The 183-Day Rule: Why Most Digital Nomads Get It Wrong

10 min read · 2,435 words

Most digital nomads treat 183 days as a shield. Stay under that number in any given country and you’re safe from its tax authorities — that’s the received wisdom on every nomad Facebook group, every remote-work forum, and half the “tax planning” content on YouTube. It’s also dangerously wrong.

The 183-day threshold isn’t a safe harbor. In most countries, it’s the minimum threshold for one pathway to tax residency. Cross it and you’re almost certainly a tax resident. But here’s what most nomads never bother to find out: you can become a tax resident of a country you spent 90 days in. You can become a tax resident of a country where you have a lease, even if you barely visited. And as a US citizen, the 183-day rule is essentially irrelevant to your federal tax obligations — the IRS doesn’t care where you live.

Understanding how this rule actually works — and how dramatically it varies by country — is the difference between a clean tax situation and an unexpected five-figure bill.

What the 183-Day Rule Actually Is

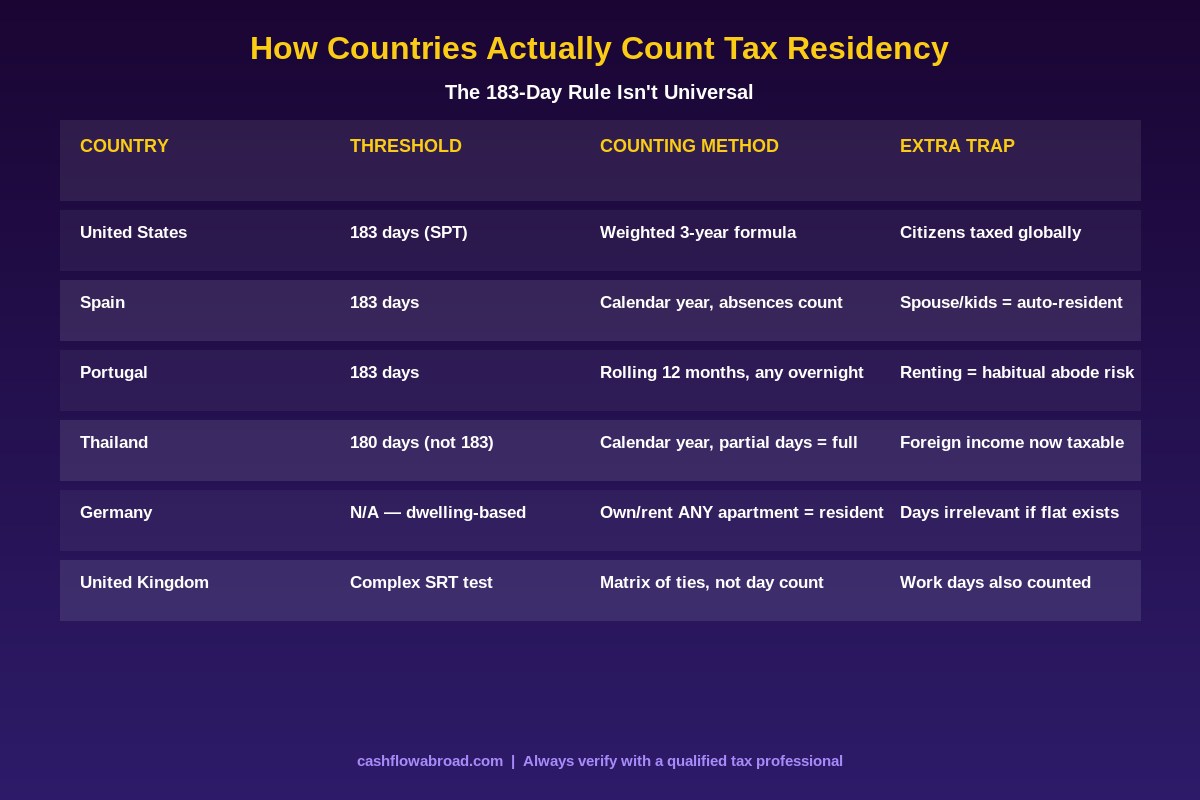

The 183-day figure traces back to the OECD Model Tax Convention, which most countries use as the foundation for their bilateral tax treaties. The convention created a simple tiebreaker: when two countries both claim you as a tax resident, the one where you spend 183+ days during the tax year generally gets primary taxing rights over employment income.

