The $75K Tax Break US Expats Leave on the Table

Most US expats claim the FEIE and stop — missing a second IRS shelter that can shield up to $93K more in cities like Hong Kong or Singapore.

Most US expats claim the FEIE and stop — missing a second IRS shelter that can shield up to $93K more in cities like Hong Kong or Singapore.

Most US expats file Form 2555 every year and pat themselves on the back for claiming the Foreign Earned Income Exclusion. What they don't realize: they left half their tax break on the table. The IRS quietly offers a second shelter on the same form — the Foreign Housing Exclusion — and in cities like Hong Kong or Singapore, it can shield an additional $75,000 to $93,000 of income from US taxation. Per year. On top of the FEIE.

The reason most expats miss it isn't complicated. Tax software buries the questions. CPAs who don't specialize in expats often skip it. And the IRS certainly isn't running ads. If you're paying rent abroad and your annual housing costs exceed roughly $20,800, you are leaving money with the US Treasury that the tax code says you don't owe.

What the Foreign Housing Exclusion Actually Is

The Foreign Housing Exclusion (FHE) lives in IRC Section 911, the same code section as the FEIE. It's claimed on the same form — Form 2555. It does not require a separate election or a different filing. And yet, surveys of expat tax professionals consistently find it is claimed far less frequently than the FEIE, even among filers who qualify for both.

The concept is straightforward: the IRS acknowledges that Americans living abroad often pay significantly more for housing than they would in the US. The excess — the amount above what the IRS estimates you'd pay domestically — can be excluded from federal taxable income.

Employees claim a Foreign Housing Exclusion (Part VIII of Form 2555). Self-employed individuals claim a Foreign Housing Deduction (Part IX) — same math, slightly different tax impact. Both reduce your ordinary income tax bill. The self-employed version has zero effect on self-employment tax, which matters enormously if you freelance.

How the Calculation Works (With Real Numbers)

The IRS uses a two-layer formula:

- Your qualifying housing expenses — what you actually paid for rent, utilities, insurance, etc.

- The base housing amount — the IRS assumes you would have spent this much on housing even if you stayed in the US, so it's subtracted from your expenses before any exclusion applies.

