The Permanent Establishment Trap Every Remote Expat Faces

11 min read · 2,680 words

There are somewhere between 40 and 80 million digital nomads worldwide right now, and 44% of them are American. Most are blissfully unaware that by working remotely from a foreign country, they may have already created a legal footprint for their U.S. employer — one that could result in six figures of corporate taxes, retroactive penalties, and mandatory payroll registration in a country their company has never stepped foot in.

This isn’t a hypothetical. The OECD updated its Model Tax Convention in November 2025 specifically because cross-border remote work had created enough corporate tax exposure that governments needed a new framework to handle it. The concept is called Permanent Establishment (PE), and it’s the most misunderstood tax risk in the entire expat finance world.

You might personally owe nothing — your foreign income exclusion is intact, your taxes are sorted. But you could still cost your employer hundreds of thousands of dollars just by showing up to your remote job from the wrong country.

What Is Permanent Establishment?

Permanent Establishment is an international tax concept that determines when a foreign business has enough of a presence in a country to be taxed there. Under most bilateral tax treaties (modeled on the OECD framework), a company is subject to corporate tax in a country if it has a “fixed place of business” there — a branch, an office, a factory, a warehouse.

But here’s the part most remote workers don’t read: a home office can qualify as a fixed place of business. Your apartment in Berlin, your rented flat in Lisbon, your Airbnb in Bangkok — if you’re conducting your employer’s business from there with any regularity, tax authorities in some countries will argue that qualifies.

A PE can also arise through a “dependent agent” — someone who habitually concludes contracts on behalf of a company in a foreign country. If you’re a sales rep closing deals in France for a California company, France may argue your employer has a PE in France through you — and that French profits are taxable in France.

Why This Exploded After COVID

Cross-border remote work was a fringe phenomenon before 2020. After it, it became mainstream almost overnight. The OECD issued temporary guidance during the pandemic saying that emergency remote work situations shouldn’t trigger PE — companies weren’t setting up foreign operations, employees were just stuck at home. Fine.

That temporary guidance expired. And since then, tens of millions of employees have continued working abroad permanently or semi-permanently, with their employers often having no idea. Meanwhile, tax authorities in Germany, France, the Netherlands, and elsewhere have been quietly updating their guidance to make clear they view habitual remote work as potentially creating a taxable presence.

The OECD’s November 2025 update to the Model Tax Convention is the most important development in this space since the pandemic. It introduces a two-part test that finally gives employers and employees a framework to assess their risk — while also making clear that some scenarios are definitively in the danger zone.

The OECD’s New 2025 Framework: Two Tests Every Expat Must Know

Test One: The 50% Working Time Benchmark

Under the updated OECD guidance, if an employee works from a foreign home location for less than 50% of their total working time over any 12-month period, that location is generally not considered a “fixed place of business” — no PE. The safe harbor is clear.

If you spend 3 months abroad and 9 months in your home country (or at a company office), you’re almost certainly fine. That 25% threshold puts you well inside the safe zone. But exceed 50% — say, 7 months abroad out of 12 — and the analysis shifts. You’re no longer protected by the benchmark, and you move to the second test.

Test Two: The Commercial Reason Test

This is where the framework gets genuinely complicated. If the 50% threshold is breached, the question becomes: why is the employee working from abroad?

Under the 2025 OECD framework, a commercial reason for the foreign presence must exist for a PE to be created. “Commercial reason” means the employee’s physical presence in that country directly serves the company’s business — serving local clients, accessing regional markets, collaborating with in-country teams, or supporting on-site operations.

Here’s what actually helps remote workers: pure lifestyle reasons do not create a commercial reason. The OECD explicitly states that talent retention, cost savings, and employee preference are not valid commercial reasons. If your company lets you work from Barcelona because you want to live in Barcelona and your job has nothing to do with Spain — you’re less likely to trigger a PE.

But if you’re a sales engineer working with Spanish clients from Madrid? If you’re an account manager whose territory includes France and you’re living in Paris? The commercial reason test probably fails — meaning a PE very likely exists.

The Dependent Agent Trap (The Sneakiest Risk)

Even if your home office doesn’t constitute a “fixed place of business,” a second PE pathway can still catch your employer: the dependent agent rule.

A dependent agent PE arises when an employee habitually exercises authority to conclude contracts on behalf of the company in a foreign country. If you’re routinely signing off on deals, closing sales, or finalizing agreements with local clients — even from a home office — you may qualify as a dependent agent.

