The Self-Employment Tax Trap Every Expat Freelancer Faces

You researched FEIE. You filed Form 2555. Then your accountant sent the final return — and there was a $20,335 bill sitting at the bottom.

You researched FEIE. You filed Form 2555. Then your accountant sent the final return — and there was a $20,335 bill sitting at the bottom.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

You researched FEIE. You filed Form 2555. You excluded every dollar of foreign earned income up to the $132,900 limit and owed exactly $0 in federal income tax. Then your accountant sent the final return — and there was a $20,335 bill sitting at the bottom.

That's self-employment tax. And it's the line item that blindsides more expat freelancers, consultants, and online entrepreneurs than any other. The FEIE is real and it works — but it has a blind spot the size of a truck: it exempts you from income tax, not self-employment tax.

The IRS treats self-employment tax as a funding mechanism for Social Security and Medicare, separate from income tax entirely. So it doesn't matter that you're living in Chiang Mai or Medellín or Lisbon. If you're self-employed and a US citizen, that 15.3% clock is running on every dollar of net profit up to $176,100 — unless you know exactly which structures and locations make it disappear.

Related: FEIE zero tax guide

What Self-Employment Tax Actually Is (And Why FEIE Can't Touch It)

When you work for an employer, FICA taxes get split down the middle: you pay 7.65% and your employer pays the other 7.65%. When you're self-employed, you're both employer and employee. That's the full 15.3%: 12.4% Social Security on income up to $176,100, plus 2.9% Medicare with no ceiling.

Here's what that looks like in real dollars at common income levels for 2026:

| Net Self-Employment Income | SE Tax Owed | Federal Income Tax (with FEIE) | Total US Tax Bill |