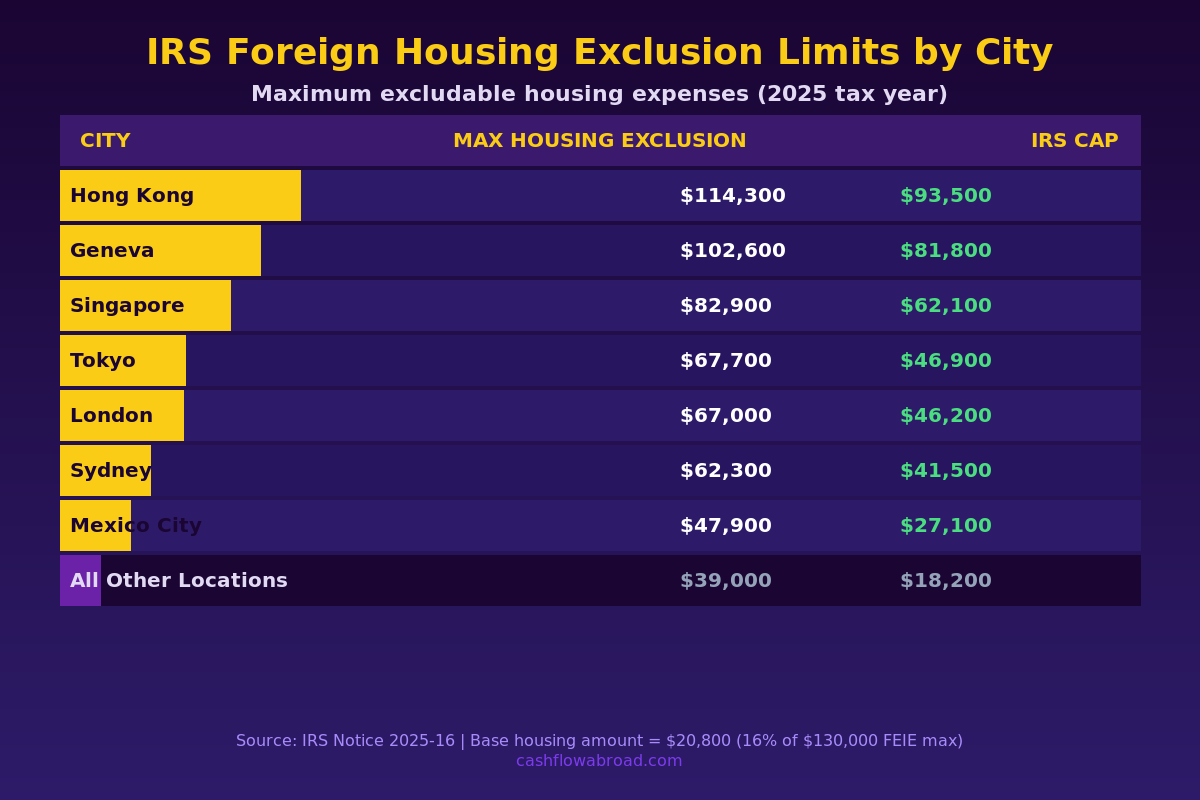

- A location-specific cap — the maximum qualifying expenses the IRS will recognize. For most cities, that's 30% of the FEIE. For high-cost cities, it's far higher.

The formula: Exclusion = MIN(Actual Expenses, Location Cap) − Base Housing Amount

| Year | FEIE Max | Base Amount (16% of FEIE) | Standard Cap (30% of FEIE) | Max Exclusion (Standard) |

|---|---|---|---|---|

| 2023 | $120,000 | $19,200 | $36,000 | $16,800 |

| 2024 | $126,500 | $20,240 | $37,950 | $17,710 |

| 2025 | $130,000 | $20,800 | $39,000 | $18,200 |

That standard cap matters mostly for expats in lower-cost countries. If you're renting a modest place in Medellín or Chiang Mai, the housing exclusion might shelter $10,000–$15,000 of income — real savings, but not dramatic. The numbers become jaw-dropping when you're in a high-cost IRS-listed city.

Where the Housing Exclusion Goes Astronomical

Every year the IRS publishes a notice (Notice 2025-16 for the 2025 tax year) with city-specific caps that blow past the standard 30% ceiling. The theory is that housing costs in places like Hong Kong or Geneva are so far above typical US housing that a higher exclusion is warranted.

What this means in practice: an employee in Hong Kong paying $96,000/year in rent (about $8,000/month — not unusual for a 2-bedroom in Mid-Levels) can exclude $75,200 of income via the housing exclusion alone ($96,000 − $20,800 base), on top of the $130,000 FEIE. That's $205,200 in combined exclusions before US tax is owed on a single dollar.

Three Real Scenarios, Dollar-for-Dollar

| Scenario | City | Income | Annual Rent | Housing Exclusion | Combined Exclusions | US Taxable Income |

|---|---|---|---|---|---|---|

| Employee A | London | $175,000 | $48,000 | $27,200 | $157,200 | $17,800 |

| Employee B | Singapore | $220,000 | $72,000 | $51,200 | $181,200 | $38,800 |

| Employee C | Hong Kong | $280,000 | $96,000 | $75,200 | $205,200 | $74,800 |

In the Singapore scenario, Employee B without the housing exclusion would have $90,000 in taxable US income (after FEIE only) — paying roughly $15,000+ in US federal tax. With the housing exclusion, that bill drops dramatically. The housing exclusion alone saves over $11,000 at the 22% marginal rate. That's not a rounding error — that's a car payment, a year of health insurance, or a long-haul flight home.

Expats moving to high-cost financial centers need to run these numbers carefully before assuming their FEIE alone covers everything. See our US expat banking and tax guide for a broader picture of the filing obligations involved.

What Counts as a Qualifying Housing Expense

The IRS allows a specific list. Getting creative outside it is an audit risk.

Allowable: rent, utilities (gas, electricity, water — not telephone or internet), renter's insurance, residential parking, furniture rental, household repairs, a second home if your family can't safely live with you in a dangerous location.

