How Expats Keep Their US Credit Score Alive Abroad

8 min read · 1,977 words

Most American expats spend months planning their move abroad — the visa, the apartment, the bank transfer. Almost none of them think about their FICO score. Then, two years in, they try to refinance a US property or co-sign a loan for a family member and discover their 790 credit score has quietly rotted to 620. Not because they missed payments. Because nobody told them that credit bureaus treat inactivity the same way they treat delinquency.

This is the expat credit trap, and it catches people who are otherwise financially sophisticated. Here’s everything you need to know to keep your US credit profile healthy — whether you’re gone for two years or twenty.

Why Your US Credit Score Still Matters Abroad

The instinct when moving abroad is to mentally separate from US financial infrastructure. That instinct is wrong — at least if you ever plan to return, own US property, or access US financial products again.

A strong credit profile is the gate to:

- US mortgage financing — foreign income increasingly qualifies with the right lender, but credit score minimums haven’t changed

- Business credit lines — if your online business is US-incorporated (and for tax reasons, many are), lenders pull your personal credit

- Card upgrades and limit increases — which directly affect your utilization ratio, which affects your score

- Returning home — the landlord running your rental application doesn’t care that you spent five years in Medellín

There’s also a less obvious reason: your US banking stack depends on it. Banks close accounts they consider dormant or low-value. A high credit score signals financial seriousness and reduces the odds of losing access to accounts you need for FBAR compliance and tax filing.

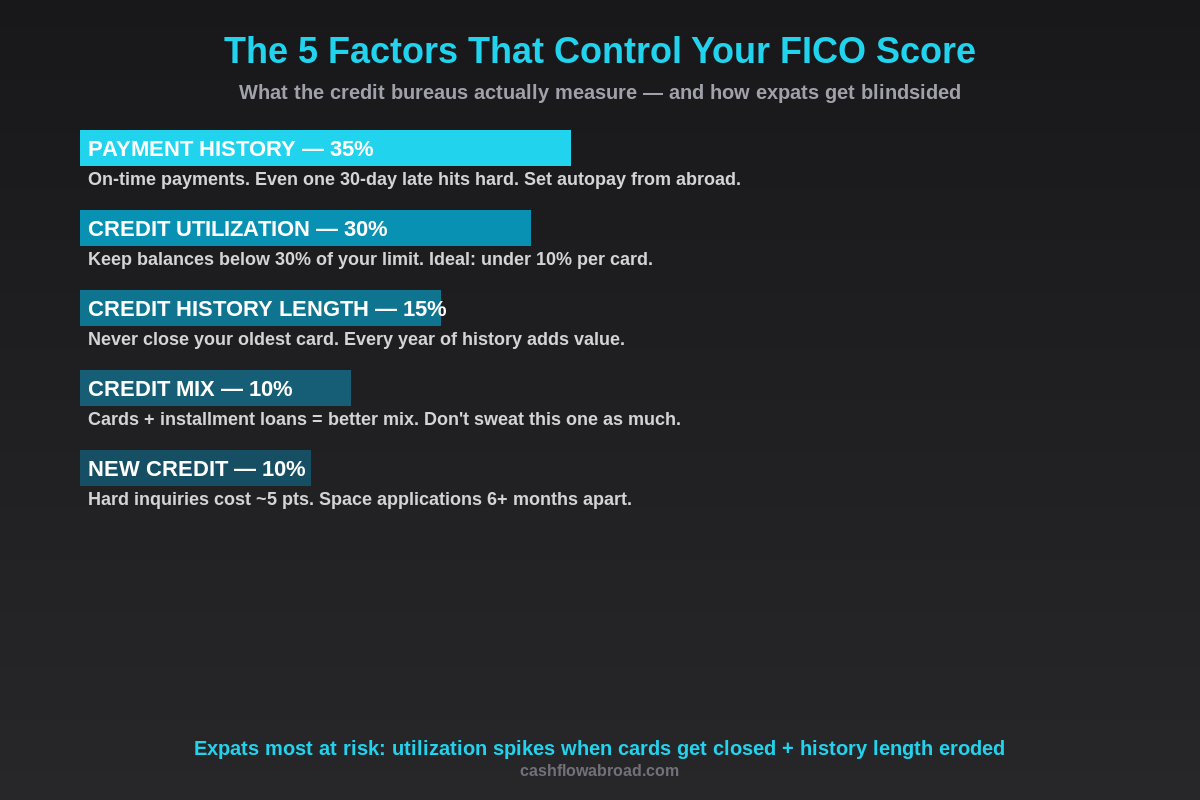

The Five FICO Factors — And Which Ones Wreck Expats

FICO scores run on five components. Expats face specific vulnerabilities in three of them:

| Factor | Weight | Expat Risk Level | Why |

|---|---|---|---|

| Payment History | 35% | Medium | Easy to miss a bill when you’re 8 time zones off |

| Credit Utilization | 30% | High | Cards get closed, shrinking your total limit and spiking your ratio |

| Credit History Length | 15% | High | Closed cards eventually drop off your report entirely |

| Credit Mix | 10% | Low | Passive — doesn’t change unless you open or close accounts |

| New Credit | 10% | Low | Rarely an issue unless you’re applying for new credit while abroad |

