Your US Credit Score Is Dying Abroad — Stop It Now

Your FICO score goes dormant after 6 months of inactivity — and card issuers close accounts in as little as 3 months. Here's the full expat credit maintenance system.

FICO scores go dormant in 6 months of inactivity. Learn the exact system to keep your US credit score alive while living abroad as an expat.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Most US expats nail the hard stuff — they set up an offshore bank account, claim the Foreign Earned Income Exclusion, find cheap health insurance. Then they return home three years later and discover their 760 FICO score has quietly cratered to 580. They can't get a mortgage. Sometimes they can't even lease a car.

It happens fast, and it happens silently. Your FICO score goes dormant — essentially "no score" — if zero US credit accounts report activity for six consecutive months. After that threshold, lenders treat you like a ghost. And card issuers have been known to close inactive accounts in as little as three months, which triggers a cascade through your credit file that takes years to repair.

This isn't a hypothetical. Expat financial forums are full of threads from people who did everything right financially while abroad — no debt, growing savings, disciplined spending — and came back to find their credit life had effectively been wiped. The fix is simple once you know about it, but most people don't find out until the damage is done.

Why Your Credit Score Dies While You're Abroad

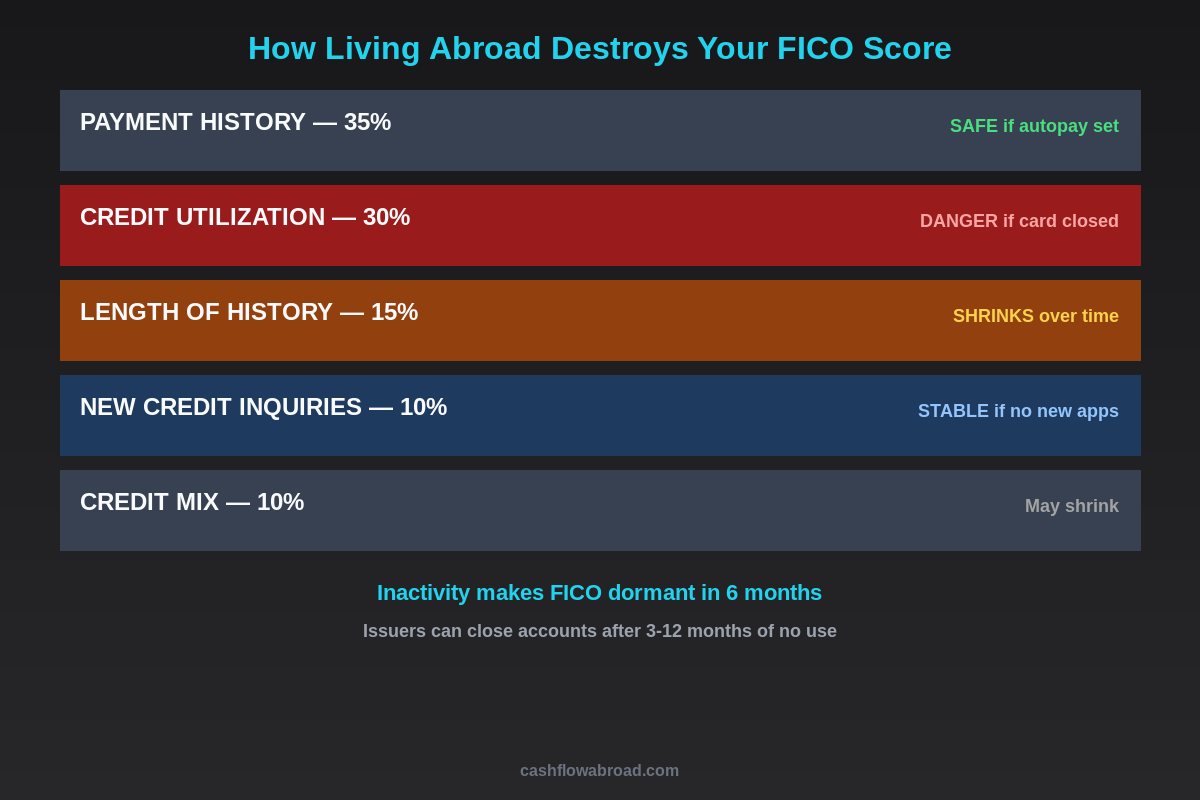

FICO scores are calculated from five categories. All five are vulnerable when you move abroad and stop actively using US credit accounts:

| Factor | Weight | What Happens Abroad | Risk Level |

|---|---|---|---|

| Payment History | 35% | Safe if autopay is set; dangerous if you forget and miss a payment | Low (if managed) |

| Credit Utilization | 30% | When a card gets closed, its limit disappears — your utilization spikes instantly | High |

| Length of History | 15% | A closed card's age eventually drops off your report; average account age shrinks | High |

| New Credit Inquiries | 10% | Stable as long as you don't apply for new credit abroad | Low |

| Credit Mix | 10% | May thin out if accounts close | Medium |

The real trap is credit utilization. Say you have three cards with a combined $30,000 limit and you carry $2,000 in balances — that's a clean 6.7% utilization. One issuer closes your $12,000 card due to inactivity. Suddenly you have $18,000 in available credit and the same $2,000 balance — utilization jumps to 11%. If two cards get closed, it climbs to 33%, which is the threshold where FICO scores start dropping meaningfully. All without you spending a single extra dollar.

