Malta’s 15% Flat Tax: EU Residency for Non-EU Expats

8 min read · 2,073 words

Most Americans hunting for EU residency default to Portugal or Spain. They’re the loudest names in the space — and for good reason. But there’s a Mediterranean island nation that quietly hands non-EU nationals an EU residency card, a Schengen permit, and a 15% flat tax on foreign income — with zero minimum stay requirement. Malta’s Global Residence Programme hasn’t gotten the press it deserves, and that’s exactly why it’s worth understanding.

The counterintuitive part: 15% sounds steep compared to Georgia’s 1% or Paraguay’s zero. But the GRP isn’t competing with low-tax havens outside the EU — it’s competing with programs that actually get you inside the European Union. That changes the calculation entirely.

What the Malta GRP Actually Is

The Global Residence Programme is Malta’s tax residency scheme for non-EU, non-EEA, and non-Swiss nationals. It grants a special tax status and an annual residency permit that functions as a Schengen visa — meaning you can move freely across all 26 Schengen countries for 90 days out of every 180 beyond your time in Malta itself.

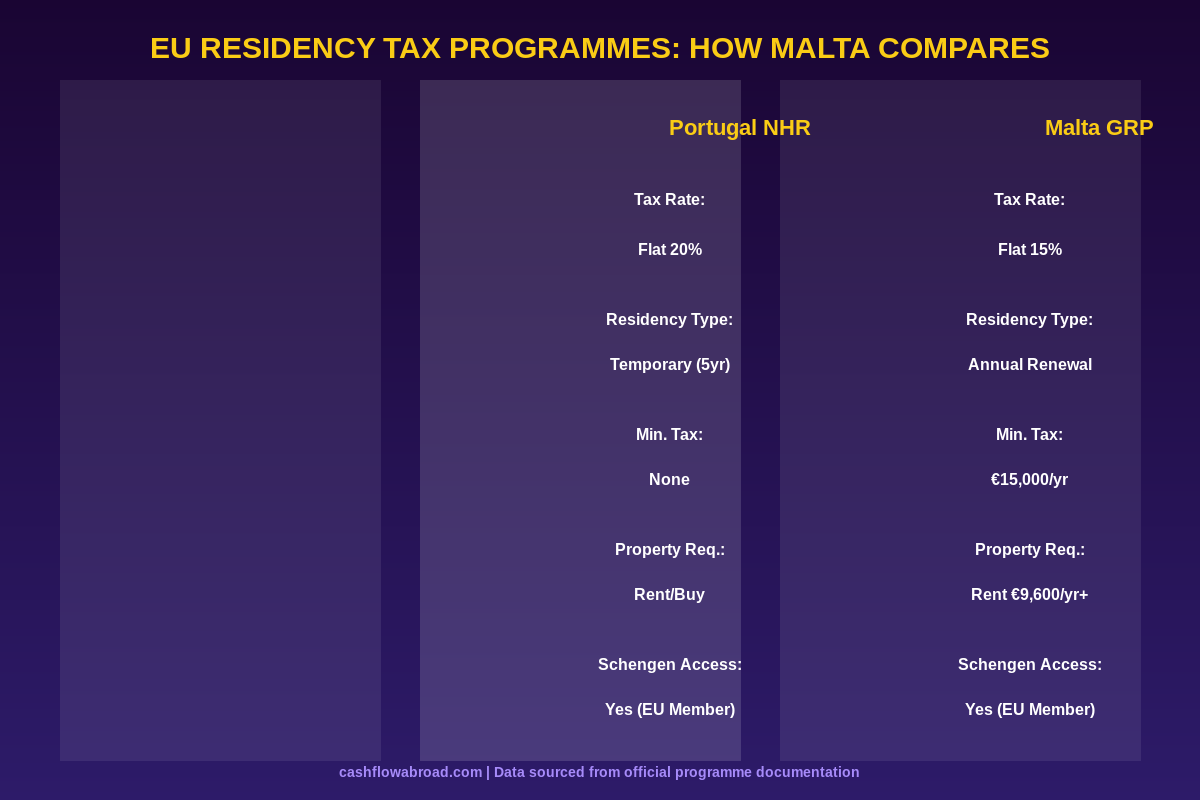

Malta designed the GRP to attract high-net-worth individuals and investors who want a legal foothold inside the European Union without the full tax burden of countries like France or Germany. The mechanics are clean: pay a flat 15% rate on foreign income you bring into Malta, with a minimum of €15,000 per year regardless of how much you actually remit, and you’re done. Foreign income that stays in overseas accounts? Not taxed at all.

This is a remittance-based system — structurally identical to the old UK non-dom regime and Singapore’s territorial approach. The critical distinction between “earned abroad” and “brought into Malta” is what drives the tax planning strategy.

How the 15% Tax Actually Works

Only foreign-source income that you physically transfer into Malta triggers the 15% rate. Foreign income sitting in an overseas brokerage, bank account, or foreign company structure? Completely exempt as long as it stays there. Malta’s tax authority doesn’t reach for income you never remit.

