The 3 Bank Accounts Every US Expat Actually Needs

Most expats lose $1,200–$2,400/year to hidden bank fees. This three-account setup costs $180/year and fixes ATM access, business banking, and IRS compliance.

Stop paying $2,400/year in bank fees abroad. This 3-account expat banking setup—Schwab, Mercury, Traveling Mailbox—costs just $180/year.

Most US expats think they've solved their banking problem. They kept their Chase or Bank of America account, downloaded Venmo, and figured they'd sort the rest out once they landed. Two years later, they've paid between $1,200 and $2,400 in avoidable fees—ATM surcharges, foreign transaction markups, bad exchange rates, and wire fees that quietly eat $25–$50 per intermediary bank hop on every SWIFT transfer.

The fix isn't complicated. But it requires three accounts, not one—and one of them isn't a bank account at all.

Why Your US Bank Is Failing You Abroad

Traditional US banks were designed for people living in the US. When you leave, their infrastructure turns against you. Here's what's actually happening when you use a standard checking account overseas:

- Foreign transaction fees: Most major banks charge 1–3% on every purchase made in a foreign currency. On $2,000/month in expenses, that's $240–$720/year before you've paid a single wire fee.

- ATM surcharges: The foreign ATM operator charges you $3–$6. Your bank charges you another $3–$5. That's $6–$11 per withdrawal. Withdraw cash twice a week and you're looking at $624–$1,144/year—just in ATM fees.

- Dynamic currency conversion (DCC): Merchants abroad offer to charge you in dollars instead of the local currency. It sounds convenient. It usually adds 3–5% to the total on top of existing fees.

- SWIFT wire intermediary deductions: Every correspondent bank between your US account and a foreign recipient can legally deduct $25–$50 from the principal. Send $2,000 and the recipient might receive $1,900.

The total annual damage for an expat running a single US checking account for all overseas expenses: $1,200–$2,400 per year, conservatively. That's $6,000–$12,000 over five years—enough to fund several months of travel or a meaningful investment contribution.

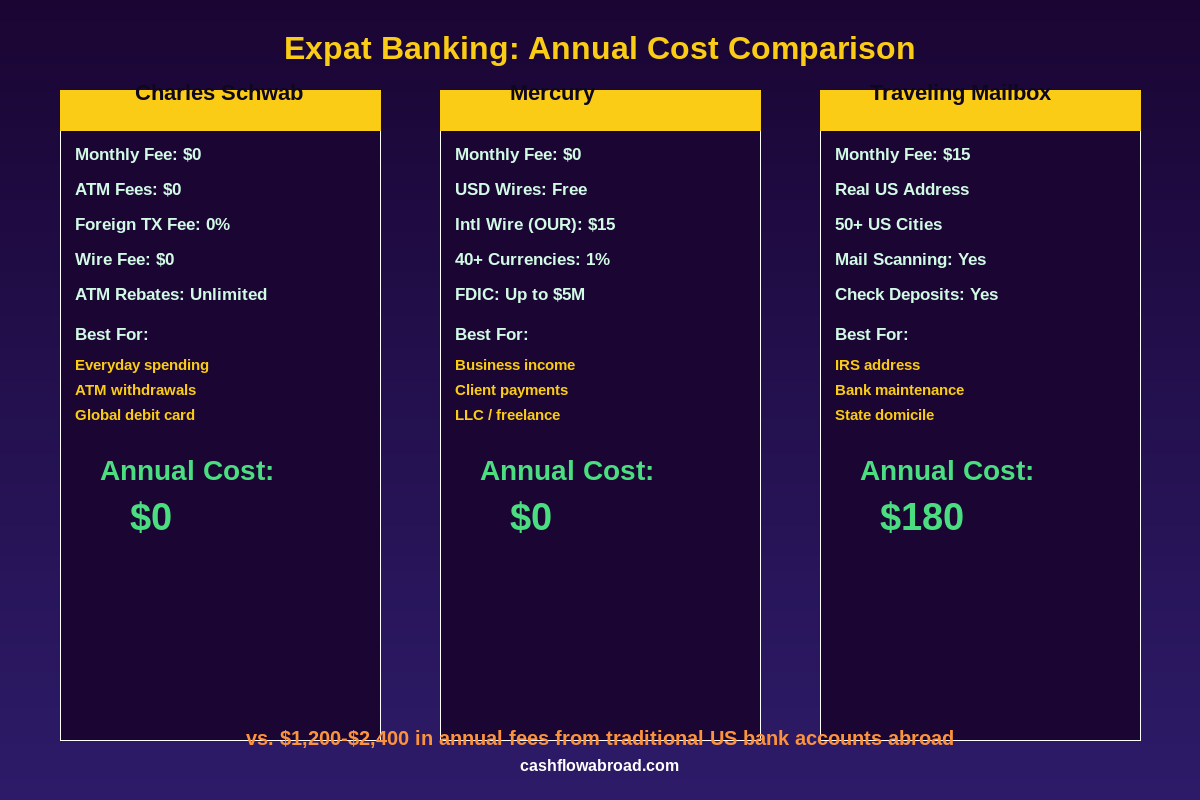

Account 1: Charles Schwab Investor Checking

This is the account the expat community has quietly rallied around for a decade. Charles Schwab's Investor Checking isn't marketed as an expat product, but it functions like one was custom-built for this use case.

