FBAR Penalties: The IRS Rule That Can Cost US Expats $165K

10 min read · 2,448 words

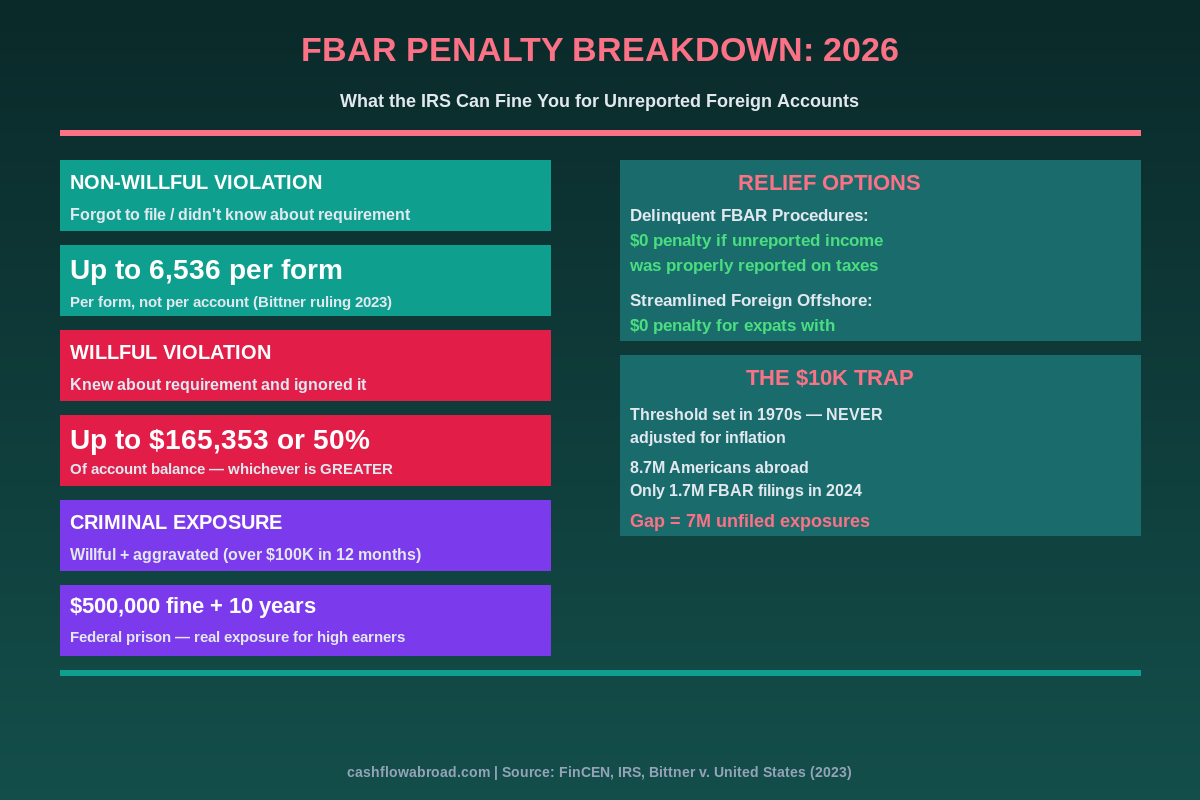

Roughly 8.7 million Americans live outside the United States. In 2024, only 1.7 million FBAR reports were filed. That gap isn’t an accident — millions of US expats simply don’t know this reporting requirement exists, or assume it doesn’t apply to them because they’re not hiding money offshore. The IRS doesn’t care why you didn’t file. Penalties start at $16,536 and can exceed $165,000 per year.

The Foreign Bank Account Report — officially FinCEN Form 114 — is one of the most widely misunderstood obligations in US tax law. It has nothing to do with how much money you earned. It triggers based on how much money sat in a foreign bank account, even briefly. Miss it once, you owe a fine. Miss it for five years, things get very expensive very fast.

Here’s the complete guide to what FBAR is, who must file, what the penalties actually look like, and how to fix things if you’re already behind.

What Is FBAR — And Why Does It Exist

The Bank Secrecy Act of 1970 gave the US Treasury Department authority to require Americans to report foreign financial accounts. The stated goal: prevent money laundering and tax evasion. The mechanism: a separate annual report filed directly with the Financial Crimes Enforcement Network (FinCEN), not the IRS, though the IRS enforces it.