Countries adopted this threshold into domestic law and it spread as a rule of thumb. But each country modified it. Some use calendar years, some use rolling 12-month windows. Some count partial days as full days. Some count arrival and departure separately. Some have additional criteria that can trigger residency with zero days spent. The “183-day rule” is now a family of loosely related rules with a shared origin, not a single standard.

The one thing most of these rules have in common: 183 days is a trigger, not a limit. Spending 182 days in a country doesn’t protect you if that country has a “habitual abode” clause, a “center of vital interests” test, or simply defines residency differently from what you assumed.

How the US Is Completely Different — and Why It Matters

If you’re a US citizen or green card holder, the 183-day rule is largely irrelevant to your IRS obligations. The United States taxes based on citizenship and long-term residency status, not on where you physically live. You owe federal income tax regardless of which country you’re in or how long you’ve been gone.

What US expats actually need to track is the 330-day Physical Presence Test — one of two ways to qualify for the Foreign Earned Income Exclusion (FEIE). To exclude up to $132,900 of foreign-earned income from US federal tax in 2026, you need to spend 330 full days outside the US during any 12-month period that overlaps the tax year. The IRS counts only full 24-hour periods spent entirely in foreign countries. Arrival days and departure days don’t count.

That’s a much higher bar than 183 days — and the counting methodology is stricter. Many nomads who confidently believe they’ve passed the physical presence test have actually missed it because they undercount departures and arrivals.

The alternative is the Bona Fide Residence Test, which requires establishing genuine residence in a foreign country for an uninterrupted period including a full calendar year. This is harder to qualify for but doesn’t require day-counting.

For a full breakdown of how FEIE interacts with the Foreign Tax Credit, see our guide on paying zero federal tax as a US expat.

Country-by-Country: Where the Rule Gets Dangerous

Spain: The Family Trap

Spain uses a calendar year and the standard 183-day threshold — but with two extensions that catch nomads off guard.

First, temporary absences count toward the 183 days unless you can prove tax residency in another country. A month in Morocco doesn’t interrupt your Spain count if you don’t have a tax residency certificate from Morocco.

Second — and this one is brutal — if your spouse and dependent children live permanently in Spain, Spanish tax authorities will presume you’re a resident regardless of how many days you personally spent there. The burden is on you to prove otherwise. Several US expats have discovered this the hard way after their partners settled in Madrid while they traveled freely, assuming the 183-day clock was their only concern.

Spain also applies a “center of economic activities” test. If the majority of your income comes from Spanish sources or most of your assets are held in Spain, authorities can argue tax residency without the day count.

Portugal: The Rolling Window Problem

Portugal doesn’t use a fixed calendar year. It counts presence over any rolling 12-month period. If you spent 100 days in Portugal in the last four months of one year and 90 days in the first two months of the next, you may have crossed 183 days within a single rolling window without realizing it — while believing you were comfortably under the threshold for both calendar years.

Portugal also defines a “day” broadly: any day involving an overnight stay counts, including partial days. And there’s a “habitual abode” clause — if you maintain a place of residence in Portugal on December 31 that is “intended to be occupied and maintained as a habitual residence,” you can trigger tax residency even without the day count. Renting an apartment in Lisbon while spending most of your time elsewhere is not the clean workaround it sounds like.

Thailand: It’s Not Even 183 Days

Thailand uses a 180-day threshold — not 183. That’s a small but meaningful difference if you’re doing careful planning. And any part of a day spent in Thailand counts as a full day. Arrive at 11pm? That’s a full day counted.

