Dubai's 0% Tax: What US Expats Actually Pay

The year I first heard "Dubai has zero income tax," I spent twenty minutes on Google Flights before my accountant called me back.

The year I first heard "Dubai has zero income tax," I spent twenty minutes on Google Flights before my accountant called me back.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

The year I first heard "Dubai has zero income tax," I spent twenty minutes on Google Flights before my accountant called me back. She wasn't impressed. "You still file a US return," she said. "You still owe the IRS. And no, there's no treaty to help you."

That's the conversation nobody has before they book a one-way ticket to the UAE. Dubai's 0% personal income tax is completely real — but for US citizens, the calculation is more complicated than the headline suggests. The good news: if you structure things correctly, you can genuinely pay close to $0 in combined taxes. The bad news: getting it wrong is expensive, and the IRS doesn't care where your apartment is.

This guide covers the actual math — UAE tax rules, how the US taxes you abroad, what the Foreign Earned Income Exclusion does (and doesn't) cover, what it really costs to live there, and whether Dubai makes financial sense as a long-term base.

How the UAE Tax System Actually Works

The UAE levies zero personal income tax on wages, salaries, and freelance income. There is no capital gains tax, no inheritance tax, and no wealth tax. For most residents — local and foreign alike — the effective tax rate on earned income is 0%.

That's not the whole picture. A few taxes do exist:

- Corporate tax (since June 2023): 9% on taxable business income exceeding AED 375,000 (~$102,000 USD). Income below that threshold: 0%. Small businesses with revenue under AED 3 million can elect 0% under a simplified regime.

- Free zone entities: Companies operating in one of the UAE's 40+ free zones — including DMCC, DIFC, and Dubai Internet City — maintain 0% corporate tax on qualifying income, provided they meet substance requirements and don't transact heavily with the mainland UAE market.

- VAT: 5% on most goods and services, introduced in 2018. Low by global standards but worth factoring into your cost model.

- Property transfer fee: 4% of the property value in Dubai, paid at the time of purchase. No annual property tax after that.

- Excise tax: 50-100% on tobacco, energy drinks, and carbonated beverages.

The corporate tax introduction in 2023 changed the calculus for business owners. Running a profitable company through mainland UAE now has a 9% rate above $102K in profit — still far below US federal rates, but no longer zero. Free zone structures remain attractive for businesses with primarily international revenue.

The American Catch: You Still File With the IRS

The United States taxes its citizens on worldwide income regardless of where they live. This is almost unique among developed nations — only Eritrea operates a comparable system. Moving to Dubai eliminates UAE taxes. It does not eliminate your US tax obligations.

Making this harder: there is no tax treaty between the US and UAE. Most countries that attract expats — Germany, France, UK, Japan — have bilateral agreements with the US that prevent double taxation and define which country gets to tax which types of income. The UAE has no such deal. You're working with the standard US rules, nothing more.

That means the two main tools available to you are:

- The Foreign Earned Income Exclusion (FEIE) — excludes a portion of your foreign earned income from US taxable income

- The Foreign Tax Credit — credits foreign taxes paid against your US liability

Because the UAE has no income tax, the Foreign Tax Credit gives you nothing to work with — you paid $0 to UAE, so there's nothing to credit. The FEIE is where the real planning happens.

The FEIE Fix: How to Actually Reach $0 Combined

The Foreign Earned Income Exclusion lets you exclude up to $130,000 of foreign earned income from US taxes in 2025 (this figure adjusts for inflation annually). To qualify, you must meet one of two tests:

Physical Presence Test: Be outside the US for 330 full days in any consecutive 365-day period. The days don't have to be in the UAE — they just can't be in the US. This is the more commonly used test for expats who haven't established full residency yet.

Bona Fide Residence Test: Be a bona fide resident of a foreign country for an uninterrupted period that includes an entire tax year. Harder to qualify for, but more flexible once established — you can visit the US without the 35-day hard cap that the Physical Presence Test implies.

