Foreign Housing Exclusion: Expats Miss This $35K Tax Break

9 min read · 2,349 words

Here’s a number that might make you furious: the IRS allows US expats to exclude an extra $18,200 to $93,500 from their taxable income on top of the Foreign Earned Income Exclusion — and the majority of qualifying Americans abroad never claim it. Not because it’s complicated to file. Because they’ve never heard of it.

The Foreign Housing Exclusion (FHE) is a separate benefit from the FEIE, calculated on the same Form 2555, and it’s specifically designed to offset the real cost of renting abroad. Expats in high-rent cities like Singapore, London, or Hong Kong can exclude tens of thousands more per year. Even expats in cheaper markets can shave another $4,000–$5,000 off their federal tax bill with zero extra paperwork or forms.

Let’s break down exactly how this works, who qualifies, how to calculate your exclusion, and the five mistakes that cause people to leave money on the table.

What Is the Foreign Housing Exclusion?

The Foreign Housing Exclusion lets qualifying US citizens and resident aliens exclude housing costs paid from employer-provided amounts from their US taxable income. If you’re self-employed, the parallel benefit is the Foreign Housing Deduction — same concept, different tax treatment (more on this below).

It sits on top of the Foreign Earned Income Exclusion. The FEIE caps at $130,000 for tax year 2025 and $132,900 for 2026. The housing exclusion stacks on top — it’s not substituted. Together, a married couple both working abroad can potentially exclude $260,000+ in combined earned income before a dollar of US tax applies.

The housing exclusion is calculated first on Form 2555. This sequencing matters: by reducing taxable income before the FEIE is applied, you can potentially use the full FEIE on top of housing costs, rather than burning part of it on rent you could’ve excluded separately.

Who Qualifies

You need to pass the same tests that govern FEIE eligibility:

- Bona Fide Residence Test: You’ve been a bona fide resident of a foreign country for an uninterrupted period that includes an entire tax year.

- Physical Presence Test: You were physically present in a foreign country for at least 330 full days during any 12-month period.

If you already claim the FEIE, you automatically satisfy these tests for the housing exclusion. There’s no separate qualification process — it’s a section on Form 2555 that most people skip past without realizing what they’re leaving behind.

One important restriction: your foreign housing amount cannot exceed your total foreign earned income for the year. This rarely affects most expats but caps the benefit in low-income partial-year situations.

How the Calculation Works

The formula is simple:

Housing Exclusion = Qualifying Expenses − Base Housing Amount

(subject to the IRS cap for your specific city)

