State Domicile for Expats: Avoid the States That Chase You Abroad

California has 300+ auditors hunting former residents. Here's how to change state domicile before moving abroad and save 0,000–0,000+ per year in avoidable state taxes.

California can tax your foreign income at 13.3% even after you leave. Learn how to change state domicile and save 5,000+ per year as a US expat.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

California employs over 300 dedicated residency auditors whose only job is to find former residents who left the state — and then prove they never really left. They subpoena cell phone records. They pull credit card statements. They reconstruct your whereabouts day by day. And if you fail to meet their strict requirements for breaking state ties, they can tax every dollar you earned abroad at up to 13.3% — even income you already excluded under the Federal Foreign Earned Income Exclusion.

Most expats obsess over federal taxes. Smart expats look at their state first, because getting this wrong can cost $10,000–$16,000 per year on a $150,000 income — and the bill can arrive years after you moved.

Domicile vs. Residency: Why the Difference Matters

These two terms sound interchangeable but carry completely different legal weight. Residency is where you physically live. Domicile is your permanent home — the place you intend to return to. You can only have one domicile at a time, and it persists until you actively replace it with another.

This is why someone who leaves California for Bangkok on day one of a two-year contract can still owe California income tax on every paycheck. They moved. They didn't change their domicile.

The legal distinction plays out in audits. If a state can show that you considered yourself "from" a place — your voter registration, your driver's license, your family home, your social ties, your professional licenses — they can argue your domicile never changed. Some states are far more aggressive than others about making that argument.

The Sticky States: Who Chases Expats Abroad

Not all states are equal. These five create the most friction for expats:

