The Foreign Company Tax Trap Every US Expat Must Know

10 min read · 2,540 words

Most US expats who set up a foreign company believe they’ve found the ultimate tax hack: earn profits offshore, keep them inside the local entity, and stay out of the IRS’s reach. That assumption is wrong — and it costs expat business owners tens of thousands of dollars every year.

The mechanism that destroys this strategy is called GILTI — Global Intangible Low-Taxed Income — now officially renamed NCTI (Net CFC Tested Income) under the One Big Beautiful Bill Act (OBBBA), effective January 1, 2026. Under NCTI, the IRS taxes your share of foreign corporation profits at an effective rate of 12.6% — even if you never paid yourself a dollar, even if the money never crossed a border, and even if your local tax rate is zero.

This isn’t a corner case targeting multinationals. It hits any US person who owns 10%+ of a foreign company. And most expat business owners have no idea it applies to them until they get the bill.

What NCTI (Formerly GILTI) Actually Is

GILTI was created by the 2017 Tax Cuts and Jobs Act as an anti-abuse provision targeting US multinationals that shifted intellectual property profits to zero-tax jurisdictions. But the rules don’t distinguish between a Fortune 500 company and a freelance developer running a Colombian SAS. If you’re a US shareholder in a Controlled Foreign Corporation (CFC), the rules apply to you.

Starting January 1, 2026, the OBBBA renamed GILTI to NCTI and made several structural changes — but the core mechanic is unchanged: every year, you must include your proportionate share of your foreign corporation’s net income in your US taxable income, regardless of whether any distribution was made. The profit just sitting in your foreign bank account is taxable to you personally in the year it’s earned.

The key changes under NCTI for 2026:

- Section 250 deduction drops from 50% to 40% — effective US rate rises from 10.5% to 12.6%

- The 10% QBAI (qualified business asset investment) routine return subtraction is eliminated — previously, a 10% return on tangible assets was carved out; now 100% of profits are included in the base

- Foreign tax credit haircut reduced from 20% to 10% — 90% of foreign taxes paid on NCTI income can offset US liability (up from 80%)

- NCTI now applies to shareholders who own CFC stock at any point during the year, not only on the last day

Who Gets Hit: The CFC Trigger

The NCTI trap only activates if your foreign company qualifies as a Controlled Foreign Corporation (CFC):

- A non-US corporation where US persons collectively own more than 50% of voting power or value

- You personally must own 10% or more to be a “US shareholder” subject to NCTI

- Attribution rules apply — ownership through spouses, parents, children, trusts, and other entities counts toward your threshold

Translation: if you own 100% of your Estonian OÜ, Georgian LLC, Colombian SAS, Dubai FZCO, or any other foreign business entity, you have a CFC. Every dollar of profit that sits in that company at year-end is potentially subject to NCTI.

Note that Subpart F income — passive income like dividends, interest, and royalties earned inside the CFC — is calculated separately and can also flow up to you as ordinary income. Subpart F is calculated first; whatever net income remains is the pool from which NCTI is drawn. The two regimes are sequential, not overlapping.

How NCTI Is Calculated: A Real Example

A concrete scenario. You run a 100%-owned foreign consulting company (a CFC) in Georgia (the country), which has a 1% flat tax on turnover. Your company earns $200,000 in net profit in 2026. You pay local taxes of $2,000. You take no salary and make no distributions.

Under NCTI with a Section 962 election:

| Step | Amount |

|---|---|

| Net CFC tested income (NCTI inclusion) | $200,000 |

| Section 250 deduction (40%) | −$80,000 |

| Taxable NCTI income | $120,000 |

| US corporate-rate tax at 21% | $25,200 |

| Foreign tax credit: $2,000 × 90% | −$1,800 |

| Net US NCTI tax owed | $23,400 |

You owe $23,400 to the IRS on money that never left your Georgian bank account and that you never touched personally. That’s the trap. And in 2026, without the QBAI carve-out, even manufacturing and service companies with heavy tangible asset bases get the full inclusion — there’s no partial shelter for owning equipment or real property inside the CFC anymore.

What the OBBBA Changed in 2026

The One Big Beautiful Bill Act made NCTI more expensive in key ways, but also improved the foreign tax credit treatment. Here’s the full before-and-after:

| Feature | Pre-2026 (GILTI) | 2026+ (NCTI) |

|---|---|---|

| Section 250 deduction | 50% | 40% |

| Effective US tax rate | 10.5% | 12.6% |

| QBAI routine return carve-out | 10% of tangible assets | Eliminated entirely |

| FTC haircut (§960(d)) | 20% (80% usable) | 10% (90% usable) |

| High-tax exception threshold | ~18.9% effective local rate | ~14% effective local rate |

| Income allocation timing | Last day of CFC tax year | Any day of stock ownership |

The rate increase hurts. But two provisions are genuinely better: the improved FTC treatment (90% instead of 80%) and the lowered high-tax exception threshold (14% instead of 18.9%). If your foreign company operates in a jurisdiction with a 14%+ effective corporate tax rate, you may now be able to eliminate NCTI entirely — a threshold that was previously out of reach for many expat business owners in moderately-taxed countries.

