Mexico’s SAT: What 1.6M US Expats Actually Owe

9 min read · 2,300 words

Roughly 1.6 million Americans live in Mexico — more than in any other country on earth. The majority have never filed a Mexican tax return. Some have lived there for a decade, paid their rent in pesos, opened a local bank account, and never once received a letter from the SAT. That silence has been mistaken for permission.

It wasn’t permission. It was a gap in enforcement that is now closing fast. Mexico’s 2026 tax reform gave the Servicio de Administración Tributaria new digital surveillance tools, mandatory RFC registration for all foreign residents, and mandatory income reporting from digital platforms. The question for the 1.6 million isn’t whether Mexico can find them — it’s what they’ll owe when it does.

How Mexican Tax Residency Works

Mexico’s trigger is deceptively simple: spend more than 183 days in Mexico in a calendar year — consecutive or not — and you are a Mexican tax resident. That means you owe Mexico taxes on your worldwide income. Not just your Mexican salary. Not just rental income from a Condesa apartment. Your US Social Security payments, your 401(k) distributions, your US dividend income, your capital gains from selling Apple stock — all of it is on the table.

There’s a second trigger most people don’t know: Mexico’s tax code also claims you as a resident if Mexico is your “center of vital interests.” The definition: more than 50% of your annual income comes from Mexican sources, or your primary professional activities are carried out in Mexico. A freelancer working with Mexican clients and getting paid in pesos can hit this threshold without ever counting a single day.

The tourist visa (FMM) does not exempt you. It prevents you from working legally in Mexico — a separate compliance issue — but for tax purposes, the day count is what matters. The SAT doesn’t care what visa you entered on.