On top of the FEIE, you can claim the Foreign Housing Exclusion — which lets you deduct qualifying housing expenses above a base amount (~$20,000/year for most locations). Dubai has a higher housing cost limit than most cities, meaning you can typically exclude an additional $15,000–$25,000 in rent payments beyond the base threshold.

Here's what the numbers look like for a self-employed consultant earning $150,000:

| Scenario | Gross Income | FEIE Exclusion | Housing Exclusion | US Taxable Income | Estimated US Tax |

|---|---|---|---|---|---|

| Dubai expat (FEIE + Housing) | $150,000 | -$130,000 | -$15,000 | $5,000 | ~$500 |

| Dubai expat (FEIE only) | $150,000 | -$130,000 | — | $20,000 | ~$2,200 |

| US resident (California) | $150,000 | — | — | $150,000 | ~$57,900 |

The gap is real. A $55,000+ annual tax advantage is not hypothetical — it's the arithmetic for self-employed Americans who move abroad and qualify for FEIE. But there's a structural quirk worth knowing: the FEIE phases out Roth IRA contribution eligibility and creates a "stacking" issue where income above the exclusion gets taxed at higher marginal rates than you'd expect. See our FEIE vs. Foreign Tax Credit breakdown for the full decision tree, and how to get to zero federal tax legally as an expat.

One more trap that catches freelancers: self-employment tax is not covered by the FEIE. The 15.3% self-employment tax (Social Security + Medicare) applies to net self-employment income regardless of the exclusion. At $130,000 of excluded income, that's potentially $19,890 in SE tax you still owe. The Foreign Housing Exclusion and business expense deductions can reduce the base, but it rarely goes to zero without restructuring into a corporation.

