The Expat Estate Plan Trap: Protect Your Wealth Across Borders

14 min read · 3,463 words

Japan will take 55% of your estate. France will take 60% if you leave assets to a non-relative. And the US? It’ll tax your worldwide assets at 40% — even if you haven’t set foot on American soil in a decade.

If you’re an American living abroad and your estate plan consists of a will you drafted before you left the States, you’re sitting on a financial time bomb. Cross-border estate planning isn’t optional — it’s the difference between your heirs inheriting your wealth and two (or three) governments carving it up first.

The 2026 changes make this more urgent than ever. The One Big Beautiful Bill Act locked in a $15 million per-person federal estate tax exemption, which sounds generous — until you realize that most expats face double taxation from their country of residence on top of the US obligation. And forced heirship laws in countries like France, Spain, and Colombia can override your will entirely.

Related: expat 401k and IRA guide

Here’s everything you need to know to protect your wealth across borders.

The US Taxes Your Estate Worldwide — Even Abroad

Let’s start with the uncomfortable truth that catches most expats off guard: the United States taxes your worldwide estate regardless of where you live, where your assets are, or how long you’ve been gone.

Unlike most countries that only tax assets within their borders, the US follows a citizenship-based system. If you hold a US passport or a green card, the IRS considers your entire global estate — your apartment in Medellín, your brokerage account in Singapore, your rental property in Portugal — fair game for estate tax.

The current federal estate tax rate is a flat 40% on assets exceeding the exemption threshold. And this isn’t just theoretical. When you die abroad, your executor still needs to file IRS Form 706 (United States Estate Tax Return) within nine months. If your estate includes foreign assets, add Form 3520 to the mix. Miss these deadlines and the penalties are brutal — 25% of the reportable value for a missed Form 3520.

This worldwide taxation becomes a real problem when you layer in the tax obligations of your country of residence. If you’re living in France with $2 million in assets, both the US and France may want their cut. That’s the double taxation trap we’ll break down below.

2026 Estate Tax Exemptions: What Changed

The One Big Beautiful Bill Act (OBBBA), signed in July 2025, made the increased estate tax exemptions permanent. Here’s what that means for 2026:

| Status | 2025 Exemption | 2026 Exemption | Change |

|---|---|---|---|

| Individual | $13.99 million | $15 million | +$1.01M |

| Married couple | $27.98 million | $30 million | +$2.02M |

| Tax rate above exemption | 40% | 40% | No change |

Before the OBBBA, the exemption was scheduled to sunset back to roughly $7 million in 2026. That would have caught millions of Americans off guard. Instead, the $15 million threshold is now permanent and indexed to inflation going forward.

Why this matters for expats: On paper, $15 million sounds like most people are safe. But consider what counts toward your estate: US and foreign real estate, investment accounts (including those held at foreign brokerages), retirement accounts, life insurance death benefits, business interests, and even foreign pensions. For expats who’ve been building wealth across multiple countries for decades, these numbers add up faster than you’d think.

And here’s the kicker: even if your estate falls below the US exemption, you may still owe significant inheritance tax to your country of residence, which may have far lower thresholds. The UK’s nil-rate band is just £325,000 (~$410,000). Germany exempts €500,000 for a spouse. Japan’s base exemption is roughly ¥30 million (~$200,000).

The Double Taxation Trap

This is where expat estate planning gets truly ugly. Here’s a scenario that plays out more often than you’d think:

Meet Sarah. She’s a US citizen living in Paris with a €1.5 million apartment, a US brokerage account worth $800,000, and a French life insurance contract (assurance vie) worth €400,000. Her total estate: roughly $2.8 million.

- US estate tax: Below the $15M exemption, so $0 federal estate tax. Good.

- French inheritance tax: She has two children. Under French law, they’re entitled to two-thirds of her estate (forced heirship). The French tax on each child’s share starts at 5% and scales to 45% above €1,805,677. Her children face a combined French tax bill of approximately €180,000.

- Net result: Even though Sarah owes nothing to the US, France takes roughly $200,000.

