The Offshore Company Tax Trap Most US Expats Miss

10 min read · 2,495 words

Here’s a number that stops most expat entrepreneurs cold: $18,900. That’s what the IRS can bill a US citizen who owns a foreign company in Dubai earning $150,000 in a year — even if that company never paid them a single dollar in dividends, and even if Dubai itself levies zero corporate tax. The money sits untouched in a foreign bank account, and the IRS still wants its cut.

This is the offshore company tax trap. It catches entrepreneurs, freelancers, and remote workers who move abroad, set up a local company to minimize local taxes, and assume the IRS doesn’t follow them across the border. It does. The rules are called the Controlled Foreign Corporation (CFC) regime, and they’ve been quietly catching Americans off-guard for decades. Since 2018, a specific provision called GILTI — now renamed NCTI (Net CFC Tested Income) under the 2025 tax legislation — made it dramatically worse.

The worst part: plenty of expat lawyers and local accountants in your new country won’t warn you. They’re focused on local tax law. Your US tax obligation is an American problem, and it doesn’t disappear just because you left.

What Makes a Foreign Company “Controlled”?

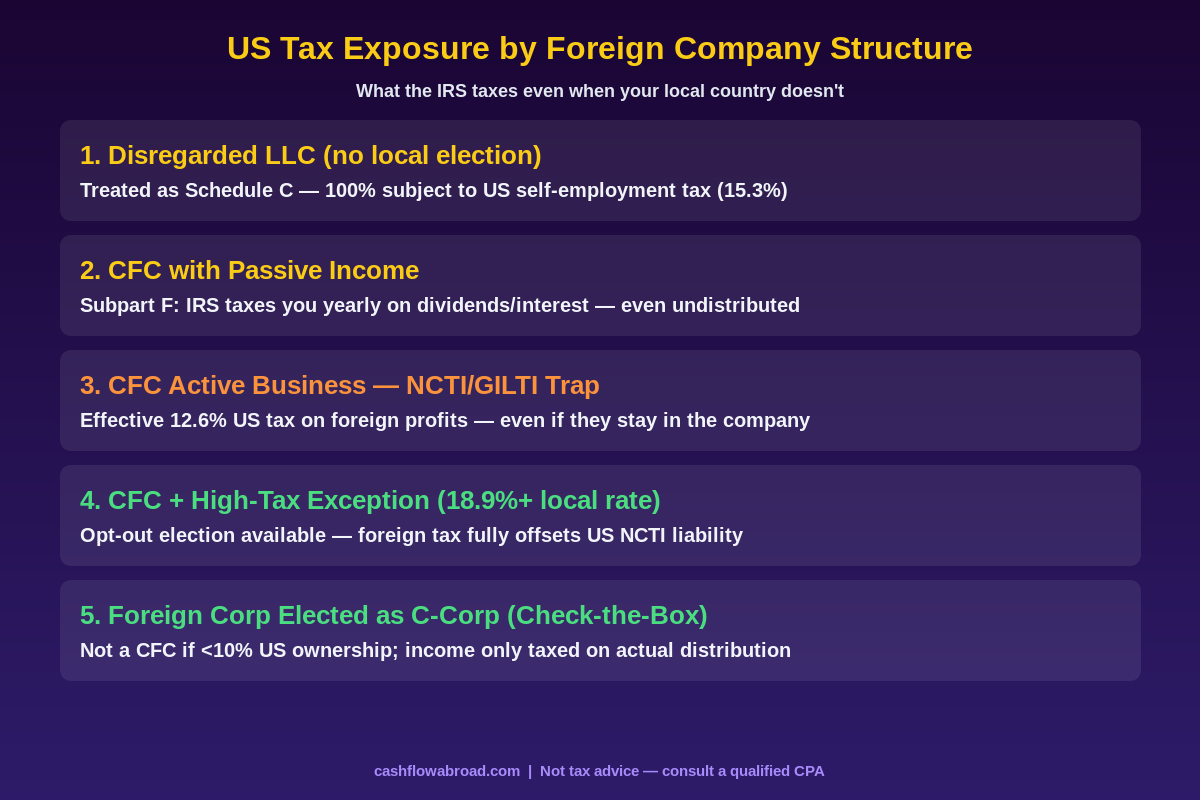

Under US tax law, a Controlled Foreign Corporation is any foreign corporation where US shareholders (each owning 10% or more) collectively own more than 50% of the company’s stock by vote or value. Most solo expat entrepreneurs own 100% of their foreign company — putting them firmly inside CFC territory.

