Andorra’s 10% Flat Tax: Europe’s Hidden Residency Play

8 min read · 1,950 words

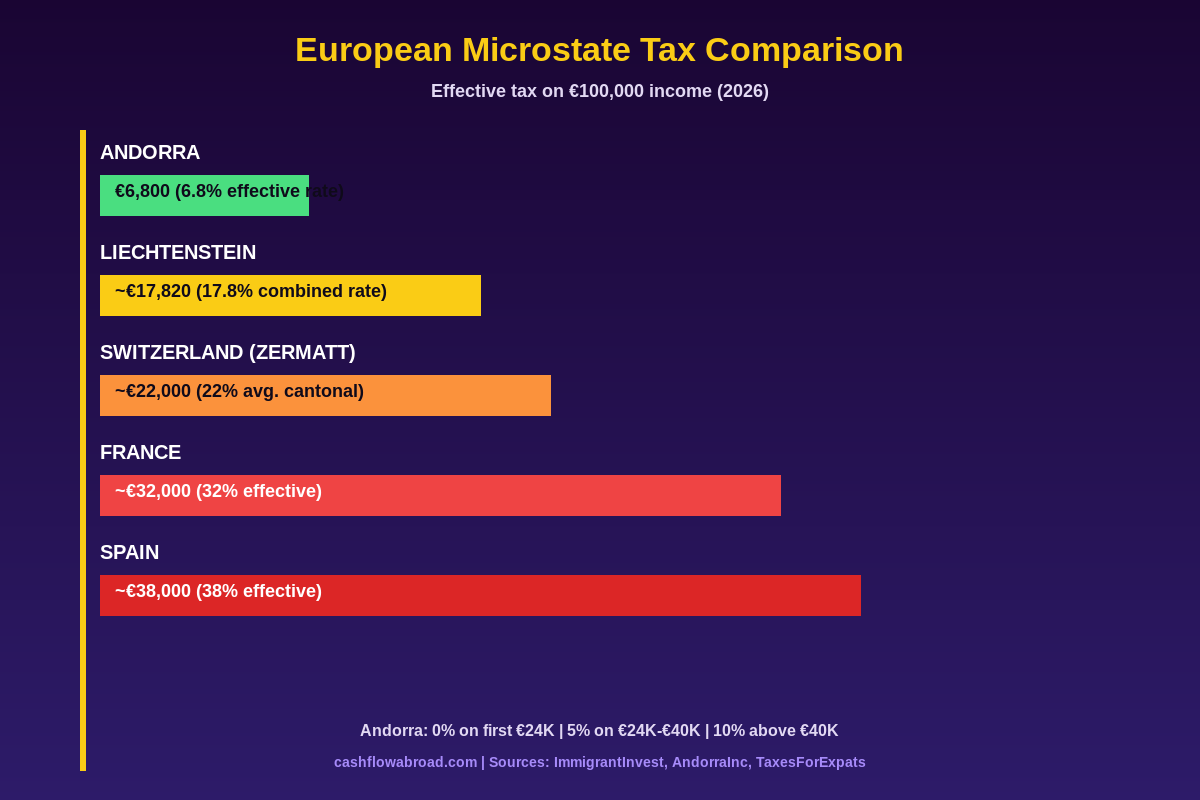

The average French resident pays roughly €32,000 in income tax on a €100,000 salary. Their neighbor in Andorra — a 90-minute drive from Barcelona, 3 hours from Paris — pays €6,800. On the same income. Legally.

That gap isn’t a loophole or a temporary regime waiting to be killed. It’s baked into Andorra’s tax code: the first €24,000 of annual income is completely exempt, the next €16,000 is taxed at 5%, and everything above €40,000 hits a maximum rate of 10%. No exceptions, no phase-outs. The system is straightforward in a way that makes most European tax codes look like deliberately bad art.

