Italy’s 7% Flat Tax: Retire in the Mediterranean

9 min read · 2,296 words

Italy will tax every dollar of your foreign pension, dividends, rental income, and capital gains at exactly 7%—for ten consecutive years. No income cap. No complex calculations. No filing thirty different schedules. Just a flat 7%, and the Italian government leaves the rest alone.

That’s not a loophole. It’s a formal tax regime written into the Italian tax code specifically to attract foreign retirees to the underpopulated south. While Portugal’s famous NHR program has been gutted and turned into a narrow professional visa, Italy quietly offers one of the most generous blanket tax breaks for retirees in the developed world—and almost no Americans know about it.

Here’s what a $90,000-per-year retiree (pension + dividends + rental income) pays over a decade under standard Italian rates versus the 7% regime:

- Standard Italian progressive rates (23–43%): Roughly $315,000 in taxes over 10 years

- 7% flat tax regime: $63,000 over 10 years

- Savings: $252,000

That’s a quarter million dollars. For moving to Puglia.

What Is Italy’s 7% Flat Tax Regime?

Introduced in 2019 via Article 24-ter of the Italian Tax Code, the regime lets foreign pension recipients who relocate to qualifying municipalities in southern Italy pay a single flat tax of 7% on all foreign-sourced income. The goal was explicitly to reverse the depopulation of rural southern Italy by attracting wealthy foreign retirees to villages hemorrhaging residents to the cities.

It worked better than expected. By 2023, hundreds of expats—primarily Northern Europeans and some Americans—had restructured their retirement around it. Italian media dubbed the beneficiaries pensionati della fortuna: pensioners of fortune.

What makes this regime exceptional is its scope. Under the 7% flat tax, the following foreign-source income streams are all taxed at the same rate:

- Foreign pension income (public and private, including Social Security and 401k distributions)

- Dividends from foreign investments

- Capital gains on foreign assets

- Foreign rental income

- Interest from foreign bank accounts

- Any other foreign-source income

During the 10-year regime period, you’re also exempt from IVIE (Italy’s annual wealth tax on foreign real estate) and IVAFE (Italy’s annual wealth tax on foreign financial assets). Those two taxes alone can run 0.2–0.76% of total foreign asset value each year—on a $1 million portfolio, that’s up to $7,600 per year in wealth taxes before a dollar of income is even taxed.

Who Qualifies

The eligibility rules are straightforward. You must:

- Receive a foreign pension. Public or private. Italian Social Security (INPS) doesn’t count—you need income sourced from outside Italy. US Social Security, a 401k, a UK NHS pension, a Canadian CPP—all qualify.

- Not have been an Italian tax resident in the preceding 5 years. If you lived in Italy before 2020 and left, you’d need to have been gone since then to qualify today.

- Come from a country with a tax information exchange agreement with Italy. The US, UK, Canada, Australia, and all EU members qualify. This covers essentially every developed nation.

- Relocate to a qualifying municipality. The municipality must have fewer than 20,000 residents and be located in one of eight southern regions.

There is no income floor. A retiree on $1,500/month qualifies as readily as one pulling $15,000/month. No means test, no net worth requirement, no professional activity requirement.

One clarification: if you generate Italian-source income—Italian rental properties, Italian employment, an Italian business—that income is taxed at standard progressive rates of 23–43%. The 7% flat rate only applies to foreign-source income. The two calculations run in parallel.

The Eight Qualifying Regions

The regime applies to municipalities under 20,000 residents in eight southern Italian regions. There are also extensions to earthquake-reconstruction zones in Lazio, Umbria, and Marche, but the southern regions are the primary target.

| Region | Notable Areas | Typical Monthly Rent (2BR) | Character |

|---|---|---|---|

| Sicily | Noto, Modica, Scicli, Ragusa interior | €500–€800 | Baroque towns, Mount Etna, coastal access |

| Calabria | Tropea area, Sila highlands | €400–€650 | Cheapest region in Italy, undiscovered coast |

| Sardinia | Oristano province, Nuoro province | €500–€900 | UNESCO villages, cleanest beaches in Europe |

| Campania | Interior towns away from Naples/Amalfi | €450–€750 | Cuisine capital, Roman ruins, Vesuvius |

| Puglia | Valle d’Itria, Salento interior | €550–€850 | Trulli houses, olive groves, Adriatic coast |

| Basilicata | Matera region, Pollino National Park | €350–€600 | Ancient cave city, near-empty villages |

| Abruzzo | Gran Sasso foothills, Majella villages | €450–€700 | Mountains meet Adriatic, ski in winter |

| Molise | Campobasso province, Isernia province | €300–€550 | Italy’s least-visited region, medieval towns |

Many of these municipalities are actively paying foreigners to come. Molise, Calabria, and Sicily have run separate cash grant programs—distinct from the tax regime—offering €25,000–€30,000 for purchasing and renovating abandoned homes, conditioned on staying for several years and investing in the property.

