Roth IRA for US Expats: The FEIE Trap & Backdoor Strategy

That's right. For most expats, it's not a tradeoff anyone warns them about before they file. The IRS isn't hiding this. Full stop.

That's right. For most expats, it's not a tradeoff anyone warns them about before they file. The IRS isn't hiding this. Full stop.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Here's the most expensive mistake US expats make with their retirement accounts: They use the Foreign Earned Income Exclusion — the single most popular expat tax strategy, saving thousands of dollars per year — and in doing so, they unknowingly make themselves ineligible to contribute a single dollar to a Roth IRA for that same year.

That's right. The tax strategy that saves you $10,000–$30,000+ per year in US income taxes also wipes out your ability to fund the most powerful tax-free retirement account in the US tax code. For most expats, it's not a tradeoff anyone warns them about before they file.

The IRS isn't hiding this. It's buried in IRC Section 219(d), which states that the IRA contribution limit is reduced — dollar for dollar — by any income excluded under the FEIE or the foreign housing exclusion. Exclude $132,900 in earned income (the 2026 FEIE limit)? Your Roth IRA contribution limit is now zero. Full stop.

Related: expat 401k and IRA guide

But here's the counterintuitive twist that most expat CPAs — let alone the expats themselves — don't know about: the same FEIE that blocks Roth contributions secretly unlocks something potentially more powerful: tax-free Roth conversions. When your FEIE exclusion zeroes out your taxable income, your standard deduction becomes a weapon. A modest one — but over a decade, it compounds into a substantial Roth IRA balance you never paid a cent of US tax to build.

This post is the complete guide. We'll cover the FEIE trap, the FTC alternative that preserves Roth eligibility, the backdoor Roth strategy (and when the pro-rata rule blows it up), the tax-free conversion hack, and which countries protect your Roth's tax-free status in retirement — and which ones quietly tax it anyway.

Why Roth IRAs Matter More When You're Abroad

Before diving into the strategies, let's establish why this matters so much for expats specifically.

The Roth IRA is unusual in the US tax code: you contribute after-tax dollars, the account grows completely tax-free, qualified withdrawals in retirement are tax-free, and — unlike traditional IRAs and 401(k)s — there are no required minimum distributions during your lifetime. That last point is enormous for estate planning flexibility.

For expats with long time horizons, this is potentially the most valuable retirement account available. Someone who moves abroad at 30 and doesn't plan to retire until 65 has 35 years of tax-free compounding. At a modest 7% average annual return, $100,000 invested at 30 becomes roughly $1.07 million by 65 — all of it tax-free on the US side.

The 2026 contribution limit is $7,500 per person per year (or $8,600 if you're 50 or older). Married couples can contribute $15,000–$17,200 annually combined. Over decades of expat life, the missed contributions from FEIE-blindness add up to a devastating retirement shortfall.

Your existing Roth IRA doesn't close when you move abroad. The account stays open, keeps growing tax-free, and you can manage it from anywhere in the world. The only question is whether you can keep contributing — and that depends entirely on your tax strategy.