The Credit Death Timeline

Here's roughly what happens if you leave for abroad and do nothing with your US credit:

- Month 3–6: Some issuers flag accounts as inactive. Lower-limit cards with smaller issuers may close with no warning, just a letter to a US address you might not be monitoring.

- Month 6: If no account reports activity to the bureaus, your FICO score can no longer be calculated. Lenders pull your report and see "no score" — treated the same as subprime.

- Month 12–18: Major issuers (Chase, Amex, Citi) may also close inactive accounts. When they do, the credit limit vanishes from your utilization calculation.

- Month 24+: If an account open for 10+ years gets closed, its age eventually stops counting toward your average account age — though closed accounts in good standing stay on your report for up to 10 years before dropping off entirely.

The damage isn't always permanent, but rebuilding takes 12–24 months of consistent active credit use. If you're returning home expecting to buy a house, you need scores above 740 to qualify for the best conventional mortgage rates. Scores under 620 disqualify you from most conventional financing entirely.

The Expat Credit Maintenance Stack

Keeping your credit alive abroad requires about 15 minutes per year of active management once set up correctly. Here's the complete system:

One Card, One Subscription, One Autopay

Pick your oldest credit card — the one with the longest history and highest limit. Set a single small recurring charge on it: a Netflix subscription ($17/month), a Spotify plan ($11/month), or a cloud storage service. Then set that card to autopay the full balance from your US checking account. The card reports activity monthly. The issuer sees a live, paying customer. The account stays open indefinitely.

Do this for every US credit card you want to keep. If you have four cards, four subscriptions. The math is trivial — $44/month in streaming subscriptions keeps $50,000 in credit limits active.

Keep a Real US Bank Account Open

You need a US bank account to automate payments, receive deposits, and maintain a US financial footprint. Charles Schwab International is the standard recommendation for expats — no foreign transaction fees, free ATM withdrawals worldwide, and they've never had the habit of closing expat accounts the way traditional banks sometimes do. Mercury works well for those running a US business abroad.

For more detail on the full expat banking stack, see our complete US expat banking guide and the zero-fee banking stack.

Lock Down a US Address

This is where many expats fail. Banks, credit card issuers, and the IRS need a legitimate US street address — not a P.O. box, not your parents' spare bedroom they may eventually sell. The safest long-term solution is a virtual mailbox service.

Traveling Mailbox provides a real US street address in 50+ cities for around $15/month, scans your incoming mail, and lets you manage everything digitally. You can deposit checks remotely, get IRS correspondence, and maintain a legitimate address for financial accounts. We cover the full strategy in our virtual mailbox guide.

One important caveat: many virtual mailbox addresses are flagged as Commercial Mail Receiving Agencies (CMRAs) in the USPS database. Some banks have started rejecting CMRA-flagged addresses. Traveling Mailbox has addresses that work with most major financial institutions, but confirm your specific bank accepts the address format before relying on it.

State selection matters too. Choose a state with no income tax for your virtual mailbox: Texas, Florida, Nevada, Washington, Wyoming, or South Dakota. You don't want to accidentally establish tax residency in California or New York just because you used a friend's apartment address there.

The Best Credit Cards to Keep Active Abroad

Not all credit cards behave the same when you're spending in foreign currencies. These are the ones worth keeping active:

| Card | Foreign Transaction Fee | Why Keep It | Annual Fee |

|---|---|---|---|

| Chase Sapphire Reserve | 0% | 8x points on Chase Travel, 3x dining globally — premium rewards with no FX hit | $550 |

| Chase Sapphire Preferred | 0% | 3x dining + 2x travel worldwide, great for moderate spenders | $95 |

| Capital One Venture/VentureX | 0% | 2x miles on everything — simplest earning structure for expats | $95/$395 |

| Schwab Investor Card (Amex) | 0% | 1.5% cash back direct to brokerage — passive wealth building while spending | $0 |

| Discover it Miles | 0% | $0 annual fee — perfect "set and forget" card for subscription autopay | $0 |

The key principle: use Visa or Mastercard abroad, not Amex or Discover. Acceptance is far wider globally, and some automated kiosks (train stations, toll booths) only accept chip-and-PIN cards, which US-issued cards generally don't have.

