Portugal D7 Visa: EU Residency on Passive Income

9 min read · 2,204 words

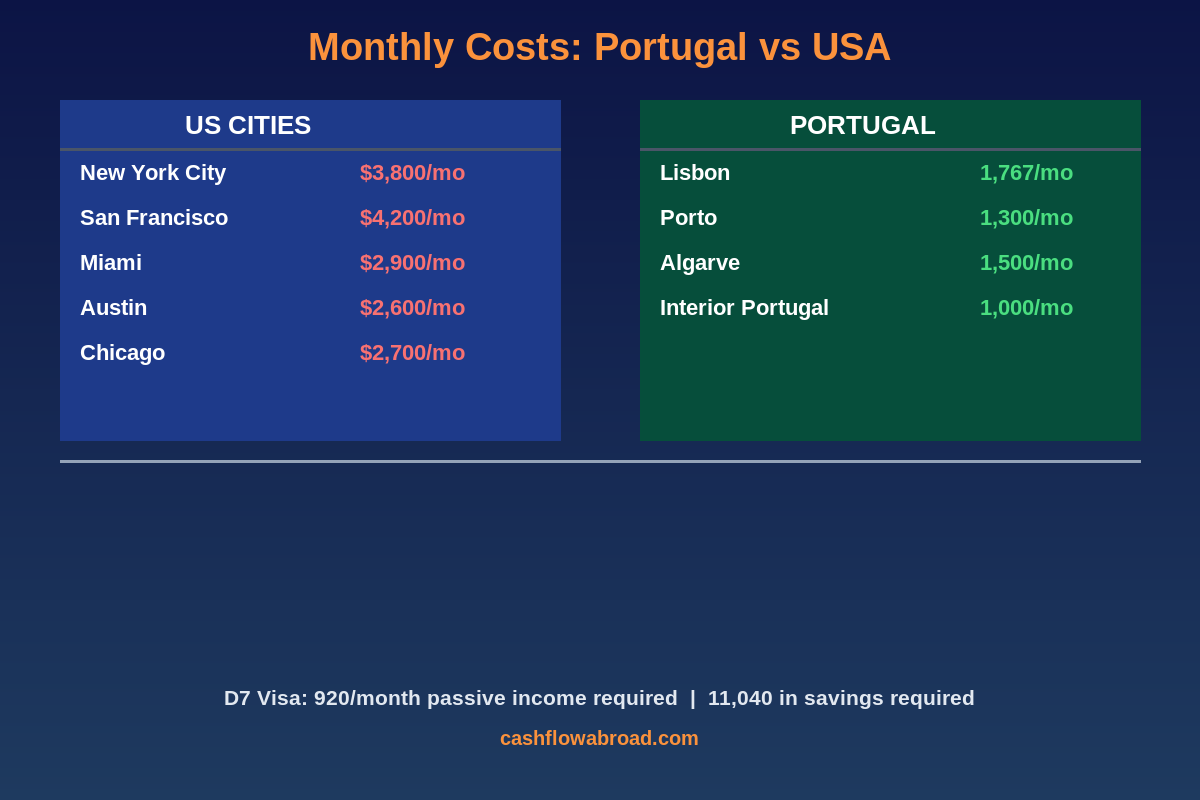

Most Americans spend more on a single month of rent in a major US city than Portugal requires as total monthly income to qualify for EU residency. That’s not a typo. The Portugal D7 Visa — officially the Passive Income Visa — lets you trade your $3,800 New York apartment for a two-year renewable residence permit in one of Western Europe’s most livable countries, for a minimum income threshold of €920 per month.

The D7 isn’t a golden visa. You’re not buying your way in with a €500,000 investment. You’re demonstrating that you can support yourself on passive income — a pension, dividends, rental income, royalties — without burdening the Portuguese social system. If you can do that, Portugal will hand you a path to permanent residency in five years and (potentially) an EU passport in ten.

Here’s everything you need to know before applying.

What Exactly Is the Portugal D7 Visa?

The D7 is a long-stay residency visa for non-EU citizens who earn sufficient passive or remote income to live in Portugal without employment from a Portuguese employer. It was designed primarily for retirees and pensioners, but the definition of qualifying income has expanded over time to include dividends, rental income from abroad, investment returns, royalties, and (in some consulates) remote employment income.