If you own a Dubai FZCO (Free Zone Company), a Georgian LLC, a Colombian SAS, a Panama SA, a Singapore Pte Ltd, or virtually any other foreign business structure where you hold 10%+ of shares, you’re a CFC shareholder. The IRS requires you to file Form 5471 annually — and non-filing penalties start at $10,000 per year per foreign company, regardless of whether you owe any tax.

That’s before we get to the actual tax liability.

The Three Tax Traps Inside a CFC

Trap #1: Subpart F Income (Passive and Mobile Income)

Subpart F has been in the tax code since 1962. It was designed to stop US companies from parking passive income — dividends, interest, royalties, rents — in low-tax offshore entities to defer US tax indefinitely.

For expat entrepreneurs, Subpart F income includes:

- Dividends and interest earned inside the foreign company

- Royalties from intellectual property licensed through the foreign entity

- Income from “personal service contracts” where the customer specifically chose you as an individual — effectively consulting or freelance income routed through a company

- Foreign base company sales income (selling goods manufactured in a third country)

The kicker: Subpart F income is taxed to you in the year it’s earned by the foreign company, not the year you actually receive a distribution. You pay US tax on phantom income — money that may still be sitting in a foreign corporate account you haven’t touched.

Trap #2: NCTI / GILTI (Active Business Income)

The 2017 Tax Cuts and Jobs Act introduced GILTI — Global Intangible Low-Taxed Income — targeting US multinationals’ offshore profits. Expat entrepreneurs got caught in the crossfire. Starting in 2026, GILTI is renamed NCTI (Net CFC Tested Income) under the One Big Beautiful Bill Act, but the mechanism is largely the same with some key changes.

The tax applies to your CFC’s “tested income” — essentially all active business income not covered by Subpart F — above a 10% deemed return on tangible assets. For service businesses (consulting, software, content, coaching), tangible assets are near zero, meaning nearly all income qualifies as NCTI.

The effective rate: NCTI income flows through at the 21% corporate rate, with a 90% foreign tax credit allowed (increased from 80% under the new law). In a 0% tax jurisdiction, you’d owe the full amount. The effective rate on NCTI income for an individual shareholder runs approximately 12.6% going forward.

Run those numbers on a real business: A consultant in Dubai earning $200,000 through a foreign company, paying 0% local tax, could owe the IRS roughly $25,200 — annually, without ever touching the money in the account.

Trap #3: The Disregarded Entity Self-Employment Trap

Some expats skip the corporate structure entirely and form a foreign LLC, assuming it’s “simpler.” Under US tax rules, a single-member foreign LLC that hasn’t made a check-the-box election to be taxed as a corporation is a “disregarded entity” — it doesn’t exist for tax purposes. All income flows directly onto your Schedule C.

Schedule C income isn’t just subject to regular income tax. It’s also subject to self-employment tax: 15.3% on the first $176,100 of net earnings (2025 threshold), plus 2.9% Medicare on anything above that. The Foreign Earned Income Exclusion can shield roughly $126,500 from income tax, but it does not shelter self-employment tax. Many expats discover they owe $18,000–$26,000 in SE tax on foreign income they assumed was protected.

The High-Tax Exception: Your Escape Hatch

Congress built an escape hatch into NCTI for companies paying significant local corporate tax. If your CFC’s effective foreign tax rate exceeds a certain threshold, you can elect out of NCTI inclusion entirely.

Under the old GILTI rules, the high-tax exception threshold was 18.9% (90% of the 21% US corporate rate). Under the 2026 NCTI restructuring, the effective threshold shifts as the foreign tax credit allowance adjusts. The core principle: if your local effective rate is high enough to push your net US NCTI liability near zero via foreign tax credits, the election provides a clean opt-out from inclusion.

| Country | Corporate Tax Rate | High-Tax Exception Likely? | Estimated US NCTI Liability |

|---|---|---|---|

| Dubai (Free Zone) | 0% | No | ~12.6% on active income |

| Georgia (Small Business Status) | 1% | No | ~12.5% on active income |

| Panama (foreign-source income) | 0% on foreign-source | No | ~12.6% on active income |

| Singapore | 17% | Borderline | Reduced but some exposure |

| Ireland | 12.5% | No | Reduced — roughly 5% net |

| Portugal (standard) | 21% | Yes | $0 (credits offset fully) |

| Germany | ~30% | Yes | $0 (credits offset fully) |

| France | 25% | Yes | $0 (credits offset fully) |

The cruel irony: expats who move to high-tax European countries and set up local companies face zero additional US tax burden on those companies. Expats who move to the lowest-tax jurisdictions specifically to reduce their tax load — Dubai, Georgia, Paraguay — get hit hardest by NCTI.

