Here's a number that should make your stomach drop: the average American living abroad unknowingly hands their bank $1,440 or more every single year in fees they could completely eliminate. That's not a typo. That's 3% foreign transaction markup on $30,000 in annual spending, plus $45 international wire fees at a conservative one per month — gone, permanently, into your bank's revenue line.

Meanwhile, a small minority of expats operate with a three-to-four account stack that costs effectively zero dollars per year in banking fees. No ATM charges anywhere on earth. No currency conversion markups. No wire fees for moving money between countries. It sounds too good, but it's been sitting in plain sight for years — most people just never learned to put it together.

This guide is that assembly instruction. By the end, you'll have the exact accounts, the setup sequence, and the optional advanced layer that smart expats in Latin America are increasingly using to squeeze even more out of the system.

Related: complete FBAR and FATCA guide

The Fee Math Nobody Shows You

Let's start with what your current bank is actually charging you. Banks don't advertise these numbers prominently, so here's the ugly breakdown:

Foreign Transaction Fees

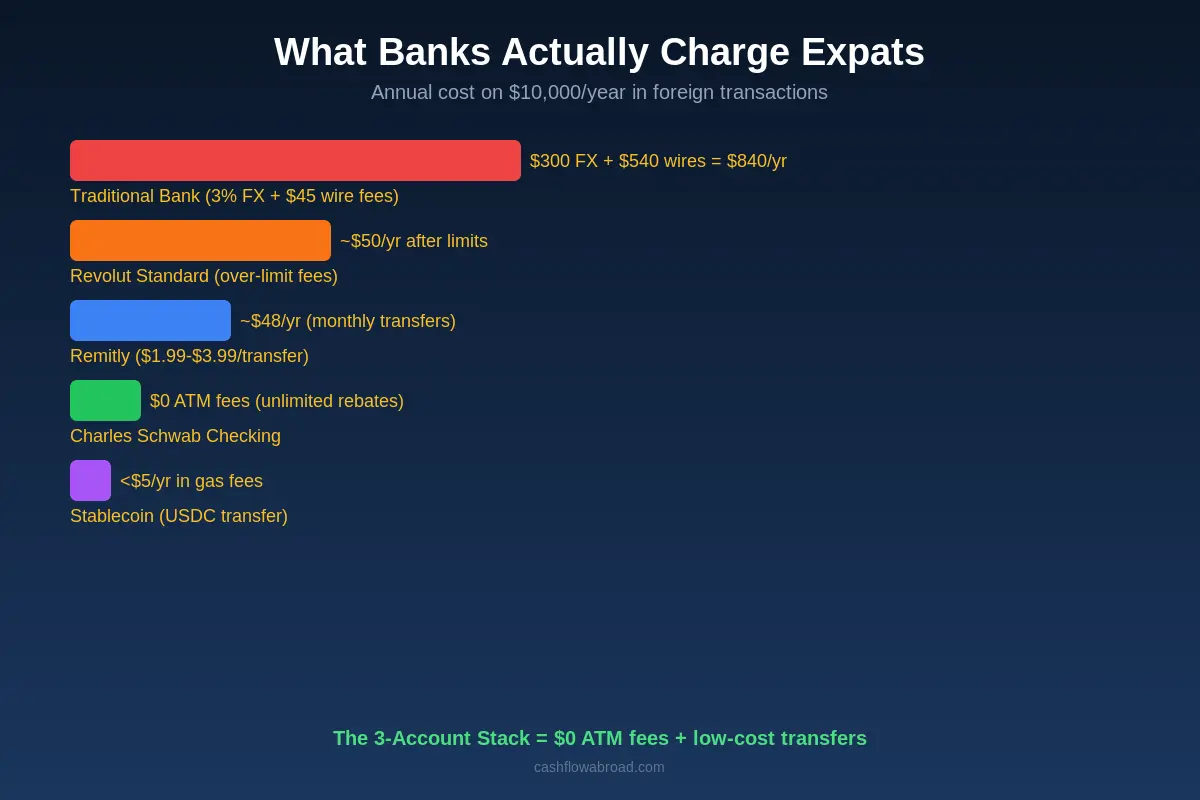

Most US checking and savings accounts charge 1% to 3% on every foreign purchase. At Wells Fargo Everyday Checking, that's 3% — meaning every $1,000 you spend costs you $30 extra. Bank of America, Chase, and most credit unions are similarly structured. Spend $30,000 abroad in a year (not hard if that's where you live), and you've paid $900 in invisible fees.