The FEIE Trap: How America's Most Popular Expat Tax Move Kills Your Roth

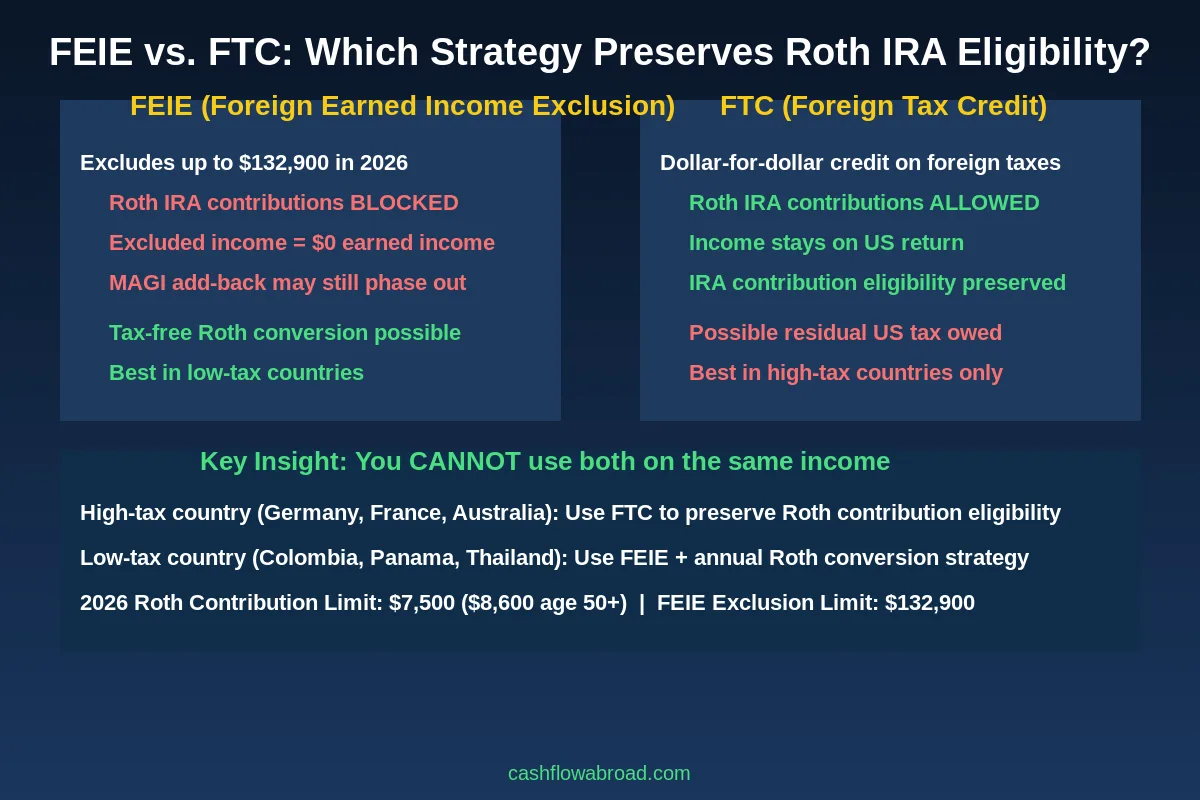

The Foreign Earned Income Exclusion is, without question, the most widely used expat tax strategy. In 2026, it allows US citizens and resident aliens who pass either the physical presence test (330 days outside the US in a 12-month period) or the bona fide residence test (established residence in a foreign country) to exclude up to $132,900 in foreign-earned income from US federal income tax.

For most expats earning under $132,900 abroad, this effectively means a $0 US federal income tax bill. It's the strategy that makes expat life financially attractive — and it's why so many people pile into it without reading the fine print.

The fine print is IRC Section 219(d)(1), which reduces your maximum IRA contribution by "any amount excludable from gross income under section 911." That's the FEIE. The exclusion isn't just invisible to the IRS for income tax purposes — it's invisible for IRA contribution purposes too.

Real example: Sofia is a US citizen freelance consultant living in Medellín, Colombia. She earns $85,000 per year in consulting fees. She uses the FEIE to exclude the full $85,000. Her US taxable income: $0. Her Roth IRA contribution limit: $0. She has no "earned income" left for IRA purposes, because the IRS effectively pretends that $85,000 never existed after she excluded it.

If Sofia contributes $7,500 to her Roth IRA anyway — which many expats do out of habit or ignorance — she faces a 6% excess contribution penalty on that $7,500. Every year the excess sits there uncorrected, she owes another $450. Over five years, that's $2,250 in penalties on money she thought was building her retirement nest egg.

The MAGI Double-Whammy

The trap has a second jaw. Even if Sofia leaves some income un-excluded (say, she uses partial FEIE or has some US-source income), the IRS adds back excluded FEIE income when calculating Modified Adjusted Gross Income (MAGI) for Roth IRA phaseout purposes.

The Roth IRA direct contribution phaseout for single filers in 2026 begins at $150,000 MAGI and eliminates eligibility completely at $165,000. For married filing jointly, the phaseout runs from $236,000 to $246,000.

Example: Marcus earns $160,000 abroad, uses the full FEIE to exclude $132,900, leaving $27,100 in taxable income. His contribution limit based on earned income? $7,500 (since he has $27,100 remaining). But his MAGI for phaseout purposes? $160,000 — because the IRS adds the excluded $132,900 back. At $160,000 MAGI (above the $150,000 phaseout threshold), Marcus is partially phased out, limiting him to a fraction of the full $7,500 in Roth contributions.

This is the MAGI double-whammy: the exclusion reduces earned income available for contributions AND inflates MAGI for phaseout calculations simultaneously. It takes a bite from both ends.

The FTC Alternative: How to Preserve Roth IRA Eligibility

Here's where expat tax strategy gets strategic rather than just mechanical: the Foreign Tax Credit (FTC) is an entirely different approach that sidesteps the FEIE trap entirely.

