Thailand Tax Rules for US Expats: The Complete Guide

11 min read · 2,793 words

Here’s a number that should make every American in Thailand uncomfortable: Thailand has no tax treaty with the United States. Zero. None. Every other major expat destination — France, Germany, Japan, Mexico, Costa Rica — has a bilateral agreement that prevents the IRS and a foreign tax authority from both taxing the same dollar. Thailand? You’re flying without a net.

Then in 2024, Thailand changed its foreign income tax rules in a way that sent 300,000+ expats scrambling. The country went from “tax-free if you keep money offshore” to “we want a piece of everything you bring in.” Expat forums melted down. Relocation agencies saw cancellations.

But here’s the counterintuitive reality: for most American remote workers, the actual tax damage is minimal. Understanding why requires knowing exactly how Thailand’s system works — and where it collides with the IRS.

Who Is a Thai Tax Resident?

Thailand’s definition is clean: spend 180 or more days in the country during a calendar year and you’re a tax resident. Days don’t need to be consecutive. Leave for a week in November, come back — that week still counts toward your 180-day total for the year.

Below 180 days, you only owe Thai tax on income sourced in Thailand. Freelance income from a US client? Not taxable. Dividends from a Schwab account? Not taxable. A salary paid by a Thai employer for work done in Thailand? Taxable.

Most visa-run tourists and slow travelers stay under the threshold. But anyone on a long-term visa — the DTV, LTR, or stacked tourist entries — often crosses 180 days without realizing it until they’re looking at a filing obligation.

The 2024 Foreign Income Rule Change

Before 2024, Thailand had an exploitable quirk: foreign income was only taxable if remitted to Thailand in the same calendar year it was earned. Earn $100,000 in Year 1, park it in a US account, bring it over in Year 2? Tax-free in Thailand. Expats routinely aged money offshore for one year and transferred it with impunity.

Thailand’s Revenue Department shut that loophole on January 1, 2024. The new rule: any foreign-sourced income earned from January 1, 2024 onward is taxable if you’re a Thai tax resident and you remit it to Thailand — regardless of which year you bring it in.

This is a material change. Money you earned in 2024 and bring to Thailand in 2027 is now assessable income under Thai law. The old strategy is dead for anything earned post-cutoff.

What didn’t change: Foreign income earned before January 1, 2024 remains grandfathered under the old rules. You can bring pre-2024 capital to Thailand indefinitely, tax-free. Many expats sitting on substantial pre-2024 savings still have a useful runway.

There is a proposed exemption working through the Revenue Department: foreign income remitted within the same year earned, or the immediately following year, may qualify for a tax exemption. As of early 2026, this proposal has not been formally enacted into law. Don’t structure your finances around it until it passes.

