Expat Tax Services Ranked: Which One Actually Files Right

10 min read · 2,380 words

Here’s a number that should make you uncomfortable: the IRS assesses a minimum $10,000 penalty per foreign account per year for an unfiled FBAR — even when the failure is accidental. TurboTax cannot file an FBAR. Neither can most domestic tax software. And yet, millions of Americans living abroad keep using the same tools they used back home, blissfully unaware of what they’re not filing.

Expat taxes aren’t just “complicated.” They involve a completely different stack of IRS forms — Form 2555 for the Foreign Earned Income Exclusion, Form 1116 for the Foreign Tax Credit, FinCEN 114 for FBAR, Form 8938 for FATCA, and potentially Form 5471 or 5472 if you run a foreign or US company abroad. Getting the wrong software means those forms either don’t get filed, get filed incorrectly, or you pay a CPA $500/hour to clean up the mess.

This is a complete, opinionated breakdown of every major US expat tax service — what they cost, what they can actually file, and who each one is right for.

Why TurboTax and H&R Block Fail US Expats

Domestic tax software is built for the 330 million Americans who live in the US. Expat-specific scenarios — bona fide residence test, physical presence test, housing exclusion calculations, totalization agreements — are afterthoughts at best. At worst, they’re flat-out missing.

The core issue is the Foreign Earned Income Exclusion (FEIE). For tax year 2025, the FEIE lets qualifying expats exclude up to $130,000 of foreign-earned income per person from US taxes. A married couple where both spouses work abroad can exclude up to $260,000. Miss this exclusion and you’re paying US federal income tax on your entire salary — on top of whatever you already paid locally.

TurboTax technically supports Form 2555 (FEIE) in its premium tiers, but it struggles with edge cases: housing exclusion calculations, self-employed expats with Schedule SE complications, and anyone triggering the “Roth IRA trap” where the FEIE reduces earned income to zero and kills your contribution eligibility. And it cannot file FinCEN 114 (FBAR) at all — that requires a completely separate system (BSA E-Filing), which many expats never even discover exists.

H&R Block’s expat offering is marginally better — their online expat service starts around $200–$250 and adds FBAR support. But their FEIE calculation is often boilerplate, and complex situations (foreign pension contributions, CFC reporting, PFIC holdings) require escalating to their “expat CPA” tier, which can run $500+ with no published pricing.

The better play is to start with a purpose-built expat service from day one.