Instead of excluding foreign income from your US return, the FTC lets you claim a dollar-for-dollar credit against your US tax bill for income taxes you've already paid to a foreign government. Your foreign-source income stays on your US tax return — it counts as earned income — but it's offset by the credit so you often owe little or nothing to the IRS.

Because the income stays on your return, it remains "earned income" for IRA contribution purposes. The MAGI calculation for Roth phaseouts doesn't artificially inflate. If your FTC fully offsets your US tax liability, you can contribute the full $7,500 to a Roth IRA with no penalty risk.

Related: FEIE zero tax guide

The FTC is generally superior for expats in high-tax countries — Germany (top marginal rate: 45% + solidarity surcharge), France (45%), Australia (45%), the UK (45%), Nordic countries (50%+). When the foreign tax rate equals or exceeds the US rate, the FTC wipes out US tax completely, and you're left with full IRA contribution eligibility at zero additional US cost.

The trade-off: in low-tax countries (Colombia, Panama, Thailand, Paraguay), the foreign tax rate may be much lower than the US rate. The FTC doesn't generate enough credit to fully offset US taxes, meaning you'll owe some to the IRS. In these situations, the FEIE's blanket exclusion is usually more valuable financially — but you sacrifice Roth contributions in exchange.

Critical rule: you cannot use both the FEIE and FTC on the same income in the same year. You have to choose. You can switch strategies year to year (subject to a 5-year moratorium if you revoke the FEIE election), but you can't double-dip.

| Factor | FEIE Strategy | FTC Strategy |

|---|---|---|

| Roth IRA contributions | Blocked (excluded income = $0 earned) | Allowed (income stays on return) |

| US tax bill (low-tax country) | $0 (income fully excluded) | Possible residual US tax owed |

| US tax bill (high-tax country) | Possible US tax on earnings above FEIE cap | Often $0 (foreign tax credit offsets) |

| Best for | Low-tax countries (Colombia, Panama, Thailand) | High-tax countries (Germany, France, UK, Australia) |

| Roth conversion opportunity | Yes — deduction surplus enables tax-free conversions | Less deduction surplus available |

| MAGI for Roth phaseout | Inflated (FEIE add-back applies) | Not inflated (income already on return) |

| 2026 FEIE exclusion limit | $132,900 | N/A (credit-based, no exclusion cap) |

If you're currently using the FEIE and want to switch to FTC, note that once you revoke the FEIE election, you're generally barred from re-electing it for 5 years without IRS permission. This makes the FEIE-to-FTC switch a significant long-term commitment. Plan accordingly — and consult a qualified expat tax professional before making the switch.

For a full breakdown of how these strategies interact with your broader tax picture — including FBAR and FATCA reporting obligations — see our complete US expat banking and taxes guide.

The Hidden Gem: Tax-Free Roth Conversions Under the FEIE

Now we get to the counterintuitive gem that most expat CPAs don't talk about — even the ones who know about the FEIE trap.

When you use the FEIE to exclude all of your earned income, something mathematically interesting happens: your taxable income drops to zero, but your standard deduction doesn't disappear. In 2025, the standard deduction is $15,750 for single filers and $31,500 for married filing jointly. You've excluded your earned income, but you still get to subtract the standard deduction — from your taxable income of $0.

This creates a "deduction surplus." Your standard deduction now has nothing to offset against your earned income. But it can offset other types of income — including a Roth IRA conversion.

A Roth conversion is the process of moving money from a pre-tax retirement account (traditional IRA, old 401(k), SEP-IRA) to a Roth IRA. The converted amount is treated as ordinary income in the year of conversion — but if that income falls within your unused standard deduction, the US tax owed is zero.

Here's the math for a single FEIE filer in 2025:

- Foreign earned income: $95,000 (fully excluded by FEIE)

- US taxable income after FEIE: $0

- Standard deduction available: $15,750

- Roth conversion amount: $15,750

- Net taxable income: $15,750 – $15,750 = $0

- US federal income tax on conversion: $0

A married couple using the full FEIE can convert up to $31,500 per year at zero US federal tax using their combined standard deduction.

Over a decade, a single filer converting $15,750 per year into a Roth IRA — with those funds growing at 7% annually — accumulates roughly $218,000 in Roth assets by year 10, all with zero US income tax paid on the conversions. That's the power of the deduction surplus compounded over time.