Mexico’s ISR Tax Brackets: The Full Picture

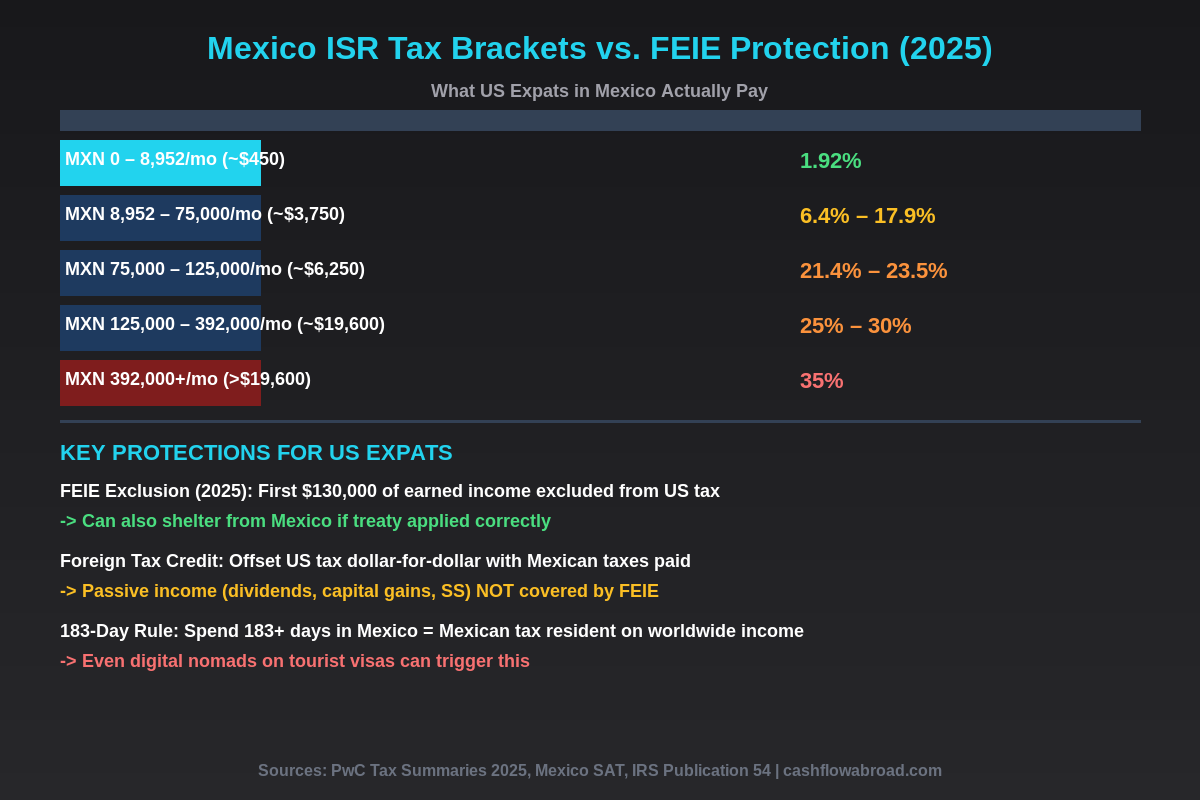

Mexico’s Impuesto Sobre la Renta (ISR) runs 11 progressive brackets from 1.92% to 35%. The full structure for 2025:

| Monthly Income (MXN) | Approx. USD/Month | Marginal Rate |

|---|---|---|

| Up to MXN 8,952 | ~$450 | 1.92% |

| MXN 8,952 – 75,984 | $450 – $3,800 | 6.4% – 17.9% |

| MXN 75,984 – 83,333 | $3,800 – $4,167 | 21.4% |

| MXN 83,334 – 125,000 | $4,167 – $6,250 | 23.5% |

| MXN 125,001 – 166,667 | $6,250 – $8,333 | 30% |

| MXN 166,668 – 391,667 | $8,333 – $19,583 | 32% |

| Over MXN 391,667 | Over $19,583 | 35% |

Non-residents — those under the 183-day threshold — face a different structure: a flat 15% or 30% on Mexico-sourced income, with the first MXN 125,901 (~$7,000) typically exempt. That threshold is why most short-term visitors owe nothing. Cross 183 days and you move from flat 15–30% on local income only to progressive rates on global income. That’s the cliff.

What US Expats in Mexico Actually Owe (And Why It’s Complicated)

The US-Mexico tax treaty has been in force since 1992 and updated several times since. Its core function is preventing true double taxation. Here’s how it works in practice:

Earned Income: The FEIE Shield

If you’re employed abroad or running a foreign business, the Foreign Earned Income Exclusion (FEIE) lets you exclude up to $130,000 of foreign-earned income from US taxes in 2025 (married couples can double this to $260,000). For many expats in Mexico earning in pesos, this effectively eliminates the US tax bill on employment income.

But the FEIE only covers earned income. Wages, freelance fees, self-employment income — yes. Social Security, 401(k) distributions, US dividends, capital gains — no. These are passive income streams, and they fall outside the FEIE entirely. For a Mexico-based retiree drawing $60,000/year from a 401(k) and $30,000 from Social Security, neither stream qualifies for FEIE. Mexico taxes both as worldwide income for a tax resident, and the US taxes both as well.

The Foreign Tax Credit Safety Net (and Its Limits)

The Foreign Tax Credit (FTC) lets you offset your US tax bill dollar-for-dollar against taxes actually paid to Mexico. If you owe Mexico MXN 120,000 (~$6,000) and the IRS calculates you owe $8,000 on the same income, the $6,000 Mexico payment reduces your US bill to $2,000. No true double taxation — but no free lunch either. You’re still paying taxes; you’re just paying them once.

The FTC and FEIE generally can’t be used on the same income. Choosing which to apply — and in what order, across which income categories — is where expat tax returns get expensive to file professionally. A mistake in the ordering can cost thousands. This is not a DIY situation if you have multiple income streams. For the full decision tree, see our guide on FEIE vs. Foreign Tax Credit.

The Passive Income Trap

Here’s the scenario that catches retirees and passive investors off guard. You’ve been living in Mexico City for four years, carefully staying under 183 days. Then one year you stay an extra month — a family visit, a health issue — and cross the threshold. Suddenly:

- Your $40,000 annual US brokerage income (dividends + capital gains) becomes subject to Mexican ISR at progressive rates

- Mexico also taxes your Social Security distributions and IRA withdrawals

- You now owe a declaración anual (annual return) by April 30, plus monthly provisional payments throughout the year

- Back taxes and penalties can be assessed for prior years where you should have been filing

The US brokerage account surprises people every time. Many expats assume that income from a US institution, reported on a 1099, is purely a US matter. As a Mexican tax resident, you have to report it to the SAT. The treaty helps prevent double taxation, but it doesn’t eliminate the filing obligation or the compliance headache.

