Puerto Rico Act 60: Cut Taxes to 0% Without Leaving the US

11 min read · 2,812 words

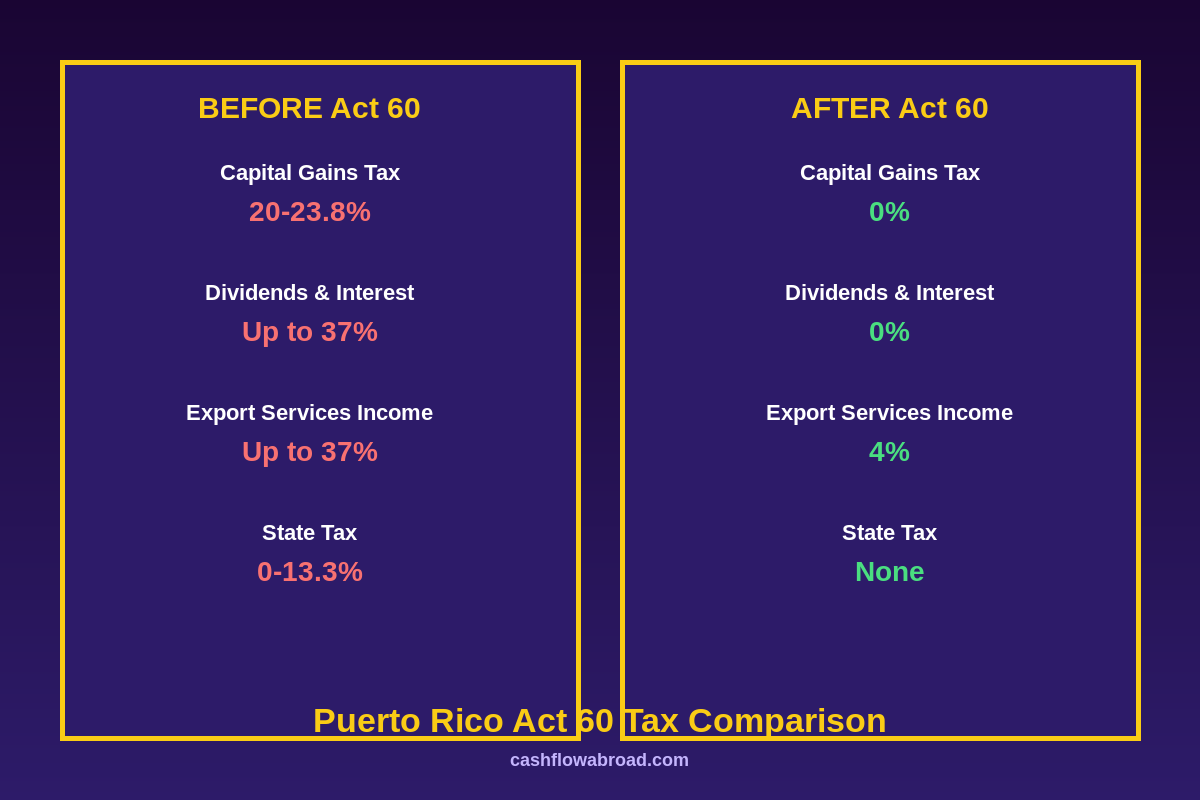

Here’s a number that should stop any high-earner cold: the top US federal capital gains rate is 23.8%. Stack California’s 13.3% on top and you’re handing 37.1% of every stock sale to the government. Now here’s the kicker — a move to a US territory (you keep your US passport, no visa required, domestic flights) can legally cut that to 0%. Puerto Rico’s Act 60, extended through 2055, remains the most aggressive legal tax reduction available to American citizens — and most people who could benefit have never seriously looked at it.

This isn’t a loophole. Congress explicitly exempted Puerto Rico from certain federal tax rules under IRC § 933. If you become a bona fide resident of Puerto Rico and get approved under Act 60, capital gains you earn after moving are taxed at 0% by both Puerto Rico and the federal government. Services exported outside Puerto Rico? Taxed at a flat 4%. No US state or territory comes close to this deal.