The core feature: unlimited ATM fee rebates worldwide, with zero foreign transaction fees and zero monthly fee. Every ATM fee you pay—at any machine, in any country—is reimbursed at the end of your statement period. There's no cap. No tiered system. No minimum balance requirement.

| Feature | Schwab Investor Checking | Typical Major US Bank |

|---|---|---|

| Monthly Fee | $0 | $12–$25 |

| Foreign Transaction Fee | 0% | 1–3% |

| ATM Surcharge Rebates | Unlimited, worldwide | None (or in-network only) |

| International Wire Fee | $0 | $25–$45 |

| Daily ATM Limit | $1,000 | $300–$500 |

| FDIC Insured | Yes (up to $250K) | Yes |

The Investor Checking account comes bundled with a Schwab brokerage account, which is actually useful: you can hold index funds, ETFs, or a cash position in the same place. For expats building long-term wealth while living overseas, this doubles as a simple expat investing entry point.

One important caveat: If you're already living abroad when you apply, you need to apply through Schwab International rather than the standard domestic portal. It requires a passport and proof of foreign residence. If you're still in the US planning your move, apply before you leave—it's significantly easier.

Account 2: Mercury for Business and Freelance Income

Schwab handles your spending. Mercury handles your income.

If you run any kind of online business, freelance practice, or LLC as an expat, you need a US business banking account that isn't Chase or Bank of America. Those banks are increasingly suspicious of accounts tied to foreign IP addresses and foreign residence declarations—account freezes and sudden closures are common enough to be a recurring topic in every expat forum.

Mercury is built for remote operators. It's free, with no monthly fees, no account minimums, and no overdraft fees. The features that matter for expats:

- Free USD international wires: Send US dollars internationally at no charge through standard SHA processing. For the OUR option (where Mercury absorbs intermediary fees and the recipient gets the full amount), there's a flat $15 fee—far cheaper than the $25–$45 most banks charge before intermediary deductions.

- 40+ local currencies: Pay global vendors or contractors in their local currency for a transparent 1% exchange fee. No hidden spread.

- FDIC coverage up to $5 million: Mercury routes deposits through a sweep network of partner banks, extending FDIC protection well beyond the standard $250K limit.

- Built-in integrations: Native connections with Stripe, Shopify, Amazon, and QuickBooks make it functional for e-commerce operators and freelancers billing clients directly.

Mercury does have one notable limitation: a 3% international transaction fee on debit card purchases in foreign currencies. This is why it's not your primary spending account—that's what Schwab is for. Mercury is purely for receiving and routing business income.

Mercury accepts US LLC and corporation accounts. If you've structured your expat business correctly, you likely already have the entity. For the structure that works best, see our guide on running a US business while living abroad.

For moving money internationally—from clients into Mercury, or from Mercury out to local accounts abroad—Remitly is the most reliable option for personal transfers. It routes through local payment rails instead of SWIFT, meaning the full amount arrives without intermediary deductions eating into the principal.

The Account People Forget: Traveling Mailbox

This one isn't a bank account. It's the account that keeps your bank accounts alive.

Here's a problem nobody tells you before you move: US banks require a US address. Not a PO box—a real physical street address. When you move abroad and update your address to a foreign location, many banks quietly flag your account for review. Some close it outright. Others stop sending physical mail to foreign addresses—replacement debit cards, 2FA backup codes, IRS correspondence. Accounts have been frozen without explanation.

Traveling Mailbox gives you a real US street address in one of 50+ US cities for $15/month. Mail arrives there, gets scanned, and you view it online within hours. You can deposit checks digitally and forward physical mail when needed.

| What a Virtual Mailbox Solves | Why It Matters |

|---|---|

| IRS mailing address | Receive tax notices, refund checks, correspondence without international delays |

| Bank account address | Maintain Schwab and Mercury accounts without foreign-address flags |

| State domicile anchor | Choose a zero-income-tax state (TX, FL, WY, SD) to avoid state filing requirements |

| FBAR and FATCA forms | Accurate US address on FinCEN 114 and Form 8938 |

| Credit score maintenance | Receive card replacements and statements without interruption |

The state domicile point deserves emphasis. A California or New York address on your Schwab account means those states may treat you as a resident—even if you haven't been there in years. Use Traveling Mailbox to anchor a Florida or Texas address, and you eliminate state income tax liability entirely. At $180/year, it's the cheapest proactive tax planning most expats skip.