For managing the US side — keeping brokerage accounts open, maintaining IRS correspondence addresses, preserving US banking while abroad — a service like Traveling Mailbox gives you a real US street address in 50+ cities, mail scanning, and check deposit capability for $15/month. Essential for keeping US financial accounts functional without a physical US presence.

The RFC: Mexico Has a Tax ID On You

The Registro Federal de Contribuyentes (RFC) is Mexico’s tax identification number. Since 2022, Mexico has required all foreign residents with a CURP identity number to obtain an RFC — even if they earn zero income in Mexico.

Getting an RFC doesn’t automatically trigger a tax bill. But it creates a permanent link between your identity and the SAT’s systems. Every bank transaction, property rental, and platform payment that gets reported to SAT is now cross-referenced against your RFC. The RFC is the foundation of SAT’s enforcement infrastructure, and the 2026 reform is building a large data collection system on top of it.

Temporary residents and permanent residents are both required to register. Enforcement of this requirement has been inconsistent — but the SAT’s 2026 tools are designed specifically to identify people who should have registered and didn’t.

SAT’s 2026 Enforcement Upgrade: Why the Math Is Changing

Mexico’s 2026 tax reform — published December 28, 2025, effective January 1, 2026 — is the single most significant enforcement escalation for expats in recent memory. Key provisions, per Baker McKenzie and KPMG analysis:

- Digital platform mandatory reporting: All platforms must report complete seller information, including foreigners and non-residents with Mexican RFCs. Five-year data retention is required.

- B2B withholding extended: VAT withholding and income tax withholding now applies to B2B digital transactions — a direct hit at remote workers and digital freelancers earning through international platforms

- Anti-disguise provisions: The reform specifically targets schemes where individuals pose as companies or non-residents to avoid platform obligations

- Expanded audit capacity: SAT received significant new resources and legal authority to pursue cross-border tax matters, with faster coordination mechanisms under the US-Mexico treaty

The treaty coordination matters. The US and Mexico exchange financial information under FATCA-style agreements. US expats in Mexico who haven’t disclosed Mexican bank accounts on their FBAR face penalties of up to $10,000 per account per year for non-willful violations — and up to 50% of the account balance per year for willful failures. That’s independent of any Mexican tax liability. The full FBAR and FATCA compliance picture is covered in our US expat banking and taxes guide.

The Tourist Visa Trap: Two Laws Violated Simultaneously

Hundreds of thousands of digital nomads are currently living in Mexico on tourist visas, working remotely for foreign employers. This creates a double compliance problem most haven’t fully thought through:

Problem 1 — Visa violation: Mexico’s FMM tourist visa explicitly prohibits paid work. Working remotely from Mexico on a tourist visa violates the terms of entry. INM (Mexico’s immigration authority) has begun occasional enforcement in Mexico City, Oaxaca, and Tulum — the three highest-concentration digital nomad areas.

Problem 2 — Tax exposure: Staying 183+ days triggers tax residency regardless of visa type. The tourist visa doesn’t provide a tax exemption. You can simultaneously violate your visa terms and be a Mexican tax resident — independent legal exposures that reinforce each other’s financial risk.

Mexico does not currently have a formal digital nomad visa, unlike many countries that have added them. The standard path for long-term residents is a Temporary Resident visa (Residente Temporal), which allows legal residence but still triggers the 183-day tax residency clock. The visa category doesn’t change the tax math.

If You’re Under 183 Days: The Non-Resident Rules

For US citizens who winter in Mexico, visit for 90 days, or otherwise stay less than 183 days in any calendar year, the non-resident rules apply. Mexico taxes non-residents only on Mexico-sourced income:

| Income Type | Non-Resident Rate | Notes |

|---|---|---|

| Wages from a Mexican employer | 15% – 30% | First MXN 125,901 (~$7,000) often exempt |

| Freelance fees from Mexican clients | 25% | Withholding at source |

| Rental income from Mexican property | 25% gross or 35% net | Election available |

| Mexican dividends | 10% | Plus corporate-level ISR already paid |

| Capital gains on Mexican real estate | 25% gross or 35% net | Certificate required |

| US-sourced remote work income | 0% | Not Mexico-sourced; not taxed by SAT |

The last row explains why most US remote workers in Mexico have had zero practical tax exposure for years. Their income comes from US employers or clients — it’s not Mexico-sourced, and unless they cross 183 days, it never enters Mexico’s tax system. The problem is that the 183-day count is cumulative across the calendar year — and it’s easy to miscalculate when splitting time between Mexico and the US.