The utilization trap is the sneakiest. Say you have three cards with a combined $30,000 limit and carry $4,000 in balances — a healthy 13% utilization. Your bank closes two of those cards for inactivity. Suddenly your available credit drops to $8,000 and your utilization hits 50%. That single event can drop your score 80–100 points, sometimes overnight.

The Inactivity Death Spiral

Credit card issuers can and do close accounts for inactivity — and the threshold is lower than most people realize. Some issuers trigger a closure review after as little as three to six months of no activity. They don’t always warn you. You find out when you try to use the card and it declines.

The chain reaction looks like this:

- You stop using your American Express after moving to Thailand

- AmEx closes the card after 12 months of inactivity

- Your available credit drops by $15,000

- Your utilization ratio spikes from 8% to 34%

- Your score drops 60–90 points in the next reporting cycle

- That closed account stays on your report for 10 years — but its positive history eventually ages off

The fix is almost comically simple: use the card for something small every month. A $5 Netflix subscription. A recurring Spotify charge. The account stays alive, the positive history accumulates, and your utilization stays where you want it.

The Mailing Address Problem

Every US financial institution wants a US mailing address. When you move abroad, this creates a tangle: update your address to a foreign one, and some banks will close your account on compliance grounds. Keep a US address, and you need something that actually receives and forwards your mail.

A virtual mailbox service solves this cleanly. Traveling Mailbox gives you a real US street address in 50+ cities — not a P.O. box, which many banks reject — for around $15/month. They scan incoming mail so you see it immediately, and can forward physical items or deposit checks on your behalf.

This matters beyond just keeping cards alive. The IRS requires a valid mailing address for correspondence. The FBAR system (FinCEN 114) requires one. State domicile questions — which affect whether you owe state income tax — often hinge on the address on file with your bank. A virtual mailbox keeps all of that clean with minimal ongoing effort.

The Banking Stack That Protects Your Score

Getting this right means choosing US financial institutions that won’t punish you for living abroad. Most big retail banks fail this test — they close accounts, add foreign transaction fees, and generally treat expats as compliance problems. Two institutions that don’t:

Charles Schwab: The Expat Default

Charles Schwab is the most universally recommended bank for US expats, and for good reason. The Schwab Bank Visa Platinum debit card charges zero foreign transaction fees, zero currency conversion fees, and reimburses all ATM fees worldwide — every month, no cap. The brokerage account requires no minimum balance and lets you manage US investments from anywhere.

Critically, Schwab doesn’t close accounts because you’re living abroad. They understand that their customer base includes a significant expat segment. Keeping your brokerage and checking at Schwab gives you a stable US financial anchor that won’t disappear. That said, a debit card doesn’t build credit — for score purposes, you still need at least one active revolving credit card running alongside your Schwab account.

Mercury: For Business Banking

If you run a US LLC or corporation from abroad — and many expats do for tax efficiency — Mercury is the cleanest business banking layer available. No fees, no minimum balance, excellent API access, and no friction about the account holder being internationally based. Business banking history doesn’t feed directly into personal FICO, but a stable US business account strengthens the overall financial picture lenders see when you need financing.

The Active Cards Strategy

Expat financial advisors consistently recommend maintaining two to three active revolving credit accounts to keep your credit profile alive. The goal isn’t volume — it’s available credit versus utilized credit. A practical setup:

- 1–2 travel rewards credit cards — Chase Sapphire, Amex Gold, or similar. Put one small recurring subscription on each. Pay in full every month via autopay.

- 1 no-fee cash-back card — Useful as a backup and adds to total available credit, keeping utilization low

- Schwab checking — Day-to-day spending abroad; unlimited ATM rebates worldwide

The arithmetic matters. A $25,000 combined credit limit with $1,500 in monthly charges paid in full gives you 6% utilization. That’s excellent. Drop that limit to $8,000 through card closures with the same spending, and you’re at 19% — still okay, but you’ve lost headroom.