|---|---|---|---|

| $50,000 | $7,650 | $0 | $7,650 |

| $80,000 | $12,240 | $0 | $12,240 |

| $100,000 | $15,300 | $0 | $15,300 |

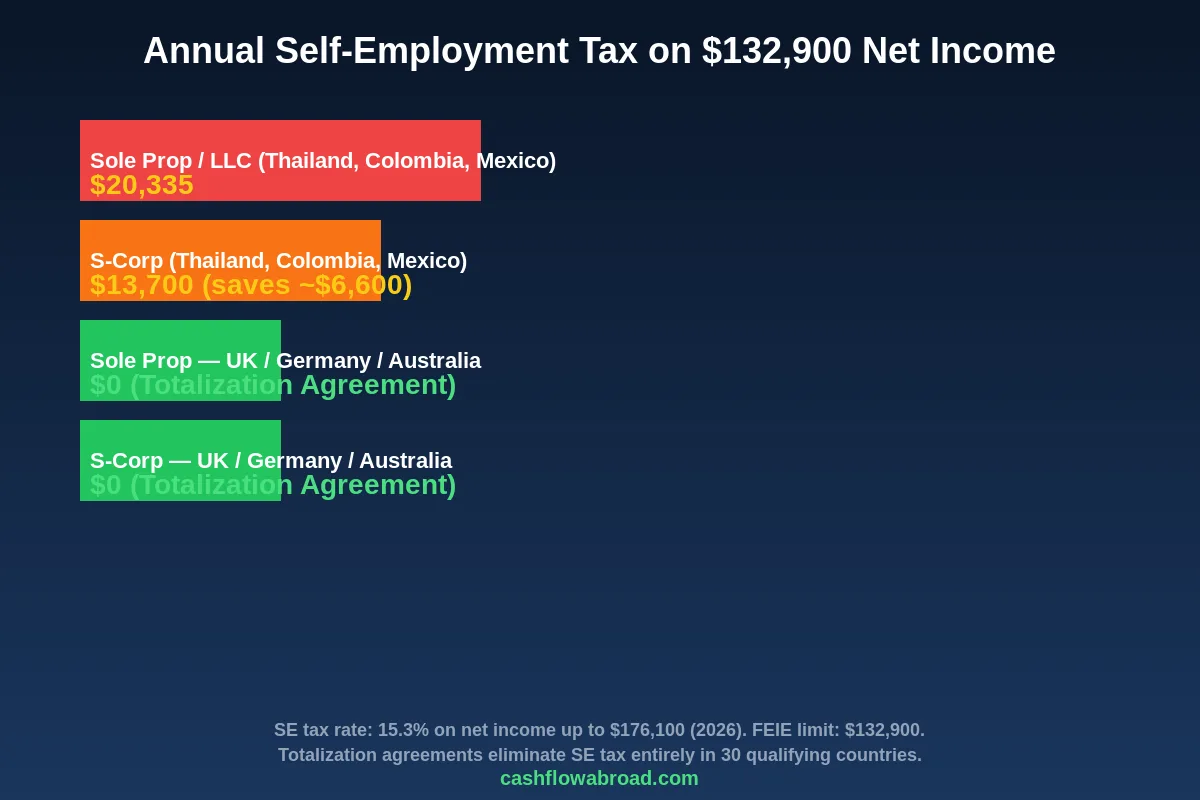

| $132,900 | $20,335 | $0 | $20,335 |

| $200,000 | $26,943 | Varies above FEIE limit | $26,943+ |

There's a small offset: you can deduct half of SE tax from your gross income, representing the "employer-equivalent" half. For US-based workers this reduces their income tax meaningfully. For expats using FEIE to zero out income tax anyway, this deduction helps much less — you're already at $0 income tax, so the deduction is partially wasted.

The counterintuitive reality: an expat freelancer earning $100,000 net can legally owe zero in federal income tax while still cutting the IRS a $15,300 check. Every year. Whether they're in Portugal, Panama, or the Philippines.

Our guide on how US expats pay zero federal income tax legally covers the FEIE mechanics in full — but this is the half of the story that guide doesn't tell.

The Totalization Agreement Arbitrage: The $20K Legal Exemption Nobody Leads With

Here is the escape hatch most expat CPAs don't open with: if you live in one of the 30 countries that have a totalization agreement with the United States, you may owe zero self-employment tax. Not reduced. Not discounted. Zero.

Totalization agreements are bilateral treaties designed to prevent double-taxation of Social Security contributions. The logic: you shouldn't have to fund two countries' retirement systems at the same time. If you're paying into a foreign country's social security system, the US cannot simultaneously collect SE tax from you.

The mechanism: you obtain a Certificate of Coverage from the foreign country's social security authority, attach it to your US return, and your SE tax obligation drops to $0 for as long as you're covered under that foreign system. No special election required beyond getting the certificate and filing correctly.

Countries with US totalization agreements (2026): Australia, Austria, Belgium, Brazil, Canada, Chile, Czech Republic, Denmark, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Japan, Luxembourg, Netherlands, Norway, Poland, Portugal, Slovakia, Slovenia, South Korea, Spain, Sweden, Switzerland, United Kingdom, Uruguay.

Notice who's missing: Mexico, Colombia, Thailand, Indonesia, Panama, Georgia, Paraguay, Ecuador, Vietnam. These are among the most popular expat destinations on earth. If you're freelancing from Medellín or Mexico City, the full 15.3% SE tax still applies, regardless of how long you've lived there.

This creates a real, quantifiable arbitrage based purely on country of residence. A freelance developer earning $132,900 net, living in Germany:

Related: five-flag strategy guide

- SE tax: $0 (totalization agreement + Certificate of Coverage)

- Federal income tax: $0 (FEIE)

- Total US tax: $0

Same developer, same income, living in Chiang Mai:

- SE tax: $20,335

- Federal income tax: $0 (FEIE)

- Total US tax: $20,335

Over a 10-year expat career, that's a $200,000 difference based entirely on which country you chose to live in. Not lifestyle. Not exchange rates. Just a treaty list.

The S-Corp Strategy: Real Savings, Real Caveats

If you're in a non-totalization country, the next tool is the S-Corporation election. It won't eliminate SE tax — but it can meaningfully reduce the base it applies to.

Here's the mechanics: as a sole proprietor or single-member LLC, 100% of your net profit flows to Schedule SE. With an S-Corp, you split income into two buckets:

- W-2 salary: Subject to full payroll taxes (15.3%). This salary qualifies as earned income for FEIE purposes.

- S-Corp distributions: No SE tax. But — critical for expats — distributions do not count as earned income and do not qualify for the FEIE exclusion.

The IRS requires you to pay yourself "reasonable compensation" for work performed — you can't set salary at $1 and take everything as distributions. For knowledge workers and consultants, most expat CPAs recommend salary of at least $60,000–$80,000 at lower income levels, scaling up with income.