Andorra doesn’t get the same attention as Monaco or Dubai, partly because it’s small (77,000 people, roughly the population of a mid-sized American suburb), partly because it’s nestled in the Pyrenees between two high-tax countries, and partly because it never marketed itself aggressively. That obscurity has quietly become its advantage — Andorra is still genuinely accessible for people who don’t have eight figures on their balance sheet.

How Andorra’s Tax System Actually Works

Andorra’s personal income tax (IRPF) has three tiers that collectively produce one of Europe’s lowest effective rates:

| Income Range | Tax Rate | Tax Owed |

|---|---|---|

| €0 – €24,000 | 0% | €0 |

| €24,001 – €40,000 | 5% | Up to €800 |

| Above €40,000 | 10% | 10% on the excess |

On €100,000 of income, you owe exactly €6,800 — a 6.8% effective rate. On €200,000, it’s €16,800, an 8.4% effective rate. The rate creeps toward 10% but never surpasses it, no matter how much you earn. There is no wealth tax, no inheritance tax, and no capital gains tax on dividends or interest income held over one year.

The VAT equivalent — called the IGI — sits at 4.5%, the lowest in Europe. Food carries a 1% rate, meaning your grocery bill is practically a rounding error in terms of tax burden. Compare that to France’s 20% TVA or Spain’s 21% IVA, and the Andorran advantage compounds across every purchase. Corporate tax (IS) follows the same logic: 10% flat, with a 2% rate available to newly incorporated companies during their first fiscal year and to companies structured for international trading income.

Residency Pathways: Your Options

Andorra offers two main residency categories, and the one you choose has significant implications for how much time you need to spend there and how much capital you need upfront.

Passive Residency (The Investor Route)

Passive residency is designed for people with enough assets to live without working locally. As of February 13, 2026 — when Andorra’s “Omnibus 2” law entered force — the minimum investment requirement jumped from €600,000 to €1,000,000. On top of that, you pay a non-refundable €50,000 to the Andorran Financial Authority (AFA), plus €12,000 per dependent.

Eligible investments include Andorran real estate (with a minimum of €800,000 per property), shares in Andorran companies, or authorized Andorran financial instruments. The financial instruments option now carries a 36-month limit, after which you must rotate the capital into real estate or company equity. If you were hoping to park €1M in a money market fund indefinitely, that option has narrowed considerably.

One of passive residency’s major attractions: you only need to spend 90 days per year in Andorra to maintain your permit. That’s a meaningful distinction from most residency programs that demand 183+ days. If you want to split time between Andorra, Southeast Asia, and the US, the math works.

Active Residency (The Entrepreneur Route)

If you don’t have €1 million to invest but you’re willing to build or buy into an Andorran business, active self-employed residency is the path. Requirements:

- Form a new Andorran company or acquire at least 34% of an existing one

- Hold a management position (director, administrator) in that company

- Pay the same €50,000 non-refundable AFA fee

- Spend at least 183 days per year in Andorra

The 183-day requirement is the main tradeoff. If you’re building a genuine Andorran-based operation — consulting, digital services, fund management — that’s workable. If you’re hoping to operate remotely from Bali and visit occasionally, passive residency is the better fit despite the higher investment threshold.

Omnibus 2: What Changed in 2026

The Omnibus 2 law, approved by parliament on January 22 and effective February 13, 2026, is the most significant overhaul of Andorra’s residency framework in years:

| Element | Before Omnibus 2 | After Omnibus 2 |

|---|---|---|

| Passive residency investment minimum | €600,000 | €1,000,000 |

| Minimum real estate value per unit | No specific floor | €800,000 per property |

| AFA fee (both residency types) | Partially refundable | Non-refundable |

| Financial instruments holding period | No limit | 36-month cap, then must redeploy |

| Grandfather clause | N/A | Pre-Jan 22 applicants follow old rules |

The intent is clear: Andorra wants long-term capital, not residency tourism. The €1M threshold eliminates casual applicants who qualified under €600K but weren’t seriously committed to the country. For genuinely high-net-worth individuals, the bar is higher but the fundamentals haven’t changed — 10% maximum tax, no wealth or inheritance tax, 90-day minimum presence.