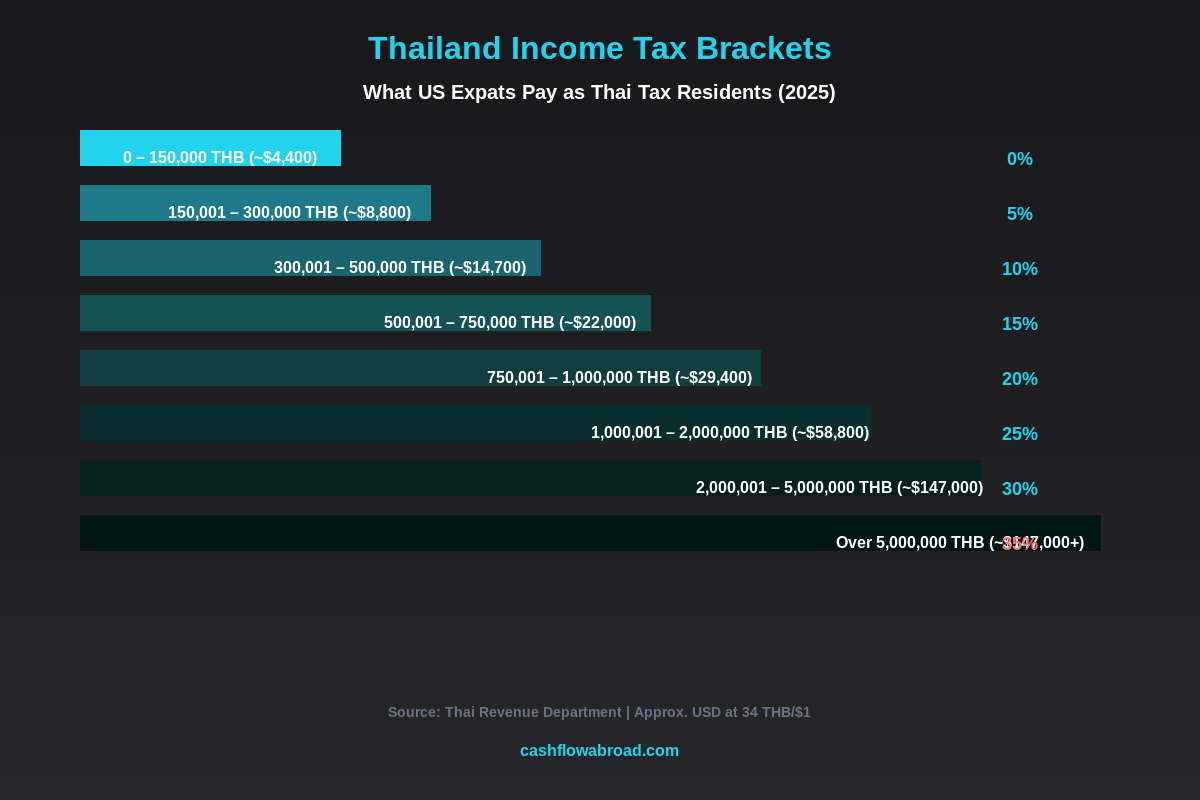

Thailand’s Income Tax Brackets

Thai personal income tax runs from 0% to 35% on a progressive scale. The rates apply equally to Thai nationals and foreign residents. At the current exchange rate of approximately 34 THB per US dollar:

| Taxable Income (THB) | Approx. USD | Tax Rate |

|---|---|---|

| 0 – 150,000 | $0 – $4,400 | 0% |

| 150,001 – 300,000 | $4,400 – $8,800 | 5% |

| 300,001 – 500,000 | $8,800 – $14,700 | 10% |

| 500,001 – 750,000 | $14,700 – $22,000 | 15% |

| 750,001 – 1,000,000 | $22,000 – $29,400 | 20% |

| 1,000,001 – 2,000,000 | $29,400 – $58,800 | 25% |

| 2,000,001 – 5,000,000 | $58,800 – $147,000 | 30% |

| Over 5,000,000 | $147,000+ | 35% |

Thailand also allows standard deductions that significantly reduce your taxable base. A personal allowance of 60,000 THB applies to all residents. An expense deduction of 50% of assessable income (capped at 100,000 THB) reduces income further. Additional allowances exist for spouses, children, parents, and health insurance premiums. A single expat bringing in 600,000 THB (~$17,600) in assessable income can often reduce their taxable base by 200,000+ THB before calculating tax owed.

The Missing Treaty: Why It Matters More Than You Think

Most developed countries have signed income tax treaties with the US. These agreements coordinate who taxes what, limit withholding rates, and provide tiebreaker rules when both countries claim the same taxpayer. Thailand is not on that list — there is no US-Thailand tax treaty.

This creates three specific problems:

No tiebreaker rules. If both the US (via citizenship) and Thailand (via 180+ days) claim you as a tax resident in the same year, there is no treaty article to resolve the conflict. You rely entirely on domestic mechanisms — FEIE and Foreign Tax Credit — to prevent double taxation.

No reduced withholding rates. Dividends and interest from Thai sources are subject to full statutory withholding (15% on dividends). A tax treaty might have reduced that rate to 5–10%, as treaties with many countries do. Without one, you pay full freight.

Higher planning complexity. With a treaty, you can often rely on treaty-defined residency rules, tie-breaking provisions, and defined income source rules. Without one, you fall back on each country’s domestic law — which can conflict in inconvenient ways.

The absence of a treaty doesn’t make Thailand unworkable for Americans. It makes it more planning-intensive than Japan or Germany, where treaty provisions handle most edge cases automatically.