The €1 House Programs (Yes, They’re Real)

Several Sicilian and Calabrian municipalities have sold abandoned properties for €1 to foreign buyers willing to renovate them. Towns most associated with these programs include Mussomeli and Sambuca di Sicilia in Sicily, Cinquefrondi in Calabria, and Ollolai in Sardinia.

The renovation requirement typically runs €15,000–€50,000 depending on the property’s condition and the municipality’s rules. You usually have 1–3 years to complete the work and must provide a renovation bond upfront. That’s still a renovated stone home in southern Italy for potentially under €60,000 total—in a country where the 7% flat tax then applies to all your foreign income for the next decade.

A couple with a combined $80,000/year in foreign income (Social Security + 401k + rental income from back home) saves roughly $26,000/year in Italian taxes versus standard progressive rates. In 10 years, that’s $260,000—enough to fund the renovation, furnish the home, and still retire with a significant cushion.

The €1 house programs have real headaches: bureaucratic delays, hidden structural problems, and finding reliable local contractors. But for someone with time, patience, and a renovation budget, the math is hard to beat.

The Math: What You Actually Save

Italy’s standard progressive income tax (IRPEF) has five brackets, topping out at 43% on income over €50,000. Add regional surcharges (1.23–3.33%) and municipal surcharges (up to 0.9%), and effective rates for higher earners approach 47%.

| Annual Foreign Income | Standard Italian Tax (est.) | 7% Flat Tax | Annual Savings | 10-Year Savings |