Thailand also overhauled its foreign income tax rules in 2024. Previously, foreign-source income was only taxable if remitted to Thailand in the same calendar year it was earned — a loophole that effectively made Thailand a tax haven for nomads who kept earnings offshore for a year before bringing them in. Under the current rules, all foreign income remitted to Thailand by tax residents is taxable, regardless of when it was earned. This makes the 180-day count far more consequential than it was two years ago.

Germany: Forget the Day Count Entirely

Germany is the starkest example of why the 183-day rule gives nomads false confidence. Germany determines tax residency based on dwelling, not days. If you maintain a home in Germany that is available for your use — renting it, owning it, even subletting it to someone while retaining the option to return — Germany may consider you a tax resident for the entire year, regardless of how many days you actually spent there.

German tax authorities use two concepts: the “residence” (Wohnsitz) and the “habitual abode” (gewöhnlicher Aufenthalt). Either triggers worldwide tax liability. You could spend 60 days in Germany while working remotely from Southeast Asia for the remaining ten months, and if you maintained an apartment in Berlin the whole time, Germany may claim you as a full-year tax resident.

UK: The Most Complex System in Europe

The United Kingdom scrapped its simple version of the 183-day rule and replaced it with the Statutory Residence Test (SRT) — a multi-factor matrix that considers:

- Days spent in the UK (with different thresholds depending on your level of “UK ties”)

- Whether you have UK accommodation available, even if you don’t own it

- Whether you work in the UK — even 3 hours in a day qualifies as a “UK work day”

- Whether family members are resident in the UK

Under the SRT, someone with many UK ties might become a tax resident after just 46 days. Someone with no UK ties at all might safely spend up to 182 days without triggering residency. The threshold is deliberately variable — the UK designed a system that can’t be gamed purely by counting days.

The Dual Residency Trap: When Two Countries Bill You Simultaneously

The scenario that does the most financial damage: you become a tax resident of two countries at once. Both claim your worldwide income. Both send bills.

Tax treaties contain tie-breaker rules to resolve this conflict, working down a hierarchy:

- Where is your permanent home?

- Where is your center of vital interests — strongest economic and personal ties?

- Where do you have a habitual abode?

- What is your nationality?

- If still unresolved, mutual agreement between the tax authorities of both countries

But treaties only exist between specific country pairs. The US has tax treaties with roughly 65 countries. If you’re a dual tax resident of two countries that don’t have a treaty — Thailand and Brazil, for instance, or Georgia and Mexico — there’s no automatic resolution. You’re potentially liable to both, and the only relief is foreign tax credits, which may not fully offset the exposure.

For US citizens specifically, the treaty tie-breaker may not help at all. Most US tax treaties contain a “savings clause” that allows the US to ignore the tie-breaker and continue taxing its citizens regardless of treaty provisions. The FEIE exists precisely because the treaty system doesn’t reliably protect Americans from double taxation.

The US Has Its Own Trap: The Substantial Presence Test

Here’s a twist most non-American nomads miss: the US applies its own version of the 183-day rule to foreign nationals. The Substantial Presence Test (SPT) determines whether non-citizens must file US taxes as residents.

The SPT uses a weighted 3-year formula. Days in the current year count at full value; days in the prior year count at 1/3; days from two years ago count at 1/6. If the weighted total reaches 183, you’re a US tax resident for that year.

| Year | Days in US | Multiplier | Weighted Count |

|---|---|---|---|

| Current year | 120 | ×1 | 120 |

| Prior year | 120 | ×1/3 | 40 |

| Two years ago | 120 | ×1/6 | 20 |

| Total | 180 (just under) |

A foreign national who regularly visits the US for 4 months per year can be just one extra week in the US away from triggering residency — and the US tax system along with it. Most people in this situation have no idea the SPT exists.

How to Actually Structure This Properly

The goal isn’t to game the day count. It’s to establish clear, defensible tax residency in one jurisdiction, maintain documentation, and ensure you’re not accidentally resident somewhere you didn’t intend.

Establish Formal Residency Somewhere

Nomads who have legal residency nowhere are increasingly in a gray zone as tax authorities share data globally under the OECD Common Reporting Standard and the newer CARF framework for crypto and digital assets. Having actual legal tax residency — with a tax residency certificate to prove it — is the cleanest defense against multiple countries making claims on your income.