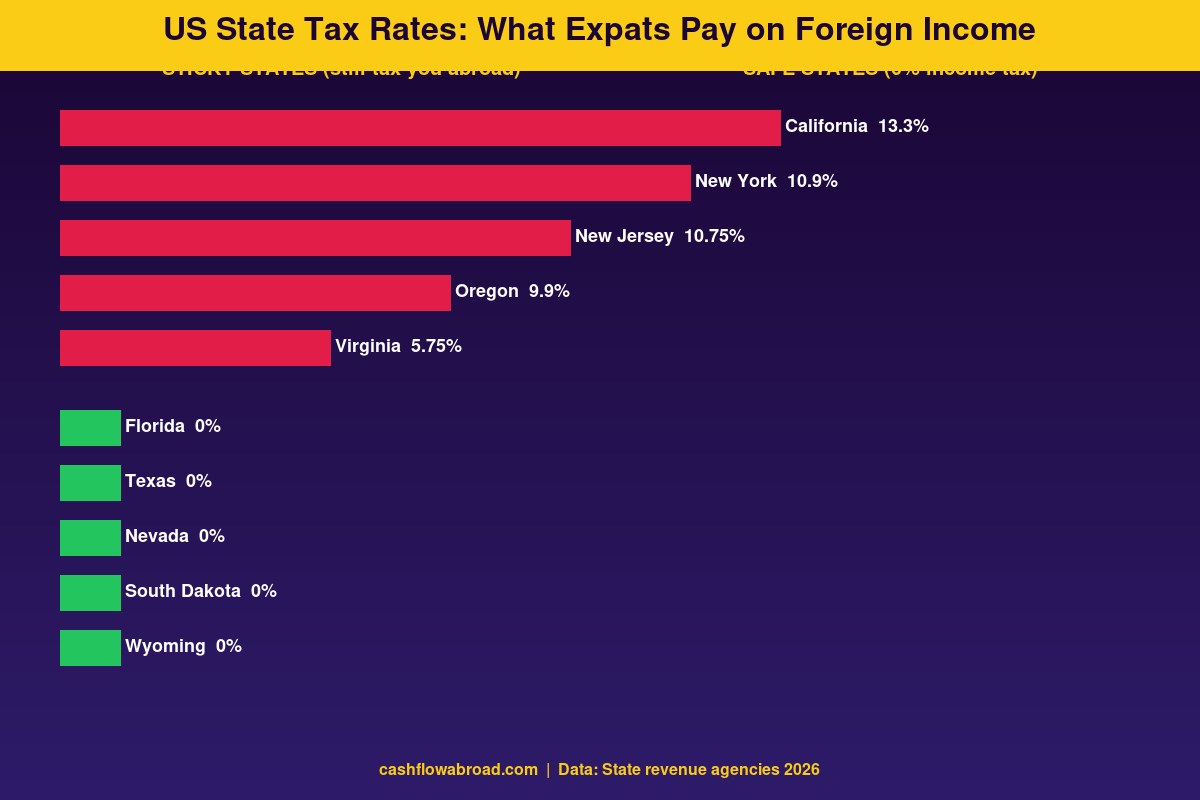

California — 13.3% Rate, 300+ Auditors, Subpoena Power

California's Franchise Tax Board (FTB) is the most aggressive tax authority in the US outside the IRS itself. The state's top marginal rate of 13.3% — the highest in the nation — creates a powerful incentive for it to pursue former residents, and it has the resources to do it.

The FTB Residency Audit Unit has over 300 dedicated auditors. They can subpoena your phone carrier for location data, request your airline records, pull your hotel stays, and cross-reference your credit card usage to reconstruct a day-by-day picture of how much time you actually spent in California.

The practical consequences are steep. A single expat earning $150,000 in foreign income who fails to properly break California ties could owe $13,000–$16,000 in California state tax per year. The FTB can audit up to four years back (six years if it believes you underreported by 25% or more).

California does have a 546-day safe harbor: if you're outside California under an employment contract for at least 546 consecutive days, your intangible income during that period may be exempt — but only if your intangible income (dividends, capital gains, etc.) stays under $200,000 per year, and your return visits to California don't exceed 45 days per tax year. One slip in any condition and the safe harbor disappears.

The most instructive case is Appeal of Bracamonte (2021). The taxpayers moved to Nevada shortly before selling their business for $16.7 million and claimed Nevada residency for the gain. The OTA found insufficient evidence of genuine domicile change and assessed $1.59 million in California tax. The lesson: establishing domicile requires a pattern of behavior, not a rushed move timed to a liquidity event.

New York — 10.9% Rate, 183-Day Trap, Thousands of Audits Annually

New York uses a two-pronged approach. You're a New York resident if: (a) your domicile is New York, or (b) you maintain a permanent place of abode there and spend more than 183 days in the state. The second prong is the "statutory residency" trap that catches expats who keep apartments in Manhattan.

The state conducts thousands of active residency audits per year. Unlike California's "totality of contacts" test, New York requires you to prove a domicile change by "clear and convincing evidence" — a higher legal bar than most states. Add the NYC local tax (up to 3.876%) and combined state/city exposure on a $200,000 income approaches $29,520 per year.

Virginia, New Jersey, South Carolina

Virginia taxes residents at 5.75% and applies an aggressive domicile standard similar to California's. New Jersey's top rate is 10.75%. South Carolina is less aggressive but notable because it requires a formal declaration of intent to abandon domicile — simply leaving isn't enough.

How to Actually Break State Ties Before You Leave

Courts and state tax authorities evaluate domicile changes through a "closest connections" test. These are the actions that matter most — roughly in order of weight:

- Sell or vacate your home. Keeping real property in a sticky state — even a rental — creates a maintained "place of abode" that can trigger statutory residency tests. If you rent, end the lease before you leave.

- Change your driver's license. In your new state if you're establishing domicile there, or at minimum surrender the sticky-state license. An active driver's license is a primary domicile indicator in audits.

- Update voter registration. Re-register in a zero-tax state. This is treated as an explicit declaration of where you consider home.

- Change your banking address of record. Update your bank, brokerage, and investment account addresses to your new domicile. California FTB has information-sharing agreements with major financial institutions.

- Update professional licenses and memberships. Bar memberships, medical licenses, professional associations — transfer or terminate.