The FEIE in Thailand: Your Primary Defense

The Foreign Earned Income Exclusion lets qualifying Americans exclude roughly $120,000–$130,000 of foreign earned income from US federal taxation annually (the amount adjusts with inflation each year). To qualify, you meet either the Bona Fide Residence Test (genuine foreign domicile) or the Physical Presence Test (330+ days outside the US in a 12-month period).

Thailand qualifies for both tests. Americans who spend 330+ days in Thailand, or who establish bona fide Thai residence, file Form 2555 and exclude their earned income. For a remote employee or freelancer earning $80,000 a year, this typically means $0 in US federal income tax on that income.

Critical caveat: the FEIE only covers earned income — wages, self-employment income, consulting fees. Passive income (dividends, capital gains, rental income, interest) is excluded from the exclusion. If your Thailand-based income is primarily investment distributions or portfolio withdrawals, the FEIE helps you less than you might expect.

There’s also a self-employment tax wrinkle. US self-employment tax (15.3% on net earnings) applies to the full amount of self-employment income even when the FEIE wipes out income tax liability. This surprises most expat freelancers. Earn $90,000 as a freelancer, exclude it all under FEIE, and you still owe roughly $12,700 in SE tax. That’s a substantial bill even with a zero income tax line.

Foreign Tax Credit: For Income the FEIE Doesn’t Cover

For passive income — dividends, rental income, capital gains — the Foreign Tax Credit (Form 1116) is the relevant tool. Thai taxes you actually pay can offset your US tax liability dollar-for-dollar on income in the same category.

The mechanics require careful tracking. Thai taxes paid on dividends credit against US tax on dividends specifically — not against US tax on capital gains or earned income. You’ll need to run separate FTC calculations for each income basket. If Thailand’s 35% top rate significantly exceeds your US rate on the same income, the excess Thai tax may not be fully creditable in the current year (though unused credits can carry forward for 10 years).

For most Americans in Thailand earning well below $147,000 (the 30% bracket threshold), Thai rates are lower than or equal to US rates. In practice, the FTC often eliminates most US tax on Thai-sourced passive income entirely. The problem cases are high earners in the 30–35% Thai brackets who pay Thai rates that dwarf their applicable US rates — wasted credits that can’t be refunded.

Visa Options for Long-Term Expats

Thailand launched two serious long-term visa options in recent years. Understanding how they interact with tax residency is essential. For a broader comparison across countries, see our digital nomad visa rankings.

| Visa | Duration | Cost | Key Requirement | Work Rights |

|---|---|---|---|---|

| Destination Thailand Visa (DTV) | 180 days + 180-day extension = 360 days/application | ~10,000 THB ($275) | 500,000 THB (~$14,500) savings | Remote work for foreign employers only |

| Long-Term Resident (LTR) — Work-From-Thailand | 5 years, renewable | ~50,000 THB ($1,470) | $80,000/year income (2 prior years) | Remote work permitted; Thai employment needs permit |

| Thailand Elite / Privilege Card | 5–20 years depending on tier | $15,000–$30,000+ | Purchase only | No work permitted |

The DTV is accessible and practical for most digital nomads. Under $300 and requiring only $14,500 in verifiable savings, it clears the bar for most remote professionals. The 180+180-day structure gives you a year per application, after which you briefly exit and reapply. The tax implication: the DTV is almost perfectly calibrated to push you over the 180-day Thai tax residency threshold. Plan for it.

The LTR targets high-income professionals with established track records. The $80,000/year income requirement for two prior years screens out most newer freelancers. In return, you get 5-year stability and — significantly — a flat 17% income tax rate on any Thailand-sourced employment income, versus the standard top rate of 35%. LTR holders who have work permits and Thai employment income save dramatically at that top bracket. For fully remote workers with foreign income, the 17% perk matters less day-to-day.

The Elite/Privilege Card is a pure purchase play — no income requirements, no employment restrictions, just long stays in exchange for a lump sum. Best suited for retirees or passive-income earners who want visa certainty without income proof paperwork.

What US Expats in Thailand Actually Owe

Concrete scenarios are more useful than abstract principles. Assume a US citizen who qualifies as a Thai tax resident (180+ days), earning remotely from US clients, and remitting living expenses monthly.

