Why Foreign Banks Refuse American Expats (And What to Do)

FATCA costs foreign banks up to $16,600 per American account. Here's why banks reject US expats worldwide — and the banking stack that actually works.

FATCA costs banks $16,600 per American account. Learn why foreign banks refuse US expats and which banking solutions actually work abroad.

You've done everything right. You moved abroad legally. You filed your taxes. You have zero criminal history. And the bank still said no — not because of anything you did, but because of your passport.

Since 2014, a quiet financial purge has been spreading across the globe. Swiss private banks. German neobanks. Thai savings institutions. French regional credit unions. They're all turning away Americans — not out of hostility, but because the math is brutal: complying with US law costs more than your deposits are worth.

This is the real story of FATCA, and it affects every one of the estimated 9 million Americans living abroad.

What FATCA Actually Requires (And Why Banks Hate It)

The Foreign Account Tax Compliance Act was signed into law in 2010 as part of the HIRE Act and fully phased in by 2014. On paper, it was designed to catch wealthy Americans hiding money in Swiss banks. In practice, it became a global reporting mandate that cost ordinary expats their savings accounts.

Here's what FATCA requires: every Foreign Financial Institution (FFI) on earth — banks, brokerages, insurance companies, pension funds — must identify all US-person account holders and report their names, addresses, taxpayer identification numbers, account numbers, and balances directly to the IRS every year.

Banks that refuse face a 30% withholding tax on all US-source income flowing through them. That's not a fine — it's a tax on the institution's own revenue stream. For any bank with meaningful exposure to US capital markets (dividends, interest, gross proceeds from US securities), non-compliance is economically catastrophic.

The Treasury has signed Intergovernmental Agreements (IGAs) with 110+ countries to enforce this through local law. The OECD's Common Reporting Standard — sometimes called "GATCA" because it was explicitly modeled on FATCA — has been adopted by 120+ countries on a multilateral basis. There is effectively nowhere to hide from US financial reach, and no foreign bank can pretend it doesn't see your American passport.

The Math That Kills Your Account

The rational response for most small and mid-sized foreign banks isn't to comply — it's to exit.