What Act 60 Actually Is

Act 60 (formally the Puerto Rico Incentives Code) is a 2019 consolidation of two earlier laws: the Export Services Act (originally Act 20) and the Individual Investors Act (Act 22). It exists because Puerto Rico, as an unincorporated territory with a struggling economy and massive debt burden, desperately needs high-net-worth individuals and businesses to relocate and spend money in the local economy.

The law works because of a Constitutional quirk. Under IRC § 933, income from Puerto Rico sources is excluded from federal gross income for bona fide residents. This isn’t a deduction — it’s an exclusion. The income never enters the federal return. Puerto Rico then taxes it at preferential rates (or not at all) under Act 60.

Puerto Rico’s Act 38-2026, signed in March 2026, extended Act 60 through 2055. But it came with one critical change: applicants who file on or after January 1, 2027 get a 4% rate on passive income instead of 0%. Anyone who applied by December 31, 2026 is grandfathered at 0% for the life of their decree — potentially decades. That window is effectively closed for new applicants going forward, but the program remains highly compelling even at 4%.

The Actual Tax Benefits by Income Type

Act 60 has two main components. Most people conflate them, which leads to confusion about what’s actually tax-free.

Chapter 2: Individual Investor (formerly Act 22)

This is the passive income play. Qualified individual resident investors pay:

- 0% tax on capital gains accrued after establishing Puerto Rico residency (4% for new applicants from 2027)

- 0% tax on dividends and interest from Puerto Rico sources

The critical nuance on dividends and interest: the IRS treats investment income as sourced where the payer is located, not where the taxpayer lives. Dividends from Apple (a US company) are US-source income — they’re still federally taxable even after you move to Puerto Rico, unless you hold those shares through a Puerto Rico entity. What does go to 0% or 4%: capital gains from assets purchased after you become a bona fide Puerto Rico resident. If you buy $1M of NVIDIA stock after establishing residency and sell it three years later for $5M, that $4M gain is Puerto Rico-source income and is fully exempt.

Pre-move gains? Still taxable at your old rate. The clock starts only when you officially become a bona fide resident.

Chapter 3: Export Services (formerly Act 20)

This is for income-producing businesses. If you own a Puerto Rico entity providing services to clients outside Puerto Rico, that income is taxed at a flat 4% by Puerto Rico. Federal tax? Zero, because it’s Puerto Rico-source income for a bona fide resident.

Qualifying services include: consulting, technology, marketing, financial services, legal services, accounting, research and development, advertising, software development. Essentially: if you’re selling expertise or digital services to non-Puerto Rico clients, it likely qualifies. The business must have genuine substance in Puerto Rico — employees, operations, management on the island.

Who Benefits Most

Act 60 isn’t for everyone. The setup costs, compliance requirements, and lifestyle commitment make it a genuine calculation. Here’s who comes out ahead:

| Profile | Annual Tax Savings (est.) | Why It Works |

|---|---|---|

| Crypto trader with large unrealized gains (CA resident) | $500K–$5M+ | 0%/4% vs 37.1% federal + 13.3% CA on realized gains |

| Remote consultant billing $300K/yr | $80K–$100K | 4% vs 37% on service income (Chapter 3) |

| SaaS founder planning a $5M exit | $1.5M–$2.5M | Business sale gains near 0% if structured correctly |

| Stock trader in NY or CA | $100K–$500K/yr | 0%/4% on post-move capital gains vs combined 37%+ |

| Dividend investor (PR-sourced holdings) | $40K–$150K | 0% on qualifying Puerto Rico dividends |

The common denominator: large capital events — business sales, stock exits, crypto liquidations — are where Act 60 generates life-changing savings. For someone whose entire portfolio was accumulated before moving, the benefit is more modest since pre-move gains remain federally taxable.

Related: How to Pay Zero Federal Tax as a US Expat — for Americans who’ve already left the US, the Foreign Earned Income Exclusion may be a better starting point.

The Three IRS Tests You Must Pass

Puerto Rico residency for Act 60 purposes is determined by three tests under IRC § 937. You must pass all three simultaneously.