- File a final part-year return. File formally as a part-year resident for the year you leave, documenting the exact date of your domicile change.

- Get a Declaration of Domicile if available. Florida lets you file a legal declaration of domicile in your county courthouse. It's not conclusive but creates a formal record.

What you do before leaving matters as much as what you do after. A pattern of behavior established months in advance — not a rushed checklist the week before your flight — is what survives audit scrutiny.

The Best States to Call Home While Living Abroad

Nine US states have no income tax: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. For expats, not all are equally useful:

| State | Income Tax | Ease of Domicile Setup | Notes for Expats |

|---|---|---|---|

| Florida | 0% | High | Declaration of Domicile filing available; large expat community; easy banking |

| Texas | 0% | High | No state filing requirement; many expat-friendly banks headquartered here |

| South Dakota | 0% | Very High | Popular perpetual traveler state — domicile possible with a single overnight stay |

| Nevada | 0% | High | No state return required; straightforward with driver's license + address |

| Wyoming | 0% | High | Minimal oversight; popular for LLC holding structures |

South Dakota deserves a separate mention for perpetual travelers. The state allows you to establish domicile with a single overnight stay and a few administrative steps. A large community of full-time nomads and long-term expats use SD as their official home state. There's no requirement to maintain a physical residence — a virtual mailbox address is widely accepted for vehicle registration, driver's license, and voter registration purposes.

Florida is the most practical choice for most expats because of its size, the availability of physical mail services, and the formal Declaration of Domicile filing at county courthouses — which gives you a timestamped legal record that survives audit scrutiny.

Keeping a US Address While Living Abroad

One of the practical challenges of establishing domicile in a zero-tax state while living abroad is maintaining a legitimate US street address. This is not optional — your bank accounts, IRS correspondence, state DMV registration, and professional licenses all require a real street address, not a P.O. box.

A virtual mailbox solves this. Services like Traveling Mailbox give you a real US street address in 50+ cities — including addresses in Florida, Texas, South Dakota, and other zero-tax states — with mail scanning, forwarding, and check deposit. At around $15/month, it's the most affordable domicile anchor available. When you're establishing domicile in Florida or Texas before your move, a virtual mailbox address in that state lets you update all financial accounts well before you physically arrive to complete the paperwork. See our full guide on virtual mailboxes for expats for a detailed breakdown.

What Actually Triggers a State Tax Audit

State revenue agencies receive information from multiple sources. These are the most common audit triggers for expats:

- IRS information sharing. When the IRS updates your address to a foreign country, that data flows to states. California and New York have formal information-sharing agreements with the IRS.

- Financial institution reporting. If you update your brokerage or bank address to a foreign address while still showing a sticky-state address on your state return, that inconsistency flags the file.

- High-income departure. Both California and New York specifically audit high-income taxpayers who file part-year returns or switch to nonresident status. Income above roughly $400,000 in the departure year is a near-automatic review.

- Sale of state-sourced assets. Capital gains from California real estate, business interests, or California-company stock options are taxable by California regardless of where you live when they're realized. Filing that income as a nonresident triggers review.

- Prior-year filings as a resident. If you filed as a California or New York resident for years and then suddenly file as a nonresident, expect scrutiny on whether the domicile change was genuine.

The Dollar Gap: Zero-Tax vs. Sticky State

Here's what the annual state tax difference looks like across income levels, comparing California (up to 13.3%) to Florida (0%):

| Annual Foreign Income | California Tax Owed | Florida Tax Owed | Annual Savings with FL Domicile |

|---|---|---|---|

| $80,000 | ~$7,400 | $0 | $7,400 |

| $120,000 | ~$11,500 | $0 | $11,500 |

| $150,000 | ~$14,800 | $0 | $14,800 |

| $200,000 | ~$20,600 | $0 | $20,600 |

This is the annual difference — recurring, compounding every year you live abroad. A 10-year stint with $150K income and California domicile costs roughly $148,000 in avoidable state tax versus Florida domicile. That's not a minor compliance detail — that's a material wealth decision made by default.