Now imagine Sarah’s estate was worth $16 million. She’d owe both French inheritance tax and US estate tax on the $1 million above the exemption — potentially $400,000 to the US plus French taxes. Without proper planning and the US-France estate tax treaty, parts of her estate could be taxed twice.

The US has estate tax treaties with only 15 countries. If you live in Mexico, Colombia, Thailand, Panama, or any other popular expat destination without a treaty, preventing double taxation requires careful structuring — and there are no guarantees.

For moving money between accounts during estate settlement, services like Remitly can handle smaller transfers, while Mercury offers US business banking that simplifies the process if the estate includes a US-based business entity.

Related: Roth IRA expat guide

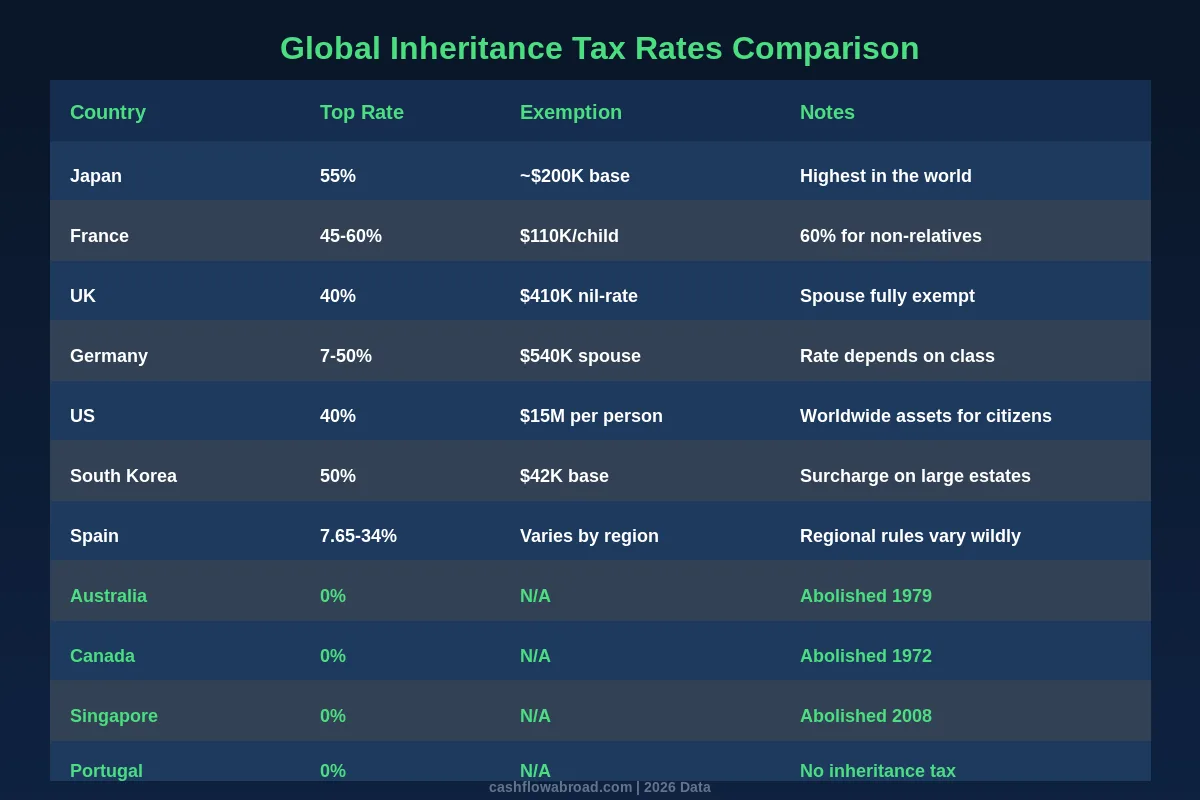

Global Inheritance Tax Rates: Country-by-Country

Before you can plan, you need to know what you’re up against. Here’s how the world’s major countries tax inherited wealth:

