State Income Tax Trap Most Expats Don't See Coming

California's Franchise Tax Board doesn't care that you live in Portugal. Here's how to legally escape state income taxes before you move abroad.

California taxes expats at 13.3% even abroad. Learn how to legally sever domicile before moving overseas and eliminate state income tax.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Most US expats obsess over the Foreign Earned Income Exclusion, FBAR filings, and the foreign tax credit. They spend weeks optimizing their federal tax situation — and then move to Lisbon without telling California they left. Six months later, the Franchise Tax Board sends them a bill for $28,000.

State income tax is the trap that catches more expats than any IRS form. The federal government at least gives you tools to legally exclude foreign income. Most states don't. And several are famous for auditing former residents years after they've left, demanding back taxes on income they earned on the other side of the world.

Here's exactly how this works, which states are the most aggressive, and the specific checklist to legally sever those ties before you get on the plane.

Why State Taxes Don't Disappear When You Leave

The federal tax system taxes on citizenship — you pay the IRS wherever you live in the world. States don't have that authority. They tax based on domicile, which is distinct from where you happened to spend last Tuesday.

Domicile is your permanent legal home — the place you intend to return to. It's not determined by where you pay rent. It's determined by where your car is registered, where you vote, where you keep your cherished belongings, where your spouse and children live, and what evidence you'd show a tax auditor if they sat across from you demanding proof.

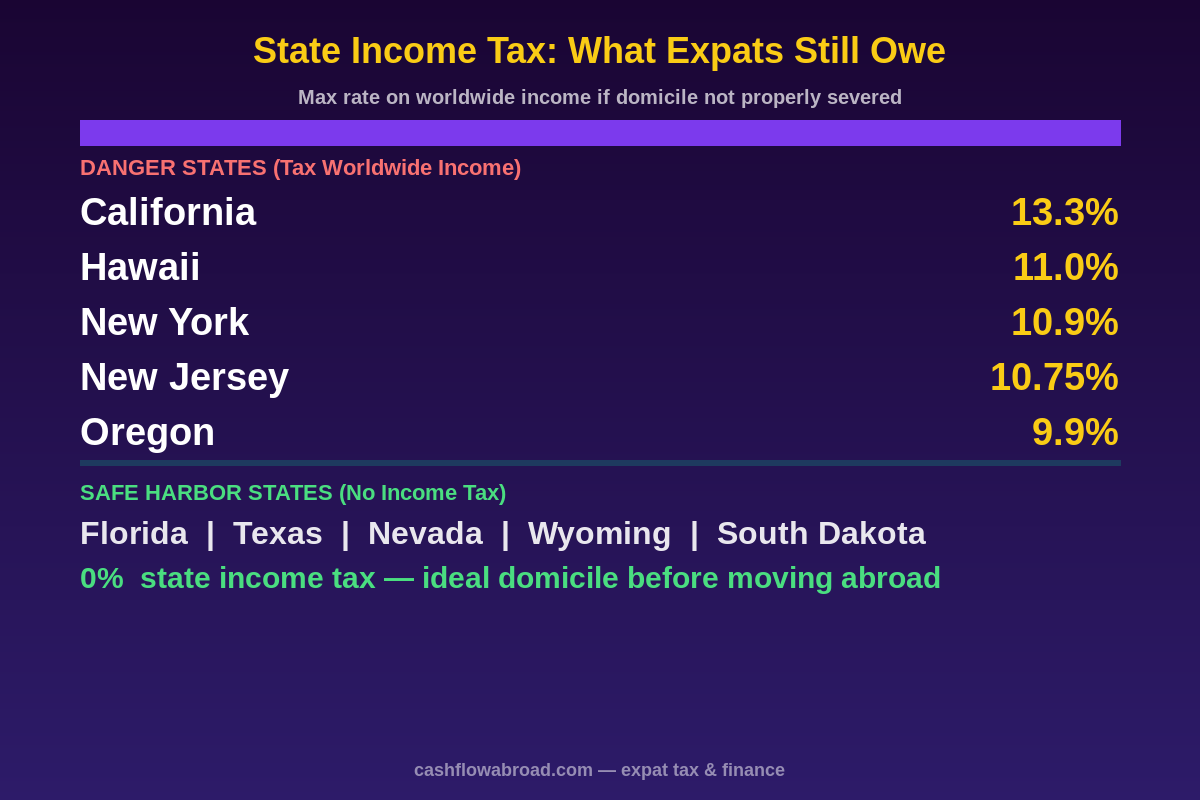

The distinction matters enormously because you can live in Medellín for three years and still technically be domiciled in New York — and therefore owe New York state income tax on every dollar you earned while abroad. New York's top rate is 10.9%. California's is 13.3%. These aren't small penalties for failing to file one form.

And unlike the IRS, states don't recognize the Foreign Earned Income Exclusion. That $126,500 you excluded from your federal return? California taxes it in full.