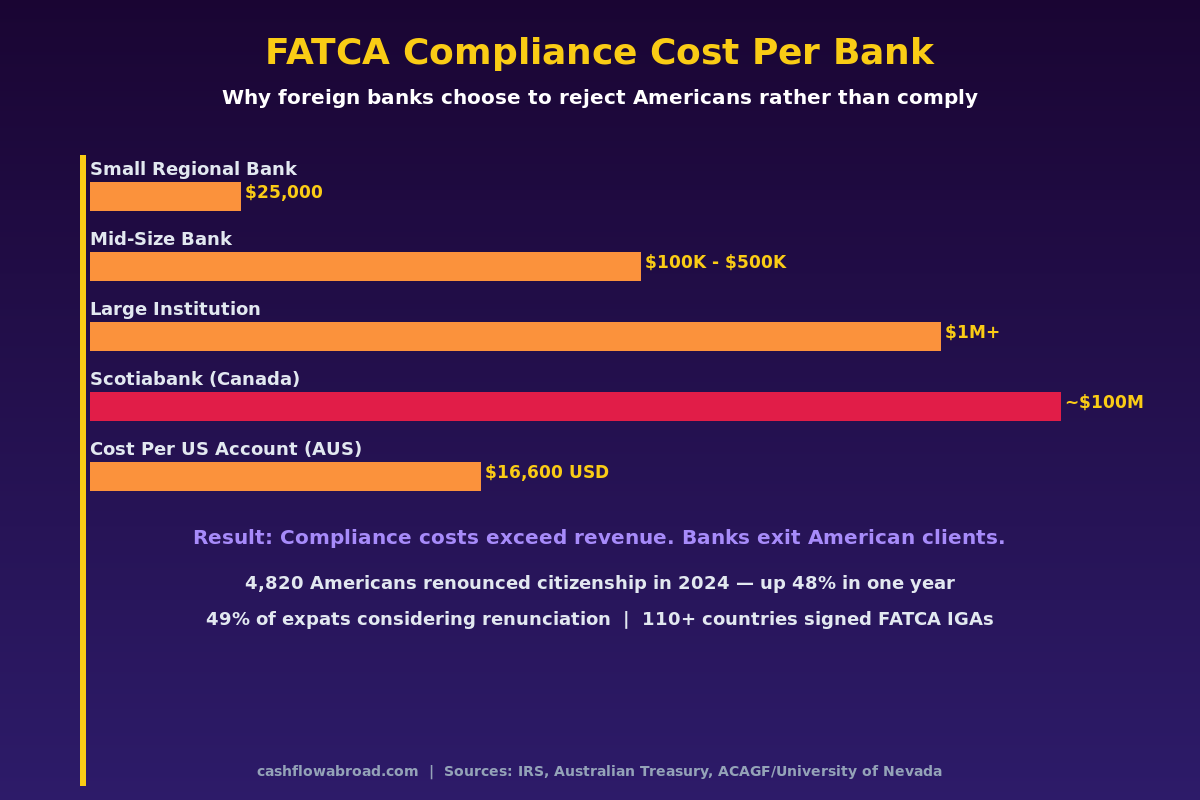

Australian government research provides the clearest illustration of why. Researchers calculated that FATCA compliance costs approximately A$25,600 (~$16,600 USD) per US-person account maintained. A small regional bank with 30 American clients generates, at best, a few thousand dollars per year in net interest margin from those accounts. The compliance cost to serve them legally: nearly half a million dollars. The math is simply inverted.

| Institution Size | Estimated FATCA Setup Cost | Source |

|---|---|---|

| Small regional bank | ~$25,000 | Executive magazine / FATCA literature |

| Mid-size bank | $100,000 – $500,000 | Executive magazine / FATCA literature |

| Large institution | $1 million+ | Executive magazine / FATCA literature |

| Scotiabank (Canada) | ~$100 million | FATCA compliance filings |

| Australia industry (10-yr total) | A$482.68 million (~$313M USD) | Australian Treasury |

| Cost per US account (Australia) | A$25,600 (~$16,600 USD) | Australian Treasury |

The ongoing cost compounds the problem. After paying to build the compliance infrastructure, banks must maintain annual IRS XML reporting pipelines, retrain staff to identify US indicia (a US phone number in your account, a US power-of-attorney, a US birthplace on your ID), and manage the tail risk that a reporting error triggers the catastrophic 30% withholding penalty.

For a bank with 25 American clients generating $4,000 in annual revenue, spending six figures annually on compliance infrastructure isn't a business decision — it's an exit decision.

Countries Where Americans Get Rejected Most

Some regions have become effectively banking deserts for Americans:

Switzerland is the most dramatic case. After UBS paid $780 million in fines in 2009 — and then an additional $5 billion to settle DOJ/IRS investigations in 2014 — Swiss private banks made a calculation: American clients aren't worth the legal exposure. Most Swiss banks now either refuse Americans outright or impose minimum asset thresholds above $1M that price out normal expats.

Germany offers no viable neobank path. N26, the widely-used German digital bank, explicitly does not accept US residents due to FATCA compliance complexity. Revolut and similar platforms work, but they are transactional tools, not banking relationships.

The Netherlands became a flash point when the Dutch Banking Association distributed widely-publicized guidance warning Americans that failure to provide FATCA compliance documentation meant banks "will no longer be allowed to accept their business." Dutch banks sent letters to customers flagged by US birthplace demanding W-9 forms or facing account closure — including people who'd never set foot in the US and didn't know they held US citizenship.

France has documented FATCA-driven account closures. Regional banks have systematically stopped accepting US-person clients, leaving expats to rely on international banks or digital solutions.

The US itself has joined in: Wells Fargo fully exited international brokerage accounts for overseas US residents effective January 19, 2021. Morgan Stanley, Fidelity, Merrill Lynch, Ameriprise, TIAA, Edward Jones, USAA, and UBS have all at various points closed accounts held by Americans living abroad, citing regulatory complexity. See the full breakdown in the expat brokerage account closure guide.

The result: by 2024, 4,820 Americans had renounced citizenship — a 48% increase over 2023 and the third-highest annual figure ever recorded. A 2025 survey by Greenback Tax Services found 49% of US expats are seriously considering renunciation, up from 30% the prior year. FATCA-related banking restrictions rank alongside tax filing complexity as the primary drivers.

An American Citizens Abroad survey found 86% of respondents believe FATCA needs to be fundamentally reworked to allow Americans abroad basic access to banking services.

The "Accidental American" Problem

FATCA's reach extends far beyond expats who moved abroad intentionally. "Accidental Americans" — people born on US soil but raised entirely in another country — often don't know they hold US citizenship. A Dutch citizen born in New York during a business trip their parents made in 1980 may have never filed a US tax return, opened a US account, or used a US passport. None of that matters to FATCA. The birthplace entry on their Dutch bank account is enough to trigger a compliance flag.