Five Expat Tax Services, Ranked

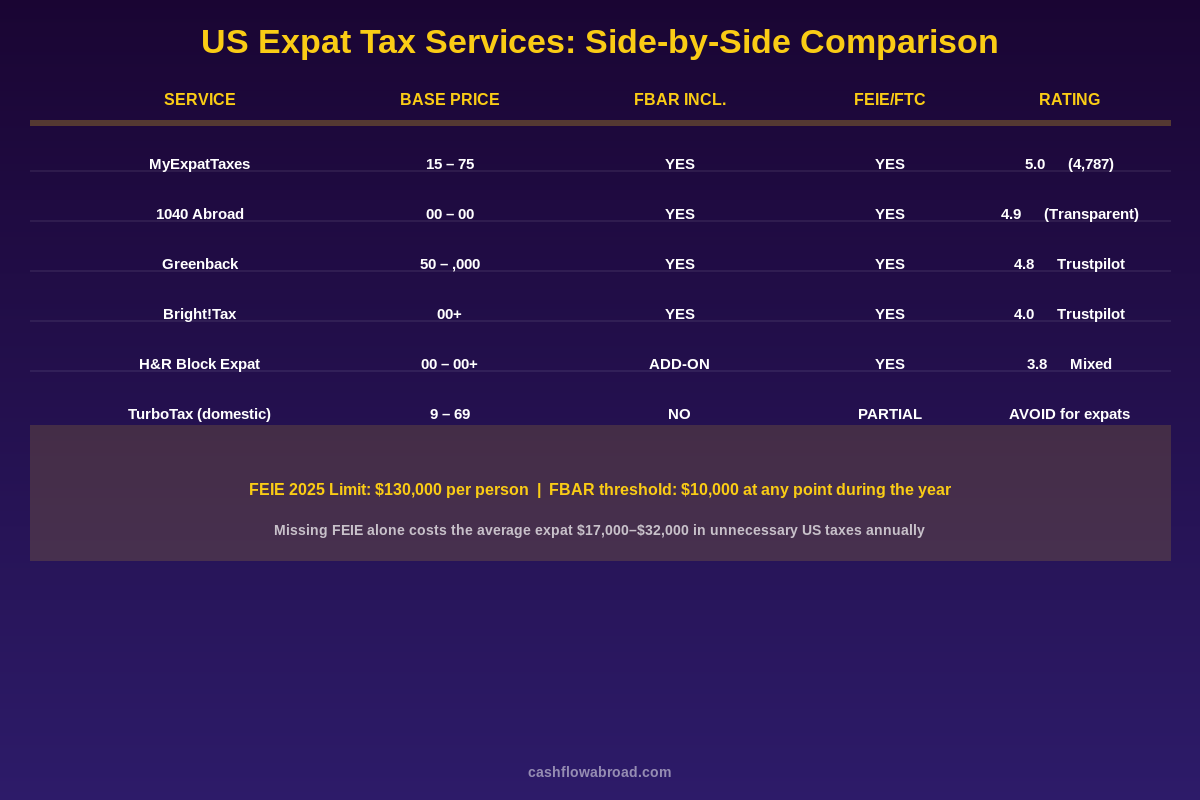

1. MyExpatTaxes — Best for Most Expat Employees

Price range: $115 (Basic) → $575 (Premium)

Trustpilot rating: 5.0 stars — 4,787 reviews

Model: Guided DIY software

MyExpatTaxes is the closest thing to TurboTax built specifically for expats. You answer interview-style questions and the software handles the FEIE, Foreign Tax Credit, FBAR, FATCA (Form 8938), and PFIC reporting (Form 8621) as an add-on in the Premium tier.

The $115 Basic tier handles straightforward returns: single income source, FEIE, FBAR. The $275 Standard tier adds foreign investment income and the Foreign Tax Credit. Premium at $575 adds Form 5471 (foreign corporation) and PFIC reporting via Form 8621.

The critical limitation: MyExpatTaxes cannot file Form 5472, the reporting form required for foreign nationals who own a US LLC. If that’s your situation, this is a hard stop.

For a W-2 or freelance expat with a clean setup — no foreign companies, no complex investments — MyExpatTaxes at $275 is an exceptional deal. The 5.0 Trustpilot rating across nearly 5,000 reviews isn’t marketing copy; it’s a genuine signal of product quality. And the math is obvious: the FEIE alone at $130,000 per person can save a single expat $17,000–$30,000 in federal taxes annually depending on bracket. Paying $275 to correctly claim it is the highest-ROI transaction in expat personal finance.

2. 1040 Abroad — Best for Transparent, Flat-Fee Pricing

Price range: ~$300 (simple returns) → $900 (non-resident LLC with Form 5472 + FBAR)

Rating: 4.9 stars, widely praised for pricing transparency

Model: CPA-prepared, flat fee per form

1040 Abroad operates differently from most services: they publish a flat fee for every form. No “get a quote” friction, no pricing surprises after you’ve submitted your documents. This is rare in an industry where competitors routinely use bait-and-switch pricing — advertise a $250 base fee, then discover your situation requires six add-on forms.

Their non-resident LLC package (Form 5472 + FBAR) runs around $900 — making them one of only two services (alongside Greenback) equipped to handle this specific filing requirement that trips up foreign nationals with US entities.

They also handle streamlined procedures for expats catching up on unfiled years, foreign corporation reporting, and treaty-based positions. For a CPA-prepared return at transparent pricing, 1040 Abroad punches significantly above its price point.

3. Greenback — Best Full-Service CPA Experience

Price range: $450 (base return) → $1,000+ (complex/LLC returns)

Trustpilot rating: 4.8 stars

Model: Dedicated CPA-prepared returns

Greenback is one of the oldest and largest dedicated expat tax firms. Every return is prepared by a licensed CPA or EA — you’re assigned a dedicated preparer, not routed to whoever’s available. This matters when your situation requires judgment calls: which method (FEIE vs FTC) saves you more this year? Does your housing exclusion apply to your lease arrangement? Should you enter the streamlined procedure or file amended returns?

Base pricing starts at $450 for a standard expat return, which includes FEIE, FTC, and FBAR. Form 5472 (non-resident LLC) brings the total to $800–$1,000. Streamlined procedures for non-filers are priced separately and typically run $1,500+.

Where Greenback earns its premium: genuinely complex situations. Foreign pensions, passive foreign investment companies (Form 8621 — easily a $400–$600 add-on), controlled foreign corporations (Form 5471 can run $680–$1,000 for this form alone), and multi-jurisdiction tax treaty analysis. If you’re pulling income from three countries, hold shares in a foreign company, and own a UK pension, Greenback is the service that can handle all of it in a single engagement without subcontracting the hard parts.