|---|---|---|---|---|

| $40,000 | ~$9,600 (24%) | $2,800 | $6,800 | $68,000 |

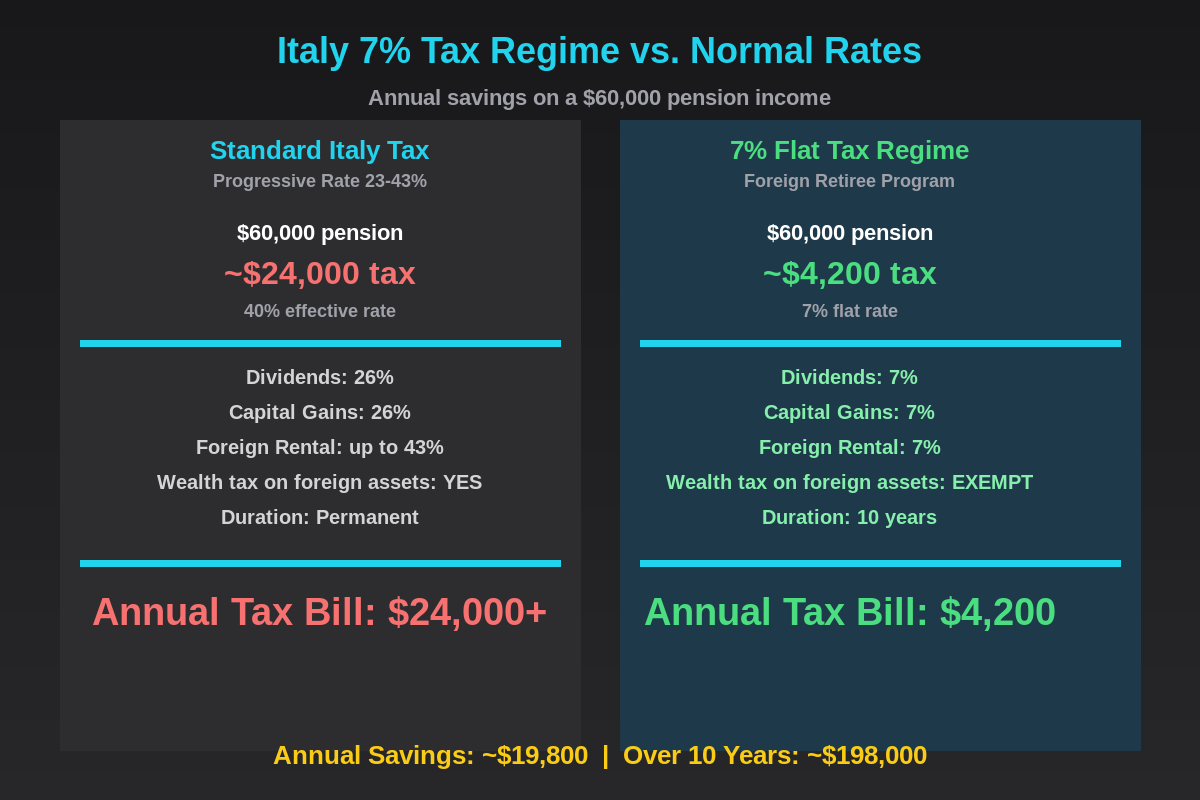

| $60,000 | ~$19,800 (33%) | $4,200 | $15,600 | $156,000 |

| $90,000 | ~$36,000 (40%) | $6,300 | $29,700 | $297,000 |

| $150,000 | ~$68,000 (45%) | $10,500 | $57,500 | $575,000 |

The higher the income, the more extraordinary the savings. At $150,000/year, you’re banking over half a million dollars in tax over the decade—all while living in one of the most beautiful countries on earth.

The Catch: No Foreign Tax Credits (Critical for US Citizens)

For US citizens specifically, there’s a critical nuance: the 7% regime explicitly prohibits claiming foreign tax credits against it. Under normal Italian taxation, you could offset US taxes paid against your Italian bill using the US-Italy tax treaty. Under the 7% regime, you cannot.

This creates a potential double-taxation issue. The US taxes its citizens on worldwide income regardless of residency—unless you qualify for the Foreign Earned Income Exclusion or the Foreign Tax Credit. Pension income and passive income (dividends, capital gains) aren’t eligible for the FEIE. The Foreign Tax Credit can offset US taxes on this income, but it won’t offset your Italian 7%—you’re paying both bills.

Real-world impact depends on your income mix. A retiree drawing primarily Social Security and 401k distributions may have a relatively modest US effective rate—particularly with the standard deduction and the favorable Social Security inclusion rules. Running the full calculation with a qualified US expat tax advisor before committing is non-negotiable. For many retirees, the combined US + Italian 7% load still comes out significantly below what they’d pay staying in the US or in higher-tax European countries.

Italy vs. Greece vs. Portugal

Italy isn’t the only country running a preferential regime for foreign retirees. Here’s how the three main options compare:

| Program | Tax Rate | Duration | Income Covered | Location Restriction | Status |

|---|---|---|---|---|---|

| Italy 7% Regime | 7% flat | 10 years | All foreign income | Under 20K residents, south only | Active (unchanged in 2026 budget) |

| Greece 7% Regime | 7% flat | Up to 15 years | All foreign income | None — any Greek municipality | Active |

| Portugal IFICI (former NHR) | 20% flat (professional) / complex | 10 years | Narrow professional categories | None | Active but severely restricted |

Greece offers more location flexibility—you can live in Athens or Thessaloniki and still qualify—and the 15-year duration beats Italy’s 10. But Italy’s rural living requirement brings a secondary benefit: dramatically lower cost of living. A two-bedroom apartment in Pugliese village: €550–700/month. Athens: €900–1,400. The lifestyle in a Sicilian hill town is genuinely different from urban Greece, and for many retirees, that’s a feature rather than a bug.

Portugal’s IFICI (the successor to NHR) is now targeted at tech workers, startup founders, and specific professional activities. Regular retirees seeking blanket passive income exemptions no longer qualify under the new structure. Italy and Greece are the actual heirs to what NHR promised.

How to Apply: The Step-by-Step

The application runs through Italy’s tax system, not an immigration authority. The mechanics:

- Obtain a Codice Fiscale. Italy’s equivalent of a Social Security number. Any Italian consulate abroad can issue one—takes a few days, costs nothing.

- Establish Italian tax residency. Register with your chosen municipality as a resident (residenza anagrafica). Requires a lease or property deed plus a declaration of intent to reside. You must spend 183+ days per year in Italy to maintain tax residency.

- File the regime election with your first Italian tax return. The 7% option is elected on your first Modello Redditi PF filed as an Italian resident. You declare which countries your income originates from—this determines potential withholding treaty exclusions.