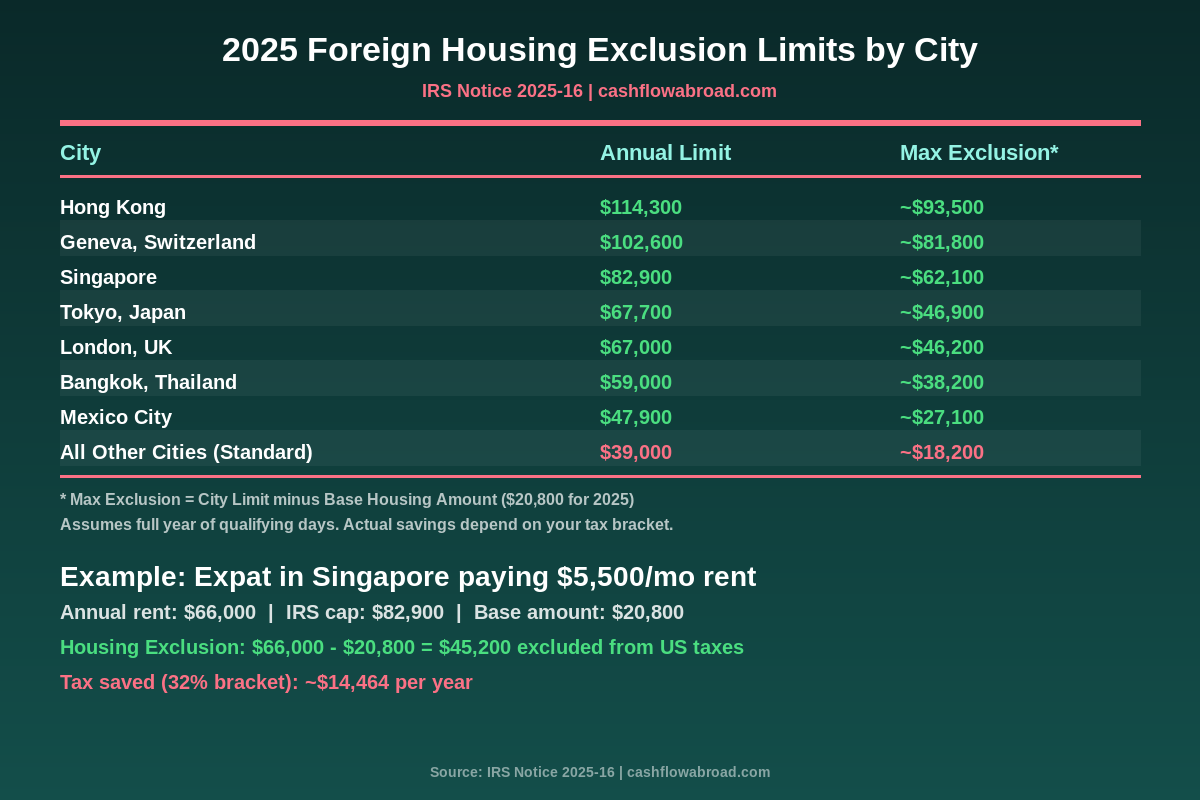

For tax year 2025:

- Base housing amount: $20,800 (always 16% of that year’s FEIE limit)

- Standard city cap: $39,000 (for locations not listed in IRS Notice 2025-16)

- Maximum exclusion in a standard city: $39,000 − $20,800 = $18,200

High-cost cities get substantially higher caps. Here’s where expats in pricier markets really benefit:

Real-World Example: Singapore

You work remotely for a US employer in Singapore, earning $150,000. You pay $5,500/month in rent ($66,000/year) — reasonable for a decent two-bedroom in Tiong Bahru or Buona Vista.

| Item | Amount |

|---|---|

| Annual qualifying housing expenses | $66,000 |

| Singapore IRS housing cap (2025) | $82,900 |

| Less: Base housing amount | −$20,800 |

| Foreign Housing Exclusion | $45,200 |

| Remaining earned income | $104,800 |

| FEIE applied to remaining income | −$104,800 |

| US taxable earned income | $0 |

| Tax saved vs. not claiming housing exclusion (32% bracket) | ~$14,464 |

Without the housing exclusion, $20,000 in income would be taxable at the 32% rate — roughly $6,400 in extra taxes paid for no reason, on the same Form 2555 you’re already filing.

Real-World Example: London

Expat in London earning $140,000, paying £3,500/month in rent (~$53,500/year at current rates):

| Item | Amount |

|---|---|

| Annual qualifying housing expenses | $53,500 |

| London IRS housing cap (2025) | $67,000 |

| Less: Base housing amount | −$20,800 |

| Foreign Housing Exclusion | $32,700 |

| Tax saved (24% bracket) | ~$7,848 |

Standard-city expats — say someone in Lisbon paying $2,800/month in rent: $33,600/year in qualifying expenses. Exclusion: $33,600 − $20,800 = $12,800. Tax saved at 22%: $2,816. Not life-changing, but that’s money returned for filling out a section you’re skipping.

What Counts as a Qualifying Expense

The IRS is specific about what qualifies. Including the wrong expenses is one of the most common audit triggers:

Qualifying:

- Rent

- Utilities — electricity, gas, water (but not telephone or internet)

- Property insurance premiums

- Residential parking fees

- Furniture rental

- Reasonable household repairs

- Occupancy taxes paid to the foreign government

Not qualifying:

- Mortgage interest or principal (this exclusion is rent-focused)

- Cable TV, streaming, or internet service

- Telephone bills

- Domestic labor — housekeepers, gardeners, nannies

- Expenses that are “lavish or extravagant” by local standards

That last point has real nuance. A $10,000/month apartment in Hong Kong is neither lavish nor extravagant in that market. The IRS city-specific caps in Notice 2025-16 reflect this explicitly. The limits exist because the IRS acknowledges that reasonable housing in Singapore costs exponentially more than it does in Atlanta.

Employees vs. Self-Employed: A Critical Difference

If you’re an employee — W-2, salary from a foreign employer, or remote work for a US company — you use the Foreign Housing Exclusion. This reduces taxable income dollar-for-dollar on Form 2555, Part V.