Active Monitoring: The Annual Credit Audit

Once your maintenance system is running, schedule one annual check-in:

- Pull all three free credit reports from AnnualCreditReport.com (Equifax, Experian, TransUnion)

- Verify all expected accounts are still open and showing recent activity

- Check that your US address is current with each card issuer

- Review for fraudulent accounts — expats are common identity theft targets since they're slower to notice unusual activity

- Confirm your FICO score is calculable (if it shows "no score," take immediate action)

Many credit card issuers now offer free FICO score monitoring through their apps. Chase, Amex, and Discover all provide this — enable alerts on at least one card so you're notified of significant score changes.

The Mortgage Reality When You Return

The stakes become concrete when you want to buy property after years abroad. Conventional lenders use automated underwriting with rigid credit score minimums:

- 760+: Best rates on conventional mortgages, full product menu available

- 740–759: Good rates with minor pricing adjustments

- 700–739: Rates noticeably higher; some lenders require extra documentation for foreign income

- 620–699: FHA loan territory; significantly higher rates and PMI requirements

- Below 620: Most conventional lenders decline; expat income complexity compounds the difficulty

- "No score" / dormant file: Treated as subprime or declined outright — requires manual underwriting that most retail lenders don't offer

Specialized expat mortgage lenders do offer DSCR (Debt Service Coverage Ratio) loans for investment properties that bypass personal credit requirements — qualification is based on rental income, not your credit file. But for a primary residence, there's no shortcut: you need an active credit history. The difference between a 720 and 760 FICO on a $500,000 30-year mortgage can be $40,000–$80,000 in total interest paid.

See our expat investing playbook for how real estate abroad fits into a global wealth strategy.

The Authorized User Shortcut

If your credit profile is thin or you've already let some accounts go dormant, ask a trusted family member or partner with excellent credit to add you as an authorized user on their oldest, highest-limit card. You don't need to use the card or even receive it physically. Their payment history and credit limit get added to your credit file immediately. This is particularly useful for expats planning to return and buy property within one to three years.

The reverse also works: if you're concerned a specific card will close, ask your issuer whether authorized user activity — someone else occasionally charging to your card — counts toward keeping the primary account active. Most issuers consider authorized user activity in their inactivity calculations.

Common Mistakes That Accelerate the Damage

Canceling cards before you leave. This immediately removes the credit limit from your utilization calculation and begins the clock on losing that account's age contribution. Close nothing before you go. Let dormant cards die naturally only if you can't avoid it — and try to replace any lost limit with other cards first.

Letting a payment slip while traveling. One 30-day late payment can drop a 760 FICO to 650–700 overnight. Set every US card to autopay the full balance. Verify the autopay is linked to an account that will actually have sufficient funds when the charge hits.

Using a family member's address carelessly. If the state has income tax and you maintain other connections there, you may inadvertently establish domicile for state tax purposes — especially in aggressive states like California, New York, Virginia, and South Carolina. A proper virtual mailbox in a zero-tax state is cleaner and carries fewer risks.

Forgetting to notify card issuers of travel. Many issuers will flag or freeze cards if they see foreign charges that don't match the address on file. A quick update to your account profile indicating you're an international account holder prevents declined transactions at inconvenient moments.

The Payoff for Getting This Right

The expats who handle this correctly barely notice the maintenance overhead. They have two cards on autopay for streaming subscriptions, a Traveling Mailbox address in Texas, and a Schwab account receiving their remote income. Their FICO scores stay above 750 for the entire duration of their time abroad. When they return — whether it's two years or twelve — they qualify for the best mortgage rates and can access the US financial system as though they never left.

The ones who don't handle it spend 12–24 months rebuilding from scratch, often at exactly the moment they're trying to make their biggest financial moves. Set up the maintenance system before you board the plane. It takes two hours once, and it costs less than dinner out each month to maintain.

Financial disclaimer: This article is for informational purposes only and does not constitute financial, credit, or legal advice. Credit scoring models vary and individual results depend on your specific credit history, account types, and issuer policies. Consult a qualified financial advisor or credit counselor before making decisions about your credit accounts or financial planning strategy.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 30, 2026

Expat Tax & FinanceMay 30, 2026

The 3 Bank Accounts Every US Expat Actually Needs

Stop paying $2,400/year in bank fees abroad. This 3-account expat banking setup—Schwab, Mercury, Traveling Mailbox—costs just $180/year.

Expat Tax & FinanceMay 23, 2026

Expat Tax & FinanceMay 23, 2026

Virtual Mailbox for Expats: Keep Your US Banking Alive

How a $15/month virtual mailbox keeps expat bank accounts open, IRS mail received, and brokerages intact. Best states and step-by-step setup.

Expat Tax & FinanceJune 1, 2026

Expat Tax & FinanceJune 1, 2026

State Income Tax Trap Most Expats Don't See Coming

California taxes expats at 13.3% even abroad. Learn how to legally sever domicile before moving overseas and eliminate state income tax.