This doesn’t require a formal office. It doesn’t require a business registration. It just requires that your job involves concluding commercial transactions in a country where your company isn’t registered.

Sales roles are the highest-risk category by far. Customer success roles with contract authority rank second. Technical roles with no contract authority are generally safe. Understanding where your job falls on this spectrum is non-negotiable for any expat working for a U.S. company.

What a PE Actually Triggers: The Company’s Bill

Here’s why your employer cares so much, even if you don’t personally owe anything. A Permanent Establishment triggers a cascade of obligations:

| Obligation | Details |

|---|---|

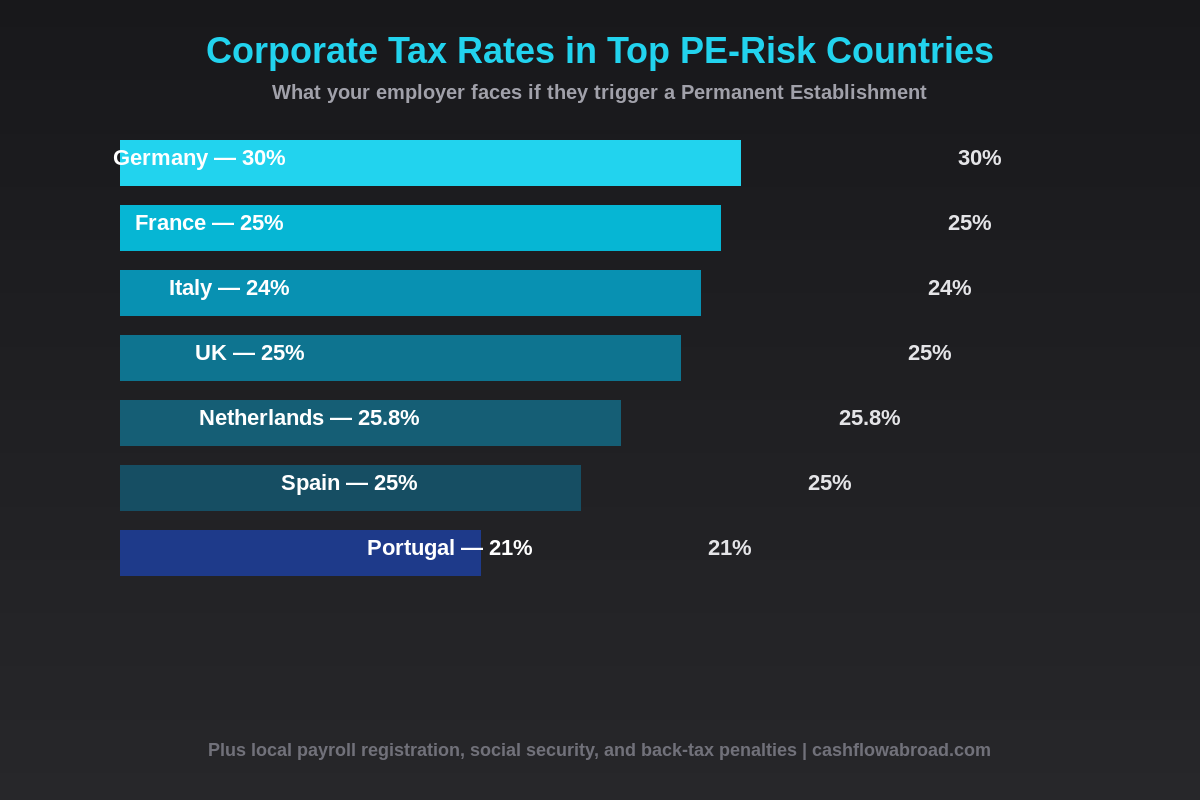

| Corporate Income Tax | The host country claims a portion of company profits. Germany charges ~30% combined (federal + trade tax). France and UK charge 25%. Italy 24%. |

| Local Payroll Registration | The company must register as an employer in the host country and run local payroll under local rules. |

| Employer Social Security | Employer-side social security contributions kick in — often 15–30% of salary on top of base wages, depending on the country. |

| Transfer Pricing Documentation | The company must formally document how profits are allocated between the PE and the parent entity — an expensive compliance exercise. |

| Retroactive Penalties | If a PE is discovered after the fact, the company owes back taxes plus interest plus penalties for every year the PE existed undeclared. |

| Annual Local Tax Filings | Corporate tax returns, local accounting records, and ongoing audit exposure in the host country — in perpetuity while the PE exists. |

For a mid-sized tech company with a $200,000/year employee, a PE discovered three years after the fact could easily result in a bill exceeding $500,000 once back taxes, penalties, and professional fees are factored in — before the cost of ongoing compliance.

