Roth IRA for Expats: Why FEIE Kills Your Contributions

9 min read · 2,244 words

Every year, thousands of US expats do something perfectly legal that accidentally costs them their retirement future: they claim the Foreign Earned Income Exclusion, pat themselves on the back for saving tens of thousands in taxes — and then quietly become ineligible to contribute a single dollar to their Roth IRA. The IRS doesn’t send a warning letter. Your brokerage won’t flag it. You’ll find out at tax time, staring at a 6% penalty on every dollar you contributed.

The FEIE and the Roth IRA are two of the most powerful tools available to Americans abroad. The cruel joke is that using one aggressively can completely shut off the other.

How the FEIE Eliminates Your Roth IRA Eligibility

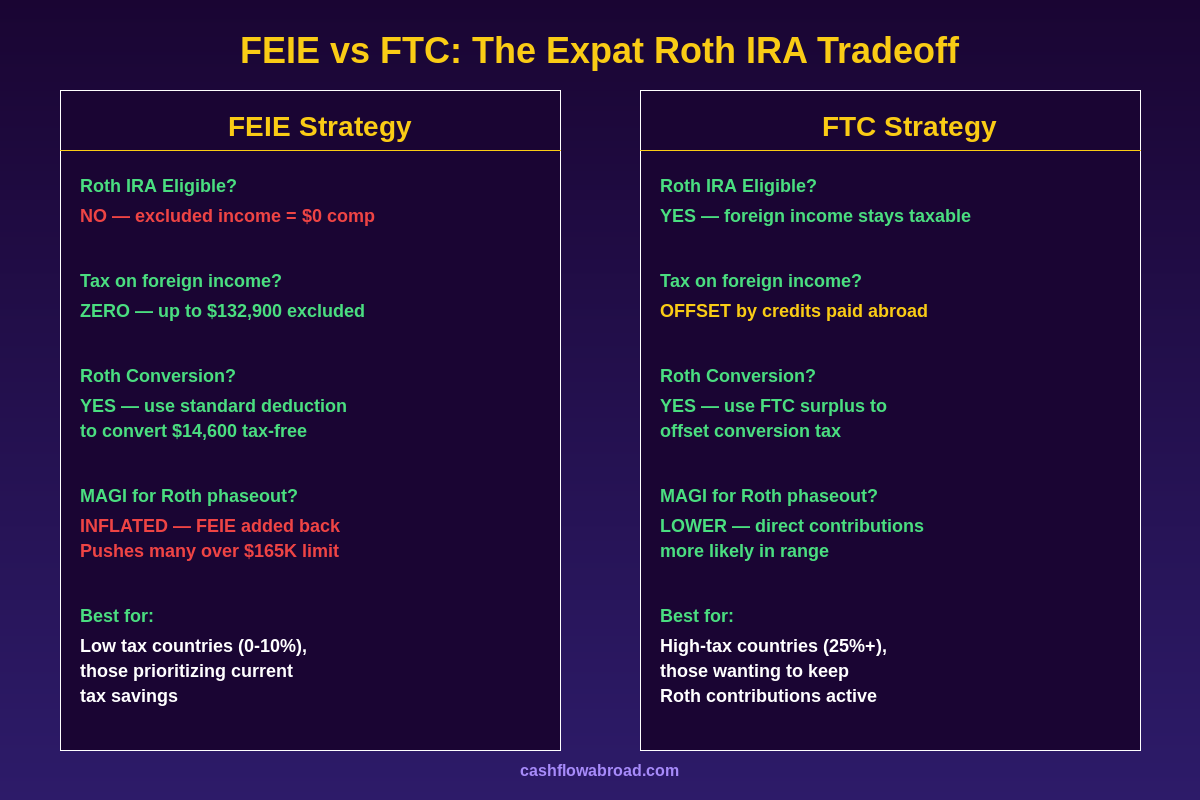

The mechanics are straightforward once you see them. To contribute to a Roth IRA, the IRS requires you to have taxable earned income — wages, salary, self-employment income. The contribution limit for 2025 is $7,000 ($8,000 if you’re 50 or older), but you can only contribute up to the amount of your taxable earned compensation.