There’s a firm floor: even if you remit nothing, you still owe the minimum annual tax of €15,000. This covers you and your dependants. Think of it as a flat residency fee — you’re buying the permit, the Schengen access, and the EU residency card, and €15,000 is the price of admission.

What’s notably exempt regardless of remittance:

- Foreign capital gains — even if brought into Malta, they’re fully exempt from Maltese tax

- Inheritance and estate taxes — Malta has none

- Net worth or wealth taxes — also absent

That capital gains exemption is significant. If you’re selling appreciated stock, crypto, or a foreign property, you can repatriate those proceeds to Malta without any Maltese tax liability. Combined with good US tax planning (using the Foreign Tax Credit to offset US capital gains obligations), this can be a remarkably clean structure around asset liquidation events.

Requirements: Property, Insurance, and the €6,000 Fee

Beyond the annual tax, the GRP has three concrete requirements:

1. A Qualifying Property in Malta

You must either own or rent a residential property in Malta. The minimums depend on location:

| Location | Purchase Minimum | Annual Rent Minimum |

|---|---|---|

| North/Central Malta (Valletta, St. Julian’s, Sliema) | €275,000 | €9,600/yr (€800/mo) |

| South Malta or Gozo island | €220,000 | €8,750/yr (€729/mo) |

Most GRP holders rent rather than buy — the rental floor is achievable in current market conditions, and buying locks up capital in a market that doesn’t always appreciate cleanly. A decent one-bedroom apartment in central Malta runs €900–€1,200/month anyway, so clearing the minimum is straightforward.

2. Valid Health Insurance

You must hold a health insurance policy covering you and any dependants in Malta. This is a hard requirement. Private health insurance in Malta runs roughly €50–€150/month depending on age, coverage tier, and provider. SafetyWing is worth considering for GRP holders who travel frequently — their nomad insurance covers you in Malta and during Schengen travel, which pairs well with the no-minimum-stay structure of the programme.

3. €6,000 Non-Refundable Admin Fee

A one-time administrative fee of €6,000 is payable to the Maltese tax authority when you apply. It’s paid by bank draft and is non-refundable regardless of outcome. Factor this into year-one budgeting.

What It Actually Costs Per Year

Running the full math on the cheapest compliant setup:

| Cost Item | Annual Cost (EUR) |

|---|---|

| Minimum annual tax payment | €15,000 |

| Rent (Gozo, minimum qualifying) | €8,750 |

| Health insurance (single person) | €900 |

| Permit renewal fees | ~€300 |

| Total minimum annual obligation | ~€24,950 |

Add living expenses on top — Malta costs roughly 27% less than the US — and a single person can live comfortably for €2,500–€3,500/month total including rent. That’s €30,000–€42,000/year for a genuinely high quality of life in a Mediterranean EU country where English is an official language. For context, €2,500/month in Malta buys a nicer lifestyle than $5,000/month in most US coastal cities.

The No-Minimum-Stay Rule (And What It Actually Means)

Here’s what makes the GRP unusual compared to virtually every other EU residency programme: there’s no minimum number of days you must spend in Malta. Portugal’s D7 visa, Spain’s Non-Lucrative Visa, Italy’s elective residency — all require you to base yourself in the country for the majority of the year. The GRP doesn’t.

The one restriction: you cannot spend 183 or more days in any other single country during the year. That rule prevents you from becoming tax resident somewhere else while holding Maltese GRP status. But you can freely split time between Malta, other EU/Schengen countries (using your Schengen permit), and non-EU destinations — as long as no single other country captures 183+ days of your year.

For location-independent earners, this structure is unusually flexible. You maintain EU residency, hold a Schengen permit, pay your €15,000 minimum tax, and travel freely for the other 11 months of the year. No one’s checking whether you spent 180 days in Malta or 20.

The Schengen Card: What You’re Actually Buying

The GRP residence permit functions as a Schengen visa. In practice, this means:

- Visa-free entry across all 26 Schengen zone countries

- 90-day stays in any Schengen country per 180-day period (beyond Malta itself)

- Travel across the EU without border queues, embassy appointments, or visa applications

- A credible legal address for banking, brokerage, and business purposes inside the EU

That last point matters more than most people realise. European brokerage accounts, EU banking with SEPA/IBAN access, and business relationships in the EU all get substantially easier once you hold legal residency in an EU member state. Malta’s English-speaking legal and financial services sector is particularly well-equipped to handle international clients — it’s been a wealth management hub for decades.

US Expat Tax Considerations

The GRP doesn’t exempt you from US obligations. As a US citizen or Green Card holder, you still file with the IRS annually and report worldwide income. The key tools available to you:

Foreign Earned Income Exclusion (FEIE): If you qualify under the bona fide residence or physical presence tests, you can exclude up to $130,000+ of earned income from US taxable income. The GRP’s flexible residency structure helps here — you can establish genuine Maltese bona fide residence while still travelling extensively. Full breakdown in our FEIE guide.

Foreign Tax Credit (FTC): The 15% Maltese tax you pay can be credited against your US tax liability on that same income. If your effective US rate exceeds 15%, you owe the difference to the IRS. If it’s under 15% — common with capital gains — no additional US tax may be owed. The FEIE vs. FTC decision is consequential here; see the complete US expat tax guide for scenario analysis.