Countries with the Most Aggressive PE Enforcement

Not all countries pursue PE claims equally. Here’s the current landscape for the most common expat destinations:

| Country | Corporate Rate | Enforcement Level | Key Risk Factor |

|---|---|---|---|

| Germany | ~30% | Very High | Wage tax withholding applies even without PE; employer registration triggered from day one |

| France | 25% | High | Aggressive audit posture; dependent agent rules interpreted broadly |

| Italy | 24% | High | Establishment rules interpreted aggressively; limited nomad-friendly guidance |

| Netherlands | 25.8% | Moderate-High | Strong treaty network; proactive guidance available but enforcement growing |

| UK | 25% | Moderate | Generally follows OECD model; home office PE low-risk but dependent agent risk is real |

| Spain | 25% | Moderate | Beckham Law holders create additional employer complexity |

| Portugal | 21% | Low-Moderate | High inbound nomad volume; enforcement capacity limited but growing |

| Thailand | 20% | Low | LTR Visa holders typically low risk; enforcement infrastructure limited |

Germany deserves a separate call-out because it’s in a category of its own. German tax law requires wage tax withholding from foreign employers with even a minimal German presence — and that minimal presence can be a single remote employee. Your employer doesn’t need a declared PE; the mere fact of you working from Germany may require them to register as a German employer. This is why many U.S. companies explicitly prohibit employees from working from Germany for more than a few weeks.

How Employers Are Responding — And Why Some Will Fire You

The honest reality is that most U.S. companies have no idea their remote employees have been abroad for 8 months. HR systems don’t track it. Managers don’t ask. The issue only surfaces when something goes wrong — an audit, a whistleblower, an employee dispute that turns ugly.

But companies that are aware are responding in three distinct ways:

Hard prohibitions. Many Fortune 500 firms now have policies explicitly banning extended international remote work — typically anything over 30 or 60 consecutive days. Violating this policy is a fireable offense. Not because they don’t trust you, but because legal has calculated the PE exposure and decided the liability isn’t worth it.

Employer of Record (EOR) services. For companies that want to legitimately support workers in foreign countries, EOR services act as the local employer on paper, absorbing the PE exposure and handling local payroll and compliance. This costs the company roughly 15–20% of an employee’s salary on top of base compensation. If your company is willing to engage an EOR, you’re in the best possible position.

Contractor conversion. Some companies solve the problem by reclassifying employees as independent contractors. This shifts compliance burden to you — you’re now self-employed in your country of residence and responsible for your own taxes and social contributions. Less elegant, but increasingly common for employees who want to live abroad long-term.

If you’re considering working remotely from abroad, an honest conversation with HR or legal before you leave is worth its weight in gold. For more on structuring your U.S. tax situation as an expat, our complete US expat banking and taxes guide covers FBAR, FATCA, and FEIE in full detail.

How to Protect Yourself (And Your Job)

If you’re already working abroad or planning to, here’s what the current framework means in practice:

Stay under 50% of working time in any one foreign country. If you spend less than half your working hours in a given location over a rolling 12-month period, you’re in the OECD safe harbor. Many nomads naturally do this by moving every few months — inadvertent compliance is still compliance.

Know your role’s PE risk profile. No contract-concluding authority and no connection to the local market means low PE risk regardless of location. Sales, legal, and business development roles need much more careful analysis. Get your job description reviewed by a cross-border tax advisor if you’re unsure.

Get it in writing from your employer. If your company approves your remote work abroad, get that approval documented. The documentation should note that you are not establishing a business presence, have no authority to conclude contracts on behalf of the company in that country, and that the arrangement is personal rather than commercially driven. This doesn’t eliminate PE risk, but it creates a paper trail supporting the commercial reason test.

Maintain your U.S. presence properly. A virtual mailbox service like Traveling Mailbox gives you a real U.S. street address for banking, IRS correspondence, state domicile, and employer HR records — $15/month for coverage in 50+ cities with mail scanning and check deposits. Keeping your U.S. address on file with your employer also helps document that your primary work location remains the United States. We covered the full case for a virtual mailbox in our guide to expat virtual mailboxes.