Important Caveats to Know

Investment income eats the surplus first. If you have dividend income, capital gains, rental income, or interest income — even from foreign accounts — this income is added to your taxable income before the standard deduction can be applied. If you have $10,000 in dividend income, your deduction surplus for conversions drops from $15,750 to $5,750 (as a single filer). Plan the conversion amount carefully each year.

Form 8606 is mandatory. Every Roth conversion must be reported on Form 8606. Failing to file this form creates a nightmare scenario where the IRS has no record that the conversion occurred — meaning your future withdrawals could be treated as taxable income. File Form 8606 religiously, every year you make a conversion.

December 31 deadline. Roth conversions must be completed by December 31 of the tax year — unlike contributions, which have until the tax filing deadline (typically April 15). Don't wait until spring to execute your annual conversion.

State tax may still apply. If you maintain a state of domicile (required for US banking, driver's license, voter registration, etc.), some states tax Roth conversions even when the federal tax is zero. States with no income tax — Texas, Florida, Nevada, South Dakota, Wyoming, Washington — are expat-friendly for this reason. A virtual US mailbox in a no-income-tax state can help you establish and maintain domicile in a favorable state while living abroad.

Maintaining a proper US address is also essential for keeping your US brokerage accounts open. Charles Schwab International is one of the few major brokerages that actively supports expats and won't close your account simply because your address updates to a foreign one. Services like Traveling Mailbox give you a real US street address in 50+ cities with mail scanning and check deposits for about $15/month — invaluable for maintaining state domicile and IRS correspondence while abroad. We covered this in detail in our virtual mailbox expat guide.

The Backdoor Roth for Expats: When It Works and When It Explodes

The backdoor Roth IRA is a well-known workaround for high earners who exceed the Roth IRA income limits. The strategy involves making a non-deductible contribution to a traditional IRA (which has no income limit) and then immediately converting it to a Roth IRA. Since the contribution was non-deductible (after-tax), only investment gains between contribution and conversion are taxable — in practice, essentially nothing if you convert immediately.

For expats, the outcome depends entirely on which tax strategy you're using:

Related: expat investing playbook

Scenario 1: FEIE Expat — Backdoor Roth Is Largely Blocked

If you're using the FEIE and excluding all earned income, you have zero earned income for IRA contribution purposes. You can't make a traditional IRA contribution — deductible or non-deductible — without earned income. The backdoor strategy requires a valid IRA contribution as its first step, so if the FEIE eliminates all your earned income, the whole mechanism falls apart before it begins.

The exception: if you have some remaining earned income after partial FEIE (for example, you earn $150,000 and only exclude $132,900, leaving $17,100 in earned income), you have enough to make the $7,500 contribution. The MAGI phaseout may still affect direct Roth contributions if MAGI is above $150,000 (as it typically would be given the add-back), but the backdoor route sidesteps the phaseout entirely — that's its purpose.

Scenario 2: FTC Expat — Backdoor Roth Works, But Watch the Pro-Rata Rule

If you're using the FTC, your earned income stays on your return. You have earned income for IRA purposes, and if your MAGI exceeds the Roth direct contribution phaseout threshold, the backdoor Roth is available and clean in principle.

But here's where a seemingly small detail can explode into a massive unexpected tax bill: the pro-rata rule.

The pro-rata rule (from IRC Section 408(d)(2)) says that when you convert any portion of an IRA to Roth, the IRS treats all of your traditional/SEP/SIMPLE IRA balances as a single pool. The taxable portion of the conversion is calculated based on the ratio of pre-tax funds to total IRA funds across all of your IRAs combined.

Example of the pro-rata trap: You have a $300,000 rollover IRA from an old 401(k) — all pre-tax dollars. You make a $7,500 non-deductible (after-tax) IRA contribution and immediately try to convert just that $7,500 to Roth. Your total IRA balance is now $307,500, of which $7,500 is after-tax (2.4%) and $300,000 is pre-tax (97.6%).

When you convert the $7,500, the IRS treats 97.6% of it as taxable income — roughly $7,320 is immediately subject to tax. You've done a backdoor Roth conversion and paid tax on nearly all of it. The "backdoor" has been sprung. This is the pro-rata rule destroying an otherwise clean strategy.

The fix: Roll your pre-tax IRA balances into a current employer 401(k) or a solo 401(k) before executing the backdoor Roth. Once the pre-tax funds are in a 401(k) — which is explicitly excluded from the pro-rata calculation — your IRA holds only after-tax funds, and the conversion is fully tax-free. This rollover step is critical and widely missed.