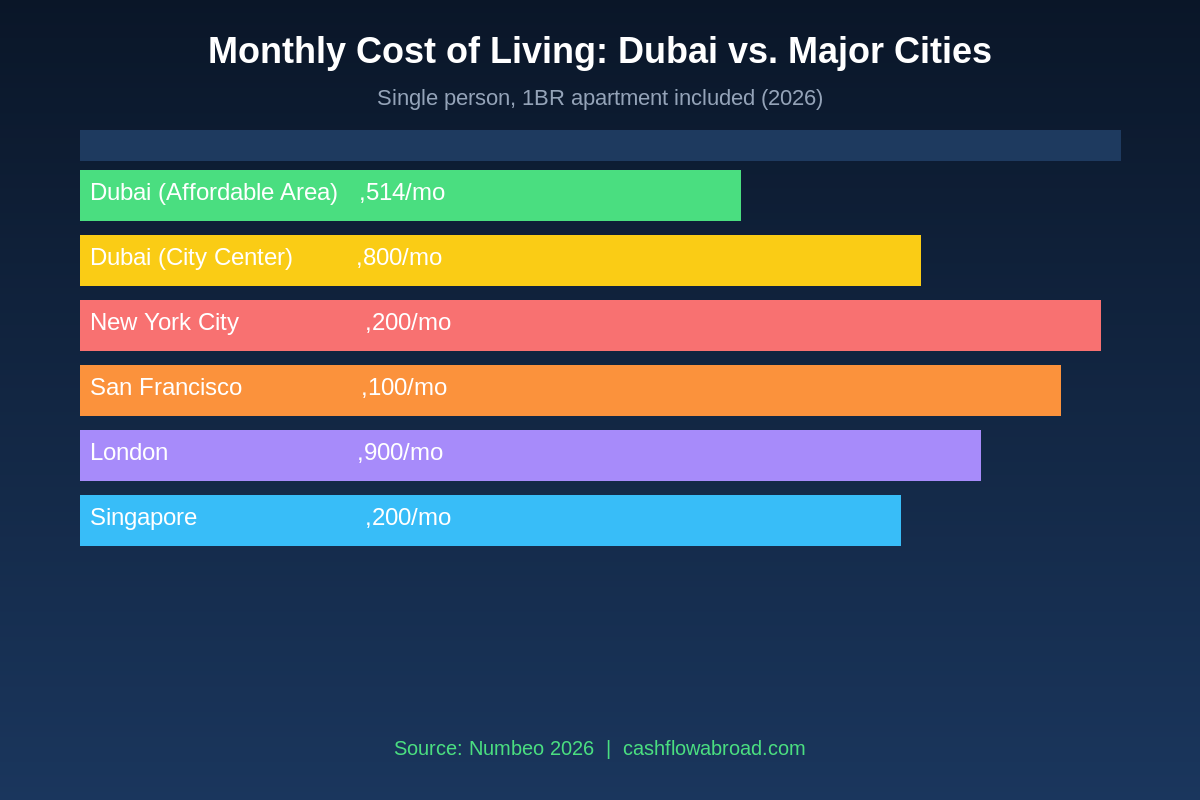

The Real Cost of Living in Dubai

Dubai is cheaper than New York, San Francisco, or London — but it's not cheap. The frequently cited "affordable" cost figures often exclude rent or undercount lifestyle costs. Here's a more honest breakdown for a single person:

| Expense | Budget | Mid-Range | Comfortable |

|---|---|---|---|

| 1BR Apartment (affordable area) | $900–$1,100/mo | $1,300/mo | $1,741/mo |

| Groceries | $250/mo | $350/mo | $500/mo |

| Dining out (15 meals/mo) | $200/mo | $350/mo | $600/mo |

| Transport (no car) | $80/mo | $150/mo | $250/mo |

| Health insurance (mandatory) | $90/mo | $150/mo | $300/mo |

| Utilities (electric/internet) | $100/mo | $130/mo | $180/mo |

| Monthly Total | ~$1,620 | ~$2,430 | ~$3,571 |

A few things that reliably skew costs upward:

Alcohol: Legal in Dubai but taxed heavily. A beer at a bar runs $8–$15. If you drink regularly, budget $100–$300/month beyond the table above.

Cars: The Dubai Metro is excellent along main corridors, but the city is sprawling and car-dependent outside Downtown and Marina. A used car plus insurance plus fuel adds $600–$900/month. Careem (Uber equivalent) is cheap at $0.30–$0.50/km but adds up over the month.

School fees: Families with kids face the single biggest budget shock in Dubai — international schools run $10,000–$30,000 per child per year. Two kids in school can eliminate the entire tax advantage at $150K of income.

Rent inflation: Dubai rental prices rose 15–20% in 2023, and growth has continued. Projections for 2026 show 4–6% annual increases in most desirable neighborhoods. Two-year lease contracts lock in your rate; month-to-month leases carry a 20–30% premium.

Visa and Residency Options

To live in Dubai legally as a US citizen, you need a UAE residence visa. There's no tourist-to-work conversion — that's a common misconception. Your main options:

| Visa Type | Duration | Approx. Cost | Primary Requirement |

|---|---|---|---|

| Employment (employer-sponsored) | 2–3 years | $816–$4,080 | UAE employer sponsorship |

| Freelance / self-employment | 1–2 years | $2,041–$4,080/yr | Free zone license or MOHRE permit |

| Business investor visa | 2 years | ~$1,089 + business setup | UAE company establishment |

| Property investor visa | 2–10 years | $3,267+ | Property valued AED 750K+ (~$204K) |

| Golden Visa | 10 years | $2,700–$5,400 | AED 2M+ property, talent, or startup |

For most remote workers and freelancers, the freelance visa via a free zone is the practical entry point. Popular choices for digital professionals include Dubai Media City and Dubai Internet City. Annual renewal runs $2,000–$4,000 depending on the zone and the activities listed on your license.

The 10-year Golden Visa has become more accessible. The AED 2M property threshold (~$545K) is the most common route for self-funded expats who want long-term stability without annual renewal stress. You can also qualify via exceptional talent in science, art, or technology, or as a startup founder with a concept approved by a UAE-accredited incubator.