How This Plays Out in Popular Expat Destinations

Dubai Free Zone Company (FZCO)

The pitch sounds perfect: 0% corporate tax, 0% personal income tax, full foreign ownership, a prestige business address. Thousands of US expats and remote workers have set up Dubai FZCOs in recent years.

The reality: a Dubai FZCO owned 100% by a US citizen is a CFC. Active business income it earns is tested income subject to NCTI. At $150,000 of profit, you’re looking at a US tax bill of roughly $18,900 — sent to an IRS address while you’re sitting in Dubai paying nothing to the UAE government. You need to file Form 5471 and include Form 8992 for the NCTI calculation, or face $10,000-per-year penalties on top of whatever taxes are owed.

Georgian LLC (Small Business Status)

Georgia’s 1% small business regime is the most aggressive low-tax structure in Europe. We covered Georgia’s 1% setup in detail previously. What that analysis didn’t fully address: if you own that Georgian LLC as a US person, it’s a CFC. Georgia’s 1% rate doesn’t come close to the high-tax exception threshold. The NCTI clock runs whether you knew about it or not. A Georgian LLC earning $100,000 means roughly $12,500 owed to the IRS — in addition to the $1,000 paid in Georgia.

Colombian SAS

A Colombian SAS (Sociedad por Acciones Simplificada) is one of the simplest companies to form in Latin America — about $200, same-day formation in many cases, minimal ongoing requirements. Colombia’s corporate tax rate is 35%, which does meet the high-tax exception threshold for NCTI purposes on locally-sourced income. However, if your SAS earns foreign-source income (common for remote service businesses), the effective rate on that portion may fall below the threshold, creating partial NCTI exposure. Get a CPA who understands both Colombian and US tax law before assuming you’re fully covered.

How to Actually Fix This

The Check-the-Box Election (Form 8832)

For foreign LLCs that default to disregarded entity status, filing IRS Form 8832 to elect corporate treatment changes how the entity is taxed. Instead of Schedule C income flowing through to you annually, the LLC is treated as a corporation — meaning you’re only taxed on actual distributions (dividends), not on retained earnings sitting in the company.

This doesn’t eliminate NCTI if you own a profitable foreign corporation. But it does solve the self-employment tax trap, and it gives you more control over timing. You can choose when to take distributions and at what rate to take them, rather than having the IRS calculate income inclusion automatically each year.

The Section 962 Election

Individual US shareholders of CFCs can elect under Section 962 to be taxed as if they were a domestic corporation. This lets individuals claim the same 90% foreign tax credit that C-corps use on NCTI income. For expats in jurisdictions with some local corporate tax — even 5–10% — this election can meaningfully reduce the US bill. At 10% local tax, the Section 962 election might cut your effective US NCTI rate from 12.6% to roughly 3–4%.

The catch: it requires additional complexity at filing time, and distributions of previously taxed NCTI income receive a second layer of tax treatment. Work with a CPA who specifically does Section 962 planning — most general practitioners don’t know these provisions.

Keep the Business as a US Entity

For US entrepreneurs running a service business primarily serving US clients, keeping the business as a US LLC or S-Corp while living abroad often produces a better total tax outcome than going offshore. You can still claim the Foreign Earned Income Exclusion on a reasonable salary paid to yourself, use a US business address, and avoid the CFC reporting complexity entirely.

The infrastructure to run a US business from abroad is straightforward. A Traveling Mailbox gives you a real US street address in 50+ cities, handles mail scanning and check deposits, and costs $15/month — essential for maintaining a registered agent address, IRS correspondence, and state business compliance while you’re operating from abroad. Pair it with Mercury for US business banking that works for expats: full online account management, no monthly fees on business checking, ACH and wire support, and none of the “you must come into a branch” friction that kills most expat banking setups.

Run the Total-Tax Math Before Choosing a Jurisdiction

Counter-intuitive from a local tax standpoint, but some expats specifically choose countries with corporate tax rates above the NCTI threshold to eliminate US tax liability entirely. Portugal at 21%, Germany at ~30%, France at 25% — all clear the threshold for the high-tax exception. Estonia’s unique system (corporate tax only on distributed profits, at 20% on dividends paid) can also be structured to minimize both local and US obligations depending on cash flow needs.