Five Ways to Reduce or Eliminate NCTI

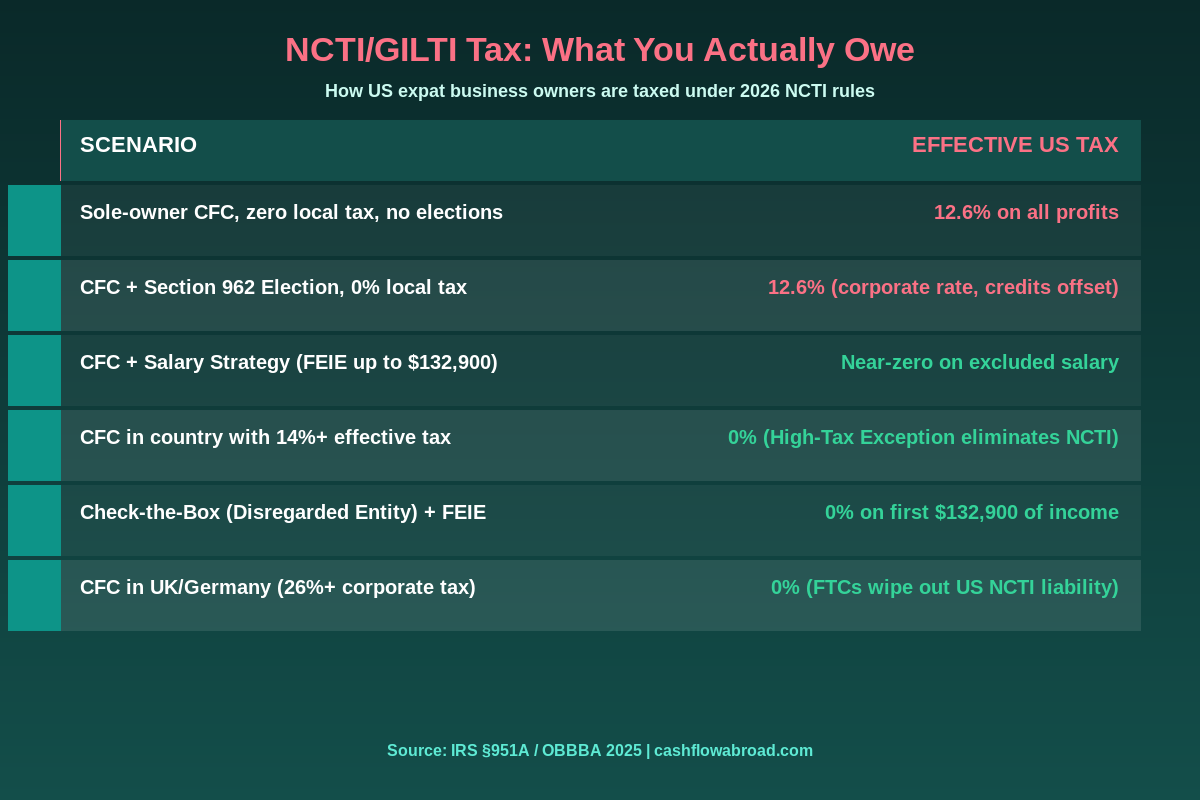

1. High-Tax Exception Election

If your foreign corporation pays a local effective tax rate of 14% or more, you can elect the high-tax exception on Form 8992, which removes that income from NCTI entirely. This is the cleanest solution available — and the OBBBA brought the threshold down from 18.9% to 14%, expanding the universe of countries where it applies.

Countries where the exception now applies: UK (25% corporate rate), Germany (~30% combined corporate + trade tax), France (25%), Japan (23%), Canada (26%), Australia (30%), Singapore (17%), Ireland (12.5% — borderline; verify effective rate). If you’re running a CFC in any of these jurisdictions, your NCTI bill could be zero — but you must elect it annually. It doesn’t apply automatically.

Countries where the exception does NOT help: Georgia (1% turnover tax), Paraguay (0% on foreign income), Dubai (0% for many structures), Cayman Islands (0%), and most other zero or near-zero tax havens. Running a CFC in a zero-tax jurisdiction without a planning strategy will cost you 12.6% to the IRS on every dollar of profit retained in the company.