ATM Withdrawal Fees

Your bank charges you $2–$5 per withdrawal. The foreign ATM operator charges you another $3–$8. That's potentially $13 per withdrawal at a foreign bank ATM. Pull cash twice a week, and you're at $1,352 per year in ATM fees alone. In Thailand, ATM operator fees often run $6–$8 per transaction — a documented case shows one traveler was charged $8 to withdraw just $10. Schwab reimbursed it (more on that below). Your regular bank would not.

International Wire Transfer Fees

Outgoing international wires from major US banks run $35–$50 per transfer. Bank of America charges $45 in USD. Chase charges $40–$50. And that's before intermediary bank fees — if your wire passes through two correspondent banks (common in less-developed banking corridors), you're looking at another $20–$40 stripped from the amount in transit. Total cost per wire: potentially $70–$90.

Do that once a month to pay rent or fund a local account, and you've spent $840–$1,080 per year just moving your own money.

The Hidden FX Spread

Even when banks advertise "no transfer fee," they make it back in the exchange rate. The difference between the mid-market rate (the real rate, the one you see on Google) and what banks actually give you is typically 2.4% to 3.5%. HSBC Expat buries a 2.4–3.5% markup into every international transfer. On a $10,000 transfer, that's $240–$350 gone quietly, with no line item on your statement.

Add it all up and it becomes clear: traditional US banking is architecturally hostile to anyone who lives outside the country it was designed for.

| Fee Type | Traditional Bank | Annual Cost (Typical Expat) |

|---|---|---|

| Foreign transaction fee (3%) | Wells Fargo, Chase, BofA | $900 on $30K spending |

| ATM withdrawal fees | $5 your bank + $5 operator | $520/yr (2x/week) |

| International wire fees | $35–$50 per wire | $540/yr (monthly wires) |

| FX spread on transfers | 2.4–3.5% markup | $240–$350 per $10K moved |

| Total | $1,500–$2,300+/yr |

That's real money — money that could be funding your travel, topping off your investment account, or just sitting in your pocket where it belongs.