High-Tax Countries (25%+ Top Rate)

| Country | Top Rate | Key Exemption | Who Pays |

|---|---|---|---|

| Japan | 55% | ¥30M + ¥6M per heir (~$200K base) | Heirs (beneficiary-based) |

| South Korea | 50% | ~$42K base | Estate, with surcharge on large amounts |

| France | 45-60% | €100K per child | Heirs; 60% rate for non-relatives |

| United States | 40% | $15M per person | Estate (worldwide for citizens) |

| United Kingdom | 40% | £325K nil-rate band | Estate; spouse fully exempt |

| Spain | 7.65-34% | Varies wildly by region | Heirs; Andalucía nearly eliminated it |

| Germany | 7-50% | €500K spouse, €400K per child | Heirs; rate depends on relationship class |

Low-Tax Countries (Under 25%)

| Country | Top Rate | Notes |

|---|---|---|

| Italy | 4-8% | 4% for close relatives above €1M; 8% for non-relatives |

| Switzerland | 0-50% | Varies by canton; spouse/children often exempt |

| Ireland | 33% | €335K tax-free for children |

| Netherlands | 10-40% | €723K exempt for partners |

| Colombia | ~10% | Progressive rate on inheritance as income; forced heirship applies |

Zero Inheritance Tax Countries

| Country | Abolished/Never Had | Catch? |

|---|---|---|

| Australia | Abolished 1979 | Capital gains tax on inherited assets when sold |

| Canada | Abolished 1972 | Deemed disposition at death triggers capital gains |

| New Zealand | Abolished 1992 | No catch — truly tax-free inheritance |

| Singapore | Abolished 2008 | No catch |

| Portugal | No inheritance tax | 10% stamp duty on Portuguese assets |

| Mexico | No inheritance tax | Income tax may apply on inherited assets |

| UAE / Bahrain / Qatar | Never had | Islamic succession law may apply |

Notice the pattern: even “zero tax” countries often have a backdoor tax through capital gains or stamp duties. Australia and Canada are the classic traps — no inheritance tax, but the deemed disposition at death can trigger a massive capital gains bill for your heirs.

Forced Heirship Laws: When Your Will Doesn’t Matter

This is the section that shocks most Americans. In the US, you can leave your entire estate to your cat if you want. In much of the world, you literally cannot.

Forced heirship means the law dictates that a fixed portion of your estate must go to specific family members — usually children, and sometimes a surviving spouse — regardless of what your will says.

How Much Your Children Are Entitled To

| Country | Reserved Portion for Children | Can You Override It? |

|---|---|---|

| France | 50% (1 child), 67% (2 children), 75% (3+) | Only the “free portion” is yours to allocate |

| Spain | Two-thirds of estate | Varies by region; some allow more flexibility |

| Italy | 50% (1 child), 67% (2+ children) | Very limited exceptions |

| Germany | 50% of statutory share (Pflichtteil) | Children can claim cash equivalent even if disinherited |

| Japan | 50% of estate split among heirs | Can be challenged in family court |

| Colombia | 50% forced, 25% mejora (children only) | Only 25% is freely distributable |

| Brazil | 50% to “necessary heirs” | Cannot override by will |

| UAE | Sharia law applies to Muslims | Non-Muslims can now elect their home country’s law in some emirates |

The real-world impact: If you’re an American living in Spain and you own an apartment there, Spanish forced heirship rules apply to that property — even if your US will says everything goes to your spouse. Your children are legally entitled to two-thirds of the property’s value. If your spouse isn’t a parent of those children (blended families), this gets extremely messy.

The European Succession Regulation (Brussels IV) Workaround

There’s a critical escape hatch for US citizens in the EU. Under the European Succession Regulation (EU Regulation 650/2012), you can elect to have the law of your nationality govern your estate, rather than the law of your country of residence.

Since the US has no forced heirship laws, a US citizen living in France can elect US law and regain full testamentary freedom. This election must be made explicitly in your will. It applies in all EU member states except Denmark and Ireland.

Warning: France added a “clawback” provision in 2021. If your children would have received a forced share under French law but were disinherited under your elected foreign law, they can claim compensatory payment against assets located in France. So the workaround isn’t bulletproof for French real estate.