Scenario A — Remote employee, $75,000/year

FEIE covers the full $75,000 → US federal income tax: $0. Thai side: if they remit $1,500/month ($18,000/year) for living costs, that $18,000 is assessable in Thailand. After standard deductions (~$5,000), taxable income is ~$13,000 — mostly in the 5–10% Thai brackets. Thai bill: roughly $700–$900 for the year. Combined tab: under $1,000 on $75,000 earned.

Scenario B — Freelancer, $140,000/year

FEIE covers ~$130,000 → ~$10,000 taxable in the US after the standard deduction, but SE tax applies to the full self-employment income. SE tax alone: roughly $15,000–$17,000. Thai side: if they remit $2,000/month ($24,000), taxable in Thailand is ~$18,000 after deductions — Thai tax around $1,200. Total combined bill on $140,000: ~$16,000–$18,000, with the vast majority being US SE tax, not Thai income tax.

Scenario C — Early retiree, $60,000/year from investments

No earned income, FEIE doesn’t apply. If all $60,000 is post-2024 income remitted to Thailand, it’s fully assessable. After Thai deductions (~$5,000), taxable income ~$55,000. Thai tax: approximately $4,500–$6,000 at blended brackets. US qualified dividends at 15% (~$9,000) minus the FTC for Thai taxes paid (~$4,500–$6,000) = US net tax $3,000–$4,500. Combined effective rate: 12–15%. Worse than the UAE or Paraguay, but still under what most US states levy on the same income.

The worst-case scenario is a high earner with income above the FEIE ceiling, paying significant Thai tax, who then can’t fully use the FTC because their US liability on excess income is lower than Thai taxes paid. Careful income timing and remittance structuring — drawing on pre-2024 capital while leaving new earnings offshore until planning is done — can manage this substantially.

Real Costs: Bangkok vs. Chiang Mai

Thailand’s price spread is wider than most expats expect. Bangkok is no longer cheap by Southeast Asian standards — it’s comfortably more expensive than Ho Chi Minh City or Kuala Lumpur. Chiang Mai runs 30–40% lower on most categories while maintaining solid expat infrastructure.

| Expense Category | Bangkok/month (USD) | Chiang Mai/month (USD) |

|---|---|---|

| 1BR condo, city center | $440–$1,030 | $235–$530 |

| Food (mostly eating out) | $235–$440 | $145–$295 |

| Transportation | $90–$175 | $45–$90 |

| International health insurance | $75–$235 | $75–$235 |

| Utilities + internet | $60–$120 | $45–$90 |

| Coworking (optional) | $90–$145 | $60–$100 |

| Midrange monthly total | ~$1,320 | ~$880 |

The Chiang Mai number is particularly striking: $880/month for a comfortable single-person lifestyle — decent apartment, eating out regularly, scooter for transport, solid internet. Add international activities and occasional flights and a $1,200–$1,400 budget in Chiang Mai is genuinely comfortable. Bangkok at equivalent comfort runs $1,500–$2,000.

A local meal at a street stall or market runs 50–100 THB ($1.50–$3). A full Western-style restaurant dinner for two runs 500–1,400 THB ($15–$40). Thailand’s food pricing is one of its strongest value propositions — you can eat extremely well, extremely cheaply, if you’re willing to eat Thai food at local prices rather than imported Western fare.

For healthcare, Thailand’s private hospital network is among the best in Southeast Asia at a fraction of Western prices. A specialist consultation in Bangkok: $30–$80. Minor surgery that would cost $15,000 in the US can run $1,500–$3,000 in a Bangkok private hospital. Most long-term expats still carry international health insurance for catastrophic coverage and evacuation. SafetyWing Nomad Insurance starts at ~$45/month for under-40s and covers hospital stays and medical evacuation globally. For a full comparison of international health plans, see the expat health insurance guide.

Banking and Money Transfers

For US-side banking, Charles Schwab’s international checking account is the standard expat solution: no foreign transaction fees, unlimited global ATM fee reimbursements. Thai ATMs typically charge 200–250 THB (~$6–$7) per withdrawal; Schwab refunds all of it. See the full US expat banking guide for side-by-side account comparisons.