Self-employed expats have a particular advantage here: a solo 401(k) (also called an individual 401(k) or i401k) can accept both employee contributions (up to $23,500 in 2026) and employer profit-sharing contributions (up to 25% of net self-employment income), and it can accept rollovers of pre-tax IRA funds, clearing the pro-rata deck for clean backdoor Roth contributions. It's one of the most powerful retirement structures available to self-employed expats and digital nomads.

For a broader look at expat investing and the PFIC rules that make most foreign mutual funds dangerous for Americans to hold, see our expat investor's playbook.

The Country Risk: Where Your Roth Stays Tax-Free (and Where It Doesn't)

Even if you successfully build a six- or seven-figure Roth IRA over decades of expat life, there's a retirement risk most people never think about until it's too late: your destination country may not recognize the Roth IRA's tax-free status.

The Roth IRA is a uniquely American tax construct. When you retire abroad, that country's tax authorities don't automatically defer to the IRS's determination that your Roth withdrawals are tax-free. Whether they honor it depends entirely on the specific provisions of the US tax treaty with that country — and many treaties are silent on Roth IRAs specifically.

Countries That Recognize the Roth IRA

A handful of countries have tax treaty provisions that explicitly or practically recognize US pension plan treatment, which covers Roth IRA distributions:

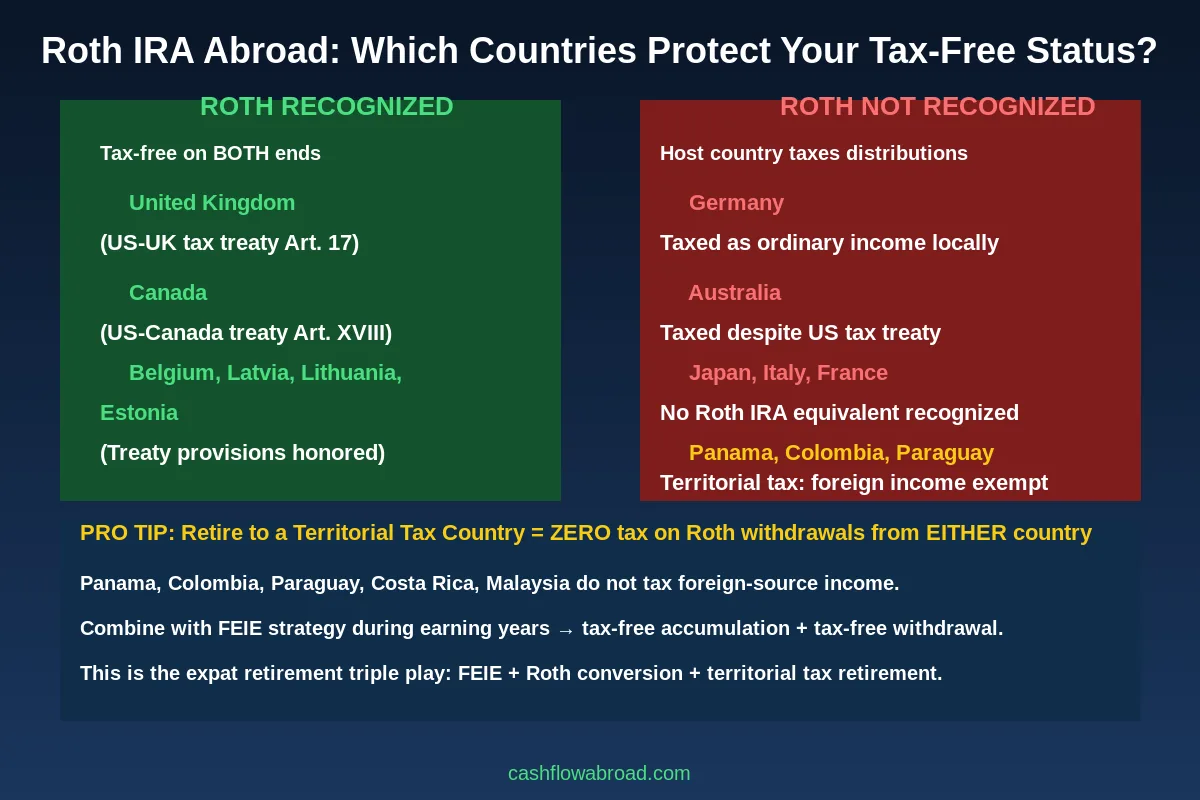

- United Kingdom: The US-UK tax treaty (Article 17) contains provisions that have been interpreted to protect Roth IRA distributions from UK income tax. This is an area of ongoing HMRC guidance, so professional advice is essential before relying on this protection.