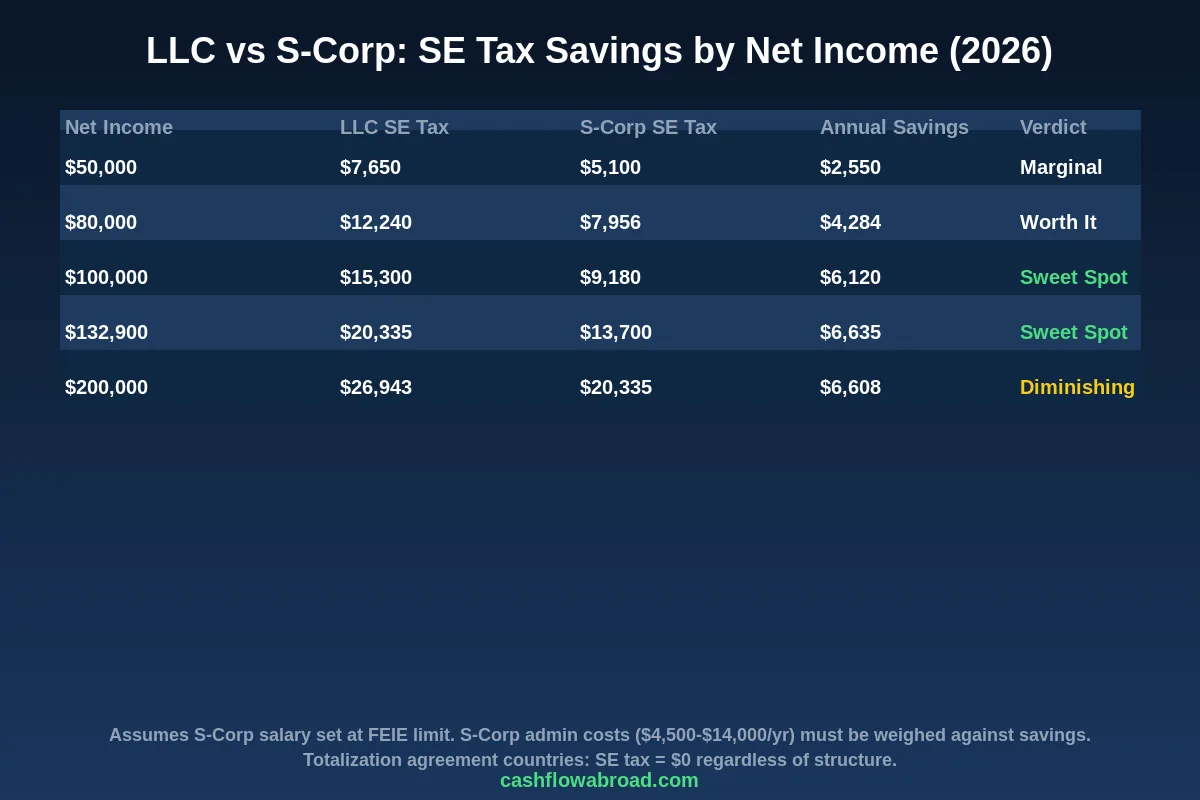

The savings at different income levels, assuming reasonable salary set at FEIE limit where possible:

| Net Income | LLC SE Tax | S-Corp SE Tax | Gross Savings | After Admin Costs ($5K/yr) |

|---|---|---|---|---|

| $50,000 | $7,650 | $5,100 | $2,550 | -$2,450 (worse) |

| $80,000 | $12,240 | $7,956 | $4,284 | -$716 (worse) |

| $100,000 | $15,300 | $9,180 | $6,120 | $1,120 |

| $132,900 | $20,335 | $13,700 | $6,635 | $1,635 |

| $200,000 | $26,943 | $15,300 | $11,643 | $6,643 |

The break-even point sits around $90,000–$100,000 in net income, depending on what your CPA and payroll provider charge for S-Corp complexity. Below that threshold, the administrative overhead typically cancels the tax savings. Above $150,000, the S-Corp almost always makes sense in a non-totalization country.

When the S-Corp Backfires for Expats

Domestic tax advisors routinely recommend S-Corps for self-employed people making over $50,000. For expats, this recommendation requires heavy caveats — and in some cases, the S-Corp structure produces worse outcomes than a simple sole proprietorship.