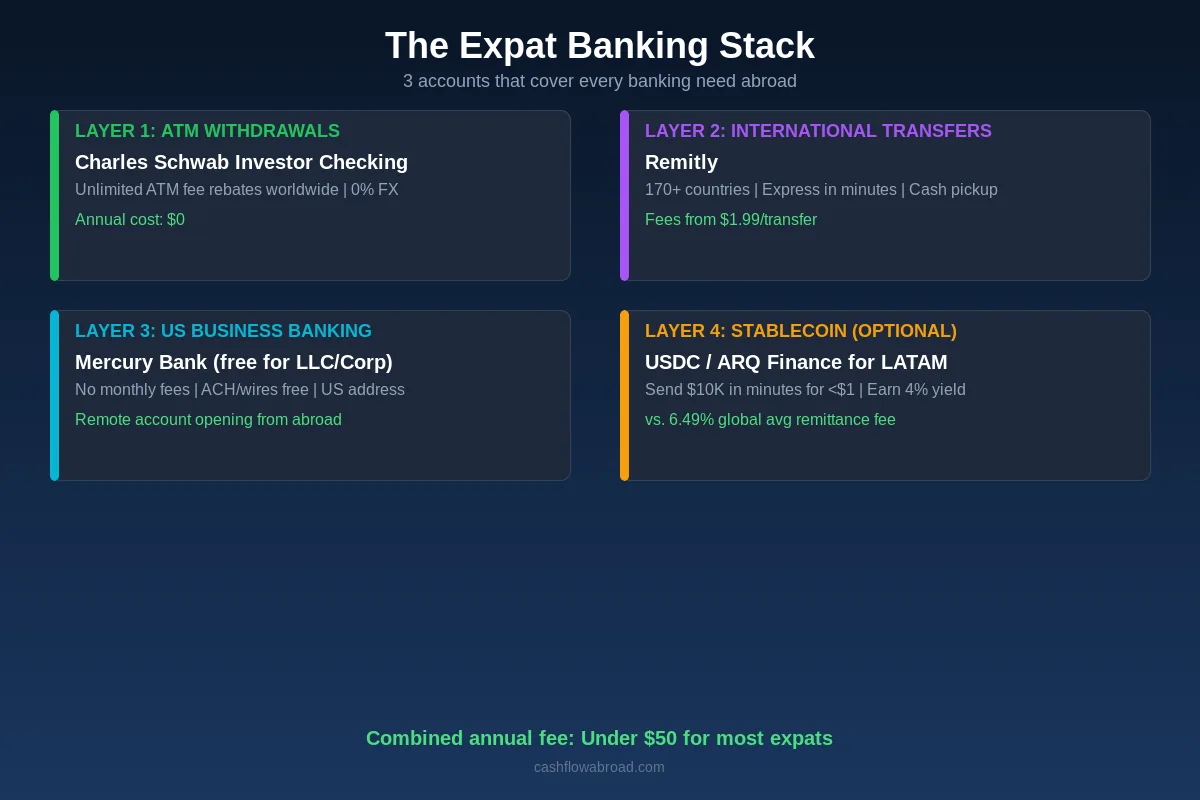

The Three-Account Stack

The solution isn't one magic account. It's a deliberate stack of two to three accounts, each optimized for a different job. Here's what the ideal setup looks like:

Account 1: Charles Schwab Investor Checking — The ATM King

If you do nothing else after reading this article, open a Charles Schwab Investor Checking account. It's the single most impactful move for expat banking, full stop.

Here's what it does that your current account doesn't:

- Zero foreign transaction fees on debit card purchases — 0%, forever

- Unlimited ATM fee rebates worldwide — Schwab reimburses every ATM fee charged globally, including the operator's fee, at month-end. They rebate the $8 fee on the $10 Thai ATM withdrawal. Every penny, every time.

- No monthly fees and no minimum balance requirement

- Daily ATM limit of $1,000 — enough for most cash needs

- FDIC insured up to $250,000

The catch: you need to open a linked Schwab One brokerage account alongside it. That account also has no minimum balance, no fees, and you don't have to put any money in the brokerage if you don't want to. It's a paperwork pairing.

One important caveat for long-term US expats: if you update your residential address to an international address, Schwab converts your account to "international status" through Schwab International. At that point, you can no longer purchase new US mutual funds or CDs (though you can still hold ones you already own). For the checking account — cash access, debit card, ATM rebates — this changes nothing. It still works perfectly from abroad.

Many long-term expats maintain a US address (a parent's home, a mail-forwarding service like Traveling Mailbox (from $15/month — real US street address with mail scanning) or Earth Class Mail, or a US-based friend) to preserve full account functionality. Either approach works.

Real-world math: one documented case shows a traveler saved approximately $80 on $500 in ATM withdrawals during a single month in Jamaica. In Southeast Asia, where ATM operator fees of $5–$8 are common, someone making regular cash withdrawals could save $500–$1,000 per year from Schwab's rebates alone.

Open a Schwab account via the Charles Schwab referral link here — the linked Schwab One brokerage also doubles as a capable international investing platform, with access to US stocks, ETFs, and bonds, which matters enormously for avoiding the PFIC trap (more on that in our expat investing playbook).

Account 2: Remitly — The International Transfer Engine

Charles Schwab handles ATM withdrawals brilliantly. But for sending money internationally — paying rent in a foreign currency, supporting family abroad, moving funds to a local account — you need a dedicated transfer service.

Related: money transfer guide

Remitly sends money to 170+ countries with Express transfers arriving in minutes and Economy transfers at reduced fees. Banks charge 2.4–3.5% on international transfers in hidden FX markups alone. Remitly's fees start at $1.99 for Economy transfers, and first-time users often get promotional rates that beat even the cheapest alternatives.

What Remitly gives you:

- Express transfers — money arrives in minutes via debit card funding (fees from ~$3.99)

- Economy transfers — lower fees ($1.99) via bank account, delivered in 3-5 business days

- Multiple delivery methods — bank deposit, cash pickup at 470,000+ locations, mobile money, and even home delivery in select countries

- Remitly One membership ($9.99/mo) — includes a digital debit card with no foreign transaction fees, a wallet that earns 4% on USD balances, and cash advances up to $250

- Transfers up to $25,000 per transaction (up to $100,000 with additional verification)

- 4.87/5 stars from nearly 4 million App Store reviews — one of the highest-rated financial apps

The complementary relationship between Schwab and Remitly is deliberate. Use Schwab to pull out physical cash from any ATM anywhere. Use Remitly to move money across borders — especially to countries where recipients need cash pickup or mobile money options that bank-only services cannot provide. These two accounts together handle 90% of expat banking needs.