FBAR and FATCA: Maltese bank accounts must be reported if balances exceed $10,000 at any point during the year. Standard expat compliance — not unique to Malta, but not optional either.

To maintain US banking and investing access while abroad, a Mercury account works well for business banking, and a Charles Schwab International account handles investing and ATM access globally without fees. You’ll also want a US street address for IRS correspondence — a Traveling Mailbox virtual address handles this cleanly for $15/month and forwards physical mail digitally.

For international money transfers between your Maltese account and US accounts, Remitly handles EUR/USD transfers with transparent rates.

Who the Malta GRP Makes Sense For

The GRP is expensive compared to zero-tax jurisdictions. At €15,000/year minimum in tax plus ~€25,000+ in total annual obligations, it doesn’t compete on raw cost with Georgia’s 1% or Paraguay’s no-tax setup. But those places don’t give you EU residency and Schengen access. Here’s who the GRP genuinely serves:

- High passive income earners ($200K+): At that income level, you’re paying 15% on whatever you choose to remit, keeping the rest offshore untaxed. The effective rate on total income can be very low depending on how much you remit.

- Investors approaching major liquidation events: The foreign capital gains exemption makes Malta particularly attractive when you’re selling a business, liquidating a property portfolio, or exiting a large crypto position. No Maltese capital gains tax on whatever you bring in.

- Remote consultants and business owners wanting EU access: EU residency opens the entire Schengen zone to extended stays, simplifies EU banking and business registration, and adds credibility to European business relationships.

- Retirees with foreign pensions and passive income: If retirement income sits in offshore accounts and you’re selective about what you remit each year, you might pay close to the €15,000 minimum while living on €35,000–€50,000 in actual annual spending.

The GRP is less compelling for:

- Earners below $100K — the fixed costs absorb a disproportionate share of income

- US citizens whose effective all-in tax rate is already below 15% — the FTC credit advantage diminishes

- People who want to fully settle in one European city — the structure suits mobile, semi-nomadic earners more than people genuinely putting down roots

Malta GRP Versus Other EU Options

The GRP sits in an interesting middle position among European tax residency programmes:

Greece’s €100K Non-Dom: Greece charges a flat €100,000/year minimum tax — more than 6x Malta’s floor — but that €100K covers all foreign income regardless of amount or what you remit. For someone remitting €1M+ per year, Greece’s effective rate undercuts Malta’s 15%. For everyone else, Malta is dramatically cheaper. Covered in full at the geographic arbitrage playbook.

Portugal NHR 2.0: The programme was overhauled and is now restricted to specific professions — researchers, qualified workers in designated “high value” activities — at 20%. The old programme’s broad non-dom accessibility is gone. Malta’s GRP has no profession restrictions and is open to any qualifying non-EU national.

Cyprus Non-Dom: Zero dividend and interest tax for 17 years, corporate tax at 12.5%. The catch: Cyprus is EU but not Schengen (Cyprus has been in accession discussions but is not in Schengen as of mid-2026). Malta gives you the Schengen permit Cyprus cannot provide.

Malta’s Own MPRP: The Malta Permanent Residence Programme offers true permanent residency — not annually renewed — for a one-time investment of €37,000+ in government contribution plus property purchase from €375,000. But MPRP carries no special tax status. You’d owe standard Maltese income tax rates, not the GRP’s 15% flat. Different tools for different goals.

Application Process and Timeline

Applications must go through a licensed Maltese agent — you cannot apply directly. The process typically runs 3–6 months:

- Engage a licensed Maltese intermediary (law firm or licensed agent)

- Submit application with proof of qualifying property (lease or purchase contract), valid health insurance, clean criminal background check, and evidence of financial means

- Pay the €6,000 non-refundable admin fee by bank draft

- Tax authority reviews application and issues the special tax status certificate

- Collect the annual residence permit from Identity Malta

- File first Maltese tax return and pay minimum €15,000

Agent fees typically run €2,000–€5,000 depending on complexity. Total first-year cost including admin fee, agent, and first year’s minimum tax: approximately €23,000–€26,000 before living expenses.

The Bottom Line

Malta’s Global Residence Programme costs more than zero-tax havens. That’s the whole point. You’re paying a premium for something no low-tax jurisdiction outside the EU can offer: a real EU residency card, a Schengen permit, and a legal base inside the world’s largest single market — with a 15% flat tax ceiling on everything you choose to bring in and zero tax on whatever you don’t.

For a US expat with significant foreign passive income, a capital gains event on the horizon, or a genuine need for EU mobility, the GRP’s structure can be highly efficient — especially when the foreign capital gains exemption and no-inheritance-tax rules are in play. For everyone else, Georgia’s 1% or Paraguay’s territorial system probably wins on pure cost.

The GRP isn’t the cheapest option. It’s the EU option. That’s a different product for a different buyer.

Disclaimer: This post is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and residency programme terms change frequently. Consult a licensed international tax professional and immigration attorney before making any decisions regarding residency restructuring or international tax planning.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.