Once approved, the D7 grants a 120-day entry visa that lets you travel to Portugal. After arriving, you apply for a two-year residence permit at AIMA (the immigration authority). That permit renews for successive three-year periods. After five years of legal residency, you qualify for permanent residence. After ten years (recently extended from five for most nationalities), you qualify for citizenship by naturalization — which comes with an EU passport and visa-free access to 186 countries.

Who Qualifies: Income Sources

Portugal’s consulates are fairly flexible on what counts as passive income for D7 purposes. Broadly accepted sources include:

- US Social Security or government pension — the most straightforward qualification

- Private pension or IRA distributions

- Dividend income from stocks or funds

- Rental income from property you own abroad

- Royalties or intellectual property income

- Remote employment income — some consulates accept this; if you’re employed remotely full-time, verify whether D7 or D8 (digital nomad visa) applies to your situation

Active local employment in Portugal does not qualify you for the D7. You’d need a different visa category for that. The D7 is specifically for people whose money follows them — not people who work for Portuguese companies.

The Numbers: Income and Savings Requirements

As of 2026, the minimum monthly passive income threshold is €920 per month, which works out to roughly €11,040 per year (approximately $1,085/month at current exchange rates). This figure is tied to Portugal’s national minimum wage and adjusts periodically.

If you’re applying with dependents, the requirements scale up:

| Applicant Composition | Monthly Income Required | Annual Total |

|---|---|---|

| Single applicant | €920 | €11,040 |

| Couple (applicant + spouse) | €1,380 (+50%) | €16,560 |

| Couple + 1 child | €1,656 (+30% per child) | €19,872 |

| Couple + 2 children | €1,932 | €23,184 |

Beyond monthly income, you’ll also need to demonstrate savings of at least €11,040 held in a Portuguese bank account. Many consulates want to see 12 months of bank statements showing consistent income, plus a lump-sum deposit in a Portuguese bank before finalizing your residency permit.

Compare that to the D7’s expensive sibling — the Golden Visa requires a minimum €500,000 investment in Portuguese funds, real estate (in limited regions), or donations. The D7 costs less than two months of New York rent to qualify.

The Application Process: Step by Step

The D7 runs in two stages. First you apply for the visa in the US; then you finalize your residency in Portugal. Budget 6–9 months for the full process.

Stage 1: Apply at Your Portuguese Consulate

Portugal has consulates in major US cities including Washington DC, New York, Boston, San Francisco, and Newark. You’ll need to schedule an appointment — which can take months during busy periods — so start early.

Documentation checklist for the consulate application:

- Valid US passport (valid for at least 6 months beyond your intended stay)

- Completed D7 visa application form

- Proof of passive income: 3–12 months of bank statements, pension award letters, dividend statements, or rental agreements

- Proof of accommodation in Portugal: signed rental agreement (12+ months) or property purchase deed

- Comprehensive health insurance valid in Portugal — required for the application

- FBI background check, apostilled (this takes 4–8 weeks; start immediately)

- Recent passport-size photos

- Application fee: approximately €90–€175, depending on consulate

The health insurance requirement trips up many applicants. Portugal requires comprehensive coverage for the duration of your initial stay. SafetyWing’s Nomad Insurance is accepted by most consulates and runs about $56–$89/month depending on your age — significantly cheaper than US-equivalent coverage. For a deeper look at expat health coverage options, see our expat health insurance guide.

Stage 2: Finalize Residency in Portugal

Once the D7 entry visa is approved (typically stamped in your passport), you have 120 days to travel to Portugal. After arriving, you schedule a biometrics appointment with AIMA — fingerprints and a photo for your residence card. AIMA processes your two-year residence permit, which can take several additional months.

During this waiting period, you’re legally allowed to live in Portugal. The residence card arrives by mail when approved.

Before the initial two-year permit expires, you renew for a three-year period. Renewal requires demonstrating you’ve maintained your income threshold, spent at least 16 of every 24 months in Portugal, and kept a valid Portuguese NIF (taxpayer number) and bank account.