If you’re self-employed — freelancer, consultant, online business owner — you use the Foreign Housing Deduction instead. Same formula, same caps, but it’s a deduction rather than an exclusion. The critical downside: the foreign housing deduction does not reduce your self-employment tax. You still owe 15.3% SE tax on the gross income before this deduction applies.

That makes the housing benefit significantly less valuable for self-employed expats. A $32,700 housing deduction at 24% income tax saves $7,848 in income tax — but you’ve still paid SE tax on that same income. Employees with the same deduction save the full amount with no SE tax owed on excluded income.

If you’re self-employed and earning abroad, the FEIE plus housing deduction combination is still worth claiming. Just understand the limitation and account for it in estimated quarterly SE tax payments. See the US Expat Banking & Taxes guide for how this interacts with FBAR and FATCA reporting obligations.

5 Mistakes That Cost Expats Thousands

1. Not Claiming It at All

The most expensive mistake. A 2023 survey by Greenback Tax Services found that roughly 40% of expats filing their own returns either didn’t know about the housing exclusion or simply skipped it. That’s thousands of dollars per filer in unrecovered taxes annually. The fix: Form 2555, Part V (employees) or Part VI (self-employed). If you’ve been filing without it, you can amend returns back three years using Form 1040-X — the statute of limitations gives you a real recovery window.

2. Using the Wrong City Cap

The IRS publishes city-specific limits annually in IRS Notice 2025-16. If your city isn’t on the list, you fall back to the $39,000 standard cap. But many expats in unlisted cities have access to higher caps if their tax home is located in or near a qualifying metropolitan area. An expat living in a Tokyo suburb might qualify for the Tokyo limit ($67,700) rather than the default. The difference: up to $28,700 in additional excludable expenses. Work with an expat tax specialist to confirm your correct city assignment — misapplying the wrong cap either leaves money behind or creates an audit risk.

3. Including Non-Qualifying Expenses

Internet service feels like a utility. To the IRS, it isn’t. Domestic help — even part-time cleaning — doesn’t count. Cable TV doesn’t count. If you inflate qualifying expenses with ineligible items, you’re overstating the exclusion, which is a red flag if audited. Maintain a separate clean spreadsheet with only rent receipts and qualifying utility payments. Keep everything else in a different column.

4. Partial-Year Prorating Errors

If you were abroad for only part of the year — say you moved to Singapore in April — every limit gets prorated by qualifying days. The $20,800 base amount and the city cap both scale proportionally. Divide by 365, multiply by your qualifying day count. Failing to prorate overstates the exclusion and is a textbook audit trigger for partial-year expats. Tax software that specializes in expat returns (Expatfile, MyExpatTaxes) handles this automatically. Generic domestic tax software often does not.

5. Conflating the Exclusion With the Deduction

If your employment status changed mid-year — you left a W-2 job in March and went freelance in April — part of your housing costs fall under the exclusion rules and part under the deduction rules. These are calculated separately on different parts of Form 2555. Mixing them together either overstates the benefit or understates your SE tax liability. This specific scenario is where hiring an expat CPA for one year pays for itself immediately — the correction typically far exceeds the cost of professional filing.

Stacking the FEIE and Housing Exclusion

Used together strategically, these two provisions give expat couples remarkable tax efficiency:

| Scenario | FEIE | Housing Exclusion | Total Excluded |

|---|---|---|---|

| Single expat, standard city | $130,000 | up to $18,200 | up to $148,200 |

| Single expat, Singapore | $130,000 | up to $62,100 | up to $192,100 |

| Single expat, Hong Kong | $130,000 | up to $93,500 | up to $223,500 |

| Married couple, both working, standard city | $260,000 | up to $18,200* | up to $278,200 |

| Married couple, both working, London | $260,000 | up to $46,200* | up to $306,200 |

*Couples share one set of housing costs, not a separate exclusion per person. The exclusion applies to actual qualifying expenses, not a per-capita figure.

A US couple earning $260,000 combined in Singapore — a solid but not exceptional tech or finance income in that city — can potentially exclude their entire earned income from US federal taxes. Their Singapore tax obligation depends on local law (Singapore taxes are generally low on most foreign-sourced income), but the US bill on $260,000? Zero.

This is legal, IRS-approved, and precisely why these provisions exist. The government doesn’t want to triple-tax expats who are already paying local taxes and absorbing above-average housing costs in expensive markets.