Here’s where expats get blindsided: the FEIE lets you exclude up to $130,000 of foreign earned income from US taxation in 2025 (rising to $132,900 in 2026). That excluded income doesn’t count as taxable compensation for IRA purposes. So if you earn $80,000 abroad and exclude every dollar under the FEIE, the IRS treats your taxable earned income as exactly zero. Zero earned income means zero Roth IRA contribution allowed — full stop.

Most expats earning under $130,000 who max out the FEIE are silently locked out of their Roth IRA and don’t know it.

The MAGI Double Trap Nobody Warns You About

Even if you have income above the FEIE ceiling and technically have taxable compensation, there’s a second trap waiting: the Modified Adjusted Gross Income (MAGI) test for Roth eligibility.

For 2025, the Roth IRA phaseout starts at $150,000 for single filers and cuts off completely at $165,000. For married filing jointly, the phaseout runs from $236,000 to $246,000.

Here’s the catch: when the IRS calculates your MAGI for Roth purposes, it adds back any income excluded under the FEIE and foreign housing exclusion. So an expat who earns $140,000 in Singapore, excludes $130,000 under the FEIE, and has $30,000 in investment income ends up with a MAGI of $170,000 — above the Roth phaseout limit — even though their taxable income is only $40,000.

The FEIE makes you look poor to the US tax system in most respects. For the Roth IRA income limit, it makes you look rich.

The FTC Fix: Keeping Your Roth IRA Alive Abroad

The Foreign Tax Credit (FTC) is the FEIE’s less glamorous sibling, and for expats in moderate-to-high tax countries, it’s often the smarter long-term play — precisely because it preserves Roth IRA eligibility.

Under the FTC, you don’t exclude your foreign income from US taxation. Instead, you claim a credit for taxes paid to your host country, which offsets your US tax bill dollar-for-dollar. Your foreign earned income remains taxable earned income in the eyes of the IRS, which means it counts toward your IRA contribution base.

The math works well if you’re living in a country with a comparable or higher tax rate than the US. A freelancer paying 30% income tax in Germany can use those credits to zero out or nearly zero out their US tax liability — while still maintaining $7,000/year in Roth IRA contribution eligibility.

The tradeoff: if you’re in a zero-tax or very low-tax country (UAE, Cayman Islands, Paraguay, Georgia), the FEIE is almost always superior for current-year tax savings. You just need to accept the Roth lockout and compensate with other strategies covered below.

| Scenario | Income | Host Tax Rate | Best Strategy | Roth IRA Access |

|---|---|---|---|---|

| Dubai freelancer | $95,000 | 0% | FEIE — saves ~$16K US tax | Locked out; use conversion strategy |

| Germany employee | $110,000 | 42% | FTC — credits offset US tax fully | Eligible for direct contributions |

| Colombia remote worker | $75,000 | 19% | Model both; often FEIE wins | FEIE: locked; FTC: small US tax, eligible |

| Singapore exec | $180,000 | 22% | FTC reduces MAGI vs FEIE | FTC: MAGI lower, Roth likely in range |

One critical warning: switching from FEIE to FTC triggers a five-year restriction. Once you revoke the FEIE election, you cannot claim it again for five years. This is not a decision to make lightly or reverse mid-plan. Model the full five-year trajectory before switching.

The Partial FEIE Trick Most Expats Overlook

You don’t have to choose between full FEIE exclusion or full FTC. One underused strategy: claim only a partial FEIE — enough to reduce your US tax bill significantly, while intentionally leaving at least $7,000 in taxable earned income to preserve Roth IRA eligibility.

If you earn $100,000 abroad, you could exclude $93,000 under the FEIE and leave $7,000 taxable. You’d owe some US income tax on that $7,000 — but the standard deduction ($14,600 for single filers in 2025) often covers it entirely, meaning your actual US tax bill on the retained income is zero. Meanwhile, you’ve preserved your right to contribute $7,000 to a Roth IRA.