Andorra vs. the Competition

Context matters when evaluating any residency play. How does Andorra compare to the other European microstates people actually consider?

| Jurisdiction | Max Personal Tax | Effective Rate (€100K) | Entry Cost (Passive) | Min. Days/Year |

|---|---|---|---|---|

| Andorra | 10% | 6.8% | €1M + €50K fee | 90 days |

| Monaco | 0% | 0% | €500K bank deposit + lease | Full-time (de facto) |

| Liechtenstein | ~17.8% combined | ~17.8% | Quota system — near impossible | 183 days |

| Switzerland (Zug) | ~22% avg. | ~22% | Lump-sum negotiation (€M+) | 183 days |

| Gibraltar (Cat. 2) | ~15% structured | ~15% | ~€30K fee + HNW requirement | 183 days |

Monaco wins on pure tax optics — zero personal income tax — but the lifestyle cost is brutal. One-bedroom apartments start at €3,000/month, property averages €50,000/sqm, and monthly expenses for a single person comfortably clear €10,000. You’re not saving taxes if you’re spending €120,000/year on housing.

Andorra’s real edge is the combination: low taxes AND a livable cost structure. A 2-bedroom apartment outside the capital runs €650–€900/month. Groceries are cheap. You can live well on €1,500/month as a single person without lifestyle sacrifice. When you run the full arbitrage calculation — tax savings minus incremental living costs — Andorra often comes out ahead of Monaco despite the latter’s nominally superior rates.

Liechtenstein is effectively closed to new entrants. Switzerland is competitive in low-tax cantons like Zug or Nidwalden, but lump-sum negotiations start in the millions and you’re looking at full-time presence. Gibraltar’s Category 2 residency is genuinely accessible but still requires 183 days and a higher effective rate than Andorra.

The US Expat Angle

For American citizens, Andorra adds a layer of complexity: the US taxes worldwide income, and there is no US-Andorra tax treaty. You’re working with the standard expat toolkit rather than treaty-specific provisions.

The FEIE (Foreign Earned Income Exclusion) lets you exclude $130,000 of foreign earned income in 2026. If you’re earning €100K from consulting or self-employment through your Andorran company, and you qualify through the Physical Presence Test (183+ days outside the US, which you’ll likely exceed), you can exclude most of that from US tax. What Andorra taxes at 6.8%, you may owe little or nothing additional to the IRS.

Investment income — dividends, interest, capital gains — doesn’t qualify for FEIE. For those, the Foreign Tax Credit offsets US liability dollar-for-dollar against Andorran taxes paid. Since Andorra’s rate (10%) is below most US marginal rates on investment income (20–23.8% on qualified dividends), there will often be a residual US liability on investment income even after applying FTCs. The math requires a CPA who understands expat investment taxation — don’t skip that step.

Operationally, US expats in Andorra should maintain solid US financial infrastructure. Mercury works well for US business banking for non-residents. Charles Schwab International remains the gold standard for US brokerage accounts abroad — no foreign transaction fees and free ATM withdrawals globally. A Traveling Mailbox virtual address preserves your US state domicile for IRS correspondence and banking, which matters when you’re spending 90+ days/year in the Pyrenees and the rest of the time traveling.

Cost of Living Breakdown

Andorra la Vella is compact — roughly the scale of a ski town — but functional. It’s bilingual in Catalan and Spanish, has reliable public services, and puts ski resorts within 20 minutes of most apartments. It’s not a cosmopolitan hub, which is a feature for people who are there to structure their finances rather than attend gallery openings.

| Expense | Monthly Cost Range |

|---|---|

| 1-bed apartment (Andorra la Vella center) | €900 – €1,400 |

| 1-bed apartment (outer parishes) | €600 – €800 |

| Groceries (1% VAT on food) | €250 – €350 |

| Utilities | €80 – €130 |

| Transport | €150 – €250 |

| Dining and entertainment | €300 – €500 |

| Single person total (comfortable) | €1,400 – €1,800 |

Healthcare is handled through CASS, Andorra’s public-private system. Residents contribute approximately 6% of income (employers match), covering access to public facilities. For international coverage during travel outside Andorra, SafetyWing Nomad Insurance runs $56–$188/month depending on age and coverage, making it an efficient supplement.