Consider destinations with formal nomad visa PE guidance. Some digital nomad visa programs come with explicit PE guidance for employers — either through bilateral treaty provisions or formal government statements clarifying that nomad visa holders don’t create PE exposure. Our digital nomad visa rankings cover which programs offer the cleanest tax treatment for both workers and their employers.

Encrypt your communications. NordVPN doesn’t affect your PE status, but it does protect work communications from surveillance on foreign networks — a reasonable security baseline when logging in from shared infrastructure in countries with different privacy laws than the U.S.

The Coming Enforcement Wave

PE enforcement has historically been limited by information gaps. Tax authorities in France couldn’t easily determine that an employee of an American company was sitting in a Paris apartment closing deals. That asymmetry is disappearing.

Under frameworks like the Common Reporting Standard (CRS) and the emerging Crypto-Asset Reporting Framework (CARF), financial data is increasingly flowing automatically between tax authorities. Bank accounts, payroll records, and digital transactions are being cross-referenced in ways that weren’t possible five years ago. We wrote in depth about how AI-powered audits and global data sharing are transforming cross-border tax enforcement — PE detection is the logical next frontier for the same infrastructure.

Germany, France, and the Netherlands have all been investing in automated cross-border payroll compliance systems. The question isn’t whether enforcement will intensify — it’s how fast.

Three Scenarios, Three Outcomes

The Nomad Developer (Low Risk). A U.S. software engineer spends 3 months in Portugal, 2 months in Colombia, 2 months in Thailand, and the rest in the U.S. No local client relationships, no contract authority, work has no connection to any of those markets. Under the 50% rule, no single country exceeds the threshold. Under the commercial reason test, no commercial rationale for any foreign presence exists. PE risk: very low.

The Germany-Based Account Manager (High Risk). A U.S. sales account manager moves to Berlin with his company’s informal approval. He manages European accounts, negotiates contracts, and closes deals with clients in Germany and the Netherlands. He’s been there 10 months. He clearly exceeds the 50% threshold. He clearly has a commercial reason for being in Germany. He has contract-concluding authority. PE risk: very high. His employer almost certainly has an undeclared PE in Germany and a significant retroactive liability building by the month.

The Spain-Based Marketer (Low-Moderate Risk). A U.S. content marketer lives in Seville under Spain’s Beckham Law. She creates materials for a U.S. audience with no Spanish client interaction and no contract authority. She spends 9 months in Spain and 3 months in the U.S. She exceeds the 50% threshold, but arguably fails the commercial reason test — her presence in Spain serves no commercial purpose for the company. PE risk: low-to-moderate. Spain may disagree, but the OECD framework supports her position.

The Bottom Line

Permanent Establishment is the tax risk almost nobody talks about because it falls in an awkward gap: it’s technically your employer’s problem, not yours. But that’s exactly why it can blow up your remote work arrangement without warning. Companies that discover undisclosed PE exposure don’t negotiate timeline or transition periods — they terminate the arrangement immediately to stop the bleeding.

The OECD’s 2025 framework is the clearest guidance the international tax community has ever had on this issue. The 50% working time safe harbor is real and meaningful. But it’s not a universal guarantee, and it won’t protect you in countries that choose to interpret their own laws aggressively regardless of OECD recommendations.

If you’re building an expat life around remote work for a U.S. employer, understanding PE basics is now a core competency. The 50% rule is your first line of defense. The commercial reason test is where the nuance lives. And a proactive conversation with your employer’s legal team is worth far more than any amount of hope that nobody will notice.

For the full picture on managing U.S. taxes as an expat — including how to use the FEIE and foreign tax credit correctly so you’re not also creating personal tax problems on top of employer ones — see our guide to paying zero federal income tax as a US expat.

Financial and Legal Disclaimer: This article is for informational and educational purposes only and does not constitute legal, tax, or financial advice. Permanent Establishment rules are highly jurisdiction-specific and depend on facts and circumstances of each individual situation, applicable tax treaties between countries, your employer’s corporate structure, and local law interpretations. Consult a qualified international tax attorney and your employer’s legal counsel before making any decisions about cross-border remote work arrangements. Affiliate links in this article may earn a commission at no additional cost to you.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.