Account 3: Mercury — The US Business Anchor

If you run any kind of online business, freelance, or operate a US LLC while living abroad (and many expats do — it's often the optimal tax structure), you need a legitimate US business banking account. Mercury is the standard for remote workers and expat entrepreneurs.

Mercury is a fintech-powered business bank account with no monthly fees, free ACH transfers, free domestic wires, and a clean interface built for modern remote businesses. You can open it from anywhere in the world — unlike most traditional US banks that now require an in-person branch visit.

Why Mercury matters for the expat stack:

- $0 monthly fees with no minimum balance requirements

- Free ACH and domestic wire transfers

- Works seamlessly with Stripe, PayPal, Remitly, and other common tools

- US business address and routing/account numbers — essential for getting paid by US clients who require this

- Fully openable remotely with EIN and LLC documents — no branch visit

- Treasury accounts earning yield on idle cash balances

For the full framework on structuring a US business as an expat — including the tax advantages that can compound to $50K+ annually — check our guide on how to run a US business while living abroad. Open a Mercury business account here.

The Full Account Comparison

Here's how the primary options stack up side by side:

| Account | Monthly Fee | FX Fee | ATM Policy | Best For |

|---|---|---|---|---|

| Charles Schwab Checking | $0 | 0% | Unlimited global rebates | Cash withdrawals anywhere |

| Remitly | $0 (One: $9.99/mo) | $1.99–$3.99 + FX markup | N/A (transfer service) | International transfers, cash pickup, mobile money |

| Mercury (Business) | $0 | Varies | Not primary use case | US business banking, client payments |

| Revolut Standard | $0 | 0% up to $1,000/mo | $400/mo free, then 2% | Everyday card spending, backup |

| Revolut Metal | $16.99/mo | 0% including weekends | $1,200/mo free, then 2% | High-volume spenders, frequent travel |

| Fidelity Cash Management | $0 | 0% | Worldwide fee-free | US investing + Schwab backup |

| HSBC Expat Premier | $0 (with £100K+ income) | 2.4–3.5% markup | $0 own ATMs | High-net-worth HSBC relationship banking |

| Traditional Big Bank | $0–$15 | 1–3% | $3–$5 + operator fee | Don't use as an expat |

Where Revolut Fits In

Revolut isn't the centerpiece of this stack, but it earns a spot as a backup card and for specific use cases. The Standard plan is free and gives you mid-market rate currency exchange up to $1,000 per month — useful for everyday card spending in local currencies without burning Remitly transfers on small amounts.

The limitations: Revolut Standard's ATM allowance is $400/month free, then 2%. Their weekend FX fee on the Standard plan can add 0.5–2% on exchange during non-business hours. For heavy cash users or anyone pulling more than $400 from ATMs monthly, Schwab still wins.

The Metal plan at $16.99/month eliminates the weekend fee and raises the ATM free tier to $1,200/month — effective as of April 22, 2025. It pencils out if you're spending heavily across multiple currencies and making frequent ATM withdrawals beyond Schwab's $1,000 daily limit. For most expats, Schwab + Remitly + Revolut Standard covers everything without a paid subscription.

The Advanced Layer: Stablecoins as a Banking Tool

This is where the stack goes from good to exceptional — particularly for expats in Latin America, Southeast Asia, or anywhere with a volatile local currency or expensive remittance corridors.

USDC — the fully audited, dollar-backed stablecoin from Circle — crossed a $75 billion market cap and processed over $1 trillion in monthly transaction volume as of late 2024. Its circulation grew 78% year-over-year. The broader stablecoin market hit approximately $230 billion in 2025. Stablecoin annual transaction volume from January to July 2025 exceeded $4 trillion — an 83% rise from the prior year period. This isn't a fringe experiment. It's becoming a parallel financial rail.

Transfer Cost Elimination

The global average remittance fee is 6.49%. Sub-Saharan Africa averages 8.78%. Stablecoin transfers cost less than 1% in most cases — and on networks like Arbitrum or Solana, literal cents per transaction. Sending $10,000 in USDC settles in under a minute and costs under $1. Sending $10,000 via traditional wire costs $70–$90 in fees and takes 1–3 business days. The difference is not marginal.