Note that the Federal Foreign Earned Income Exclusion (FEIE) — which excludes up to $130,000+ in foreign-earned income from federal tax — has zero effect on state taxes. California and New York don't recognize the FEIE. Every dollar you exclude federally is still fully taxable by a sticky state if you maintain domicile there. See our complete guide to zero federal income tax using the FEIE for the federal side of this calculation.

State Domicile and Your US Banking Setup

Establishing domicile in a zero-tax state before moving abroad isn't just a tax move — it also determines which financial accounts remain accessible to you. Many banks and brokerages restrict or close accounts when they detect a foreign address on file, but they generally accept a US address in a zero-tax state without issue.

Charles Schwab International is one of the few US brokerages explicitly friendly to expats: they permit account maintenance with a foreign address after initial setup, charge no foreign ATM fees, and reimburse foreign ATM surcharges globally. Establishing your Schwab account with a Florida or Texas address before you move is the cleaner path. For a complete overview, see our US expat banking and taxes guide.

State Taxes Are Part of the Geographic Arbitrage Calculation

Expat finance comparisons almost never factor in state taxes when calculating the savings from moving abroad. But for someone leaving New York with a $200,000 income, eliminating $20,600/year in state tax isn't just a line item — it's a month of living costs in most of Southeast Asia or Latin America.

The geographic arbitrage calculation is only complete when state domicile is part of the picture. A move from California to Thailand that doesn't include a domicile change leaves $14,000+ per year on the table. The cost of establishing Florida domicile — a few hundred dollars, a couple of afternoons, and a $15/month virtual mailbox — is recovered in the first month of savings.

Pre-Departure Domicile Checklist

If you're moving abroad from a sticky state, run through this list at least 90 days before your flight:

- Establish domicile in a zero-tax state — driver's license, voter registration, physical street address

- Set up a virtual mailbox in your chosen state for ongoing mail management

- Update all financial accounts (bank, brokerage, IRA, 401k) to the new US address

- Surrender sticky-state driver's license; obtain new-state license

- Terminate lease or make arrangements for any property in the sticky state

- File a Declaration of Domicile if in Florida (county courthouse, ~$10)

- Update professional licenses, bar memberships, and medical licenses

- File a formal part-year resident return for the departure year with the exact domicile change date

- Log days spent in former state after the change date — stay under 45 days per year for California safe harbor purposes

Conclusion

State domicile is one of the highest-leverage tax decisions a US expat can make — and it's almost entirely within your control. But only if you act before you leave. Changing domicile after the fact, or while under audit, is exponentially harder than doing it cleanly before your departure date.

Pick a zero-tax state. Do the paperwork. Get a virtual mailbox in that state. File the part-year return. Then move. The difference over a decade abroad is routinely more than $100,000 — for a setup cost measured in hundreds of dollars and a few afternoons.

Disclaimer: This post is for informational purposes only and does not constitute legal or tax advice. State domicile and residency rules are complex and vary significantly by state. Consult a qualified tax attorney or CPA who specializes in US expat taxation before making domicile changes. Tax laws change frequently — verify current rules with your state's revenue agency or a licensed professional.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJuly 4, 2026

Expat Tax & FinanceJuly 4, 2026

State Income Tax for Expats: Which States Follow You

California, New York, and Virginia keep taxing Americans abroad. Learn which states follow you, what triggers audits, and how to exit cleanly.

Expat Tax & FinanceJune 1, 2026

Expat Tax & FinanceJune 1, 2026

State Income Tax Trap Most Expats Don't See Coming

California taxes expats at 13.3% even abroad. Learn how to legally sever domicile before moving overseas and eliminate state income tax.

Expat Tax & FinanceMay 30, 2026

Expat Tax & FinanceMay 30, 2026

FBAR vs FATCA: What Every Expat Must Know

FBAR and FATCA are two separate foreign account reporting requirements with different penalties and thresholds. Learn what every US expat must file.