Autopay Is Not Optional

Payment history is 35% of your FICO score — the single largest factor. One missed payment can cost you 60–110 points depending on your starting score. The higher your score, the more a single delinquency hurts, because the model assumes high scorers don’t miss payments.

When you’re managing US accounts from abroad, time zone differences and the cognitive load of international life mean manual bill payment is a disaster waiting to happen. Set every US account to autopay the full statement balance, not the minimum. Then add email and SMS alerts for each card so you know when payments process.

Check your autopay settings every six months. Banks silently reset autopay configurations when they reissue card numbers after a fraud incident. You won’t know until a payment bounces and your score takes the hit.

Utilization Tricks That Actually Work

Pay before the statement closes, not the due date. FICO models snapshot your balance at the statement date. Pay down a $4,000 balance to $500 two days before the statement generates, and you report 2% utilization instead of 25%. This single habit can shift your score 20–40 points month to month.

Request credit limit increases before you move. Higher limits mean lower utilization on the same spending. Most premium cards will grant increases after 12+ months of on-time payments. Do this while you’re still a US resident — easier to approve when you can verify income against domestic tax returns.

Call and tell them you’re moving internationally. Proactively informing your card issuers that you’re relocating often prevents the account closures and fraud flags that catch expats off guard. Banks close accounts without warning when transactions suddenly appear in foreign countries. A 10-minute call before you leave removes that risk.

Monitoring Your Credit From Abroad

Pull your credit report at least twice a year via AnnualCreditReport.com — free access to Equifax, Experian, and TransUnion. Weekly free reports are available now (a COVID-era policy that became permanent). What to look for:

- Accounts closed without your knowledge

- Hard inquiries you didn’t authorize — a common sign of identity theft

- Payment history errors — banks do misreport, and the dispute process is easier than recovering from months of apparent delinquency

- Individual card utilization, not just the aggregate number

Identity theft runs disproportionately high among expats because mail forwarding creates gaps in address verification. Real-time credit monitoring alerts from Experian or Credit Karma are worth setting up — free, and they notify you of changes immediately, which matters more when you’re not physically around to catch problems early.

Foreign Credit Scores: Starting From Zero

Your US FICO score does not transfer abroad. Every country runs its own credit system, and most don’t recognize US data. In Canada, the UK, and Australia, you start with a blank file when you arrive — which is genuinely frustrating if you have 20 years of spotless US credit history.

| Country | Credit System | Time to Establish | Notes |

|---|---|---|---|

| United Kingdom | Experian UK, Equifax UK, TransUnion | 12–24 months | US history not recognized; need UK address and registered voter roll |

| Canada | Equifax Canada, TransUnion Canada | 6–18 months | Secured cards readily available for newcomers |

| Mexico | Buró de Crédito | 12+ months | Requires RFC (tax ID) and local bank account first |

| UAE | Al Etihad Credit Bureau | 3–6 months | Fast to establish if you have a salary-deposit bank account |

| Germany | Schufa | 6–12 months | Landlords require Schufa reports; establish this early |

| Australia | Equifax Australia, Experian AU | 6–12 months | Secured cards and credit builder loans available |

For long stays, building local credit is worth the effort — especially in countries where landlords, employers, or telecom providers run credit checks. It doesn’t replace maintaining your US profile; it runs in parallel. See the geographic arbitrage playbook for financial setup details by country.

The One Case Where Letting It Slide Makes Sense

If you’re pursuing US citizenship renunciation — which some long-term expats do for tax simplicity — your FICO score becomes irrelevant once you surrender your passport. The exit tax implications are substantial and worth modeling carefully before that decision. But if you’ve made it, the credit maintenance calculus changes entirely.

For everyone else planning to maintain US ties — property, family, future return, or just the optionality — 30 minutes a month of credit hygiene is among the cheapest forms of financial insurance available.

Put the System on Autopilot

A strong FICO score took years to build. The system that protects it is simple: a virtual mailbox for your US address, a Schwab account as your banking anchor, autopay on every US card, and small recurring subscriptions keeping each card alive. Total cost: maybe $20/month. Total ongoing effort: 30 minutes a month to scan statements and confirm payments processed.

The expats who get blindsided are the ones who assume their credit score will maintain itself. It won’t. But once the system is set up, it runs quietly in the background while you focus on what actually matters — building a life and wealth on your own terms. For the full financial picture, see the FEIE zero-tax strategy and expat investing playbook.

Financial Disclaimer: This post is for informational and educational purposes only and does not constitute financial, legal, or tax advice. Credit scoring models, bank policies, and financial regulations change frequently and vary by institution. Consult a qualified financial advisor or credit specialist before making decisions about your credit profile, banking relationships, or financial planning as a US expat living abroad.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.