Dollar Access in Restricted Markets

In countries with capital controls or weak currencies — Argentina, Nigeria, Lebanon — holding USDC effectively gives you a dollar account outside the local banking system. You preserve purchasing power without physically moving dollars across a border or navigating exchange rate restrictions.

Yield on Idle Dollars

Some DeFi platforms currently offer 4–10% annualized yield on stablecoin deposits. Even at the conservative 4% end, that meaningfully beats most US savings accounts. USDC is backed 1:1 by cash or short-term US Treasuries and audited monthly by Deloitte — meaningfully more transparent than competing stablecoins.

ARQ Finance: The LATAM-Specific Play

For expats in Mexico, Colombia, Argentina, or Brazil, ARQ Finance is worth serious attention. It's a stablecoin-powered platform that lets you:

Related: stablecoin savings guide

- Hold dollar balances in USDc or EURc

- Swap to local currencies (MXN, COP, ARS, BRL) at competitive rates

- Deposit USDC/USDT from external wallets

- Earn up to 4% on dollar balances

- Pay with a Mastercard with cashback

- Access stock and ETF investing from within the platform

It's essentially a dollar account accessible from LATAM without needing a US address or waiting for a wire transfer window. For expats in Medellín, Mexico City, or Buenos Aires tired of watching their local currency erode while waiting for bank transfers, this solves a real problem.

Note: ARQ Finance is not an investment advisor. Available in Mexico, Colombia, Argentina, and Brazil.

For more on how the banking landscape works specifically in Colombia, the team at ColombiaMove covers the best banking options for foreigners in Colombia in thorough detail.

Stablecoin Debit Cards

Crypto debit card spending has grown from roughly $100 million per month in early 2023 to $1.5 billion per month by late 2025 — an annualized run rate now exceeding $18 billion. The Coinbase Card, for instance, charges 0% foreign transaction fees and 0% on USDC spending, with no monthly or annual fee. This adds a useful zero-cost card layer on top of the stablecoin stack.

Offshore Banking: Is It Actually Worth It?

Every few months, someone in an expat Facebook group posts breathlessly about opening a Swiss bank account. Let's clear this up.

Traditional offshore banking — in the sense of secretive accounts in Switzerland, the Cayman Islands, or Singapore — is largely a relic of the pre-FATCA world. Here's the current reality:

- Switzerland: Minimum deposits typically $100,000+. Swiss banks now share information with US authorities under FATCA and CRS. Privacy advantages versus 20 years ago: minimal.

- Cayman Islands: Minimum deposits often $100,000+. Serious ongoing compliance requirements. Not for everyday expats.

- Georgia (the country): Low barriers. Accounts openable with a few hundred dollars at some banks. No residency requirement at some institutions. Genuinely accessible — but limited utility if your money is USD-denominated and your life is already global.

- Mauritius: Offshore accounts openable with a few thousand dollars. Useful for specific business structures, not everyday banking.

The honest assessment: for most expats, the three-account stack above (Schwab + Remitly + Mercury) is more useful than any offshore account. It's legal, transparent, zero-fee, and actually usable day-to-day. Offshore accounts are worth exploring for specific asset protection, estate planning, or business structuring scenarios — which we cover in the expat estate planning guide.

The FBAR and FATCA Reality Check

Opening foreign accounts doesn't make you a criminal. But it creates reporting obligations for US citizens and green card holders. Here's the quick version:

- FBAR (FinCEN Form 114): Required if your aggregate foreign account balances exceed $10,000 at any point during the calendar year. Filed separately from your tax return, due April 15 (automatic extension to October 15). Penalty for non-willful failure: up to $10,000 per violation. Willful violation: up to $100,000 or 50% of the account balance per violation.

- FATCA (Form 8938): Filed with your tax return. Threshold for Americans living abroad: $200,000 single at year-end ($300,000 at any point), or $400,000 married filing jointly at year-end ($600,000 at any point).

The accounts in this guide — Schwab, Remitly, Mercury — are all US-based or US-registered entities. They generally don't trigger FBAR reporting. But if you open a local bank account in your host country, you need to track its balance as part of the aggregate calculation. See our complete FBAR and FATCA guide for the full rundown on reporting obligations.

