluded $130,000 sits underneath it — pushing you into higher marginal rates than the dollar amount alone would suggest. For high earners with moderate foreign tax rates (say, 20–25%), pure FTC can sometimes beat stacking. Run both calculations — the gap is often $5,000–$15,000.

The 5-Year Lock-In You Cannot Ignore

Once you revoke the FEIE — either via a written statement or by simply not filing Form 2555 — you cannot re-elect it for five years without IRS permission. Getting that permission requires a Private Letter Ruling: currently $43,700 for most taxpayers (reduced to $3,450 if gross income is under $250,000). The IRS can deny it.

This means switching from FEIE to FTC is a long-term commitment. Sensible if you've permanently relocated to Germany. A costly mistake if you're in a high-tax country temporarily before moving back to Panama or the UAE.

Going the other direction carries no lock-in — you can elect FEIE at any time on a qualifying return without penalty. The asymmetry matters: default to caution before revoking FEIE if your long-term country isn't settled.

The Decision Framework

| Your Situation | Best Election | Key Reason |

|---|---|---|

| Zero-tax country (UAE, Panama, Qatar) | FEIE | No foreign taxes to credit — exclusion is only option |

| High-tax country (Germany, UK, France) | FTC | Foreign taxes paid exceed or match US rates |

| High earner ($130k+) in low-tax country | FEIE + FTC stacking | Exclude first $130k, credit taxes on the rest |

| Self-employed in zero-tax country | FEIE | SE tax unavoidable — minimize income tax separately |

| Want to fund Roth IRA, income under FEIE cap | FTC | FEIE zeroes out IRA-eligible compensation |

| High earner in high-tax country | FTC | Often generates surplus credits to carry forward |

| Planning to move countries in 2–3 years | Be cautious before revoking FEIE | 5-year lock-in makes re-election expensive |

One note on passive income: if you earn significant dividends, interest, capital gains, or rental income, run Form 1116 regardless of which election you use for earned income. FEIE never applies to passive income — FTC is the only mechanism to offset foreign taxes on those income baskets.

Tools That Support Either Strategy

Whichever election you use, a few tools make the financial infrastructure work. Charles Schwab International remains the benchmark for expat banking and brokerage — zero foreign transaction fees, worldwide ATM fee reimbursements, and an account that doesn't close simply because you moved abroad (unlike Fidelity and Vanguard, which routinely do).

For US business banking while abroad, Mercury requires no branch visits, integrates with US accounting software, and is compatible with LLCs and S-corps for freelancers managing the SE tax issue through entity structure.

To maintain a US address for IRS correspondence, banking, and state domicile, a virtual mailbox is non-negotiable. Traveling Mailbox provides a real US street address in 50+ cities, mail scanning, and check deposits for $15/month — the full breakdown is in our virtual mailbox guide. For international money movement, Remitly handles transfers without the hidden markup structure embedded in most bank wire fees.

Bottom Line

The FEIE versus Foreign Tax Credit decision comes down to three variables: where you live, how much you earn, and whether Roth IRA eligibility matters to your retirement plan. In zero-tax countries, FEIE wins clearly — FTC has nothing to work with. In high-tax countries, FTC wipes your US liability and often generates carryforward credits. The traps to budget for: SE tax (15.3%) survives both elections in countries without totalization agreements; FEIE eliminates Roth eligibility for lower earners; and revoking FEIE triggers a five-year lock-in that costs $3,450 to $43,700 to undo.

For straightforward situations — employee income, clear country — you can handle this yourself with Form 2555 or Form 1116. For self-employment, incomes above the exclusion ceiling, or significant Roth contribution plans, a qualified expat CPA running both scenarios is worth the fee before you file.

Further reading: Zero Federal Income Tax as a US Expat | Complete FBAR, FATCA & FEIE Guide | Expat Investing Playbook

Disclaimer: This post is for informational purposes only and does not constitute legal or tax advice. Tax laws change and individual circumstances vary significantly. Consult a qualified US expat tax professional before making any elections on your return. The 5-year lock-in and PLR fees referenced reflect rules in effect as of 2025.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJuly 4, 2026

Expat Tax & FinanceJuly 4, 2026

Canadian TFSA and US Taxes: The Reporting Trap

US citizens holding a Canadian TFSA owe tax on all annual growth and must file Form 3520 — PFIC rules apply to Canadian mutual funds inside the

Expat Tax & FinanceJuly 4, 2026

Expat Tax & FinanceJuly 4, 2026

State Income Tax for Expats: Which States Follow You

California, New York, and Virginia keep taxing Americans abroad. Learn which states follow you, what triggers audits, and how to exit cleanly.

Expat Tax & FinanceJuly 3, 2026

Expat Tax & FinanceJuly 3, 2026

FBAR: The $10,000 Expat Rule Most People Get Wrong

FBAR: when any foreign account aggregate hits $10,000 during the year, all accounts must be reported. Penalties, Bittner ruling, and catch-up