See also: the PFIC trap explainer for why holding foreign mutual funds creates a reporting nightmare — and why Form 8621 is non-negotiable if you do.

4. Bright!Tax — Premium Positioning, Variable Execution

Price range: $800+ (base) → $1,860+ (streamlined procedures), $280 per 30-min CPA consultation

Trustpilot rating: 4.0 stars (lowest among dedicated expat firms)

Model: CPA-prepared, personalized quote

Bright!Tax markets itself as a premium, white-glove expat tax service. Their base returns start at $800, CPA consultations run $280 for 30 minutes, and the Streamlined Foreign Offshore Procedure starts at $1,860. They handle Form 5471 for foreign corporate reporting at $680+.

The quality floor is genuinely high — most Bright!Tax CPAs are expert in expat tax law, and their published content on IRS updates is among the better free resources available. The issue is consistency. A 4.0 Trustpilot rating isn’t terrible, but when competitors in the same space run 4.8–5.0, the gap warrants scrutiny. Common complaints: communication delays and pricing surprises after document submission. For $800+ base, zero pricing surprises should be the baseline expectation.

Bright!Tax is a defensible choice if a specific CPA there comes recommended from someone whose situation mirrors yours. As a cold selection, the price-to-rating ratio is harder to justify versus Greenback or 1040 Abroad at the same complexity level.

5. H&R Block Expat — Acceptable for Simple Returns Only

Price range: ~$200 (online expat service) → $500+ (CPA tier)

Rating: 3.8 stars among expat users

Model: Online software + optional CPA upgrade

H&R Block’s expat offering works for exactly one profile: a US employee on foreign assignment with a single W-2, standard FEIE, and FBAR. At $200 for the online service with FBAR included, it undercuts most competitors by a wide margin.

The drop-off comes fast. Housing exclusion calculations, self-employed Schedule C, foreign pensions, anything touching Form 5471 or 8621 — all push you into their premium CPA service with quote-based pricing that can rival Greenback without Greenback’s specialization depth.

For anyone beyond the simplest expat situation, H&R Block Expat is a lateral move from TurboTax, not an upgrade.

The Six Forms That Domestic Software Can’t Handle

Understanding which forms your situation triggers helps you pick the right service tier — and avoid expensive gaps.

| Form | What It Is | Who Needs It | Penalty for Missing |

|---|---|---|---|

| Form 2555 | Foreign Earned Income Exclusion | Any expat with foreign-earned income | $17K–$30K+ in excess taxes annually |

| FinCEN 114 (FBAR) | Foreign Bank Account Report | Anyone with $10K+ in foreign accounts at any point | $10,000/account/year (non-willful) |

| Form 8938 (FATCA) | Statement of Foreign Financial Assets | Foreign assets over $200K abroad or $50K in US | $10,000 + $50,000 max for continued failure |

| Form 5471 | Foreign Corporation Disclosure | US persons with ≥10% stake in a foreign corp | $10,000 per year per form |

| Form 5472 | Foreign-Owned US LLC Disclosure | Non-resident foreign nationals owning a US LLC | $25,000 per return per year |

| Form 8621 | PFIC (Passive Foreign Investment Company) | Anyone holding foreign mutual funds or ETFs | Statute of limitations stays open; back taxes + interest |

The Form 5472 penalty is particularly severe: $25,000 per return per year. Foreign nationals who form Delaware or Wyoming LLCs for their online businesses are frequently unaware this form exists. The LLC formation agents don’t mention it, Stripe and Shopify don’t mention it, and domestic tax software literally cannot file it.

FEIE vs. Foreign Tax Credit: The $8,000 Decision

The choice between the Foreign Earned Income Exclusion and the Foreign Tax Credit is the most consequential tax decision most expats make — and the wrong choice is often permanent. Switching methods requires IRS permission and triggers a five-year lockout from the excluded method.

FEIE wins when: You’re in a low-to-medium tax country (Thailand, Mexico, Colombia, Southeast Asia, Eastern Europe). You exclude the income rather than waiting for a credit, which is cleaner and more predictable.

FTC wins when: You’re in a high-tax country (UK, Germany, France, Australia, Japan). If you paid 40% to HMRC, that credit offsets your US liability dollar-for-dollar. Taking the FEIE instead means you lose the credit on that income permanently and may end up paying both countries.

The worst outcome: taking the FEIE in a high-tax country and generating excess foreign tax credits you can’t apply. The second-worst: taking the FTC in a low-tax country and paying more US tax than the exclusion would have required.

A competent expat tax service will model both scenarios annually. If yours doesn’t proactively run this comparison, ask explicitly. See the full FEIE guide for the mechanics, or the complete expat tax overview for the broader framework.