Where to Live: Portugal by City and Budget

Portugal is not a monolith. Lisbon has gentrified aggressively in the past decade. Porto remains significantly cheaper. The interior is another world — medieval towns where €800 goes further than $4,000 in Boston.

| Location | 1BR Rent/Month | Comfortable Solo Budget | Notes |

|---|---|---|---|

| Lisbon (city center) | €1,200–€1,500 | €1,767/month | Expensive by Portuguese standards, cheap by Western European |

| Porto (city center) | €700–€1,000 | €1,300/month | Strong expat community, lower costs, excellent food and wine scene |

| Algarve (coastal) | €900–€1,400 | €1,500/month | Popular with British and Northern European retirees, warm winters |

| Interior Portugal | €450–€700 | €900–€1,100/month | Towns like Évora, Coimbra, Viseu — slower pace, dramatic savings |

| Silver Coast (Óbidos area) | €600–€950 | €1,200/month | Scenic coastal towns, less tourist pressure than Algarve |

A couple in Porto can live well — good apartment, eating out regularly, healthcare, occasional travel — on €2,000–€2,500 per month. The same lifestyle in San Francisco costs $8,000+. That gap is what drives the geographic arbitrage math for most American D7 applicants.

The Tax Reality: NHR Is Dead. Here’s What Replaces It.

If you’ve done any research on Portugal taxes, you’ve seen the phrase “Non-Habitual Resident” (NHR) everywhere. Ignore most of that content — the NHR program closed to new applicants on December 31, 2023.

What replaced it: the IFICI regime (Incentivo Fiscal à Investigação Científica e Inovação), also called NHR 2.0. IFICI offers a 20% flat tax on Portuguese-source income for 10 years — but it targets researchers, qualified professionals in technology and innovation, teaching, and scientific investigation. Passive income retirees living on pensions and dividends typically do not qualify.

If you can’t access IFICI, you face standard Portuguese income tax rates, which range from 14.5% on income up to €7,703 to 48% on income above €80,882, plus a municipal surtax of up to 1.5%. Portugal does not have wealth taxes. The stamp duty (inheritance tax) is 10% for non-direct family members.

What This Means for Americans

US citizens are taxed on worldwide income regardless of where they live — that doesn’t change when you move to Lisbon. However, the mechanisms available to reduce double taxation are substantial:

- Foreign Tax Credit (FTC): Dollar-for-dollar credit against your US tax liability for taxes paid to Portugal. If you’re paying Portuguese income tax, you credit that against your US bill. Most Americans with passive income in the €920–€3,000/month range end up owing little to nothing in US taxes after applying the FTC.

- Foreign Earned Income Exclusion (FEIE): Excludes up to $126,500 of earned income if you pass the physical presence test. Not useful for passive income retirees, but relevant if you’re also working remotely. See the full FEIE breakdown here.

- US-Portugal Tax Treaty: The two countries have a bilateral tax treaty that addresses double-taxation scenarios on pensions, dividends, and capital gains, though it doesn’t eliminate all US filing obligations.

You will still file a US 1040 annually. If your Portuguese bank account balance ever exceeds $10,000, you file an FBAR. The savings requirement alone — €11,040 — triggers the FBAR immediately. For a complete breakdown of FBAR, FATCA, and US expat tax obligations, see the US expat banking and tax guide.

D7 vs Golden Visa: Which One Is Right for You?

| Factor | D7 Passive Income Visa | Golden Visa (Investment) |

|---|---|---|

| Financial requirement | €920/month passive income | €500,000+ investment |

| Physical presence | 16 months per 2-year period | 7 days/year minimum |

| Income type | Must be passive or remote | Any (investment visa) |

| Upfront cost | ~€90–€175 consulate fee | €500,000+ plus legal fees (~€10k–€20k) |

| Tax residency triggered? | Yes, after 183 days/year | Not necessarily (7 days/year) |

| Citizenship eligibility | 10 years for most nationalities | 10 years for most nationalities |

| Best for | Retirees, remote workers wanting to actually live there | Investors wanting EU optionality without relocating |

If you want to live in Portugal — not just hold a card as insurance — the D7 is the obvious choice. You’re spending your own savings either way; the D7 just doesn’t require you to lock up €500,000 in a Portuguese fund to do it.