FBAR isn’t a tax form. It doesn’t create any tax liability on its own. You’re not paying tax when you file — you’re just disclosing that the accounts exist. The entire purpose is transparency. That’s why the penalties feel so disproportionate to people who owe zero additional tax: you can be fined hundreds of thousands of dollars for paperwork you weren’t aware of, even if every dollar in those accounts was fully legal and already taxed.

The threshold — $10,000 in aggregate across all foreign accounts at any point during the year — was set in 1970 and has never been adjusted for inflation. In today’s money, that threshold would be roughly $77,000. But the law hasn’t been updated, so a US expat with a modest checking account abroad for everyday expenses can easily trigger the requirement without realizing it.

Who Must File FBAR

If you are a US person and you had a financial interest in, or signature authority over, one or more foreign financial accounts with an aggregate value exceeding $10,000 at any point during the calendar year, you must file.

“US person” means US citizens, green card holders, and resident aliens — regardless of where they live. It also covers US corporations, partnerships, LLCs, trusts, and estates.

“Signature authority” is a common trap. If you’re a US employee at a foreign company and you have signing authority over the company’s bank account — even if the money is not yours — you may be required to file. Many corporate treasurers and CFOs at international companies get caught by this provision.

“At any point during the year” is the other trap. Your account doesn’t need to average over $10,000. If you received a large wire transfer in March that briefly pushed your balance to $12,000, and the account was back to $3,000 by April, you still triggered the requirement for that year.

What Counts as a Foreign Financial Account

Beyond checking and savings accounts, FBAR covers a wider set of accounts than most expats expect:

- Foreign investment and brokerage accounts

- Foreign mutual funds

- Foreign pension and retirement accounts (including government pensions)

- Foreign life insurance policies with a cash surrender value

- Foreign annuity contracts with a cash value

- Foreign commodity futures or options accounts

Foreign real estate does not trigger FBAR directly — but if you hold it through a foreign company or trust, the ownership interest in that entity can trigger it. Cryptocurrency held at foreign exchanges sits in a gray area that FinCEN has signaled it intends to cover through future rulemaking.

The Penalty Breakdown: Non-Willful vs. Willful

The single most important thing to understand about FBAR penalties is the distinction between willful and non-willful violations. The difference determines whether your penalty is measured in tens of thousands or hundreds of thousands of dollars.

| Violation Type | Maximum Civil Penalty (2026) | Criminal Exposure |

|---|---|---|

| Non-willful (per form) | $16,536 per unfiled FBAR | None |

| Willful (per violation) | $165,353 or 50% of account balance — whichever is greater | Up to $250,000 + 5 years prison |

| Willful + aggravated (>$100K in 12 months) | $165,353 or 50% of balance | Up to $500,000 + 10 years prison |

| Pattern of illegal activity | Discretionary | Up to $500,000 + 10 years prison |

Penalty amounts are adjusted annually for inflation. The 2026 figures represent the current ceiling — what the IRS can assess, not what it always does. In practice, IRS agents have discretion to go lower.

How the IRS Determines “Willfulness”

Willfulness doesn’t require proof that you consciously decided to break the law. In January 2026, the US Court of Appeals for the Second Circuit held that reckless disregard of the FBAR requirement is sufficient to trigger willful penalties — joining six other circuit courts that have adopted the same standard. This ruling effectively applies nationwide.

What does “reckless disregard” look like? Courts have found it where taxpayers: signed tax returns that asked about foreign accounts and checked “no,” consulted a professional who mentioned foreign account reporting and didn’t follow up, received bank statements referencing FinCEN requirements, or earned substantial foreign income without investigating their filing obligations.

In other words, “I didn’t know” is not automatically a defense. If a reasonable person in your position should have known — because you signed forms, had advisors, or earned significant foreign income — willfulness can still be found.

The Bittner Ruling: The Supreme Court Win That Changed Everything

Until 2023, the government’s position was that non-willful FBAR penalties applied per account. This produced nightmare scenarios: Alexandru Bittner, a Romanian-American businessman, failed to file FBARs for 2007–2011. The IRS assessed him a $2.72 million penalty — $10,000 per account, per year, across 272 separate accounts.

