New Zealand’s 4-Year Tax Exemption for New Residents

9 min read · 2,192 words

Most people thinking about moving abroad for tax reasons cycle through the same shortlist: UAE, Panama, Paraguay, Georgia. New Zealand almost never comes up. That’s a mistake — because New Zealand offers one of the most underrated tax breaks in the developed world, and most expats don’t even know it exists.

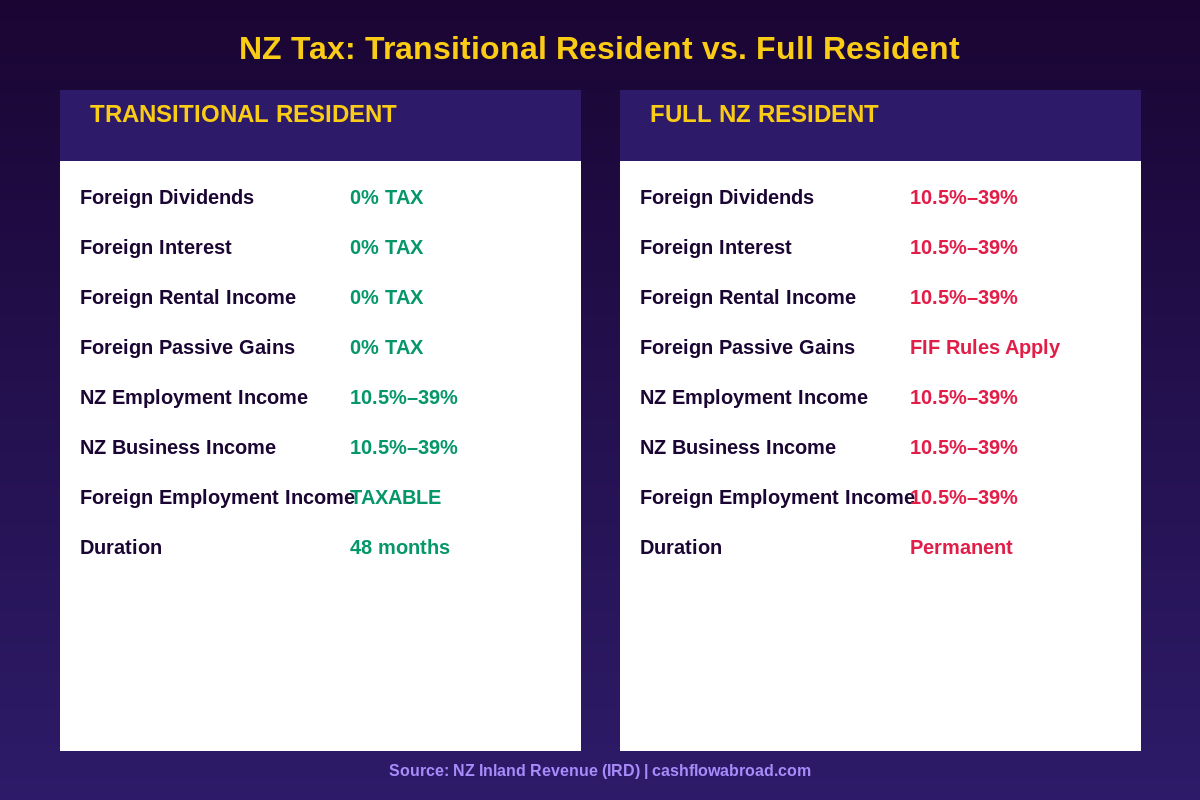

Here’s the deal: if you move to New Zealand and become a tax resident, you get a 48-month exemption on virtually all foreign passive income. Offshore dividends, foreign interest, overseas rental income, foreign trust distributions — all of it, completely tax-free for four years. The New Zealand Inland Revenue Authority (IRD) calls it the Transitional Resident Exemption, and it’s been sitting in the tax code since 2006, largely ignored by the mainstream expat community.