Dutch, French, and German banks have all sent closure letters to customers whose only "US indicia" is a birthplace. The IRS doesn't care if you've never lived in America, earned money there, or even applied for a US passport. If FATCA says you're a US person, your bank has a reporting obligation — or it exits the relationship.

US-Based Accounts That Work Worldwide

The foundation of any expat banking stack is a US-based account designed for international use. Two options dominate:

Charles Schwab Investor Checking

Charles Schwab's International account is the most-recommended expat banking solution for a reason: unlimited worldwide ATM fee rebates. Every ATM fee charged anywhere on earth gets reimbursed at month-end. Add no foreign transaction fees, no monthly maintenance fees, and genuine customer service for overseas holders, and it's hard to beat for daily cash access. The linked brokerage provides access to US investment accounts that many platforms close when you move abroad.

One caveat: once registered as an international client, purchasing new US mutual funds and CDs may be restricted under SEC regulations. Existing holdings are unaffected. It's a transactional banking and brokerage tool, not a one-stop shop.

Mercury for Business Banking

If you run any kind of US business — freelancing, consulting, LLC — Mercury is the cleanest US business banking solution for expats. No monthly fees, no minimum balance, FDIC-insured up to $500K through its partner banks, and fully functional from anywhere. It pairs well with a Schwab personal account for the full banking stack.

Maintaining Your US Address

Here's a practical problem most expats hit immediately: US banks want a US mailing address. When you move abroad, your old address disappears. Updating to a foreign address sometimes triggers account review flags — or worse, account closure requests from compliance teams.

Traveling Mailbox solves this with a real US street address in 50+ cities, mail scanning, check deposits, and secure online access. At $15/month, it keeps your US banking relationships intact, maintains a legitimate address for IRS correspondence, and preserves state domicile for those who need it. More on why this matters is in the virtual mailbox expat guide.

Opening Local Accounts: What Actually Works by Country

US-based accounts handle dollar savings and ATM access. But for daily life — paying rent, utilities, local bills — a local account simplifies everything. The good news: foreign banks in popular expat destinations do still accept Americans, though the process requires patience and the right documents.

Mexico

BBVA Mexico (formerly Bancomer) is the largest bank in Mexico with 1,700+ branches and 14,000+ ATMs. It accepts US citizens — but you must appear in person at a branch with: passport, temporary or permanent residency card (FM2/FM3), proof of Mexican address, and an RFC (Mexican tax ID from SAT). Getting your RFC before attempting account opening saves significant time. Santander Mexico and Banorte are backup options. Individual branch experience varies widely; a location in a major expat area (Mexico City's Condesa, Oaxaca, San Miguel de Allende) will be far more practiced at the process.

Colombia

Bancolombia — founded in 1875, with 14+ million clients — accepts foreigners using a Cédula de Extranjería (issued after obtaining a Colombian visa) plus RUT registration from DIAN, Colombia's tax authority. The process requires an in-person visit. For a faster path, Nubank Colombia is reportedly more flexible with documentation and is growing in popularity among expats in Medellín and Bogotá.

Thailand

Bangkok Bank, with 1,200+ branches, explicitly markets to foreign customers and is the most foreigner-friendly major bank in Thailand. Account opening requires an in-person visit, a non-immigrant visa (not a tourist visa), and — because Bangkok Bank knows FATCA applies — W-9 documentation for US citizens. Prepare the W-9 in advance. The Kasikorn Bank (KBank) and SCB are alternatives, though branch-level discretion varies significantly.

Europe

Options narrow considerably. HSBC Expat, based in Jersey (Channel Islands), was explicitly designed to serve internationally mobile clients including US citizens. Balance minimums make it impractical for many expats, but it's the cleanest institutional solution for Americans who need a European banking relationship. Bunq, the Dutch neobank, has been noted as more accommodating to non-EU residents than most European digital banks.

International Transfers

For moving money across borders — dollars to pesos, dollars to baht, dollars to euros — Remitly handles international transfers reliably at rates far below what traditional banks charge. The full breakdown of fee structures across transfer services is in the expat money transfer guide.