Over 20 years of expat life, $7,000/year in Roth contributions compounding at 8% grows to approximately $357,000 in tax-free retirement wealth. The value of maintaining that eligibility with a partial exclusion strategy frequently exceeds the modest tax cost of doing so.

The Roth Conversion Window Only Expats Get

Here’s a strategy that actually works better when you’re abroad and using the FEIE: converting traditional IRA or 401(k) money to a Roth IRA during your expat years.

The FEIE cannot be used to exclude Roth conversion income — conversions are not earned income. But if your FEIE excludes all your regular earnings, your US taxable income drops close to zero, which means your marginal tax rate on a Roth conversion is also very low.

An expat in a zero-tax country who earns $90,000 and excludes it all under the FEIE has effectively $0 in US taxable income. They can then convert up to $14,600 from a traditional IRA to a Roth IRA — shielded entirely by the standard deduction — completely tax-free. Convert $14,600/year for 10 years while abroad and you’ve moved $146,000 into a Roth IRA without paying a dollar in US income tax on those funds.

For expats with significant pre-tax retirement balances — 401(k)s from years of US employment, SEP-IRAs, rollover IRAs — this is one of the most powerful tax windows they’ll ever encounter. The combination of a low earned income year (FEIE cleared the runway) plus the standard deduction creates a zero-tax conversion corridor that closes entirely once you return to a US salary.

The 6% Penalty Trap: What Happens If You Contribute When You Shouldn’t

Let’s say you’re an expat, you claimed the FEIE, and through your own miscalculation or bad advice, you contributed $7,000 to your Roth IRA for the year anyway. What happens?

The IRS charges a 6% excise tax per year on any excess contribution — every year the money stays in the account. On $7,000, that’s $420/year. If you contributed incorrectly for three years before catching it, you’re looking at $1,260 in penalties plus potentially amended returns for each year.

To fix it, you have a few options:

- Timely withdrawal: Remove the excess plus any earnings before the tax filing deadline (including extensions). This eliminates the penalty. Earnings you withdraw are taxable income in the withdrawal year.

- Recharacterization: Convert the Roth contribution to a traditional IRA contribution before the deadline. Doesn’t help if you’re also ineligible for traditional contributions (same earned income requirement applies).

- Apply to future year: If you become eligible next year, the excess can count toward next year’s limit — but you still owe the 6% penalty for the year the excess was made.

The cleanest move is staying ahead of this. If you’re claiming the full FEIE on all your earned income, don’t contribute to a Roth that year. Period. Run the calculation first — determine exactly how much taxable earned income you’ll have after any exclusions — before making any IRA contributions.

Does the Backdoor Roth Work for Expats?

The backdoor Roth — contributing to a traditional IRA and converting immediately to Roth — is the standard workaround for high earners over the MAGI limits. For expats, it works in theory but hits the same FEIE wall.

The backdoor still requires taxable earned compensation for the initial traditional IRA contribution. If the FEIE has zeroed out your earned income, you cannot make the first step, and the backdoor is unavailable. Same problem, different door.

The pro-rata rule creates a separate headache if you do have taxable income. If you hold any pre-tax money in traditional, SEP, or SIMPLE IRAs — common for expats who rolled over old 401(k)s — the IRS treats every conversion as proportionally drawn from pre-tax funds, triggering ordinary income tax on that portion. The backdoor only runs cleanly if your total pre-tax IRA balance is zero.

Expats considering the backdoor Roth should calculate their entire pre-tax IRA balance across all accounts. Rolling that balance into a current employer’s 401(k) before executing the backdoor can clear the pro-rata complication — if your plan allows incoming rollovers. Worth checking with your plan administrator before assuming it’s available.

What Your Host Country Thinks of Your Roth IRA

The US taxes citizens on worldwide income, but it doesn’t control how your host country taxes your assets. Not every country recognizes the tax-exempt status of a US Roth IRA, and this blind spot catches expats off guard.