New Zealand’s top income tax rate is 39%. For someone with $200,000 in foreign passive income, that’s a $78,000 annual tax bill — turned to zero for up to four years. Let that sink in.

What Is New Zealand’s Transitional Resident Status?

When you first become a New Zealand tax resident — either by moving there as a new migrant or returning after a gap of at least 10 years — you automatically qualify as a transitional resident. No application, no form to file, no fee. You’re in by default.

The exemption window runs for 48 months from the date your NZ tax residence begins. Depending on exactly when your “permanent place of abode” in New Zealand is established, this window can technically stretch to up to 54 months.

Returning New Zealanders qualify under one strict condition: you must have been absent from New Zealand for at least 10 consecutive years before coming back. If you left in 2015 and come back in 2026, you’re in. If you left in 2020, you’re not — you have to wait until 2030.

For new migrants, there’s no prior residency requirement. Americans, Canadians, Brits — anyone gaining NZ tax residence for the first time qualifies automatically.

What Income Is Actually Exempt?

This is where you need to read carefully, because the exemption is broader than most people think but has one significant carve-out.

What the exemption covers (foreign-sourced):

- Dividends from foreign companies

- Interest from foreign bank accounts or bonds

- Rental income from foreign property

- Income subject to the Foreign Investment Fund (FIF) rules — including offshore ETFs and managed funds

- Distributions from foreign trusts

- Most other foreign passive income

What the exemption does NOT cover:

- Foreign employment income — salaries, wages, or consulting fees for services you personally perform during the exemption period, even if the employer is overseas

- Income from New Zealand sources (fully taxable from day one)

If you’re a remote worker earning a salary from a foreign employer, that income is taxable in NZ regardless of transitional resident status. But if you’re living off dividends, rental cash flow, bond interest, or trust distributions from overseas assets — you pay nothing for four years.

New Zealand’s Normal Tax Rates (What You’re Avoiding)

To understand the value of the transitional exemption, you need to see what full NZ residents actually pay on foreign passive income.

| Taxable Income (NZD) | Tax Rate |

|---|---|

| $0 – $15,600 | 10.5% |

| $15,601 – $53,500 | 17.5% |

| $53,501 – $78,100 | 30% |

| $78,101 – $180,000 | 33% |

| Above $180,000 | 39% |

On $200,000 USD in passive income (roughly NZD $333,000 at current rates), a full NZ resident would owe approximately NZD $117,000 (~$70,000 USD) in income tax annually. Under transitional residency, that’s $0 for 48 months — a four-year benefit worth over $280,000 USD.

Even for someone with a $500K investment portfolio generating 5% ($25,000/year), the annual tax savings under transitional residency run to roughly $8,000–$10,000 USD per year compared to full resident status. Multiply by four years: $32,000–$40,000 in total savings, just from timing your move correctly.

One more thing NZ doesn’t have: a capital gains tax. Gains on most investments — shares, property held long-term for capital purposes — aren’t taxed at all for anyone, transitional resident or not. Combined with the passive income exemption, it’s a genuinely favorable regime for wealth builders.

Critical Rules That Can Kill Your Exemption

The IRD doesn’t hand this out and let you forget about it. There are a handful of rules that can terminate your transitional resident status early — and some of them are surprising.

Working for Families Credits: If you or your partner apply for Working for Families (NZ’s family tax credit program), this is treated as a formal opt-out of transitional resident status. The opt-out is irrevocable — once you opt out, you can never go back, even if you’re still within the 48-month window. For expats with significant foreign income, Working for Families is rarely worth claiming anyway, but it’s a trap to know about.

One-time only: You can only ever use transitional resident status once. New migrants who eventually return to NZ after another absence don’t get a second 48-month window — that option only applies to Kiwis returning after a 10-year absence, and even then it’s once per lifetime.