Catching Up: The Streamlined Filing Procedure

A significant portion of American expats haven’t filed US taxes in years — some because they didn’t know they were required to, others because they moved abroad without understanding that citizenship-based taxation follows you everywhere. If that’s you, the IRS Streamlined Foreign Offshore Procedure is the primary path back to compliance — and it’s more forgiving than it sounds.

The procedure requires filing three years of back tax returns plus six years of FBARs. The penalty structure is dramatically lighter than standard delinquency: 0% penalty for the Streamlined Foreign Offshore Procedure (available to expats living abroad, versus the 5% rate for US residents using the domestic version).

Services that handle streamlined filings:

- Greenback: $1,500+ depending on complexity

- 1040 Abroad: Flat-fee per year of returns

- Bright!Tax: Starts at $1,860

- MyExpatTaxes: Limited support; complex cases require CPA referral

The window for favorable streamlined treatment doesn’t stay open indefinitely. If the IRS contacts you first, the program is no longer available. Acting before that point is both legally and financially the right move.

When Crypto Gets Involved

If you hold or trade crypto as an expat, you have a compounding compliance issue. The IRS treats cryptocurrency as property, meaning every sale, trade, or swap triggers a taxable event. Critically: crypto gains are generally classified as investment income, not earned income — so the FEIE does not exclude them. You can be completely tax-free on your $130,000 salary via FEIE and still owe US capital gains tax on a $30,000 crypto gain.

Reporting crypto correctly requires cost-basis tracking across potentially dozens of wallets and exchanges over multiple years. Most expat tax services accept a consolidated export from a dedicated crypto tax tool rather than reconstructing every transaction manually.

CoinTracking is the tool most expat CPAs prefer — it connects to 110+ exchanges and wallets, calculates gains using FIFO/LIFO/HIFO methods, and exports IRS-ready Form 8949 data. See the full crypto expat tax breakdown for the complete picture.

Keeping Your US Financial Infrastructure Intact

A tax service handles your annual filing. Your US financial infrastructure — banking, brokerage, credit — requires separate maintenance that most expats neglect until it’s too late.

Brokerages like Charles Schwab International — the most consistently recommended brokerage for expats, with free worldwide ATM reimbursements and maintained US account access for non-residents — require a valid US mailing address on file. When that address disappears (because you closed your US PO box, or your family stopped receiving mail), accounts get flagged and eventually closed without warning.

A virtual mailbox like Traveling Mailbox ($15/month) provides a real US street address in 50+ cities, mail scanning, and check deposit capabilities. It maintains IRS address compliance, state domicile documentation for taxes, and brokerage account access while abroad. Without it, you’re one account closure notice away from a frozen investment account you can’t log into from your country. The site owner uses Traveling Mailbox specifically for this reason.

Quick Decision Framework

| Your Situation | Best Service | Expected Cost |

|---|---|---|

| Employee abroad, single income, FEIE + FBAR | MyExpatTaxes Standard | $275 |

| Freelancer/contractor, self-employed abroad | MyExpatTaxes Premium or 1040 Abroad | $300–$575 |

| Foreign national with US LLC (Form 5472) | 1040 Abroad or Greenback | $800–$1,000 |

| US person with 10%+ stake in foreign company | Greenback or Bright!Tax | $1,000–$1,500+ |

| Multi-country income, foreign pension, PFIC holdings | Greenback | $1,000–$2,000+ |

| Non-filer catching up (streamlined procedure) | 1040 Abroad or Greenback | $1,500–$2,500 |

| Simple W-2, budget-conscious, low-tax country | H&R Block Expat online | $200–$250 |

Bottom Line

The US expat tax obligation isn’t optional, and the penalty structure for getting it wrong is severe enough that a dedicated service pays for itself in a single year — often several times over. The FEIE alone saves most expats more than their entire annual prep fee. The FBAR penalty avoided by filing correctly is $10,000 per account. The Form 5472 penalty skipped is $25,000 per return.

For most expats without complex entity structures, MyExpatTaxes at $275–$575 is the starting point — 5.0 stars across nearly 5,000 reviews earns that default recommendation. For anything involving foreign corporations, US LLCs held by non-resident persons, or multi-year non-filing, go directly to 1040 Abroad or Greenback. Either way, don’t use domestic software for a situation it wasn’t designed to handle. The downside is not worth the $100 you save on preparation fees.

Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. US expat tax law is complex and situation-specific. Consult a licensed CPA or Enrolled Agent for guidance on your individual circumstances. All pricing figures are approximate and subject to change — verify current pricing directly with each service provider.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.