Setting Up a Business in Dubai Free Zones

Freelancers billing foreign clients can operate on a freelance visa, but if your revenue is substantial or you want to hire people, incorporating a proper entity makes more sense — and free zones offer compelling terms.

Free zone companies get 0% corporate tax on qualifying income, 100% foreign ownership (no local sponsor required), full profit repatriation, and streamlined residence visa processing for employees. The main tradeoff: you generally can't sell directly to UAE mainland companies without additional licensing, which limits your local revenue.

Setup costs by free zone:

- Budget options (IFZA, Fujairah FZ): AED 10,000–15,000/year (~$2,700–$4,080) for a basic single-activity license

- DMCC (most popular overall): AED 18,000–25,000/year (~$4,900–$6,800)

- Dubai Internet City / Dubai Media City: AED 20,000–35,000/year for tech and media companies

- DIFC (financial services): Premium pricing, $10,000+ for regulated financial-sector licenses

Annual renewal typically runs 70–80% of initial setup cost. Budget $3,000–$5,000/year as a baseline for maintaining a free zone entity.

A US-specific planning note: a UAE free zone company is a foreign corporation for US tax purposes. Depending on ownership structure and income type, you may trigger Subpart F income rules or need to file Form 5471 (the information return for US shareholders of controlled foreign corporations). This doesn't usually create additional tax, but the compliance burden is real — budget $1,500–$3,000/year in accountant fees for proper filing.

Banking in Dubai as a US Person

FATCA — the Foreign Account Tax Compliance Act — requires foreign financial institutions to report US account holders to the IRS, or face 30% withholding penalties on US-source payments. This compliance infrastructure costs the global banking system an estimated $8 billion annually. The result: many UAE banks actively avoid US persons, or impose burdensome onboarding requirements and deprioritized service tiers.

Emirates NBD, Mashreq Bank, and Abu Dhabi Commercial Bank technically accept US persons, but expect extensive documentation, possible in-person branch visits, and occasional account closures when bank policies shift. The onboarding experience is inconsistent and sometimes requires a UAE employer's letter or proof of local income.

The practical solution most expats use: maintain US accounts as primary banking and use a UAE account only for local expenses (rent, utilities, everyday spending).

Charles Schwab International Checking remains the gold standard for expat banking — no foreign transaction fees, unlimited global ATM fee rebates (including UAE ATMs charging AED 20–30 per withdrawal), no minimum balance, no monthly fees. It's the single most useful US account for anyone living abroad.

Mercury is the go-to for running a US LLC or corporation while living abroad. No monthly fees, a clean API, and no branch requirement. Many Dubai-based freelancers keep their billable entity as a US pass-through and route income through Mercury.

Two compliance requirements that catch people off guard:

FBAR (FinCEN Form 114): If you have more than $10,000 in aggregate across all foreign financial accounts at any point during the year — not just at year-end — you must file by April 15. A $6,000 savings account plus $5,000 in checking triggers this. Willful non-filing: the greater of $100,000 or 50% of the account balance per violation.

Form 8938 (FATCA): Filed with your tax return. Threshold for expats living abroad: $200,000 at year-end, or $300,000 at any point during the year (single filer). You may need to file both 8938 and FBAR — they're not duplicates.

For keeping a legitimate US mailing address while living in Dubai — essential for IRS correspondence, maintaining US bank accounts, and establishing state domicile — Traveling Mailbox provides a real US street address in 50+ cities, scanned mail delivery, and check deposit for about $15/month. Our virtual mailbox guide covers why this matters and how to choose the right state for your situation.

Healthcare: The Mandatory Cost Most People Underestimate

Dubai requires all residents to carry health insurance — employers provide this for sponsored employees, but freelancers and business owners must source their own. Mandatory basic plans start around $50–$100/month but come with limited networks, low annual coverage caps ($50,000–$150,000), and significant copays for anything beyond routine care.