Bittner argued the penalty should be $50,000 — $10,000 per year for five unfiled forms. The Supreme Court agreed, ruling 5-4 in Bittner v. United States (2023) that non-willful penalties apply per form, not per account. His penalty dropped from $2.72 million to $50,000.

For ordinary expats, this ruling is transformative. Someone who failed to report five foreign accounts for three years now faces a maximum non-willful exposure of $49,608 (3 forms × $16,536) rather than $247,500 (15 account-years × $16,500). It’s still significant — but it’s no longer existentially catastrophic for honest mistakes.

The catch: Bittner only applies to non-willful violations. Willful penalties still apply per account, per year. The recklessness standard makes the willful/non-willful line more important than ever.

How the IRS Actually Finds Out

The common assumption that offshore accounts are private died with FATCA. The Foreign Account Tax Compliance Act (2010) requires foreign financial institutions to report US account holders directly to the IRS or face a 30% withholding tax on their US-source income. As of 2026, banks in over 100 countries participate.

Beyond FATCA, the Common Reporting Standard (CRS) — a separate global framework with 120+ participating countries — means banks worldwide are exchanging account information with each other’s tax authorities. If you have an account in Germany, Colombia, Thailand, or most other developed countries, that information flows automatically to FinCEN and the IRS.

The practical result: the era of genuinely hidden offshore accounts is over for most Americans. What remains is a large population of expats who simply didn’t realize they had a compliance obligation — because they weren’t hiding anything, just living abroad and using local bank accounts. The IRS doesn’t know the difference until it audits you.

One underappreciated enforcement vector: whistleblowers. The IRS Whistleblower Program pays informants 15–30% of collected penalties. Former business partners, accountants, ex-spouses, and disgruntled employees have all triggered FBAR investigations.

FBAR vs. Form 8938: You May Need to File Both

FBAR and Form 8938 (Statement of Specified Foreign Financial Assets, required under FATCA) overlap but are not identical. Many expats must file both — and assume incorrectly that filing one satisfies the other.

| Feature | FBAR (FinCEN 114) | Form 8938 (FATCA) |

|---|---|---|

| Filed with | FinCEN (BSA E-Filing System) | IRS (attached to Form 1040) |

| Threshold (expats) | $10,000 aggregate | $200K (single) / $400K (MFJ) year-end, or $300K/$600K at any point |

| What’s covered | Foreign financial accounts | Broader — includes direct interests in foreign entities, foreign pension rights, certain foreign contracts |

| Penalty for non-filing | Up to $16,536/year (non-willful) | $10,000 + $50,000 for continued non-compliance after IRS notice |

| Deadline | April 15, auto-extension to Oct 15 | Same as tax return (April 15 / Oct 15) |

The 8938 thresholds are much higher — good news for expats with modest foreign account balances. But if you’re above both thresholds, both forms are required. An FBAR filed correctly doesn’t satisfy the 8938 requirement and vice versa.

For a deeper dive into the full US expat tax picture — including the FEIE, foreign tax credits, and state filing traps — see our complete US expat banking and taxes guide.

Deadline and How to File

The FBAR deadline is April 15, with an automatic extension to October 15. You don’t need to request the extension — it kicks in automatically if you miss April 15. However, “automatic extension” does not mean “free pass.” If you’re contacted by FinCEN or the IRS before you file, the late-filing analysis changes dramatically.

FBAR is filed electronically through the BSA E-Filing System at bsaefiling.fincen.treas.gov. It’s completely separate from the IRS filing system. There is no paper option for most filers.

If you have accounts in multiple countries, all accounts are listed on a single Form 114. The form asks for: financial institution name and address, account number, maximum value during the year (in USD), and account type. There’s no tax computation involved — it’s purely a disclosure form.

If You’re Already Behind: Your Options

If you’ve missed FBAR filings for one or more years, the worst thing to do is nothing. The IRS has a statute of limitations for civil FBAR penalties — generally 6 years from the filing deadline — but that clock only starts when the FBAR is actually filed. If you never filed, the clock never started.

Two primary catch-up programs exist for expats:

Delinquent FBAR Submission Procedures

If you properly reported all foreign income on your US tax returns but simply forgot to file the FBAR, you may qualify for the Delinquent FBAR Submission Procedures. Requirements: the IRS hasn’t contacted you about the missing FBARs, your foreign income was fully reported, and your failure was non-willful. Result: file the delinquent FBARs with a brief statement of explanation, pay zero penalty.