If you’re considering Colombia as a base — where forced heirship reserves 75% of your estate — check out ColombiaMove.com’s complete visa guide for understanding residency options that may affect succession rules.

Why Your US Trust Might Be Worthless Abroad

If you have a revocable living trust — the cornerstone of most American estate plans — here’s the bad news: many countries don’t recognize trusts at all.

The concept of a trust is fundamentally an Anglo-American legal invention. Civil law countries (most of continental Europe, Latin America, and parts of Asia) have no equivalent legal framework. Here’s what happens when your US trust meets foreign law:

How Different Countries Treat US Trusts

| Country | Trust Recognition | What Happens |

|---|---|---|

| France | Partially recognized | Trust assets may be subject to French wealth tax; grantor still taxed as owner |

| Germany | Treated as transparent | Assets taxed as if directly owned; trust offers no estate planning benefit |

| Spain | Not recognized | Trust assets treated as personal property of grantor or beneficiary |

| Italy | Limited recognition since 1989 | Subject to Italian trust tax rules; complex compliance |

| Japan | Own trust laws | Foreign trusts may be reclassified under Japanese tax rules |

| Colombia | Has “fiducia” (similar concept) | US trusts not automatically recognized; may need local structuring |

| UK / Australia | Fully recognized | Common law countries — trusts work as expected |

The IRS adds another layer: If you create a trust abroad or your US trust becomes a “foreign trust” (which can happen if you move abroad and become the trustee while non-US persons are beneficiaries), punitive IRS reporting kicks in. Forms 3520 and 3520-A carry automatic penalties of 35% of the trust’s gross value for failure to file.

The takeaway: your US trust may actively harm your estate plan when you move abroad. At minimum, you need a cross-border estate planning attorney to review how your trust interacts with local law.

US Estate Tax Treaty Countries: The Full List

The US has estate and gift tax treaties with exactly 15 countries. If you live in one of these countries, you have a framework for preventing double taxation. If you don’t, you’re navigating without a map.

Related: complete FBAR and FATCA guide

The 15 Treaty Countries

| Country | Treaty Type | Key Benefit |

|---|---|---|

| Australia | Situs | Tax credit for Australian taxes paid |

| Austria | Situs | Austria abolished its inheritance tax in 2008 |

| Canada | Special (income tax treaty covers estate) | Deemed disposition rules coordination |

| Denmark | Domicile | Primary taxing rights to domicile country |

| Finland | Situs | Tax credit mechanism |

| France | Domicile | Domicile country gets first taxing rights |

| Germany | Domicile | Credits for taxes paid to the other country |

| Greece | Situs | Assets taxed where located |

| Ireland | Situs | Tax credit for taxes paid |

| Italy | Situs | Assets taxed by country of location |

| Japan | Situs | Prevents double tax on same assets |

| Netherlands | Domicile | Fiscal domicile determines primary tax |

| South Africa | Situs | Tax credit mechanism |

| Switzerland | Situs | Canton-level coordination |

| United Kingdom | Domicile | Domicile-based primary taxing rights |

What If You’re in a Non-Treaty Country?

Most popular expat destinations — Mexico, Colombia, Thailand, Panama, Costa Rica, Portugal, Spain — have no estate tax treaty with the US. For these countries:

- Foreign Tax Credit: You can claim a credit on Form 706 for foreign death taxes paid (IRS Code §2014), but it’s limited and doesn’t always fully offset.

- Asset location strategy: Careful placement of assets by jurisdiction can minimize overlap.

- Life insurance: Proceeds from US life insurance are generally estate-tax-included but income-tax-free, and can provide liquidity to pay estate taxes without selling assets.

- Gifting strategy: The annual gift tax exclusion ($18,000 per recipient in 2026) lets you transfer wealth during your lifetime, reducing your taxable estate.

For expats managing investments across borders, platforms like tastytrade keep your US brokerage accessible from abroad, while SoFi provides a solid foundation for US-based banking and investing that won’t close your account for having a foreign address.