Setting Up the Stack: The Practical Sequence

Here's the implementation order for getting this running, starting from wherever you are:

Step 1: Open Charles Schwab (Do This First)

Go to Schwab's website and open both the Investor Checking account and the linked Schwab One brokerage simultaneously — the application is online and takes 10–20 minutes. You'll need your SSN. If you're already abroad, use your US address initially (or a mail-forwarding service address). Fund it with a small initial transfer from your existing bank — even $100 to get the debit card ordered and shipped.

Schwab ships debit cards internationally. Expect 1–3 weeks for international delivery. Open online via this Charles Schwab referral link.

Step 2: Set Up Remitly

Remitly account creation takes about 5 minutes online. You'll verify your identity with a government ID. Link your US bank account or debit card for funding transfers. Download the mobile app for the best experience — it's where you'll manage transfers, track delivery, and access the Remitly wallet.

Step 3: Mercury (If You Have a US Business)

Mercury requires an EIN and business entity documents (LLC operating agreement, articles of organization). If you have a US LLC, the application is entirely online and takes about a week to approve. No branch visit required. Apply through the Mercury referral link.

If you don't have a US business yet but are earning more than $60K annually remotely, the tax math often makes setting one up worthwhile. We walk through the full structure in our guide to building a $100K online business from anywhere.

Step 4: Consider a Local Account

In many countries, you'll eventually want a local bank account for landlord payments, utility bills, or transactions that require local banking infrastructure. This varies enormously by country. In Colombia, Bancolombia and Davivienda are the most accessible for foreigners; in Mexico, BBVA Mexico is often easiest. Key reminder: keep FBAR in mind once the balance crosses $10,000 at any point. For Colombia specifically, see the full Colombia banking guide at ColombiaMove.

Step 5: Add the Stablecoin Layer (Optional)

If you're doing large international transfers regularly, receiving payments in crypto, or living in a high-inflation LATAM country, set up a USDC wallet (Coinbase is the simplest starting point). For LATAM specifically, explore ARQ Finance for dollar-yield and local-currency swap capabilities without wire delays.

Related: virtual mailbox guide

The VPN Problem for Expat Banking

One often-overlooked friction point: US banking apps frequently flag logins from foreign IP addresses and may temporarily lock your account, require extra 2FA verification, or in some cases suspend access entirely. A VPN set to a US server is a practical solution — log in to your bank using a US IP address to avoid these flags.

NordVPN is the reliable standard here. Keep it enabled when accessing any US financial account from abroad. It also protects against man-in-the-middle attacks on public WiFi — a real threat when you're banking at a café in Bangkok or a coworking space in Lisbon.

The Cost Math Revisited

Let's close the loop on the numbers. Here's the annual fee comparison for someone making $30,000 in foreign card transactions per year, pulling cash twice weekly, and sending one international transfer monthly:

| Scenario | ATM Fees | FX Fees | Wire/Transfer Fees | Total Annual Cost |

|---|---|---|---|---|

| Traditional US bank | $520 | $900 | $540 | $1,960 |

| Revolut Metal only | $204 (subscription) | $0 | ~$200 (fees apply) | ~$404 |

| Schwab + Remitly + Mercury | $0 | ~$150 (0.5% avg on conversions) | $0 (ACH/domestic wires) | ~$150 |

| Schwab + Remitly + Stablecoins | $0 | ~$100 | <$10 (on-chain) | <$110 |

The difference between "leave your Bank of America account running" and "set up the three-account stack" is roughly $1,800 per year. That's a business-class flight. That's three months of housing in Medellín. That's a meaningful addition to your investment account every single year, compounding quietly in your favor for the entire duration you live abroad.

Bonus: The Schwab Brokerage Advantage

Here's what most people miss: the Schwab One brokerage account you open alongside the checking account is a fully functional investment platform with zero-commission stock and ETF trading and no account minimum.

That means your expat banking setup is simultaneously a world-class investing platform. US expats have notoriously limited investment options — many platforms block non-US residents from opening accounts, and the PFIC rules create tax nightmares for foreign-domiciled funds. Schwab's brokerage lets you hold US ETFs, US stocks, and bonds without those issues, accessible from anywhere on earth.

For international exposure in your portfolio, use US-listed international ETFs through Schwab: iShares MSCI EAFE (EFA), Vanguard FTSE All-World ex-US (VEU), or similar. These are not PFICs. The equivalent S&P 500 tracker sold by a German bank through a German brokerage is a PFIC — same underlying assets, wildly different tax treatment. See our expat investor's playbook for the full framework.