Banking and Logistics: What Americans Need Before Leaving

The D7 requires opening a Portuguese bank account. The main options for expats are Millennium BCP, Banco Santander Portugal, and Caixa Geral de Depósitos. Some online fintechs can bridge the gap before you arrive, but most consulates want a traditional Portuguese IBAN for the savings requirement.

For your US-side banking, Charles Schwab’s investor checking account reimburses 100% of ATM fees worldwide — including every Multibanco ATM in Portugal — with no foreign transaction fees. It’s the practical choice for expats pulling euros from ATMs regularly without bleeding money on access fees.

For transferring larger amounts — like funding your required €11,040 savings deposit — Remitly offers competitive USD-to-EUR exchange rates with transparent fees and bank-level transfer security. Run a test transfer before you need to move the full amount.

You’ll also need to maintain a US address for IRS correspondence, brokerage accounts, and banking relationships back home. Most US banks close or freeze accounts when they detect a foreign address on file. A virtual mailbox — like Traveling Mailbox ($15/month, real US street address in 50+ cities, mail scanning and forwarding) — handles all of that from your Lisbon apartment.

The Citizenship Path: What the 10-Year Rule Means in Practice

Portugal’s citizenship timeline extended in 2023. Most non-EU/CPLP (Lusophone) nationals — including Americans — now need 10 years of legal residency before qualifying for naturalization, up from the previous five-year threshold. The practical sequence for an American on a D7:

- Year 0–2: First two-year residence permit

- Year 2–5: First three-year renewal

- Year 5: Apply for permanent residence (this you qualify for after five years; permanent residence doesn’t expire or require renewal)

- Year 10: Apply for Portuguese citizenship and EU passport

A Portuguese passport opens visa-free access to 186 countries and the right to live and work anywhere in all 27 EU member states. That optionality compounds in value with each year of legal residency. The investment in time — not money — is the real cost of the D7 path.

Getting Started: Your D7 Checklist

Six months before applying:

- Order your FBI background check and submit for apostille — the process takes 4–8 weeks minimum

- Open a Portuguese bank account (some banks allow partial remote opening for non-residents)

- Secure accommodation in Portugal: sign a 12-month rental lease or present proof of purchase

- Purchase health insurance covering Portugal for at least 12 months

- Gather 12 months of income documentation: bank statements, pension letters, dividend records

One to two months before your consulate appointment:

- Book your appointment at the nearest Portuguese consulate (slots fill fast — don’t wait)

- Complete and print the D7 visa application form

- Fund your Portuguese bank account with the required €11,040 savings

- Get your NIF (tax identification number) — mandatory for any financial transaction in Portugal; available through some services remotely

After arriving in Portugal:

- Register your address with the local Junta de Freguesia (parish council)

- Book your AIMA biometrics appointment immediately — the queue runs 2–6 months in major cities

- Set up your virtual US mailbox before departure to protect your domestic banking and IRS correspondence

The Bottom Line

The Portugal D7 Visa is one of the clearest residency pathways available to Americans. The income threshold is low enough that a modest Social Security payment often qualifies a single retiree. The cost of living in Porto or interior Portugal makes €920/month stretch further than it has any right to. And the bureaucratic path — while slow at times — is transparent and well-documented without requiring you to park a half-million euros somewhere.

The real caveat: the NHR tax benefit that made Portugal so attractive to foreign retirees no longer exists for new arrivals. You’ll pay standard Portuguese rates on local-source income. Americans should run their numbers through both the Foreign Tax Credit and their specific income structure before assuming the tax picture is clean. It usually works — but verify with a cross-border CPA before signing a Lisbon lease.

If you’re serious about geographic arbitrage, Portugal checks more boxes than almost anywhere else in Western Europe. Here’s how it stacks up against nine other countries worth considering.

Financial Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or immigration advice. Visa requirements, income thresholds, and tax regulations change frequently. Consult a qualified immigration attorney and cross-border tax professional before making any residency or relocation decisions. Income and cost figures cited reflect data available as of the publication date and may not reflect current requirements.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.