Countries With Zero Inheritance Tax

If estate tax planning is a major concern, choosing the right base country can eliminate an entire layer of complexity. These countries have abolished or never implemented inheritance taxes:

Top Zero-Tax Destinations for Expats

Portugal — No inheritance tax, and the NHR (Non-Habitual Resident) regime offered up to 10 years of reduced income taxation. Portugal charges a 10% stamp duty on Portuguese assets at death, but that’s far less than the 40%+ rates in France or the UK. Popular with American and British retirees for good reason.

Singapore — Abolished estate duty in 2008. No capital gains tax either, making it arguably the most estate-friendly jurisdiction in the world for wealthy expats. The catch: cost of living is steep and permanent residency is competitive.

Australia — No inheritance tax since 1979, but beware the deemed capital gains trap. When you inherit assets, their cost base may reset (or not, depending on when the deceased acquired them), and selling triggers capital gains tax at your marginal rate (up to 45%).

New Zealand — Abolished estate duty in 1992 with no capital gains tax on most assets. One of the cleanest inheritance situations globally.

Mexico — No inheritance tax. However, inherited assets may be subject to income tax, and the legal process (succession proceedings) can take 1-2 years. If you own property in Mexico’s restricted zone (near the coast or border), a fideicomiso (bank trust) structure adds complexity.

Remember: Even in zero-tax countries, US citizens still face US estate tax on worldwide assets above the $15M exemption. Moving to Portugal eliminates the local tax but doesn’t eliminate the US obligation. Your citizenship follows you to the grave — literally.

8 Estate Planning Mistakes Expats Make

Mistake #1: Assuming Your US Estate Plan Works Abroad

Your will drafted by a lawyer in Ohio doesn’t account for French forced heirship, Spanish community property rules, or the fact that Colombia doesn’t recognize your revocable trust. A domestic estate plan is a domestic solution — it stops at the border.

Mistake #2: Having One Will for Everything

Best practice is to have separate wills for each jurisdiction where you own significant assets. A US will for US assets. A French will for French property. A Colombian will for Colombian assets. The trick: they must be coordinated so one doesn’t accidentally revoke the other. Always include a clause like “this will covers only my assets located in [Country].”

Mistake #3: Ignoring Forced Heirship Until It’s Too Late

If you own property in a forced heirship country, those rules likely apply to that property regardless of your nationality or what your will says. You can’t disinherit your children from a French apartment just because you’re American — unless you’ve properly elected US law under the EU Succession Regulation and even then, France’s clawback may apply.

Mistake #4: Thinking Your Trust Travels Well

We covered this above, but it bears repeating: your US revocable living trust may be invisible, worthless, or actively harmful depending on where you live. Some countries will tax the trust itself. Others will ignore it and apply their own succession rules to the underlying assets.

Mistake #5: Not Updating Beneficiary Designations

Your 401(k), IRA, life insurance, and brokerage accounts pass by beneficiary designation — not by will. If your ex-spouse is still listed as the beneficiary on your Fidelity account, they’re getting the money regardless of what your will says. Expats often forget to update these after major life changes.

Related: rental property abroad guide

Mistake #6: Ignoring the FBAR and FATCA for Estate Purposes

Your executor needs to file the final FBAR (FinCEN 114) and FATCA Form 8938 for the year of your death. If they don’t know about your foreign accounts — or can’t access them — penalties accumulate. Keep a detailed inventory of all foreign accounts and share it with your executor. This isn’t just about tax compliance; it’s about making sure nothing falls through the cracks.

Mistake #7: Not Planning for Probate in Multiple Countries

If you own real estate in three countries, your estate may go through probate in all three — simultaneously, under three different legal systems, with three different timelines. Without proper structuring, this can take years and cost tens of thousands in legal fees. Solutions include holding property through corporate structures, using local trusts where recognized, or gifting property during your lifetime.

Mistake #8: Forgetting About Digital Assets and Crypto

Your cryptocurrency holdings, online business accounts, domain names, and digital content are all part of your estate. If your heirs don’t have access to your private keys or passwords, these assets are effectively lost. Keep an encrypted digital inventory and make sure your executor knows how to access it. For crypto specifically, tools like CoinTracking help maintain records that your executor will need for tax compliance, and platforms like Kraken have estate settlement procedures in place.