2. Section 962 Election

A Section 962 election allows individual US shareholders to elect corporate-level treatment on their NCTI inclusion. Without it, an individual shareholder faces ordinary income rates up to 37% on their gross NCTI inclusion — no Section 250 deduction, no favorable rate. With the 962 election, you access the 40% Section 250 deduction and the 90% foreign tax credit, bringing the effective rate down to 12.6% before credits.

Example: you own a German CFC paying 30% local corporate tax. Your NCTI inclusion is $100,000. Without the 962 election, at 37% ordinary rate, you owe $37,000 (less some FTCs). With the 962 election: 21% × 60% = 12.6% effective rate, and your German FTCs (30% × 90% = 27% creditable) wipe out the 12.6% entirely. Net US NCTI tax: $0.

The catch: when you eventually distribute earnings from the CFC as dividends, a portion of the distribution may be taxed again at qualified dividend rates (0–20%), though previously taxed income (PTI) rules prevent complete double taxation. The 962 election is most powerful when combined with a long-term strategy of retaining earnings inside the CFC for reinvestment rather than regular distributions.

3. Check-the-Box Election + FEIE

For sole-owner CFCs earning under roughly $132,900, the check-the-box election (Form 8832) is often the most efficient strategy. By electing disregarded entity status, you turn off the CFC rules entirely. Your foreign company stops existing as a separate entity for US tax purposes, and its net income flows directly onto your Schedule C as self-employment income.

Once it’s on Schedule C, you can exclude up to $132,900 in 2026 using the Foreign Earned Income Exclusion (FEIE) — provided you satisfy the bona fide residence or physical presence tests. You’ll owe self-employment tax (15.3% on net earnings up to ~$176,100), but that replaces NCTI exposure with a known, predictable cost and eliminates the Form 5471 filing requirement.

Check-the-box is only available for entities not on the IRS “per se corporation” list. Most common expat structures — UK Ltd, Irish Ltd, Canadian CCPC, Colombian SAS, German GmbH, Estonian OÜ — are eligible. Consult a tax professional for your specific jurisdiction before filing Form 8832.

4. Pay Yourself a Market-Rate Salary

Even with the CFC intact, paying yourself a commercially reasonable salary from the foreign company reduces the company’s net profit — and therefore its NCTI base. That salary flows to you as earned income, which qualifies for the FEIE (up to $132,900).

The math: a CFC with $200,000 in profit that pays you a $130,000 salary has only $70,000 in tested income subject to NCTI. Your salary is excluded via FEIE. You’ve cut the NCTI exposure by 65% without restructuring anything. The salary must be commercially reasonable and consistent with what you’d pay a third-party employee in the same role — the IRS scrutinizes inflated salary-to-profit ratios in low-tax CFC structures.

5. Foreign Tax Credits in Moderately-Taxed Countries

With the FTC haircut now at 10% (down from 20%), you can credit 90% of foreign corporate taxes against your US NCTI liability. The full-offset crossover point is approximately 14% effective local rate. This means: if your CFC pays 14% or more in local tax, the FTC alone can eliminate your entire US NCTI bill.

In practice, the math means you’re paying only the higher of the two rates — the local rate or 12.6%. Running a CFC in Singapore paying 17% in corporate tax? Singapore is higher; your NCTI tax is zero. Running in Ireland at 12.5%? Below the 14% threshold, so you’ll have a small US NCTI residual. Running in Germany at 30%? Full FTC offset; zero NCTI owed in the US.

The Paperwork: Forms You Cannot Skip

NCTI doesn’t just cost money — it costs compliance hours. The filing requirements for CFC owners are substantial, and the penalties for non-filing often exceed the actual tax owed:

- Form 5471 — annual disclosure for US shareholders of CFCs. Required if you own 10%+ of a foreign corporation at any point during the year. Penalty for non-filing: $10,000 per year per form, escalating to $50,000 for continued failure. Applies regardless of income or tax owed.

- Form 8992 — calculates and reports your NCTI inclusion. Required any year you have tested income from a CFC.

- Form 8832 — check-the-box election for disregarded entity status. File before the deadline for the tax year you want the election to apply. Late elections require IRS approval.

- Form 1118 — claims foreign tax credits on NCTI income. Filed alongside Form 8992 when you have creditable foreign taxes to offset.

- FinCEN 114 (FBAR) — required if the CFC holds bank accounts where you have signature authority or financial interest exceeding $10,000 at any point during the year, separate from your personal FBAR.