The distribution trap in detail: Any income taken as an S-Corp distribution is passive/investment income by IRS definition. It does not qualify for FEIE. If you set a low salary to minimize payroll taxes, you're also shrinking your FEIE-eligible earned income bucket — potentially creating a taxable residue that wouldn't exist with a sole prop structure.

Concrete example: $100,000 net income, S-Corp salary set at $40,000 to minimize SE tax.

- FEIE covers $40,000 salary: $0 income tax on salary ✓

- $60,000 distribution: not earned income, taxable at ordinary rates after standard deduction

- $60,000 − $15,000 standard deduction = $45,000 taxable at ~12–22%: roughly $5,000–$7,000 federal income tax

- SE tax on $40,000 salary: $6,120

- Total: $11,000–$13,000

Same person, sole proprietor:

Related: complete FBAR and FATCA guide

- SE tax on $100,000: $15,300

- Income tax: $0 (full FEIE)

- Total: $15,300

The S-Corp still wins in this scenario — but the margin narrows significantly, and once you account for $4,500–$14,000 in annual S-Corp admin costs (payroll processing plus CPA complexity), it can flip negative.

The cleanest expat S-Corp scenario: net income significantly above the FEIE limit, salary set at exactly the FEIE limit ($132,900 in 2026) to maximize earned income exclusion, excess taken as distributions with minimal income tax after the standard deduction or foreign tax credits.

Stacking the Solo 401(k) on Top

Here's where S-Corp strategy gets genuinely powerful for expats with higher income. S-Corp owners can contribute to a Solo 401(k) — up to $70,000 per year in 2026 ($77,500 if you're 50+) — based on their W-2 salary.

For an expat earning $200,000 net in a non-totalization country, with S-Corp salary set at $132,900:

- FEIE excludes $132,900 salary → $0 income tax on salary

- Contribute $70,000 of that salary to Solo 401(k) → $70,000 sheltered from current taxation

- $67,100 taken as distribution → taxable, but potentially offset by foreign tax credits

- SE tax on $132,900: $20,335 (same as sole prop at FEIE limit)

The 401(k) stacking changes the long-term math dramatically. $70,000/year growing at 7% for 20 years compounds to approximately $2.87 million — tax-deferred, growing inside a structure that didn't exist as an option for a simple sole proprietor in a non-totalization country trying to minimize SE tax by putting all income on Schedule SE.

For the broader picture of expat investing and what structures to use for retirement accounts abroad, see our Expat Investor's Playbook.

Your S-Corp Needs a Real US Address — Here's the Cheapest Fix

An S-Corporation must be registered in a US state and maintain a registered agent with a physical US street address. If you've given up your US apartment, this creates an immediate logistical problem.

A virtual mailbox like Traveling Mailbox provides a real street address (not a PO Box) in 50+ US cities, scans all incoming mail to a secure portal, and handles check deposits — starting at $15/month. It's the cheapest line item in your entire expat tax infrastructure, and without it, maintaining a legitimate S-Corp from abroad gets messy fast. (Full disclosure: this is what I personally use.)

State of incorporation matters too. Wyoming, Delaware, and Nevada have no state income tax and minimal LLC/S-Corp annual fees. Forming your S-Corp in your old home state of California or New York — where state tax authorities aggressively pursue former residents — can add 5–13% in state income tax on top of everything else. If you're forming a new entity, pick a favorable state and establish domicile there properly before leaving. Our virtual mailbox guide covers state domicile selection in detail.

Banking for Your S-Corp From Abroad

An S-Corp requires a separate business bank account — commingling personal and business funds risks the IRS reclassifying your distributions as salary, negating the entire SE tax reduction strategy. Opening a US business account from abroad is notoriously difficult with traditional banks that require in-person branch visits.

Mercury is built for this: US-based fintech business banking with fully remote account opening, no monthly fees, and no physical branch requirement. It accepts newly formed LLCs and S-Corps without a branch visit. Pair it with a Charles Schwab international checking account for your personal finances — Schwab refunds all foreign ATM fees worldwide, making it the cleanest US banking setup for expats who need to withdraw local currency anywhere.

Related: running a US business from abroad

Our full US Expat Banking and Taxes guide covers the complete stack: accounts, FBAR reporting, FATCA obligations, and how to stay compliant across multiple banking relationships while living abroad.