Your Cross-Border Estate Plan: Step by Step

Here’s the practical action plan. Do this whether your estate is $200,000 or $20 million — the complexity scales, but the framework is the same.

Step 1: Take a Global Asset Inventory

List every asset you own, organized by country of location:

- Real estate (including any land or timeshares)

- Bank accounts (foreign and domestic)

- Brokerage and retirement accounts

- Business interests and ownership stakes

- Life insurance policies

- Cryptocurrency and digital assets

- Vehicles, art, jewelry, and other tangibles

- Foreign pensions or social security entitlements

Step 2: Identify Applicable Laws

For each country where you hold assets, determine:

- Does the country have an inheritance/estate tax? At what rate?

- Does the US have an estate tax treaty with this country?

- Do forced heirship laws apply? To which assets?

- Are trusts recognized? How are they taxed?

- What is the probate process and timeline?

Step 3: Engage Cross-Border Legal Counsel

You need attorneys in each jurisdiction where you hold significant assets, plus a US-based international estate planning attorney to coordinate. This is not a DIY project. A single mistake — like one will accidentally revoking another — can cost your heirs hundreds of thousands.

Step 4: Create Jurisdiction-Specific Wills

Draft separate, coordinated wills for each country. Ensure each will:

- Specifies it covers only assets in that jurisdiction

- Doesn’t revoke wills in other jurisdictions

- Meets all local formal requirements (notarization, witnesses, language)

- Includes a US law election under the EU Succession Regulation (if applicable)

Step 5: Review Beneficiary Designations

Audit every account that passes by beneficiary designation. Update as needed. Consider whether your foreign spouse or children face any cross-border complications in claiming these assets.

Step 6: Consider Lifetime Gifting

The US annual gift tax exclusion is $18,000 per recipient (2026). Gifts to your spouse who is a US citizen have an unlimited exclusion. Gifts to a non-citizen spouse are limited to $185,000 annually. Strategic gifting during your lifetime reduces your taxable estate and simplifies probate.

Step 7: Set Up a Digital Estate Plan

Create an encrypted document or use a password manager with emergency access features. Include:

- All account credentials and 2FA backup codes

- Cryptocurrency private keys and seed phrases

- Location of physical documents (wills, deeds, insurance policies)

- Contact information for attorneys in each jurisdiction

Protect your digital estate plan with a strong VPN like NordVPN when accessing financial accounts from abroad, and use a dedicated password manager with legacy contact features. Store sensitive estate documents and communications in Proton Mail and Proton Drive — end-to-end encrypted, Swiss-based, and your heirs can access them with the right credentials without worrying about a provider scanning or locking the account.

Step 8: Review Annually

Tax laws change. You change countries. You acquire or sell assets. Relationships evolve. Review your cross-border estate plan every year — or whenever you have a major life event (marriage, divorce, new child, new country, significant asset acquisition).

Conclusion

Cross-border estate planning isn’t optional for US expats — it’s one of the most consequential financial decisions you’ll make. The $15 million exemption gives most Americans breathing room on the federal side, but it means nothing if France takes 45%, your trust is invisible in Spain, or forced heirship overrides your wishes in Colombia.

The core principle is simple: plan for every jurisdiction where you hold assets, not just the one where you live. Get local counsel. Coordinate your wills. Update your beneficiaries. And for the love of your heirs, document your digital assets.

Your wealth took decades to build across borders. Don’t let a few missing documents or a misunderstood foreign law undo it all.

If you’re considering a move to Colombia as part of your geographic arbitrage strategy, ColombiaMove.com’s guide to moving as an American covers residency options, and the banking guide for foreigners explains how to structure your financial accounts there. For expat health coverage that follows you anywhere — and is a key component of your estate’s ongoing obligations — SafetyWing provides global health insurance designed specifically for nomads and expats.

This article is for informational purposes only and does not constitute legal or tax advice. Consult qualified cross-border estate planning professionals for your specific situation.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.