The Break-Even Math

The €50,000 non-refundable AFA fee is a real cost, but it front-loads what is otherwise an extraordinarily efficient tax structure. Here’s how the math works at different income levels:

| Annual Income | Tax in France (~32%) | Tax in Andorra | Annual Savings | AFA Fee Break-Even |

|---|---|---|---|---|

| €100,000 | ~€32,000 | €6,800 | ~€25,200 | ~24 months |

| €200,000 | ~€70,000 | €16,800 | ~€53,200 | ~11 months |

| €500,000 | ~€200,000 | €46,800 | ~€153,200 | ~4 months |

At €200K income, the AFA fee pays for itself in under a year. At €500K, it pays back in a quarter. The investment threshold for passive residency (€1M) is also capital you still own — it’s not spent, just committed. The real cost is the €50K fee, the legal setup (roughly €3,000–€8,000 with a good gestoria), and the first year of living expenses while you establish presence.

Who Andorra Actually Makes Sense For

Strong candidates: High-income consultants or executives earning €150K+ who want a permanent European base. Business owners who can genuinely incorporate in Andorra. Retirees with substantial investment portfolios who want EU-adjacent living. Anyone currently paying 35%+ effective rates in France, Spain, or Belgium.

Poor candidates: People who need EU freedom of movement for business (Andorra is not an EU member). Anyone looking for a purely nominal residency they won’t actually use — the AFA fee is now explicitly non-refundable. US citizens with complex investment structures who haven’t run the FTC analysis. And anyone earning under €80,000 annually — the break-even period stretches past three years, which is long for a lifestyle you might not want to commit to that quickly.

Andorra also requires you to genuinely give up, or at least severely limit, ties to your home country. If you’re still domiciled in France and spending 200 days there, the French tax authority will not simply accept that you’ve moved to Andorra. The geographic arbitrage has to be real, not cosmetic.

The Practical Setup Process

- Hire a local gestoria — nearly every expat uses one. They handle paperwork, immigration filings, and company formation if needed. Budget €3,000–€8,000 for the full process.

- Secure accommodation — you need a valid rental contract or property deed before applying. Budget 2–4 weeks to sort housing.

- Apostille criminal background checks — required from every country you’ve lived in for the past 5 years. Allow 4–8 weeks depending on country.

- Submit AFA investment declaration — passive residents submit the investment plan and pay the €50K fee at this stage.

- Medical examination in Andorra — basic health screening; can be completed in a single appointment.

- Receive initial residence card — valid 1 year, renewed in 2-year blocks three times, then 10-year renewals. Andorran citizenship is available after 20 years of legal residency.

The full process typically takes 3–6 months from first contact with a gestoria to card-in-hand. It’s not fast, but it’s predictable.

Conclusion

Andorra’s pitch is 10% maximum tax, no wealth or inheritance tax, 4.5% VAT, and a cost of living that makes the savings genuinely meaningful rather than immediately recaptured by €10,000/month rents. The Omnibus 2 Law raised the barrier for passive investors — €1M is real capital, and the non-refundable €50K is not a casual commitment. But for the right profile, the numbers are difficult to argue with.

As France, Spain, and Germany continue experimenting with exit taxes, wealth levies, and bracket creep, the Pyrenean microstate between them starts to look less like an obscure tax trick and more like a sensible long-term address. The US expat banking and tax infrastructure requires careful setup, and the FEIE/FTC analysis needs a real CPA. But the core proposition — live in a stable, well-functioning European country at 6.8% effective tax on €100K — is as clean as tax planning gets.

Financial Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently; always consult a qualified tax professional and immigration attorney before making any residency or tax decisions. US citizens and green card holders have specific reporting obligations (FBAR, FATCA, Form 8938) that apply regardless of country of residence.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.