The Decision Framework: Which Structure Is Right for You

Work through this in order:

Step 1: Check the totalization agreement list. Is your country on it? If yes, get a Certificate of Coverage from the local social security authority. File it with your return. Your SE tax goes to $0. Structure becomes a secondary question because you're eliminating the tax entirely, not optimizing around it.

Step 2: If you're in a non-totalization country, assess net income.

- Under $80,000: Sole prop or SMLLC. Admin costs eat the savings at this income level.

- $80,000–$100,000: Run the specific numbers. Depends heavily on accountant fees.

- $100,000–$150,000: S-Corp typically works. Model the FEIE/distribution interaction.

- $150,000+: S-Corp almost certainly the right call, especially paired with Solo 401(k) stacking.

Step 3: Model the FEIE and distribution interaction explicitly. Ask your CPA to show you total tax (SE tax + income tax) under both sole prop and S-Corp structures, with the FEIE coverage on salary versus taxability of distributions laid out clearly. Any advisor who gives you an S-Corp recommendation without this analysis doesn't specialize in expat taxation.

Step 4: Factor in real admin costs. Payroll processing (Gusto, ADP): $600–$1,200/year. S-Corp tax return (Form 1120-S): adds $2,000–$10,000 to your CPA bill. Total annual overhead: $3,000–$12,000 before any savings. Make sure the math clears this bar before committing.

Step 5: Consider your country timeline. If you're planning to move to a UK, Germany, or Australia within two years, setting up an S-Corp now — only to dissolve it when totalization eliminates your SE tax entirely — may not be worth the setup costs.

Key 2026 Numbers

| Item | 2026 Figure |

|---|---|

| FEIE exclusion limit | $132,900 |

| Housing exclusion limit | $39,870 |

| SE tax rate (net income ≤ $176,100) | 15.3% (12.4% SS + 2.9% Medicare) |

| SE tax rate (net income > $176,100) | 2.9% (Medicare only) |

| Solo 401(k) max contribution | $70,000 ($77,500 if age 50+) |

| Totalization agreement countries | 30 |

| SE tax on $132,900 (no agreement) | $20,335 |

| SE tax on $132,900 (with agreement) | $0 |

The Bottom Line

The FEIE is the most powerful tax tool available to US expats — and by design, it's incomplete. Self-employment tax exists in a separate statutory bucket from income tax, and Form 2555 cannot reach it. That's not a bug to complain about; it's a structural constraint to plan around.

Your two real options: move to a totalization agreement country and eliminate SE tax entirely through proper filing, or implement an S-Corp structure carefully calibrated to the FEIE/distribution interaction and Solo 401(k) stacking. Neither path is plug-and-play. Both require a CPA who specializes in expat tax — not just any practitioner who's seen a foreign income form once.

The expats who get this right don't save $6,000 a year. Over a 15-year expat career at $150,000+ net income, the compounded difference between an optimized SE tax strategy and the default — just using FEIE and ignoring the SE tax bill — can exceed $300,000. That's the number worth thinking about.

For more on managing the full picture of running a US business while living abroad, see our guide on how to run a US business from Colombia — covering LLC structure, CFC rules, local labor law, and what the Colombian tax authority may or may not care about.

Disclaimer: This article is for informational and educational purposes only and does not constitute tax or legal advice. Tax rules change frequently and vary based on individual circumstances, country of residence, and treaty positions. The interaction between FEIE, self-employment tax, S-Corp elections, and totalization agreements is complex — consult a qualified CPA or tax attorney who specializes in US expat taxation before making structural decisions about your business. Nothing in this post should be relied upon as professional tax advice.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJuly 4, 2026

Expat Tax & FinanceJuly 4, 2026

Canadian TFSA and US Taxes: The Reporting Trap

US citizens holding a Canadian TFSA owe tax on all annual growth and must file Form 3520 — PFIC rules apply to Canadian mutual funds inside the

Expat Tax & FinanceJuly 4, 2026

Expat Tax & FinanceJuly 4, 2026

State Income Tax for Expats: Which States Follow You

California, New York, and Virginia keep taxing Americans abroad. Learn which states follow you, what triggers audits, and how to exit cleanly.

Expat Tax & FinanceJuly 3, 2026

Expat Tax & FinanceJuly 3, 2026

FBAR: The $10,000 Expat Rule Most People Get Wrong

FBAR: when any foreign account aggregate hits $10,000 during the year, all accounts must be reported. Penalties, Bittner ruling, and catch-up