Comprehensive private insurance runs $150–$350/month for a healthy adult under 40. For expats who travel internationally or move between multiple countries, an international health policy often makes more practical sense than buying into the UAE's local insurance market. SafetyWing's Nomad Health plan starts around $120–$180/month and covers you globally, UAE included. Our full expat health insurance guide compares SafetyWing, Cigna Global, and Aetna International with actual premium data.

Is Dubai Actually a Geographic Arbitrage Play?

Dubai is a world-class city with excellent infrastructure, genuine cosmopolitan culture, and near-zero street crime. The geographic arbitrage argument has real merit — but it works for specific profiles, not everyone.

Dubai makes the most sense for:

- High earners ($150K+) in tech, finance, consulting, or remote corporate roles — the tax savings scale with income, and the higher your US liability would have been, the more meaningful the move

- Founders and freelancers who want a free zone structure with 0% corporate tax on international revenue

- People who genuinely want a cosmopolitan, modern city with Western amenities, international food, and a large expat community

Dubai makes less sense for:

- Earners under $80K — the tax savings don't justify setup costs and the higher cost of living vs. alternatives like Mexico City or Medellín, where cost of living is 40–60% lower

- Families with school-age children, where international school fees alone can run $20,000–$60,000/year and directly erode the tax advantage

- People who want a genuinely low cost of living — Dubai is cheaper than NYC but is not the budget play that Southeast Asia or Latin America can be

The honest arbitrage math for a single person earning $200K remotely: you save roughly $70,000–$90,000 in combined US federal, state, and SE taxes versus living in a high-tax US state. First-year setup costs (visa, business entity, security deposit, flights) run $8,000–$15,000. Net year-one financial benefit: $55,000–$80,000. Year two and beyond, annual maintenance (visa renewal, compliance filing, insurance) runs $5,000–$8,000.

If you're comparing Dubai to lower-cost expat destinations, the geographic arbitrage playbook covers the full spectrum — from Medellín at $1,500/month to Dubai at $2,500/month to Singapore at $4,200/month. See our geographic arbitrage playbook for the income-to-location matching framework. And for the banking side of any expat move, the US expat banking and taxes guide covers FBAR, FATCA, and account setup in detail.

The Bottom Line

Dubai's 0% personal income tax is real. For high-earning US expats who qualify for FEIE, the combined annual tax bill can drop from $50,000+ to a few thousand dollars — a genuinely transformative financial change. But the calculation requires actual planning: meeting the 330-day physical presence test, correctly handling self-employment tax, structuring any business entity properly, navigating FATCA-compliant banking, and staying current on FBARs and Form 8938 compliance.

The expats who win in Dubai ran the actual numbers before they moved, hired a CPA who specializes in US expat returns, and didn't confuse "zero UAE tax" with "zero tax." The ones who get burned assumed the brochure told the whole story.

This post is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently and individual situations vary significantly. Consult a qualified US expat tax professional before making decisions about residency, tax strategy, or financial structure abroad. All figures are estimates based on publicly available data as of 2025–2026.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJuly 4, 2026

Expat Tax & FinanceJuly 4, 2026

Canadian TFSA and US Taxes: The Reporting Trap

US citizens holding a Canadian TFSA owe tax on all annual growth and must file Form 3520 — PFIC rules apply to Canadian mutual funds inside the

Expat Tax & FinanceJuly 4, 2026

Expat Tax & FinanceJuly 4, 2026

State Income Tax for Expats: Which States Follow You

California, New York, and Virginia keep taxing Americans abroad. Learn which states follow you, what triggers audits, and how to exit cleanly.

Expat Tax & FinanceJuly 3, 2026

Expat Tax & FinanceJuly 3, 2026

FBAR: The $10,000 Expat Rule Most People Get Wrong

FBAR: when any foreign account aggregate hits $10,000 during the year, all accounts must be reported. Penalties, Bittner ruling, and catch-up