If you want to add active trading to the mix, tastytrade is the platform of choice for options trading and derivatives — also accessible to US expats with a US address on file.

Moving Large Amounts: $10K–$500K

The stack above handles everyday spending. For larger transfers — moving $50,000 or $200,000 to buy property, fund a business, or consolidate accounts internationally — the dynamics are different. Remitly handles transfers up to $25,000–$100,000 depending on verification level. For very large amounts, specialist FX brokers like OFX, XE Money Transfer, or Currencies Direct often offer better rates on transfers above $50,000–$100,000.

For the complete breakdown on moving large sums internationally — including how to avoid wire fees, when to use forward contracts, and which corridors have the worst fees — see our expat money transfer guide covering $10K to $500K.

For day-to-day smaller transfers to local accounts — paying a housekeeper, splitting rent with a local partner, reimbursing local friends — Remitly consistently offers competitive exchange rates with transparent fees for common expat corridors (US to Colombia, US to Mexico, US to Philippines, etc.).

Common Mistakes to Avoid

Based on how often these come up in expat communities:

- Closing your US bank account before the new stack is set up. Keep the old account active during transition. You need it to fund the new accounts.

- Using your bank for international transfers. Banks charge 2.4–3.5% in hidden FX markups. Use Remitly for international transfers — fees start at $1.99 and Express transfers arrive in minutes.

- Using credit cards with foreign transaction fees. If you use credit cards for points, make sure they're fee-free abroad — Chase Sapphire Preferred, Capital One Venture, and most premium travel cards have 0% foreign transaction fees. Standard credit cards from traditional banks often charge 1–3%.

- Forgetting the FBAR threshold is aggregate. If you have a local checking account with $6,000 and a local savings account with $5,000, your aggregate is $11,000 — FBAR is required, even if neither account individually exceeds $10,000.

- Ignoring the international status implications of updating Schwab address. If you update your address internationally, some account features change. Many expats keep a US address on file for this reason.

- Opening a local brokerage account and buying local mutual funds. These are almost certainly PFICs. Hold all investment funds through US-listed accounts and US-listed ETFs only.

The Scale of This Problem

The reason this matters at a macro level: there are an estimated 9 million Americans living abroad according to State Department estimates, and roughly 35 million digital nomads globally. A 2025 survey found that 32% of expats struggle to open bank accounts abroad.

Expatriating Americans hit a new high in Q1 2025, with 1,285 Americans renouncing citizenship — a 102% jump versus Q4 2024. More people are moving abroad, more are running remote businesses, and more are navigating banking systems that weren't designed for them. The global remittance market reached $857 billion in annual flows, with $656 billion going to developing countries — yet global average remittance fees remain at 6.49%, meaning roughly $55 billion per year disappears in fees alone. The stablecoin rail cutting that to under 1% represents a generational shift in how international money moves.

If you're in that 9 million — or planning to join them — the banking decisions you make in the first few months set the cost structure you'll live with for years.

Conclusion: Stop Paying the Expat Tax on Your Own Money

The average expat pays $1,500 to $2,300 per year in banking fees they'd pay nothing for with a different account setup. That's not a small rounding error — it's a meaningful sum that compounds over years and decades of living abroad. The $1,800 you save annually in fees, invested at a modest 7% return, becomes $94,000 over 20 years. The account setup takes an afternoon.

The fix is straightforward. Open Charles Schwab for free global ATM access. Use Remitly for international transfers at a fraction of what banks charge. Add Mercury if you have a US business. Layer in stablecoins — or ARQ Finance for LATAM — if you want to go further. Use a VPN when logging into US accounts from abroad. Keep your FBAR filing current on any local accounts.

The expat life is already full of trade-offs and learning curves. Your banking setup doesn't have to be one of them.

Financial Disclaimer: This article is for informational and educational purposes only and does not constitute financial, legal, or tax advice. Banking products, fees, and features are subject to change. FBAR and FATCA requirements are complex — consult a qualified US tax attorney or CPA with expat experience before making decisions about foreign accounts. Affiliate links are present in this post; we may receive compensation at no additional cost to you. ARQ Finance is not an investment advisor. All investing involves risk, including the possible loss of principal.