How to File: Form 2555 Walkthrough

You don’t need a separate form. The housing exclusion lives on Form 2555 — the same form used for the FEIE. The key sections:

- Part I: General info, tax home address, residency test election

- Part II or III: Bona Fide Residence or Physical Presence Test (whichever applies)

- Part IV: Your total foreign earned income for the year

- Part V: Foreign Housing Exclusion (employees). Line 25: total housing expenses. Line 33: IRS cap for your location. Line 36: your actual housing exclusion amount.

- Part VI: Foreign Housing Deduction (self-employed only)

- Part VII–VIII: FEIE calculated on income remaining after the housing exclusion

The software fills Part V before Part VII — housing costs are excluded first, then FEIE applies to remaining income. If your tax software runs this in reverse order, your calculation is wrong and you’re likely overpaying. Most generic domestic tax software doesn’t handle Form 2555 correctly. Dedicated expat tax software or a qualified expat CPA are worth the cost specifically for this sequencing issue.

Maintaining US Infrastructure While Abroad

A practical note: the IRS requires a valid US mailing address for all correspondence related to your return, including any notices about your FEIE and housing exclusion claims. Using a foreign address for IRS correspondence creates compliance friction and delays.

A virtual mailbox solves this. Traveling Mailbox gives you a real US street address (not a P.O. box — which many institutions reject) in 50+ cities, scans your mail digitally so you see it anywhere in the world, and handles check deposits on your behalf. It’s $15/month and keeps your IRS correspondence, bank statements, and brokerage notices in one clean place. I use it for exactly this purpose.

For US banking that won’t close your account the moment you log in from Singapore, Mercury works well for US business accounts — no fees, no minimum balance, and no compliance paranoia about international account holders.

Can You Amend Past Returns?

Yes, within limits. The IRS allows amendments within three years of the original filing deadline using Form 1040-X. If you filed your 2022 return in April 2023, you have until April 2026 to amend and retroactively claim the housing exclusion.

Important caveat: if you’ve been filing Form 2555 and claiming the FEIE but not the housing exclusion, the amendment is straightforward — you’re adding Part V to an already-accepted form. If you’ve never filed Form 2555 (because you used the Foreign Tax Credit instead), switching from FTC to FEIE requires filing Form 8833 and triggers a five-year lock-in. You cannot revert to the FTC strategy for five years after making the FEIE election.

The FTC approach often remains better for expats in high-tax countries — Germany, France, Australia — where foreign taxes already eliminate most US liability. The FEIE plus housing exclusion is most powerful for expats in low-to-moderate tax countries where the foreign tax credit doesn’t fully offset US obligations. The expat investing and tax playbook covers which strategy wins by country.

Expat Filing Deadlines

Expats automatically get a two-month extension — the standard federal deadline of April 15 moves to June 15 for those living outside the US. With a standard extension request, this extends to October 15. The housing exclusion must be claimed at the time of filing — you cannot submit a late Form 2555 on a separate schedule. If you’re amending, attach the completed Form 2555 to your 1040-X.

Keep records of all qualifying housing expenses for at least six years. The IRS audit window for expat returns is sometimes extended beyond the standard three years due to the complexity of international provisions.

Bottom Line

The Foreign Housing Exclusion is not an obscure loophole. It’s a mainstream IRS provision with its own dedicated section on Form 2555, city-specific limits published annually by the IRS, and a clear formula. The only reason more expats don’t claim it is that it’s undersold by generic tax advice and overlooked by do-it-yourself filers who copy their domestic filing habits overseas.

If you’re an employee working abroad, paying rent, and already claiming the FEIE: add the housing exclusion. The additional excludable amount ranges from $18,200 in standard cities to $93,500 in Hong Kong. At a 24% marginal rate, that’s $4,368 to $22,440 in real money returned to your pocket annually — from a form you’re already filing.

If you’ve filed without it for multiple years, run the math on Form 1040-X amendments back to 2022. The three-year window is closing. Make sure you’re not one of the expats leaving tens of thousands on the table.

Disclaimer: This article is for informational and educational purposes only and does not constitute tax, legal, or financial advice. Expat tax rules are complex and subject to change. The examples in this article are illustrative only. Consult a qualified CPA or tax attorney who specializes in US expat taxation before making any decisions about your tax filing strategy, including whether to claim the Foreign Housing Exclusion or Deduction, and whether to amend prior returns.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.