Not allowable — and commonly over-claimed: mortgage interest (still deductible on Schedule A, just not here), furniture purchases, any cost of buying property, housekeepers, gardeners, cable/satellite, internet, and anything the IRS considers "lavish or extravagant." Employer-provided housing that isn't included in your W-2 as income also doesn't count — you can't exclude what was never income in the first place.

Keep every receipt, every bank statement showing rent paid, every utility bill. If you're audited on Form 2555, housing expense documentation is the first thing the IRS requests.

The Self-Employment Trap Most Freelancers Don't See Coming

This is where the Foreign Housing Exclusion becomes genuinely tricky for digital nomads and freelancers.

Employees get the exclusion — it reduces taxable income dollar for dollar, cutting their income tax bill. Self-employed expats get the deduction version, which also reduces income tax. But here's the critical difference: the housing deduction does not reduce self-employment (SE) tax.

SE tax (15.3% on the first $168,600 of net self-employment income in 2024) is calculated on net self-employment income before the housing deduction is applied. A freelance developer in Singapore earning $150,000 might shelter $51,200 via housing, saving roughly $11,264 in income tax (at 22%). But they still owe SE tax on all $150,000 of earnings — approximately $21,240 — regardless of how much rent they pay.

The only way self-employed expats reduce SE tax is through totalization agreements, which exempt you from US Social Security if you're paying into a host country's equivalent system. The US has these agreements with 30 countries — worth checking before assuming you'll owe SE tax in perpetuity.

For a more complete picture of how the FEIE interacts with other strategies, see our breakdown of FEIE vs. the Foreign Tax Credit — which wins depends heavily on whether your host country taxes you and at what rate.

When You Shouldn't Use the Foreign Housing Exclusion

Not every expat benefits from stacking the FEIE and housing exclusion. In high-tax countries — the UK, Germany, France, Australia — the Foreign Tax Credit (FTC) alone often zeros out US tax entirely. Taking the FEIE and housing exclusion in a high-tax country creates a structural problem: you can't take the FTC on income you've already excluded (IRC §911(d)(6)).

Here's the scenario that trips people up: An employee in London earns $180,000 and pays $72,000 in UK income tax. With FEIE + housing exclusion, they exclude roughly $175,000 of income. But they can't use the FTC on the excluded portion. The sliver of taxable US income remaining generates a small US tax bill — but the massive FTC credits that could have wiped it out entirely are unavailable because the income was already excluded.

With FTC alone on $180,000 of income, the $72,000 in UK taxes paid generates enough credit to eliminate US tax completely — with leftover credits that carry forward 10 years.

Rule of thumb: FEIE + housing exclusion wins in low-tax or zero-tax countries (UAE, Cayman, Singapore at lower incomes). FTC wins in high-tax countries (UK, Germany, France, Australia). The break-even depends on your specific income level, country tax rate, and how much of the housing exclusion you'd actually use. Model it before choosing — and remember the FEIE election is sticky: revoking it requires IRS permission, and you can't re-elect for 5 years after revocation.

Form 2555: The Actual Mechanics

Both the FEIE and the Foreign Housing Exclusion/Deduction are claimed on Form 2555. The parts relevant to housing:

| Form 2555 Part | What It Does |

|---|---|

| Part I | General info: foreign address, employer, tax home |

| Part II or III | Qualify via Bona Fide Residence or Physical Presence Test |

| Part VI | List all housing expenses; compute total qualifying amount |

| Part VII | Foreign Earned Income Exclusion computation |

| Part VIII | Employee Housing Exclusion — subtract base, apply city cap |

| Part IX | Self-Employed Housing Deduction — same math, treated as a deduction |

The employee exclusion flows to Schedule 1, Line 8d of Form 1040. The self-employed deduction flows to Schedule 1, Line 24b. Most expat-focused tax software populates these automatically — if you enter data into Part VI. The problem is that many people stop at Part VII (the FEIE) and never reach the housing section.

Nine Expensive Mistakes to Avoid

Not claiming it at all. The most common error by far. If your rent abroad exceeds roughly $1,734/month, you almost certainly qualify for some exclusion amount regardless of city.

Using consumer software's defaults. TurboTax and H&R Block standard flows frequently bypass the housing exclusion unless you manually navigate to expat sections and prompt for it.