- Canada: The US-Canada tax treaty (Article XVIII, paragraph 7) explicitly addresses Roth IRAs, allowing a Canadian resident to elect to defer Canadian tax on income accumulating in a Roth IRA. This is one of the clearest and most explicit treaty protections available for Roth IRAs anywhere in the world.

- Belgium, Latvia, Lithuania, Estonia: These countries have treaty provisions that have been interpreted to honor the Roth's tax-free treatment, though the analysis remains treaty-specific and highly fact-dependent.

Countries That Don't Recognize the Roth

Several major expat retirement destinations do not recognize the Roth IRA's tax-free status — with significant financial consequences:

- Germany: Germany taxes Roth IRA distributions as ordinary income at German income tax rates (up to 45% + the solidarity surcharge). If you retire in Germany with a $1 million Roth IRA and withdraw $50,000/year, you could owe substantial German tax on the full withdrawal — despite having already paid US taxes to build it over decades.

- Australia: Despite having a tax treaty with the US, Australia does not recognize Roth IRA distributions as tax-free. The Australian Tax Office treats them as taxable foreign pension income subject to Australian marginal rates (up to 45%).

- Japan and Italy: No recognition. Distributions are subject to local income tax as ordinary pension or foreign-source income.

- France: Nuanced position — some French tax guidance suggests limited treaty protection, but the default position is that US pension distributions are taxable at French rates.

The Territorial Tax Triple Play

Here's the geographic arbitrage play that makes the entire Roth strategy sing: retire to a territorial tax country.

Countries with territorial tax systems only tax income earned within their borders. Foreign-source income — including Roth IRA withdrawals — is simply not taxable, regardless of treaty provisions. Panama, Colombia, Paraguay, Costa Rica, Malaysia, and several others operate on territorial tax principles.

This creates the expat retirement triple play:

- Earning years: Use FEIE + tax-free Roth conversions to build Roth balance at $0 US tax.

- Accumulation years: The Roth grows tax-free inside the account indefinitely.

- Retirement in a territorial tax country: Withdraw Roth funds — $0 US tax (Roth is tax-free by definition), $0 local tax (territorial system ignores foreign-source income).

This is entirely legal. It's a matter of knowing the rules and planning accordingly — ideally decades in advance. Colombia is one of the most popular territorial tax destinations for US expats, with a low cost of living, good private healthcare, warm climate, and a maturing expat infrastructure. For a real-numbers breakdown of what life in Medellín actually costs, this detailed monthly budget breakdown at ColombiaMove.com covers the full picture.

Decision Framework: Which Strategy Is Right for You

Let's make this concrete with a decision table based on common expat scenarios:

Related: expat estate planning guide

| Your Situation | Recommended Strategy | Roth Vehicle |

|---|---|---|

| Low-tax country, earning under $132,900, clean IRA slate | FEIE + annual Roth conversion | Convert up to $15,750/year (single) at $0 US tax |

| High-tax country (Germany, France, Australia) | FTC to preserve contribution eligibility | Direct Roth contribution up to $7,500/year |

| Earning over $165K (single) / $246K (MFJ), using FTC | FTC + Backdoor Roth (clean IRA required) | Non-deductible IRA contribution → immediate Roth conversion |

| Self-employed, using FEIE, large pre-tax IRAs | Solo 401(k) + FEIE + Roth conversion | Roll IRAs into solo 401(k), then convert to Roth using deduction surplus |

| Planning to retire in Germany, Australia, Japan | Reconsider Roth-heavy strategy | Host country taxes Roth anyway; traditional IRA + FTC in retirement may be neutral |

| Planning to retire in territorial tax country (Panama, Colombia) | FEIE during earning years + Roth accumulation | Zero tax from both US and host country on Roth withdrawals in retirement |

No single strategy is universally optimal. The right approach depends on your income level, your country of residence, the specific tax treaty provisions between the US and that country, your existing pre-tax retirement balances, your expected retirement location, and your current marginal tax rate. A few hundred dollars spent on expat-specialist tax advice pays dividends worth thousands in avoided penalties and optimized retirement savings.

Practical Mechanics: Managing Your Roth IRA From Abroad

Even if the contribution and conversion questions are settled, expats face practical challenges managing Roth IRAs from overseas that stateside investors never encounter.