1. Physical Presence Test

Spend at least 183 days per year in Puerto Rico. Days in any US state don’t count. The IRS has access to airline records, credit card transaction data, cell phone location records (via carrier agreements), and social media metadata. The GAO’s December 2025 report explicitly recommended the IRS systematically cross-reference this data for all Act 60 decree holders — and the IRS agreed with all recommendations.

In 2025, Puerto Rico’s Office of Business Incentives audited nearly 1,800 decree holders and found a significant portion spending fewer than 183 days on the island. The IRS ran over 300 Act 60 audits that same year.

2. Tax Home Test

Your principal place of business must be in Puerto Rico. If you work remotely for a New York company from your San Juan condo, you may fail this test — your tax home could still be argued as New York. The cleanest structure: a Puerto Rico entity (Chapter 3) that is your employer or consulting business. That anchors your tax home to the island.

3. Closer Connection Test

You must have stronger ties to Puerto Rico than to any US state. Measured by: location of your permanent home, car registration, bank accounts, where your family lives, professional license registration, voter registration, and social/community ties. If your spouse and kids stay in Dallas and you vote in Texas, you fail this test regardless of day count.

The Real Cost of Going Act 60

The government fees alone aren’t prohibitive. The full compliance stack is where the math gets real.

| Cost Item | Amount | Frequency |

|---|---|---|

| Government application fee | $5,005 | One-time |

| Acceptance fee | $105 | One-time |

| Annual compliance filing fee | $5,005 | Annual |

| Mandatory charitable donation (2 Puerto Rico nonprofits) | $10,000–$15,000 | Annual |

| Puerto Rico CPA (local tax filing) | $3,000–$8,000 | Annual |

| US tax attorney / Act 60 counsel | $5,000–$15,000 | Annual |

| Housing (San Juan, good neighborhood) | $2,500–$6,000/mo | Monthly |

| Property purchase (required within 2 years) | $300K–$800K+ | One-time |

All-in, expect $30,000–$50,000 per year in compliance overhead and living costs before housing. That’s the break-even math: if annual tax savings clearly exceed $50K, Act 60 likely makes financial sense. If you’re saving $500K a year, it’s a no-brainer. If you’re saving $20K, the math doesn’t work.

The property purchase requirement — own residential property in Puerto Rico within two years of your decree approval — has caught many people off guard. It doesn’t have to be your primary residence; a rental investment qualifies. But you must own it.

The IRS Crackdown Is Real and Accelerating

The early Act 22 days (2012–2019) were the Wild West. Wealthy tech founders moved to Puerto Rico on paper, kept their families in California, spent much of the year in San Francisco, and claimed 0% rates. Many got away with it for years. That era is definitively over.

The IRS launched Campaign 685 specifically targeting Puerto Rico residency claims. The GAO’s December 2025 report recommended — and the IRS agreed — establishing systematic procedures to cross-reference all Act 60 decree holders with federal tax data, flight records, and financial transaction data. This is no longer relying on self-reporting.

Penalties for non-compliance escalate quickly: fines start at $1,000 per violation, late compliance portal submissions cost $200 per day, and the government can revoke your decree entirely — retroactively. Revocation means back taxes, a 25% penalty, and accumulated interest on everything you thought you’d avoided. Some high-profile cases have resulted in criminal referrals.

The 2026 compliance portal requires enhanced annual reporting: certified CPA attestation letters, proof of 183+ days (travel records, utility bills), proof of primary residence, and documentation of charitable donations. This isn’t paperwork you assemble in a weekend.

How to Apply: The Step-by-Step Process

- Establish physical residency first. Rent an apartment, set up utilities in your name, and open a Puerto Rico bank account. Document everything with dated receipts from day one.

- Hire a Puerto Rico incentives attorney. Non-optional. The application requires legal certification and Puerto Rico-specific expertise. Fees: $5,000–$15,000.

- Form your Puerto Rico entity (for Chapter 3 applicants). A Puerto Rico LLC or corporation must be registered and operational before you apply for the export services decree.

- Submit the decree application through the Puerto Rico DDEC (Department of Economic Development and Commerce) portal. Pay the $5,005 fee plus $105 acceptance fee.