Streamlined Foreign Offshore Procedures

For expats who missed both FBARs and US tax returns, Streamlined Filing is the path forward. You file 3 years of tax returns, 6 years of FBARs, pay any taxes owed plus a 3% miscellaneous offshore penalty — and for expats living abroad, that 3% penalty is waived entirely. The program requires certifying that your non-compliance was not willful.

The streamlined procedures are genuinely effective and widely used. Expat tax firms see dozens of clients use them successfully each year. The key is acting before the IRS contacts you — at that point, the amnesty programs close.

One caution: the IRS has signaled increased scrutiny of streamlined certifications where the amounts involved are large. If you have significant unreported foreign assets, hire a tax attorney, not just an accountant, before submitting.

The 5 Most Expensive FBAR Mistakes

- Assuming low balances don’t matter. The $10,000 threshold is aggregate. Five accounts with $2,500 each equal $12,500 — that triggers the requirement even though no single account exceeded $10,000.

- Forgetting foreign pension accounts. If you’ve worked abroad and participated in a local pension plan, that account almost certainly counts. Germany’s Riester-Rente, UK ISAs, Australian superannuation — all potentially reportable.

- Ignoring signature authority accounts. If you sign on your employer’s foreign business account, you may be required to file even though the money isn’t yours. Check with your compliance department.

- Treating FBAR and Form 8938 as the same form. They overlap but aren’t identical. If you’re above both thresholds, both must be filed. An expat tax software that files your 1040 doesn’t automatically file your FinCEN 114.

- Waiting for the problem to go away. FBAR penalties have no statute of limitations on an unfiled form. Every year you don’t file is another year of potential exposure. The streamlined amnesty programs are available now — they won’t necessarily be available forever.

Practical Setup: How to Structure Your Accounts as an Expat

The goal isn’t to avoid foreign accounts — that’s impossible if you live abroad. The goal is to file correctly and minimize administrative friction.

Keep a US bank account active throughout your time abroad. Charles Schwab’s international account is widely used by expats because it refunds all ATM fees worldwide, has no foreign transaction fees, and doesn’t close accounts due to foreign addresses — a real problem with many US banks. This account keeps you anchored to the US banking system, simplifies your FBAR (one or two accounts rather than ten), and avoids the situation where your only bank accounts are foreign.

If you need a US business account you can open remotely, Mercury is built for remote entrepreneurs and offers USD accounts accessible from anywhere without requiring US residency.

Maintaining a valid US mailing address matters for both the IRS and FinCEN. Many expats use a virtual mailbox like Traveling Mailbox ($15/month) to hold a real US street address in one of 50+ cities, receive and scan mail, and keep a valid IRS correspondence address — especially important when you’re receiving FBAR confirmation letters or IRS notices that need fast responses. See our complete virtual mailbox guide for expats for the full breakdown.

Track your foreign account balances at year-end and at month-high each month. You need to report the maximum value during the year, and banks often don’t keep that data easily accessible after the fact. A simple spreadsheet updated monthly saves hours during tax season.

For expats who want to understand the broader tax picture — including how to legally reduce your US tax bill through the Foreign Earned Income Exclusion — read our guide to zeroing out federal income tax as an expat via the FEIE.

Bottom Line

FBAR is not a tax. It’s not a wealth tax or a penalty for earning money abroad. It’s a transparency requirement that the US government takes extremely seriously — with penalties designed more for offshore tax evaders than for expats living normal lives abroad with local bank accounts. That mismatch has created millions of unintentional non-filers who don’t know they’re exposed.

The good news: if you haven’t filed and your noncompliance was honest, the IRS provides real paths to compliance at zero or minimal cost. The bad news: those paths require action before the IRS comes to you. Once an audit or investigation begins, your options narrow sharply.

File your FBAR, understand what counts, and track your maximum balances. It takes 20 minutes a year. The downside of not doing it is measured in six figures.

Financial disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. FBAR rules are complex and penalties are significant — consult a qualified US expat tax attorney or CPA for guidance specific to your situation. IRS penalty amounts are adjusted annually and current as of the date of publication.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.