Expat Banking in Mexico: FATCA and the Account Problem

Opening a Mexican bank account as a foreign resident is increasingly difficult. FATCA compliance imposes significant costs on Mexican banks, and many have responded with added friction: extensive documentation, longer approval timelines, and informal policies that deprioritize US citizen accounts. BBVA Mexico, Santander Mexico, and Banamex are the most common choices for expats who navigate this successfully — but expect the process to take weeks and require a valid residency visa, RFC number, Mexican address proof (Comprobante de Domicilio), and sometimes a local reference.

For US-side banking, Mercury is excellent for freelancers and business owners who need a US business account compatible with international operations. For personal banking, Charles Schwab’s Investor Checking account reimburses all ATM fees globally — pulling pesos from any Banamex, BBVA, or Santander ATM in Mexico without the typical 2–3% foreign transaction hit.

For international transfers back to the US — tax payments, IRA contributions, or just moving money home — Remitly handles MXN-to-USD at competitive exchange rates with transparent fees before you commit.

The Action Plan for US Expats in Mexico

If you’re living or planning to live in Mexico, here’s the sequence that keeps you out of trouble:

- Count your days carefully. The 183-day rule uses a calendar year, not a rolling 12-month period. Crossing in December and leaving in early June could mean you’ve accumulated 183 days across two calendar years. Use a spreadsheet. Be precise.

- Get an RFC if you have a CURP. Resistance doesn’t protect you — it creates a compliance gap to explain later when SAT’s automated systems flag your RFC as missing.

- File FBAR if you have Mexican bank accounts over $10,000. Any Mexican account over $10,000 at any point during the year requires FinCEN Form 114 by June 15 (extendable to October 15). The penalties for missing this are severe and entirely separate from any Mexican tax bill.

- Hire a dual-licensed tax professional for year one. The complexity of applying FEIE, FTC, treaty provisions, and Mexican ISR correctly is significant. A CPA fluent in both US expat returns and Mexican ISR pays for itself in year one alone.

- Keep a US address active. For IRS correspondence, US brokerage accounts, credit card accounts, and banking relationships — a virtual mailbox is the cleanest solution. Our guide to virtual mailboxes for expats covers why this matters and how to choose the right state.

For the full framework on geographic arbitrage — comparing Mexico against nine other destinations by cost, tax environment, and visa stability — see our geographic arbitrage playbook. Mexico typically offers the best cost-of-living value in Latin America for US expats, but the tax picture is meaningfully more complex than the low rent suggests.

The Bottom Line

Mexico has been the world’s most popular US expat destination for a reason: extraordinary food, dramatically lower cost of living than the US, and for years a tax system that was theoretically present but practically invisible. The 183-day trigger existed but enforcement was minimal. The RFC requirement existed but registration was inconsistent. SAT knew there was a large untaxed expat population and lacked the digital infrastructure to pursue it systematically.

That infrastructure now exists. The 2026 reform gave SAT reporting hooks into every digital platform, every landlord issuing digital tax invoices, every bank account tied to an RFC. The window where ignorance was a viable strategy is closing. A US expat in Oaxaca who has spent more than 183 days per year for the last three years — without filing a Mexican declaración anual — may have accumulated a material tax liability they don’t know about.

The good news: the US-Mexico tax treaty works. With competent professional help, most expats can structure their filings to avoid true double taxation. But “not double-taxed” and “no tax owed in Mexico” are not the same thing. The passive income streams — 401(k), Social Security, US dividends — are the exposure that blindsides people. Plan for them explicitly, before SAT sends a letter that introduces itself.

Financial disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. Tax laws change frequently and individual circumstances vary significantly. Consult a qualified tax professional licensed in both the US and Mexico before making any tax-related decisions. All figures are based on published 2025–2026 tax rates and may be subject to change.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.