- Await approval. The DDEC typically processes applications in 45–90 days; complex cases can take longer.

- File Form 8898 with the IRS to formally establish your Puerto Rico residency for tax purposes. Missing this filing is its own penalty.

- Purchase property within 2 years of your decree approval date.

- File annual compliance reports and pay the $5,005 annual fee plus charitable donations.

One mistake that kills Act 60 benefits before they start: failing to properly sever ties with your former state. California’s Franchise Tax Board is notoriously aggressive. You need to update your driver’s license, vehicle registration, voter registration, professional licenses, and bank accounts to Puerto Rico. Keep dated records of each change. Our full guide on expat banking and taxes covers the state-tie severance process in detail.

Crypto Traders: The Specific Math

Act 60’s most dramatic beneficiaries are often crypto holders sitting on massive unrealized gains. A California crypto investor with $10M in unrealized gains faces:

- Federal capital gains: 23.8% = $2.38M

- California state tax: 13.3% = $1.33M

- Total tax bill if sold today: $3.71M

Move to Puerto Rico, spend 183+ days, establish bona fide residency, then accumulate new positions in crypto from your Puerto Rico exchange account. Any appreciation on assets purchased after your residency date generates Puerto Rico-source income — exempt at 0% (or 4% for post-2026 applicants). The pre-residency gain on coins you held before moving? Still taxable. But any new gain from the day you become a resident: zero.

The IRS has been particularly aggressive about crypto + Act 60 cases because income sourcing rules are genuinely complex. Holland & Knight’s November 2025 analysis noted that “the source of cryptocurrency gain depends on facts and circumstances” — specifically where the taxpayer was domiciled when the asset was sold, not when it was purchased. For the full picture on crypto taxes as a US person abroad, see our expat crypto tax guide.

Crypto exchange infrastructure in Puerto Rico has grown substantially. For tracking your crypto tax positions across exchanges, CoinTracking generates IRS-compliant reports and handles the cost-basis tracking that becomes critical when some positions are Puerto Rico-source and some aren’t.

Act 60 vs. Other Legal Tax Reduction Strategies

| Strategy | Effective Rate | Keep US Passport? | Leave the US? | Annual Compliance Cost |

|---|---|---|---|---|

| Puerto Rico Act 60 (grandfathered) | 0% on passive income | Yes | No (US territory) | $30K–$50K |

| Puerto Rico Act 60 (post-2026) | 4% on passive income | Yes | No (US territory) | $30K–$50K |

| FEIE (move abroad) | ~0% on first ~$130K earned income | Yes | Yes | $5K–$15K |

| Georgia (country) 1% flat tax | 1% on local income | Yes | Yes | $3K–$8K |

| Paraguay foreign income exemption | 0% on foreign income | Yes | Yes | $3K–$6K |

| Renounce US citizenship | 0% (if properly structured) | No | Yes | $5K exit tax + $2,350 fee |

Act 60 is uniquely positioned because it keeps you in the US ecosystem. US banking works normally, no FBAR complications (Puerto Rico is domestic territory, not a foreign country), Social Security contributions continue, and you travel to the mainland as freely as any American. The trade-off: significantly higher compliance costs and stricter physical presence enforcement than most foreign residency strategies.

If you’re considering moving abroad instead, the geographic arbitrage playbook covers 10 countries where your dollar goes 3–5x further, many with territorial tax systems that exempt all foreign income.

Four Mistakes That Get Act 60 Decrees Revoked

1. Splitting time 50/50 and hoping for the best. The IRS uses flight data systematically under Campaign 685. If your credit card shows regular charges in Manhattan and your cell phone pings cell towers in New Jersey 120 days a year, expect scrutiny. The 183-day rule means 183 days physically in Puerto Rico — not 183 days outside a specific state.

2. Failing to sever state ties. California’s FTB is notorious. A California driver’s license, a California LLC still on the books, and kids in a California school gives the FTB grounds to maintain you’re a California tax resident — meaning both California and Puerto Rico claim your income. Double taxation with penalties from both.