The Digital Banking Bridge Layer

Between your US account and your local account, fintech tools handle FX and multi-currency spending more efficiently than traditional banks:

| Need | Best Solution |

|---|---|

| US dollar savings + ATM globally | Charles Schwab International |

| US business banking | Mercury |

| US mailing address abroad | Traveling Mailbox |

| Multi-currency spending card + FX | Revolut (FATCA-compliant) |

| International money transfers | Remitly |

| High-balance European banking | HSBC Expat (Jersey) |

| Local account in Mexico | BBVA Mexico (in person + residency) |

| Local account in Colombia | Bancolombia or Nubank Colombia |

| Local account in Thailand | Bangkok Bank (in person + non-immigrant visa) |

Revolut accepts US citizens, offers multi-currency accounts at or near interbank FX rates, and is FATCA-compliant. Premium tiers ($9.99–$16.99/month) add higher ATM limits and travel insurance. It doesn't replace a bank — no lending, no FDIC coverage — but as a spending and currency conversion layer, it's among the most efficient tools available.

N26, Monzo, and most other European neobanks do not accept US residents. Don't waste time applying.

The "Same Country Exemption" — Will FATCA Ever Be Reformed?

American Citizens Abroad (ACA) has lobbied Congress for a Same Country Exemption (SCE) to FATCA for years. The proposal is straightforward: accounts held by US citizens in the country where they are a bona fide resident shouldn't require foreign bank reporting, because the account isn't hiding anything — it's paying for groceries.

As of 2025, the SCE has been introduced in Congress multiple times and has not passed. The political will to reform FATCA has been consistently outgunned by revenue collection priorities and the institutional inertia of 110+ countries that have already built IGA compliance frameworks. The 2025 Eleventh Circuit ruling — finding that some FBAR penalties may violate the Eighth Amendment's Excessive Fines Clause — suggests courts are slowly receptive to proportionality arguments, but that's penalty enforcement, not FATCA banking access.

For practical purposes: build a banking stack that works within the current reality. The US taxes citizenship, not residence, and that's not changing soon.

Building Your Stack and Moving Forward

No single account solves every problem. The expats who navigate this best use a three-layer approach:

Layer 1 — US Dollar Foundation: Charles Schwab for dollar savings, ATM access everywhere, and a US investment account that doesn't get closed when your address changes. Mercury if you have a US business entity.

Layer 2 — Local Presence: Open a local bank account once you establish residency. This requires patience, a local tax ID, and often multiple branch visits — but it makes daily life dramatically simpler for rent, utilities, and local payroll.

Layer 3 — Movement and Conversion: Revolut for multi-currency spending and FX. Remitly for international transfers without the 3–5% fee spread traditional banks charge.

One critical detail: maintain a real US mailing address for the entire duration of your time abroad. Banks send compliance letters there. The IRS mails notices there. A virtual mailbox like Traveling Mailbox handles this cleanly for $15/month and keeps your entire US financial infrastructure intact.

For the broader tax picture, the US expat banking and taxes guide covers the full framework of what you owe and how banking connects to your filing obligations. If your goal is structuring your life to minimize both taxes and banking friction simultaneously, the geographic arbitrage playbook maps which countries make both easiest.

FATCA was designed to catch billionaires using Swiss accounts to evade taxes. Its practical effect has been to make an ordinary American expat's financial life needlessly complicated — generating account closures, bank rejections, and six-figure compliance costs that no small bank wants to absorb for a handful of modest savings accounts. Nine million Americans living abroad didn't create this problem. The stack above is how you live around it until the law catches up.

Financial Disclaimer: This article is for informational and educational purposes only and does not constitute financial, tax, or legal advice. Banking regulations, FATCA compliance requirements, and individual bank policies change frequently and vary by country and jurisdiction. Consult a licensed tax professional or financial advisor familiar with US expat law before making banking or financial decisions. Affiliate links are present in this article; the site may receive compensation if you use them, at no additional cost to you.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 10, 2026

Expat Tax & FinanceMay 10, 2026

FATCA vs. GDPR: Why US Expats Lose European Banks

Belgium declared FATCA illegal under GDPR. Now EU banks face a catch-22. Here is what US expats need to know about European banking in 2026.

Expat Tax & FinanceMay 30, 2026

Expat Tax & FinanceMay 30, 2026

FBAR vs FATCA: What Every Expat Must Know

FBAR and FATCA are two separate foreign account reporting requirements with different penalties and thresholds. Learn what every US expat must file.

Expat Tax & FinanceMay 30, 2026

Expat Tax & FinanceMay 30, 2026

The 3 Bank Accounts Every US Expat Actually Needs

Stop paying $2,400/year in bank fees abroad. This 3-account expat banking setup—Schwab, Mercury, Traveling Mailbox—costs just $180/year.