Foreign employment income is always taxable: If you’re doing consulting, freelancing, or earning any kind of service income from foreign clients, that income is fully taxable in NZ from day one. The exemption is strictly for passive income. Remote workers on a foreign salary should run the numbers carefully — depending on your NZ-source income versus foreign salary, the FTC or tax treaty provisions may partially offset this.

NZ-source income is taxable immediately: Any income with a New Zealand source — local employment, NZ bank interest, NZ rental property, NZ dividends — is taxable from the moment you become a tax resident, regardless of transitional status.

What US Expats Need to Know: NZ + IRS Double Filing

New Zealand is one of the relatively small number of countries with a comprehensive tax treaty with the United States, signed in 1983 and updated since. That treaty matters for US expats because it clarifies which country gets primary taxing rights on various income types — but it doesn’t eliminate the US filing obligation.

American citizens moving to New Zealand still must file US tax returns and report worldwide income to the IRS every year. The key tools for minimizing the US tax bite:

Foreign Earned Income Exclusion (FEIE): If you’re working in NZ and earning employment income locally, the FEIE lets you exclude up to approximately $126,500 (2024) of foreign earned income from US tax. This covers wages and self-employment income — not passive income. See our guide to the FEIE for the full mechanics.

Foreign Tax Credit (FTC): Once you exit transitional resident status and start paying NZ tax on foreign income, you can claim the FTC to offset US taxes dollar-for-dollar with NZ taxes paid. Given NZ rates run up to 39%, this often eliminates most or all US tax owed on the same income. Our expat investing guide covers how to structure this efficiently.

PFIC warning: Foreign mutual funds and NZ-based managed funds typically qualify as PFICs (Passive Foreign Investment Companies) under US rules. NZ’s own FIF (Foreign Investment Fund) regime makes offshore ETFs complicated from both sides. US expats in NZ should hold US-domiciled ETFs through a US brokerage rather than buying NZ or Australian-domiciled funds. Charles Schwab International offers US brokerage accounts that stay open for expats in most countries, with free ATM withdrawals worldwide — one of the cleanest setups for expat investors who want to keep their US portfolio intact.

The combination of NZ transitional residency (zero NZ tax on foreign passive income for 4 years) plus the FEIE (zero US tax on NZ employment income up to ~$126K) creates a window where a well-structured US expat in NZ can have a very low combined tax rate on both income streams simultaneously.

Banking and Infrastructure for US Expats in NZ

New Zealand has a mature, English-language banking system — setting up a local account is straightforward once you have a visa and proof of address. Major banks include ANZ, ASB, BNZ, and Westpac NZ.

For keeping your US financial footprint intact — which matters for credit history, US investment account access, and IRS address — a Traveling Mailbox gives you a real US street address in 50+ cities at $15/month. Mail scanning, check deposits, and state domicile documentation all run through it. We cover the full use case in our virtual mailbox guide.

For US-based business banking, Mercury is a strong pick for expats — no monthly fees, solid international wires, and a US account structure that doesn’t close on you for living abroad. And for expat-specific FBAR and foreign account compliance strategy, the complete expat banking and tax guide covers every reporting obligation you’ll need to stay clean with the IRS.

Cost of Living in New Zealand: City by City

New Zealand has a reputation for being expensive, and it’s not entirely undeserved — but the comparison to the US is more nuanced than the headline numbers suggest. Numbeo’s 2026 data puts NZ at roughly 13% cheaper than the US overall, with rent running 39% lower than major US cities.

| City | 1-Bed Apartment (City Center) | Cost vs. US Index | Monthly Budget (Couple, USD) |

|---|---|---|---|

| Auckland | NZD $2,400–$3,200/mo | ~105% | $3,800–$5,200 |

| Wellington | NZD $2,000–$2,800/mo | ~100% | $3,200–$4,500 |

| Christchurch | NZD $1,600–$2,200/mo | ~90% | $2,500–$3,500 |

| Dunedin | NZD $1,200–$1,800/mo | ~85% | $2,000–$2,800 |

Auckland is legitimately expensive — housing approaches mid-tier US city pricing. But Christchurch and Dunedin tell a different story: high quality of life, world-class public healthcare, English as the native language, and monthly costs that undercut many American cities. The NZD currently trades at roughly $0.59–0.61 USD, which means NZD $2,000 in rent converts to about $1,200 USD.