3. Building a shell operation. A Puerto Rico LLC with no Puerto Rico employees, a $200/month virtual office address, and a CEO who “manages remotely” from Boston fails the economic substance test. Chapter 3 auditors request phone records, meeting schedules, payroll records, and utility bills. Genuine operations mean genuine operations.

4. Missing the charitable donation documentation. The $10,000–$15,000 to qualifying Puerto Rico nonprofits must be documented with receipts in the compliance portal. Missing this filing triggers an automatic $1,000 fine and can flag the entire return for broader audit.

Banking and Logistics in Puerto Rico

Because Puerto Rico is a US territory, most of your US financial infrastructure transfers without friction. Your existing US brokerage accounts, 401(k), and IRA stay intact. FDIC-insured Puerto Rico bank accounts (Banco Popular, FirstBancorp, Oriental Bank) are domestic accounts — no FBAR required.

For investment accounts, Charles Schwab International works seamlessly in Puerto Rico as a domestic account — free ATMs worldwide, no foreign residency-triggered closures, and access to international ETFs. Unlike Fidelity and Vanguard, which have closed expat accounts, Schwab has historically maintained accounts for US citizens living abroad, including in Puerto Rico.

If you’re maintaining a US mainland address for IRS correspondence, state domicile documentation, or banking with institutions that require a state-specific address, a Traveling Mailbox virtual address ($15/month) gives you a real US street address with mail scanning. Given that Act 60 compliance requires documenting your state-tie severance with dated evidence, having a formal mainland address management system in place is worth the cost.

Living in Puerto Rico: What You’re Actually Getting

The financial case is clear for the right income profile. The lifestyle case is often undersold. San Juan has neighborhoods — Condado, Miramar, Isla Verde — that feel like Miami with year-round 80°F temperatures, better beaches, and no state income tax. The food scene is underrated. English is universally spoken in professional and commercial settings.

Cost of living is lower than any comparable US coastal city. A two-bedroom apartment in Condado runs $2,000–$3,500/month. Restaurants average $15–$30/entrée at mid-range spots. A comfortable monthly budget (excluding housing) runs $2,500–$4,000 for a single person. The island is 110 miles long — you can live in San Juan and be at a remote beach in 45 minutes.

The main trade-offs: professional isolation if your network is in New York or Silicon Valley (a 3-4 hour flight), infrastructure that lags the mainland (power outages, though much improved since the 2022 grid investments), and a dating/social scene that’s smaller than major metros. These are real factors that some Act 60 residents underestimate.

For international health coverage while you build out your Puerto Rico setup — particularly in the first year before you’re fully integrated into the local system — SafetyWing Remote Health provides comprehensive international hospital and specialist coverage at a fraction of US insurance costs.

The Bottom Line

Puerto Rico Act 60 is not a loophole — it’s a Congressional policy tool that has redirected billions in capital to a territory that needed investment. Done right, it’s the closest legal equivalent to eliminating capital gains tax for a US citizen without giving up citizenship. Done poorly, it’s a six-figure compliance disaster with the IRS.

The 0% grandfathering window closed at end of 2026. New applicants face a 4% rate — still dramatically lower than any US state rate for high earners, and still worth the compliance cost at scale. The enforcement environment is materially stricter than five years ago. The people who succeed under Act 60 treat it as a genuine relocation, not a tax filing trick: 183+ actual days on the island, real business operations, genuine community ties, and a compliance infrastructure that would survive an IRS audit.

If that description fits your situation and your tax savings exceed $50K annually, the math strongly supports a serious look. If you’re hoping to spend six months in your California house and file a Puerto Rico return — the IRS is waiting for you.

Financial Disclaimer: This article is for informational and educational purposes only and does not constitute legal, tax, or financial advice. Puerto Rico Act 60 rules, compliance requirements, and IRS enforcement priorities change frequently. Individual circumstances vary significantly. US citizens should consult a qualified tax attorney with specific expertise in Puerto Rico Act 60 incentives and US international tax law before making any residency, investment, or tax planning decisions. Nothing in this article constitutes a recommendation to establish residency in any jurisdiction or restructure any financial arrangement.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.