The "Sticky States": Who Pursues Expats Most Aggressively

Not all states make it easy to leave. A handful have developed a reputation for auditing high-earning former residents years after they've established themselves abroad. Here's the breakdown:

California — The Most Aggressive

California's Franchise Tax Board operates like a collections agency with subpoena power. The FTB can audit up to 4 years from the filing date, or indefinitely if you never filed a return they claim was required. They're specifically interested in high earners — anyone who made $200,000+ and filed a "final" California return gets extra scrutiny.

California's 13.3% top marginal rate is the highest in the country (the extra 1% is a mental health surcharge). The state does not recognize the FEIE. If they decide you're still a California resident while you're teaching English in Thailand, they'll tax your entire worldwide income at California rates.

California has a "546-day safe harbor" for employment-related absences — if you're outside California under an employment contract for at least 546 consecutive days, with California visits under 45 days per year, and intangible income under $200,000, you may qualify. But this is documentation-heavy, and independent contractors often don't qualify at all.

New York — Intent Matters More Than Days

New York focuses on "domicile intent" and the concept of a "permanent place of abode." Even if you're living in Madrid, if you maintain an apartment in New York — or if your spouse remains there — New York may claim you as a statutory resident. Statutory residents owe New York tax on all income worldwide.

The top New York combined rate (state + NYC) for city residents hits 13.65%, making it effectively identical to California's burden. New York's Division of Taxation audits departures by high earners with the same vigor as California's FTB.

Other States That Won't Let Go

| State | Top Rate | Why It's Sticky |

|---|---|---|

| Hawaii | 11.0% | Aggressively audits high earners; no FEIE recognition |

| New Jersey | 10.75% | Requires proof of abandonment; monitors NYC-adjacent earners |

| Oregon | 9.9% | Taxes all income of residents; few concessions for foreign earners |

| Virginia | 5.75% | Considers overseas moves "temporary" without substantial evidence |

| South Carolina | 6.5% | Requires extensive documentation; challenges claims years later |

| New Mexico | 5.9% | Uses complex formulas for multi-state connections |

The states with no income tax — Florida, Texas, Nevada, Wyoming, South Dakota, Washington, Alaska, and Tennessee — cannot pursue you for income you earned abroad because there's nothing to pursue.

The Math: Why This Is Worth Solving

Consider someone earning $120,000 annually as a remote software developer living in Portugal. Their federal liability with the FEIE: $0 on the first $126,500 of foreign earned income. Their California liability if domicile was never severed: potentially $8,000–$12,000 per year in state taxes.

Over a five-year stint abroad, that's $40,000–$60,000 in avoidable tax — before counting penalties, interest, and the cost of a tax attorney if California audits you. The FTB charges 5% per month on unpaid taxes (up to 25% total), plus 0.5% monthly interest. Ignored bills compound fast.

If you're from California, New York, or Hawaii, fixing your domicile situation before you leave isn't optional. It's a financial decision worth tens of thousands of dollars.

The Domicile Checklist: Breaking Ties Legally

The IRS cares where you physically were. States care where your life is anchored. Severing domicile means creating a preponderance of evidence that you have genuinely made a new place your permanent home. Here's what that looks like in practice:

Step 1: Pick a No-Income-Tax State First

Before you leave the US, establish domicile in a state that won't follow you with a tax bill. Florida and South Dakota are the most expat-friendly. Florida requires proof of physical presence (a lease or utility bill), a Florida driver's license, and Florida vehicle registration. South Dakota is even more streamlined — you can establish residency with just a brief visit and a registered address.

The critical piece: you need a physical street address in your new state — not a P.O. box. This is where a virtual mailbox service becomes essential infrastructure. Services like Traveling Mailbox give you a real US street address in Florida, Texas, Nevada, or whichever state you choose. Your mail gets scanned and forwarded digitally wherever you are in the world. That address becomes your legal domicile address for your driver's license application, voter registration, IRS filings, banking, brokerage accounts, and the hundred other places you need a US address. It runs about $15–$25/month — the single most cost-effective piece of expat infrastructure you can set up. The site owner uses it personally.

See the full breakdown: The Complete Virtual Mailbox Guide for Expats.

Step 2: Get the New State Driver's License

Your driver's license state is one of the strongest signals auditors look for. Get a Florida or Texas license before you leave. Most states require you to surrender your old license when you get the new one — do it. An auditor finding a current California driver's license while you claim Florida domicile is an immediate credibility problem that creates years of headaches.

Step 3: Update Voter Registration

Cancel your voter registration in your old state and register in your new one. US citizens abroad can vote via absentee ballot from their last state of residence — so registering in Florida before you leave means you vote as a Florida resident. This is entirely legal, widely recommended by expat CPAs, and strongly documented.

Step 4: File Your Last Return Correctly

File a part-year resident return in your old state covering the period through your departure date. In subsequent years, file as a non-resident only if you have California or New York source income (rental income, stock options from a CA employer, etc.). Don't just stop filing and hope they don't notice — they will, and the statute of limitations never starts running if no return was filed.