For a deeper look at FBAR and FATCA obligations once you hold foreign accounts, the complete FBAR/FATCA reporting guide has the full breakdown.

The Setup in Practice

Here's how the three-account stack works on a typical month:

- Client pays you via Stripe → funds land in Mercury (business checking)

- You transfer your "salary" from Mercury to Schwab via ACH (free, 1–2 business days)

- Day-to-day expenses in your country of residence → Schwab debit card, zero fees, ATM surcharges reimbursed monthly

- IRS correspondence, bank statements, card renewals → Traveling Mailbox address, viewed online within hours

- International transfers to local accounts → Remitly from Mercury or Schwab, local rails, no SWIFT intermediary fees

Total monthly cost of this setup: $15 (Traveling Mailbox). Everything else is free.

Compare that to the $100–$200/month the average expat burns through bank fees, wire charges, and exchange rate spreads without realizing it—because the costs are buried across multiple transaction records.

Common Mistakes Worth Avoiding

Keeping a traditional US bank as your primary account. Chase and Bank of America work fine domestically. Abroad, the 3% foreign transaction fee and per-ATM charges compound quickly. There's also a documented pattern of account closures tied to foreign IP addresses and foreign residence updates.

Using the wrong state address. An address in a state with income tax creates liability. If you're already anchored to a high-tax state address, updating to a Traveling Mailbox Texas or Florida address before your next tax filing can eliminate state filing requirements going forward.

Mixing business income with personal spending. Separate accounts keep bookkeeping clean, make tax prep straightforward, and prevent a payment processor hold from hitting the same account your local rent withdrawal comes from.

Sending regular transfers via SWIFT when local rail alternatives exist. For amounts under $10,000, Remitly and similar services route through local payment networks at a fraction of SWIFT cost. Reserve SWIFT for large, one-time transfers where per-transaction fees are negligible relative to the principal.

For how banking integrates with your full expat financial picture—FEIE, foreign tax credits, investment accounts—the US expat banking and taxes guide covers the complete framework.

One More Essential: Health Coverage

Banking solved. One more financial gap trips up most expats after their first year abroad: health insurance. Once you leave an employer plan, you need portable international coverage. SafetyWing's Nomad Insurance starts at $56.28/month for travelers under 40 and covers emergency medical, evacuation, and travel disruptions across 185 countries. It's not a substitute for comprehensive long-term coverage, but for most expats early in their move, it handles the acute risks at a manageable cost. See the full breakdown in our expat health insurance guide.

The Bottom Line

The expat banking problem isn't about finding the perfect single account—it's about building a minimal stack that handles each use case correctly. Schwab for spending and ATM access. Mercury for business income and USD wires. Traveling Mailbox for maintaining the US address that keeps everything else functional.

Total cost: $180/year. Potential savings over a traditional US bank setup: $1,200–$2,400 annually.

Open the Schwab account first. It takes 15 minutes and is easiest done before you leave the US. Set up Mercury when your business entity is registered. Get the Traveling Mailbox address before you update your information anywhere official—IRS records, bank accounts, state driver's license.

The expats who get this right aren't doing anything exotic. They just stopped letting their bank make passive income off their relocation.

This post is for informational purposes only and does not constitute financial, legal, or tax advice. Banking products, fees, and availability change—verify details directly with each provider. Some links in this post are affiliate links; we may earn a commission at no additional cost to you. Consult a qualified financial advisor or expat tax professional for advice specific to your situation.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 29, 2026

Expat Tax & FinanceMay 29, 2026

Your US Credit Score Is Dying Abroad — Stop It Now

FICO scores go dormant in 6 months of inactivity. Learn the exact system to keep your US credit score alive while living abroad as an expat.

Expat Tax & FinanceMay 23, 2026

Expat Tax & FinanceMay 23, 2026

Virtual Mailbox for Expats: Keep Your US Banking Alive

How a $15/month virtual mailbox keeps expat bank accounts open, IRS mail received, and brokerages intact. Best states and step-by-step setup.

Expat Tax & FinanceMay 8, 2026

Expat Tax & FinanceMay 8, 2026

Why Foreign Banks Refuse American Expats (And What to Do)

FATCA costs banks $16,600 per American account. Learn why foreign banks refuse US expats and which banking solutions actually work abroad.