In most countries without a specific US tax treaty provision covering Roth IRAs, the account may be treated as ordinary investment income subject to local taxation. Annual growth, distributions, or even just holding the account could trigger local tax reporting and liability — eliminating the tax-free benefit that makes Roth accounts worth building.

The United Kingdom has a treaty provision that specifically addresses Roth IRAs and generally respects their tax-exempt treatment for US persons living in the UK. Most other countries do not. France, Australia, Canada, and most of the EU each treat US retirement accounts differently. Before assuming your Roth is untouchable everywhere you live, get explicit guidance from a tax advisor in your host country — not just your US-side CPA.

Don’t Let PFICs Ruin Your IRA

Whether you’re contributing to a Roth or a traditional IRA as an expat, one trap applies regardless: Passive Foreign Investment Companies (PFICs). If you hold foreign mutual funds, ETFs, or investment funds registered outside the United States inside your IRA, those may be classified as PFICs — and the US tax treatment is punishing.

PFIC income is taxed at maximum ordinary income rates plus interest charges on deferred gains, and each PFIC requires annual reporting on Form 8621. The practical rule: hold only US-domiciled funds (Vanguard, Fidelity, iShares US-registered ETFs) inside your IRA. Keep any foreign-registered investment funds in separate taxable accounts where proper PFIC elections can be made, or avoid them entirely. Our expat investing playbook covers the full PFIC minefield.

Which Strategy Is Right for You?

| Your Situation | Recommended Approach |

|---|---|

| Zero-tax country, income under $130K | Full FEIE + annual Roth conversion using standard deduction corridor |

| Zero-tax country, income over $130K | FEIE for $130K + partial taxable income retained → direct Roth contribution |

| High-tax country (25%+) | FTC strategy — credits offset US tax, preserves Roth eligibility |

| Medium-tax country (15–25%) | Model both; often FEIE + Roth conversion beats FTC + contributions on net |

| Large pre-tax IRA/401(k) balance | Prioritize Roth conversions during low-income expat years |

| Planning to return to US within 5 years | Max conversions now at low expat rates; resume direct contributions post-return |

For anyone running these numbers, Charles Schwab’s International Account is widely regarded as the best brokerage for US expats — it won’t close your account when you give a foreign address, has no foreign transaction fees, reimburses all ATM fees worldwide, and handles IRA contributions and Roth conversions cleanly. It’s where your IRA should live if you’re moving abroad.

To maintain a US mailing address for your IRA custodian, brokerage, or IRS correspondence while you’re overseas, a Traveling Mailbox gives you a real US street address in 50+ cities, mail scanning on demand, and check deposits for around $15/month. Keeping a consistent US address is often what keeps brokerage accounts open and IRS notifications from going to a black hole. We covered this more fully in our virtual mailbox guide for expats.

For the complete picture of how FEIE, FTC, and retirement accounts interact inside the full US expat tax filing structure, the expat banking and tax guide is the right next read. And if you’re comparing whether the FEIE or FTC is better for your specific income level and host country, the FEIE deep-dive walks through the decision framework in detail.

The Bottom Line

The FEIE is a legitimate, powerful tool for reducing your US tax bill abroad. Treating it as a default setting without examining its downstream effects on your Roth IRA is a quiet, compounding mistake. The damage doesn’t show up immediately — it shows up 20 years later when you realize the tax-free retirement account you thought you were building was never actually growing.

The good news: there are real strategies to work around it. Partial FEIE elections, FTC switching for high-tax-country expats, Roth conversion windows during low-income years — each of these can recover what an aggressive FEIE strategy takes away. But they require intentional planning, not autopilot.

Run the numbers before you file. The expat years are often the best Roth conversion window you’ll ever have — if you use them right.

Disclaimer: This article is for educational purposes only and does not constitute tax or financial advice. US expatriate tax law is complex and fact-specific. The FEIE exclusion amount, MAGI thresholds, and contribution limits cited reflect 2025 and 2026 tax years and are subject to IRS adjustments. Consult a qualified CPA or tax attorney who specializes in US expatriate taxation before making decisions about your FEIE elections, Roth IRA contributions, or retirement account conversions.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.