Step 5: Sever Physical Ties

This is where most expats fall short. You need to do all of the following:

- Sell or rent your primary home — keeping it vacant is the worst outcome. A vacant home signals intent to return

- Move your valued personal property — family photos, heirlooms, art, and collections. California specifically asks about this in audits

- Close state-based memberships — gym memberships, country clubs, professional licenses, library cards

- Update your address everywhere — banks, brokerage accounts, IRS Form 8822, passport, credit cards

- Move your business connections — if you have a California LLC or business license, consider converting or re-registering out-of-state

For your US banking: maintain accounts that function globally. Charles Schwab International reimburses all ATM fees worldwide and charges no foreign transaction fees — it's the benchmark expat checking account. Mercury handles US business banking without requiring a US physical presence. Both work seamlessly from abroad. Full account-by-account strategy in our expat banking guide.

What Income Can States Still Tax After You Leave?

Even after you successfully establish domicile elsewhere, some income remains taxable in your old state. This is called "source income" — income generated within that state's borders, regardless of where you live:

| Income Type | CA/NY Source Income? | Notes |

|---|---|---|

| Foreign salary (remote job) | No | Once non-resident domicile is established |

| California rental property | Yes | Real property income is always source income |

| California business profits | Yes | Apportioned based on California operations |

| Stock options granted while in CA | Partially | Prorated for CA work period vs. total vesting period |

| Deferred comp from CA employer | Yes | Taxed when received; CA source regardless of where you live |

| Interest, dividends, capital gains | No | Intangible income is non-source once you're a non-resident |

| Social Security | No (CA) / Partial (NY) | California exempts SS; New York taxes above certain thresholds |

The big win for most remote workers: your foreign salary becomes completely state-tax-free once you're a non-resident domiciliary of a no-income-tax state. Capital gains, dividends, and investment income are similarly freed up. The only ongoing state tax exposure is typically source income from property or business operations physically located in the old state.

For investment accounts, move your brokerage to a state-neutral platform with expat-friendly policies. See our expat investing guide for brokerage account strategy and PFIC traps to avoid.

Timing: When to Make This Move

Establish your new domicile before you leave — not after. Changing domicile retroactively while already abroad is significantly harder to prove and much easier for aggressive states to challenge. You lose the ability to show physical presence in your new state, and the timeline looks suspicious.

If you're already abroad and haven't done this yet: the best next step is a brief US trip, specifically to get your new state driver's license, document your presence at your new address, open a new state bank account, and register to vote. Document everything with dated receipts and photos.

For earners above $300,000/year, the risk-adjusted cost of getting this wrong is high enough to justify a CPA who specializes in expat state tax. A proper domicile analysis runs $500–$2,000. It can save $10,000–$30,000 per year. That's a 5x–60x return on the fee.

The Complete Expat Tax Stack

Here's the full optimized setup, end-to-end:

- Establish domicile in Florida or South Dakota — virtual mailbox + driver's license + voter registration before departure

- File final part-year return in old state through your move date

- Claim FEIE or Foreign Tax Credit on your federal return to eliminate or minimize federal liability. Our FEIE guide covers the mechanics of both exclusions

- Maintain expat-friendly US banking — Schwab for personal checking, Mercury for business

- File no return or zero-income return in your new no-income-tax state (usually no filing required if there's no state income tax)

Done correctly, a US expat earning $100,000–$200,000 abroad can legally pay $0 in federal and $0 in state income tax. The FEIE eliminates federal liability; the domicile move eliminates state liability. The total ongoing compliance cost is an annual CPA fee, a $15/month virtual mailbox subscription, and a state driver's license renewal every few years.

Conclusion

The expat community talks endlessly about FEIE thresholds, FBAR deadlines, and PFIC traps. State income tax gets a fraction of the attention — and costs people far more. California's Franchise Tax Board has issued tens of millions of dollars in back-tax assessments to former residents who thought physically leaving the state was enough to end their tax obligation there. It isn't.

The fix is straightforward: pick a zero-income-tax state, get a real street address there (Traveling Mailbox makes this a 15-minute task from anywhere in the world), get the driver's license, register to vote, file your final part-year return, and cut the physical ties. Do it before you board the plane.

For the full picture on expat finances, see our US Expat Banking and Taxes Guide and our Expat Estate Planning Guide.

This content is for educational and informational purposes only and does not constitute legal, accounting, or tax advice. US state and federal tax law is complex and varies by individual circumstances. Consult a qualified CPA or tax attorney before making decisions about state domicile, tax residency, or international tax planning.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJuly 14, 2026

Expat Tax & FinanceJuly 14, 2026

Expat State Taxes: Which US States Won't Let You Go

Move abroad and California may still tax you 13.3%. Learn which five states chase expats, how domicile works, and how to sever state ties legally.

Expat Tax & FinanceJuly 4, 2026

Expat Tax & FinanceJuly 4, 2026

State Income Tax for Expats: Which States Follow You

California, New York, and Virginia keep taxing Americans abroad. Learn which states follow you, what triggers audits, and how to exit cleanly.

Expat Tax & FinanceJune 16, 2026

Expat Tax & FinanceJune 16, 2026

Expat State Income Tax: Which States Still Collect

Which US states still tax you while living abroad, how California's 546-day safe harbor works, and how to properly establish domicile elsewhere.