The math has to include both sides of the ledger. A Georgian LLC at 1% local + 12.6% US NCTI = 13.6% total effective rate. An Irish company at 12.5% local + residual US NCTI = potentially similar or less, depending on structure. A French SARL at 25% local + $0 US NCTI = 25% total. The lowest local rate isn’t always the lowest total rate once you account for NCTI. Many expat tax advisors miss this calculation entirely because they only specialize in one side.

The Reporting Stack: Forms You Can’t Ignore

CFC ownership comes with significant annual reporting obligations beyond the tax payment itself:

| Form | What It Covers | Penalty for Non-Filing |

|---|---|---|

| Form 5471 | Annual CFC information return — structure, financials, transactions | $10,000/year per company minimum |

| Form 8992 | NCTI/GILTI calculation and inclusion amount | 20%+ accuracy penalties on underpayment |

| FinCEN 114 (FBAR) | Foreign bank accounts if combined balance exceeds $10,000 | Up to $10,000/year non-willful; criminal for willful |

| Form 8938 (FATCA) | Foreign financial assets above $50K–$400K thresholds | $10,000 to $50,000 |

| Form 926 | Cash or property transferred to a foreign corporation | 10% of transferred amount |

The complete picture of US expat banking and compliance obligations — including how FBAR and FATCA interact with your foreign company structure — is covered in our US Expat Banking & Taxes guide. The reporting is genuinely complex, and the penalties for ignoring it are severe even when no actual tax is owed.

For expats with crypto held inside or transacted through their foreign company, the picture gets even more complicated. Crypto transactions in a CFC may create additional Subpart F inclusions or NCTI exposure depending on how the activity is characterized. Our crypto taxes for US expats guide covers the intersection of crypto and expat tax rules in detail.

If You Already Have a Foreign Company: What to Do Now

If you set up a foreign company thinking it was a clean solution and are now reading this with a sinking feeling, you have options — but the window to use some of them cleanly narrows the longer you wait.

Back-file Form 5471 under the Delinquent International Information Returns Submission Procedures. The IRS has a formal amnesty-adjacent program for people who missed CFC filings without fraudulent intent. Submit the delinquent forms with an explanation, and the IRS typically waives penalties in the initial cycle. This window tends to close if the IRS contacts you first or if your return gets flagged during processing.

Hire a CPA who specializes in expat corporate tax, not just expat personal returns. There’s a meaningful difference. Firms like Greenback Tax Services, Taxes for Expats, and US Tax Help have practitioners who handle Form 5471 and Section 962 elections regularly. A general CPA who “also does expat returns” may not know these provisions exist — ask directly whether they’ve filed Form 8992 before hiring them.

Run the restructure math before dissolving anything. Winding down a CFC can trigger a “deemed distribution” — one last tax event where accumulated earnings are treated as paid out to you. Plan the exit with a professional. Sometimes it’s worth taking the NCTI hit for one more year while structuring an optimal wind-down that minimizes the total exit tax.

For expats building investment portfolios alongside their business, the related PFIC trap catches people who hold foreign mutual funds or ETFs inside their investment accounts. Our Expat Investor’s Playbook covers the PFIC regime — a different but equally punishing tax structure that affects expat investors who don’t use US-based brokerage accounts.

The Bottom Line

The promise of setting up a foreign company to cut your tax bill isn’t false — it’s incomplete. The US tax code specifically anticipated that Americans would try to use foreign corporate structures to defer or eliminate US tax, and the CFC regime represents decades of legislative countermeasures designed to prevent exactly that.

Foreign companies still make sense for US expats in the right circumstances. A Dubai FZCO is genuinely useful for certain purposes. A Georgian LLC at 1% can still outperform other structures once you net out the NCTI and weigh against alternatives. But the structure has to be chosen deliberately, with full awareness of what follows you across the border.

The expats who get this right tend to share one trait: they hire a US expat CPA before forming the foreign entity, not two years after. That consultation runs $500–$2,000. The cost of getting it wrong can run to five figures annually — compounded, with penalties.

Financial Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. US international tax law is complex and fact-specific. Tax rules change frequently — particularly in 2025–2026 as GILTI transitions to NCTI. Consult a qualified tax professional with specific experience in US expat corporate taxation before making any decisions about foreign company structures, CFC elections, or restructuring strategies.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.