Which Brokerages Actually Support Expats?

Many US brokerages restrict or close accounts when they learn a customer has moved abroad. Fidelity and Vanguard have been particularly aggressive about limiting functionality or closing accounts for non-US residents. This is driven by regulatory compliance with MiFID II (EU rules on financial product marketing) and similar regulations elsewhere — brokerages don't want exposure to foreign financial regulations.

Charles Schwab International is the gold standard for US expats. They have a dedicated international division and explicitly serve US citizens abroad. You can maintain existing accounts and open new ones while living in most countries (a small number are restricted). Schwab also offers a checking account with fee-free ATM withdrawals worldwide — an underrated perk for expats who need local currency cash regularly.

For the Roth conversion strategy to work long-term, you need a brokerage that won't kick you out when your address changes to a Colombian or Thai one. Opening and maintaining your Schwab account before you move is the cleanest path. Their account was specifically designed for this kind of continuity.

Maintaining Your US Address and State Domicile

A US address is essential infrastructure for expat financial management. You need it for:

- Receiving tax documents (1099s, form 5498 for IRA contributions)

- Maintaining state domicile (for brokerage account retention)

- IRS correspondence

- Keeping banking and investment accounts open

- Receiving mail-forwarded checks and statements

A virtual mailbox service like Traveling Mailbox provides a real US street address (not a PO box) in over 50 cities across all 50 states, with mail scanning and forwarding, check deposit services, and about $15/month in cost. Choosing a state with no income tax — Texas, Florida, South Dakota, Nevada, Wyoming — means your virtual address also doesn't trigger state income tax obligations on your Roth conversions. This one detail is worth hundreds of dollars per year for active converters.

Reporting Requirements You Can't Ignore

Managing a Roth IRA abroad comes with tax forms beyond just your 1040:

- Form 8606: Required every year you make a non-deductible IRA contribution or a Roth conversion. This is the record that proves you've already paid tax on converted amounts. Failing to file creates double-taxation on future withdrawals. File it every single year.

- Form 5329: Required if you've made an excess contribution to your Roth IRA — for example, by accidentally contributing while using the full FEIE with no remaining earned income.

- FBAR (FinCEN 114): Required if your foreign financial accounts exceed $10,000. Your US Roth IRA is a US account and does not count toward FBAR — but your foreign bank accounts do.

- Form 8938 (FATCA): Required for foreign financial assets above $200,000 at year-end while living abroad. Again, your US Roth IRA doesn't count toward this threshold.

If you've accidentally contributed to your Roth IRA in a year when the full FEIE eliminated all your earned income, the fix is to withdraw the excess contribution plus earnings before the tax filing deadline (including extensions). After the deadline, the 6% annual penalty applies and Form 5329 must be filed. Address this immediately — it compounds every year uncorrected.

Long-Term Planning: Building a Roth-Centered Retirement Abroad

For expats whose careers will span decades abroad, the Roth vs. traditional IRA decision has retirement-destination implications that deserve early thinking.

If your plan is to eventually retire to a territorial tax country — Panama, Colombia, Costa Rica, Malaysia, Paraguay — the Roth is almost certainly the optimal retirement vehicle. You'll pay zero US tax on withdrawals (Roth is inherently tax-free) and zero local tax (territorial system ignores foreign-sourced income). The combination is the most tax-efficient retirement scenario legally available to US citizens anywhere in the world.

If you plan to retire in a non-recognition country — Germany, Australia, Japan — the calculus changes. The host country will tax your Roth distributions as ordinary income regardless of what the IRS says about them. In this case, a traditional IRA funded with pre-tax dollars, combined with the Foreign Tax Credit in retirement, might produce a comparable or better outcome. This is a planning question worth resolving long before retirement, not during it.

Geographic arbitrage isn't just about cutting living costs — it's about structuring the entire financial picture to legally minimize tax at every stage. See our geographic arbitrage playbook for a country-by-country breakdown of how this plays out across different financial profiles.

For health coverage during accumulation years, SafetyWing's Nomad Insurance offers solid international coverage starting around $50/month — particularly well-suited for expats who want flexible coverage without a long-term commitment to a single plan. For a comprehensive comparison of all expat health insurance options, see our expat health insurance guide.

For banking while building your Roth from abroad, Mercury offers an excellent US business banking option for self-employed expats and online business owners — fee-free, fully online, and designed for the kind of borderless financial life expats actually live.