Not prorating for partial years. Move abroad on July 1? Both the base amount and the cap must be prorated by qualifying days. Claiming the full annual amounts on a half-year abroad overstates the exclusion and triggers IRS notices.

Using the wrong Part of Form 2555. Employees use Part VIII. Self-employed use Part IX. Using the wrong one gets the claim automatically disallowed.

Claiming non-qualifying expenses. Internet, phone, new furniture, domestic help — none of these qualify. IRS auditors know the list and will ask for itemized documentation.

Double-dipping with the FTC. Trying to take the Foreign Tax Credit on income already excluded is an immediate audit trigger and requires an amended return to fix.

Missing city-specific caps. If you're in London, Tokyo, Singapore, or Hong Kong, the default 30% cap doesn't apply. The city-specific cap is much higher. Missing this means leaving thousands unclaimed even if you do file the housing exclusion.

Thinking employer-paid housing disqualifies you. If your employer includes a housing allowance in your W-2 as taxable compensation, that income qualifies as the basis for the housing exclusion calculation. Many corporate expat packages include exactly this.

Not amending prior years. If you qualified for the housing exclusion in prior years and didn't claim it, you can generally file Form 1040-X going back three years. Notice 2025-16 also allows the 2025 housing limits to be applied retroactively to 2024 amended returns, which may increase the excludable amount beyond what was originally available.

The Practical Logistics: Keeping Your US Presence Current

Claiming the Foreign Housing Exclusion and staying current on expat tax compliance requires maintaining a valid US address for IRS correspondence, banking, and state domicile. Many expats use a virtual mailbox service for this — a real US street address that scans and forwards physical mail.

The owner of this site personally uses Traveling Mailbox — it provides a real US street address in 50+ cities, scans incoming mail, and lets you deposit checks remotely for about $15/month. If you're filing Form 2555 from abroad and need a reliable address for IRS letters and bank statements, it's covered in more detail in our virtual mailbox guide for expats.

For expat brokerage and banking options that work while living overseas, Charles Schwab International remains one of the few US brokerages that actively supports expats — with free global ATM withdrawals and no foreign transaction fees, it solves the banking side of the equation while you focus on the tax side.

The Bottom Line

The Foreign Housing Exclusion is one of the most underused provisions in the entire US tax code. It's not buried in obscure IRS guidance — it's on Form 2555, the same form millions of expats file every year. It goes unclaimed because expats stop at the FEIE and assume they're done, because tax software defaults push users past Part VI without prompting, and because generalist CPAs often don't ask the right questions.

If you're paying rent abroad that exceeds $1,734/month, you qualify for some exclusion. If you're in Hong Kong, Geneva, Singapore, Tokyo, or London, you may be able to shelter an additional $27,000–$93,000 of income — potentially saving $5,940 to $20,000+ in federal taxes this year alone. And if you've missed it in prior years, amended returns are on the table.

For broader context on structuring your finances as a US expat, see our guides on expat investing and PFIC rules and the complete FEIE guide for expats.

Financial Disclaimer: This article is for informational and educational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently and individual circumstances vary significantly. Consult a qualified tax professional who specializes in US expatriate taxation before making any decisions based on this content. Some links in this article are affiliate links — we may earn a commission at no additional cost to you.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 6, 2026

Expat Tax & FinanceMay 6, 2026

The Foreign Housing Exclusion Most Expats Forget to Claim

The IRS Foreign Housing Exclusion stacks on top of FEIE. In Hong Kong, it can exclude another $93,500. Here are the 2025 city limits and how to claim

Expat Tax & FinanceJuly 14, 2026

Expat Tax & FinanceJuly 14, 2026

Expat State Taxes: Which US States Won't Let You Go

Move abroad and California may still tax you 13.3%. Learn which five states chase expats, how domicile works, and how to sever state ties legally.

Expat Tax & FinanceMay 29, 2026

Expat Tax & FinanceMay 29, 2026

Self-Employment Tax: The Expat Freelancer’s Hidden Bill

FEIE zeroes your income tax abroad—but SE tax still applies. See the exact numbers and legal ways to reduce your bill as a US expat freelancer.