The Form 5471 penalty alone — $10,000 per year, per form — applies even if the company had no revenue and you owe zero NCTI. Non-filers get caught through FATCA reporting by foreign banks and through the IRS’s expanding network of international data-sharing agreements under CARF. For the full picture on FBAR, FATCA, and FEIE interaction, the complete expat banking and taxes guide covers these in depth.

The Mistakes That Blow Up Expat Business Owners

Mistake 1: “I didn’t pay myself, so I don’t owe US tax.” NCTI is an inclusion — it’s triggered by the company’s profits, not by distributions. The profit sitting inside your CFC is taxed in the year it’s earned, whether or not you touch it.

Mistake 2: Assuming the FEIE covers CFC income. The FEIE excludes earned income — salary, wages, and net self-employment income. It has no effect on NCTI inclusions from a CFC. These are entirely different tax calculations on different forms.

Mistake 3: Setting up a zero-tax CFC with no planning. A Georgian LLC, Dubai FZCO, or Paraguayan SA with no high-tax exception, no salary strategy, and no 962 election is a 12.6% NCTI exposure on every dollar of retained profit. The zero local tax doesn’t make it disappear — it makes it worse, because you have no FTCs to offset the US bill.

Mistake 4: Not filing Form 5471 because the company is dormant. The $10,000 penalty applies regardless of revenue. Zero-activity CFCs still require the form if ownership thresholds are met.

Mistake 5: Conflating Subpart F and NCTI. Subpart F targets passive income inside the CFC (interest, dividends, royalties from related parties). NCTI targets active business profits that escape Subpart F. Both can hit simultaneously. Subpart F is calculated first and excluded from NCTI — but misclassifying income between the two regimes creates both over-reporting and under-reporting risks.

Choosing the Right Structure Before You Incorporate

The NCTI rules should inform where and how you incorporate — not become a problem to solve after the fact. Three common frameworks:

Disregarded entity + FEIE — best for sole operators earning under $132,900 living in a FEIE-qualifying country. Eliminates the CFC entirely. Works well in Georgia, Paraguay, Dubai, and other low-tax destinations where the goal is minimizing local tax, not building retained corporate capital. Simple, cheap to maintain, and removes the Form 5471 obligation.

CFC + salary + 962 election — better for higher earners or those retaining capital inside the company for reinvestment. FEIE covers the salary component; retained earnings face 12.6% NCTI but benefit from the 962 election and any available FTCs. Requires an international tax CPA, annual elections, and solid recordkeeping of PTI balances.

CFC in a high-tax country — if your business naturally operates in the UK, Germany, Canada, or another high-tax jurisdiction, the high-tax exception can eliminate NCTI entirely. You pay the higher local rate (often 25–30%) but owe zero to the IRS on NCTI. Effectively, you pay only one government — the local one. This structure works well for expats who moved abroad for reasons other than tax minimization and happen to be in a country with a mature corporate tax regime.

For US banking while operating a foreign company, Mercury is the standard for expat founders — no monthly fees, built for remote teams, and it remains accessible regardless of where you physically reside. If you need to repatriate earnings or make wire transfers between your CFC and a US account, a solid US banking foundation matters. See the expat investor’s playbook for structuring your cross-border financial architecture, and the breakdown on running a US business while living abroad if you’re operating a US LLC alongside your foreign entity.

If you operate in Latin America and need a financial tool built for dollar access in the region, ARQ Finance lets you hold USDc/EURc balances, earn up to 4% on dollar savings, and swap to local currencies (MXN, COP, ARS, BRL) — useful for managing currency risk between your CFC and local expenses.

The Bottom Line

GILTI — now NCTI — is the single biggest tax surprise for US expats who build businesses abroad. The rate went up in 2026 (from 10.5% to 12.6%), the taxable income base got broader (QBAI carve-out eliminated), and the IRS’s international data-sharing capabilities under FATCA and CARF make non-filers increasingly easy to identify.

But the strategies to eliminate or minimize NCTI are real and well-tested: the high-tax exception, Section 962 election, check-the-box, salary extraction, and foreign tax credits all work. They just require deliberate planning, annual elections, and compliance with a filing stack that most general CPAs have never touched.

Don’t set up a zero-tax CFC and assume you’ve escaped the IRS. Run the numbers on your structure before you incorporate, pick the right combination of strategies for your income level and jurisdiction, and file every required form. The savings from NCTI planning can be $20,000–$50,000+ per year for a mid-size expat business. The cost of ignoring it is the same number — but with penalties and interest added.

Disclaimer: This article is for educational purposes only and does not constitute tax or legal advice. US international tax law is complex, and individual circumstances vary significantly. Rules under the OBBBA were still being finalized as of publication — verify current thresholds, rates, and election procedures with current IRS guidance or a qualified international tax professional (CPA or tax attorney) before filing.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.