Opening a Thai bank account requires your valid visa and local address. Bangkok Bank, Kasikorn Bank (KBank), and SCB are the most foreigner-friendly. DTV and LTR holders can typically open accounts within weeks of arrival with passport, visa, and proof of address. Hold your Thai account in THB; maintaining a USD-denominated account in Thailand adds complexity without much practical benefit.

For regular USD-to-THB remittances, Remitly consistently outperforms bank wire on both fees and FX spread. A bank wire from a US account to a Thai bank can cost $25–$45 plus a 1–3% FX spread. On a $2,000 monthly transfer, that’s $50–$100 in transaction friction — Remitly typically brings this down significantly.

Maintain a US mailing address while abroad. The IRS, your brokerage, and any US state you maintain domicile in all require a physical US address for correspondence. A Traveling Mailbox gives you a real street address in 50+ US cities with mail scanning and forwarding for ~$15/month — essential for keeping US banking, IRS compliance, and financial accounts intact. More on this setup in our virtual mailbox guide for expats.

If you’re working from Thailand and need reliable access to US streaming, banking portals, and corporate VPNs, a good VPN is non-negotiable. NordVPN runs about $3–$5/month on annual plans and performs well across Thailand’s varying network quality. For data while traveling between Thai cities or across Southeast Asia, Saily eSIM covers multiple countries without swapping physical SIMs.

Thai Tax Filing: Dates and Obligations

The Thai tax year runs January 1 through December 31. Annual personal income tax returns are due by March 31 of the following year, with an extension to April 8 for online filers through the Revenue Department’s e-filing portal at rd.go.th.

You must report all assessable foreign income remitted to Thailand during the year. Supporting documentation includes bank statements showing inbound transfers, records of the income source and date earned, and documentation of any deductions claimed. Since the 2024 rule change, the Revenue Department has been significantly increasing scrutiny on foreign income declarations. Filing accurately with full documentation is no longer optional.

US filing obligations run parallel and independently. Form 1040 with either Form 2555 (FEIE) or Form 1116 (FTC), FBAR (FinCEN 114) if any Thai account exceeded $10,000 at any point during the year, and Form 8938 (FATCA) if total foreign financial assets exceed $200,000 for single filers abroad at year-end. These requirements exist regardless of whether you owe any US tax. The expat investing and PFIC guide covers reporting on any foreign investment accounts you might hold.

Practical First Steps

- Consult a US international tax professional before your first Thai tax year. The FEIE vs. FTC decision depends on your specific income mix; getting it wrong costs real money.

- Track your days from arrival. Use a spreadsheet or app to log entry/exit dates. The 180-day threshold is not the IRS’s concern — it’s Thailand’s — but crossing it determines whether you have Thai filing obligations.

- Set up US financial infrastructure first. Open a Schwab international checking account, get a virtual mailbox for your IRS address, and ensure your brokerage has a valid US address on file before you leave.

- Understand remittance vs. income sourcing. Income earned before 2024 can be brought to Thailand without Thai tax. Know which of your assets are pre-2024 vs. post-2024 and document the dates clearly.

- Visit first. Bangkok and Chiang Mai are genuinely different cities suited to different lifestyles. A 3–4 week exploratory trip before committing to a visa application saves significant grief.

Bottom Line

Thailand’s 2024 tax change is real and requires genuine planning adjustments. The one-year offshore aging strategy for foreign income no longer works for earnings after the cutoff. But the situation isn’t the disaster that panicked expat forums predicted. Most American remote workers using the FEIE still face combined US-Thai tax bills well under $2,000 per year on incomes up to $100,000. The missing US-Thailand tax treaty adds complexity but doesn’t create prohibitive double taxation for most income profiles.

What Thailand offers in exchange: one of the most livable climates in Southeast Asia, a food culture that makes cooking at home feel like a downgrade, hospital care that costs 10–20% of US prices, and monthly living costs that undercut almost any equivalent quality of life in a developed country. At $800–$1,300 a month in Chiang Mai, the geographic arbitrage math still works — even with a Thai tax bill in the mix.

This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax rules change frequently and individual circumstances vary significantly. Consult a qualified US international tax professional and a licensed Thai tax advisor before making any residency, visa, or financial decisions. Verify all figures with current official sources before acting.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.