Action Checklist: Your Roth IRA Roadmap as an Expat

Currently Living Abroad

- Identify your current strategy: Check your last tax return. Form 2555 = FEIE. Form 1116 = FTC.

- If using FEIE: Stop making direct Roth contributions if FEIE excludes all earned income. Calculate your deduction surplus for a tax-free conversion instead.

- If using FTC: Verify you have earned income on your return and check your MAGI against Roth phaseout thresholds. If above, evaluate the backdoor Roth — but audit pre-tax IRA balances for pro-rata contamination first.

- Inventory all pre-tax IRA balances across traditional, SEP, and SIMPLE IRAs. This determines your pro-rata exposure and whether you need to act before running a backdoor Roth.

- Open or confirm your Schwab International account is active and in good standing.

- Confirm your US address is in a no-income-tax state using Traveling Mailbox or an equivalent service.

- Plan your annual conversion amount by October — don't wait until December 31.

Planning to Move Abroad

- Max out Roth contributions this year while you're still US-resident and fully eligible.

- Research the US tax treaty with your destination country on pension plan recognition. If Roth isn't recognized (Germany, Australia), that affects your long-term strategy.

- Consider a Roth conversion blitz in low-income transition years — if you're taking a gap year, career break, or have a lower-income year before the move, convert aggressively while marginal rates are low.

- Open Schwab International and Traveling Mailbox before your address updates to a foreign one.

- Hire an expat-specialist CPA before filing your first return abroad — not a domestic generalist. The cost is a fraction of what an incorrect first filing can cost to unwind.

Conclusion: The Roth IRA Is Worth Pursuing Abroad — Just Not the Way Most People Think

The Roth IRA remains one of the most powerful retirement savings vehicles in the US tax code — arguably more powerful for long-term expats than for stateside Americans, given the time horizons and geographic arbitrage possibilities available. But it requires a fundamentally different approach when you're living abroad.

The FEIE trap is real, and it catches thousands of expats every year with excess contribution penalties and missed opportunities. The good news: the same exclusion that blocks direct contributions enables annual tax-free conversions — a strategy that, executed consistently, builds substantial Roth wealth without triggering a dollar of US income tax.

The framework, simplified:

- Low-tax country expat + FEIE: Skip contributions, use deduction surplus for annual Roth conversions at $0 US tax.

- High-tax country expat + FTC: Direct Roth contributions preserved; possible backdoor Roth if income is above the phaseout threshold.

- Self-employed expat: Solo 401(k) cleans up pro-rata exposure, enabling clean backdoor Roth contributions.

- Retirement destination: Territorial tax countries give you the full triple play — zero tax from both countries at every stage.

None of this is simple, and all of it deserves professional guidance from a CPA who specializes in US expat taxation. The cost of that advice — typically $1,500–$4,000 annually for a properly filed expat return — is a fraction of what a single year of excess contributions, missed conversions, or incorrect filing elections can cost to correct. Make the Roth a deliberate, annually reviewed part of your expat financial plan. Your future self — decades from now, withdrawing tax-free from a beach in a territorial tax country — will thank you.

Financial Disclaimer: This article is for informational and educational purposes only and does not constitute financial, tax, legal, or investment advice. Every expat's tax situation is unique — strategy depends on income level, country of residence, applicable tax treaties, existing retirement account balances, state domicile, and many other factors. Tax laws, FEIE limits, contribution limits, and treaty interpretations change frequently. Always consult a qualified CPA or enrolled agent specializing in US expat taxation before making decisions about Roth IRA contributions, conversions, or elections. Nothing in this article should be construed as a recommendation to pursue or avoid any specific tax strategy.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJuly 4, 2026

Expat Tax & FinanceJuly 4, 2026

Canadian TFSA and US Taxes: The Reporting Trap

US citizens holding a Canadian TFSA owe tax on all annual growth and must file Form 3520 — PFIC rules apply to Canadian mutual funds inside the

Expat Tax & FinanceJuly 4, 2026

Expat Tax & FinanceJuly 4, 2026

State Income Tax for Expats: Which States Follow You

California, New York, and Virginia keep taxing Americans abroad. Learn which states follow you, what triggers audits, and how to exit cleanly.

Expat Tax & FinanceJuly 3, 2026

Expat Tax & FinanceJuly 3, 2026

FBAR: The $10,000 Expat Rule Most People Get Wrong

FBAR: when any foreign account aggregate hits $10,000 during the year, all accounts must be reported. Penalties, Bittner ruling, and catch-up