Healthcare is a significant lever. New Zealand’s public system covers residents and is genuinely functional — not an afterthought. Emergency care and most specialist referrals are free or heavily subsidized. For coverage during the initial period before full public eligibility kicks in, SafetyWing’s Nomad Insurance fills the gap. Our full breakdown is in the expat health insurance guide.

How to Actually Get There: Visa Pathways

Transitional resident status only applies once you’re a NZ tax resident, which requires an approved visa and establishing a “permanent place of abode” in New Zealand. The main pathways:

Accredited Employer Work Visa (AEWV): Requires a job offer from an NZ-accredited employer. Valid up to 3 years, extendable, and leads to residency. Salaries for skilled workers typically run NZD $65,000–$120,000/year depending on field.

Skilled Migrant Category (SMC): Points-based visa for workers with high-demand skills. Usually requires a job offer; processing times vary.

Active Investor Plus Visa: Requires NZD $5 million in direct investment over 4 years. In USD terms, that’s roughly $3 million — steep, but significantly lower than comparable investment migration programs in Western Europe.

Temporary Retirement Visitor Visa: For 66+, requires NZD $750,000 (~$450K USD) in NZ investments, NZD $500,000 in living funds, and NZD $60,000/year in income. Two-year visa with renewal options.

Tax residency is generally confirmed once you’ve been in NZ for more than 183 days in any 12-month period and have established a permanent place of abode — meaning genuine intent to stay, not just a temporary rental. From that point, the 48-month clock starts.

Who This Strategy Works Best For

New Zealand’s transitional resident exemption isn’t for everyone. But for specific profiles, it’s genuinely compelling in ways that more obvious tax haven destinations aren’t.

High-income passive investors with $1M–$5M+ in offshore assets generating $50K–$250K/year in dividends, interest, or distributions will see the largest absolute benefit. Four years of 0% NZ tax on that income, combined with smart FTC treatment on the US side, can save hundreds of thousands of dollars over the exemption window.

Retirees drawing from foreign trusts, pension accounts, or brokerage portfolios are ideal candidates. The exemption applies directly to the income types most retirees live on. A US retiree with $2M in a brokerage account, a foreign rental property, and some bond income could pay zero NZ tax for four full years — then benefit from the NZ-US tax treaty when full residency kicks in.

People who want to actually live in New Zealand — not just maintain a mailbox residency. Unlike some tax structures that require you to live somewhere you’d otherwise never choose, NZ consistently ranks in the world’s top five for political stability, quality of life, safety, and natural beauty. The tax break is a bonus on top of a genuinely excellent place to be.

The profile this doesn’t fit: remote workers earning 100% active income from foreign employment. Your income is fully taxable regardless, and NZ’s progressive rates are steep. If pure active-income tax minimization is the goal, you’ll find better rates in Georgia, Bulgaria, or Romania.

The Bottom Line

New Zealand’s transitional resident exemption is a legitimate, statutory, fully documented tax break. No offshore structures, no complex trusts, no residency in a country you’d never voluntarily visit. You move to one of the world’s most desirable places to live, and your foreign passive income is untaxed for four years by default.

For a passive investor with meaningful offshore assets, the four-year window represents real money — often six figures or more in cumulative savings. For a US expat who layers in the FEIE and keeps a clean US brokerage setup, the combined tax picture is one of the most favorable available in any OECD country.

The only catch: you have to actually move there. Given what NZ offers, that’s not much of a catch.

Financial Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. New Zealand tax residency rules are complex and depend on individual circumstances. US citizens have worldwide tax reporting and filing obligations regardless of where they reside. Consult a qualified tax professional in both New Zealand and the United States before making any residency or investment decisions.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.