- Pay the annual flat tax by July 31. Unlike US quarterly estimated taxes, the Italian 7% is settled annually in a single payment by the last business day of July each year.

A commercialista (Italian accountant/tax advisor) familiar with the expat regime costs €1,500–3,000/year and is worth every cent. On the US side, a specialist in expat returns—Greenback Expat Tax Services and US Tax Help both have Italy experience—runs another $1,500–3,000/year. Budget $3,000–6,000/year for professional tax support across both systems. On a $90,000 income with $29,700 in annual tax savings, that’s still a net gain of $23,000–$26,000 per year.

Practical Realities: Healthcare, Banking, and US Obligations

Healthcare: Once you establish residency and pay Italian taxes, you can register with the Italian National Health Service (Servizio Sanitario Nazionale). Italy’s public healthcare is ranked among the best globally—comprehensive, low-cost, and particularly strong in specialist care. Wait times for elective procedures can stretch. Many expats maintain private supplemental coverage at €100–200/month for a healthy retiree in their 60s. For the first year before SSN registration is fully processed, SafetyWing’s Nomad Insurance provides solid international coverage at $56–200/month depending on age—worth having in the gap.

Banking: You’ll still need a US bank account for Social Security deposits, IRA distributions, and brokerage income. Charles Schwab International is the standard for expats—no foreign transaction fees, free ATM withdrawals anywhere in Italy, and no account closure risk based on your country of residence. Locally in Italy, BancoPosta (via the Italian postal service) is widely used by expats for its relative simplicity and nationwide branch coverage.

US mailing address: You need a permanent US address for Social Security correspondence, IRS filings, brokerage accounts, and state domicile purposes. A virtual mailbox is the cleanest solution. Traveling Mailbox provides a real US street address in 50+ cities, scans your mail on demand, and handles check deposits for $15/month—the site owner uses it personally. Without a functioning US address, brokerage accounts start closing and IRS correspondence goes unanswered.

FBAR and FATCA: Moving to Italy doesn’t reduce your US reporting obligations one dollar. Italian bank accounts holding over $10,000 at any point during the year must be reported via FBAR. Foreign account balances above $200,000 abroad trigger FATCA Form 8938. For the full breakdown, see the complete US expat banking and tax guide.

State taxes: Your home state may still claim you as a resident even after you’ve moved to Sicily. California, New York, and Virginia are the most aggressive. See which states pursue expats hardest—and what you need to do before departing to cleanly sever state tax residency.

Who This Actually Makes Sense For

The Italy 7% regime fits a specific profile—and being honest about who it doesn’t fit is as important as the pitch:

Strong fit: US retirees with $50,000–$200,000/year in foreign passive income (pension, dividends, Social Security, 401k) who would face significant Italian rates at progressive bands. People who genuinely want to live in a quiet, small town in southern Italy. Those with low-to-moderate US effective tax rates on passive income, minimizing double-taxation concern. Couples, who can each qualify individually and each run 10 years of regime protection.

Poor fit: High earners with significant US tax liability on the same income streams (the no-foreign-tax-credit restriction becomes painful). Anyone who wants to live in a major Italian city—Rome (2.8 million), Milan (1.4 million), Florence (370,000), and Naples (900,000) all exceed the 20,000 resident cap. Those unwilling to spend 183+ days per year in Italy.

The Bottom Line

Italy’s 7% flat tax regime delivers what almost no other country in Western Europe will: a dramatically lower rate on all foreign income, wealth tax exemptions on foreign assets, and a 10-year runway to build wealth in one of the world’s great cultures. The €1 house programs running in Sicily, Calabria, and Sardinia aren’t just internet clickbait—they’re real programs that pair with the tax regime to create a retirement arbitrage opportunity without precedent in the developed world.

The paperwork is Italian. You’ll need professional help on both sides of the Atlantic. And you’ll need to actually live in a small southern Italian town, which for some retirees is the dream and for others is simply not workable.

But for financially independent Americans in their late 50s and 60s with a genuine appetite for Mediterranean life, this is one of the most compelling moves on the board right now. The Italian government left the regime completely intact in the 2026 budget. The window is open. The beach in Calabria is warm. The arancini are perfect.

Financial disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently and vary by individual circumstances. The Italy 7% flat tax regime has specific eligibility requirements that must be individually verified. Consult a qualified US expat tax professional and Italian commercialista before making any residency or tax planning decisions.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.