Low-tax options with clear residency paths include Paraguay ($3,500–5,000 total cost, 0% tax on foreign income), Georgia (1% flat rate on foreign income, setup in under a month), and Panama (territorial tax system, Friendly Nations Visa for under $5,000). See our geographic arbitrage playbook for a full comparison.

Track Your Days Rigorously

This sounds tedious but is non-negotiable. Use passport stamps, boarding passes, and credit card transaction records to build a complete picture. Reconstruct two years of travel from memory under a Portuguese audit and you’ll understand why documentation matters.

A good eSIM service like Saily generates data logs by country that can serve as secondary evidence of your travel timeline — a useful supplement to passport stamps, particularly in countries that have moved to digital border crossings with minimal paper trail.

Maintain a US Address for IRS and Banking Purposes

US expats still need a permanent US address for IRS correspondence, brokerage accounts, and — critically — demonstrating they’ve severed domicile with a high-tax state. A virtual mailbox gives you a real street address without the fiction of pretending you live somewhere you don’t.

Traveling Mailbox provides a real US street address in 50+ cities, scans mail digitally, and handles check deposits for about $15/month. It’s the most practical solution for managing IRS correspondence, banking verification letters, and state tax authority communications from abroad. The site owner uses it personally.

Keep Your Banking Clean

For US expats managing money across multiple countries, Charles Schwab International remains the gold standard — no foreign transaction fees, free ATM withdrawals worldwide, and no account closures for living abroad. Pair it with Mercury for a US business checking account if you’re running any kind of online operation.

The full rundown on expat banking — including which institutions don’t close your accounts — is in our US expat banking guide.

FBAR Still Applies Regardless of Where You Live

Even after successfully establishing foreign tax residency and eliminating most of your US income tax liability through FEIE, one obligation follows US citizens everywhere: FBAR reporting.

If the aggregate value of your foreign financial accounts exceeds $10,000 at any point during the year, you must file FinCEN Form 114. The penalties aren’t theoretical:

| Violation Type | Maximum Penalty (2026) | Notes |

|---|---|---|

| Non-willful FBAR | $16,536 per annual report | Per-report after 2023 Bittner ruling |

| Willful FBAR | $165,353 or 50% of balance | Whichever is greater |

| Criminal FBAR | $250,000 + up to 5 years prison | Aggravated cases: $500K + 10 years |

| Streamlined Filing | $0 penalty if accepted | Must file before IRS initiates contact |

Nomads who discover years of non-compliance can often use the IRS Streamlined Filing Compliance Procedures to come clean without penalties — but only if they act before the IRS contacts them first. Once the IRS initiates contact, that door closes.

Our complete expat tax and FBAR guide walks through exactly what to file, when, and what the thresholds are for each form.

The Bottom Line

The 183-day rule is the beginning of the conversation, not the end of it. The countries where most digital nomads spend meaningful time — Spain, Portugal, Thailand, Germany, the UK — all have their own variations, and some have replaced the day count with entirely different frameworks. Germany doesn’t care how many days you spent there. Portugal counts rolling windows, not calendar years. Thailand uses 180 days. Spain can claim you based on where your family lives.

For US citizens, the parallel challenge is the 330-day physical presence test for FEIE, plus perpetual FBAR compliance regardless of which country you call home. For everyone else, the risk is becoming a dual tax resident in countries with no treaty framework to resolve it.

The clean solution isn’t more careful day-counting. It’s deliberate residency planning: choose a jurisdiction, establish it formally, document everything, and understand the full range of rules that apply to your specific situation — not just the one number that gets repeated everywhere.

For practical next steps, our digital nomad visa ranking covers which programs come with the clearest tax frameworks alongside their entry requirements.

Financial disclaimer: This post is for informational purposes only and does not constitute tax or legal advice. Tax laws vary by country and individual circumstances change frequently. Always consult a qualified international tax professional before making decisions about tax residency, FBAR filings, or any cross-border financial arrangements.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.