How Expats Legally Pay $0/Month on Student Loans

US expats using the FEIE can legally reduce IBR student loan payments to $0/month. With SAVE dead as of March 2026, here is how to implement this now.

Use the FEIE + IBR combination to reduce student loan payments to $0/month while living abroad. SAVE is dead — here is what works in 2026.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

42.8 million Americans owe a combined $1.83 trillion in student loans. A meaningful chunk of those borrowers are living abroad — and the vast majority have no idea they could be making $0 monthly payments while their loan clock ticks toward forgiveness. Legally. Using a mechanism the Department of Education built into the system themselves.

The mechanism: pair the Foreign Earned Income Exclusion (FEIE) with an income-driven repayment (IDR) plan. The FEIE reduces your US federal adjusted gross income (AGI) to near-zero. IDR plans calculate your monthly payment as a percentage of your discretionary income — derived directly from your AGI. Combine the two and your required payment collapses, often all the way to $0.

This isn't a loophole in the pejorative sense. It's arithmetic. Newsweek called it an "exposed loophole" in 2023 when it went viral on financial TikTok, but the DOE hasn't changed the rules. The math still works — with one major update: the SAVE plan is dead as of March 2026, and expats who haven't switched repayment plans face an urgent deadline.

The Math That Makes It Work

Income-driven repayment plans calculate your monthly payment using this formula:

Monthly payment = (AGI − 150% of Federal Poverty Line) × plan rate ÷ 12

For 2026, 150% of the Federal Poverty Line for a single person in the contiguous US is $23,940. For new IBR and PAYE, the payment rate is 10% of discretionary income (15% under old IBR for loans taken before July 1, 2014).

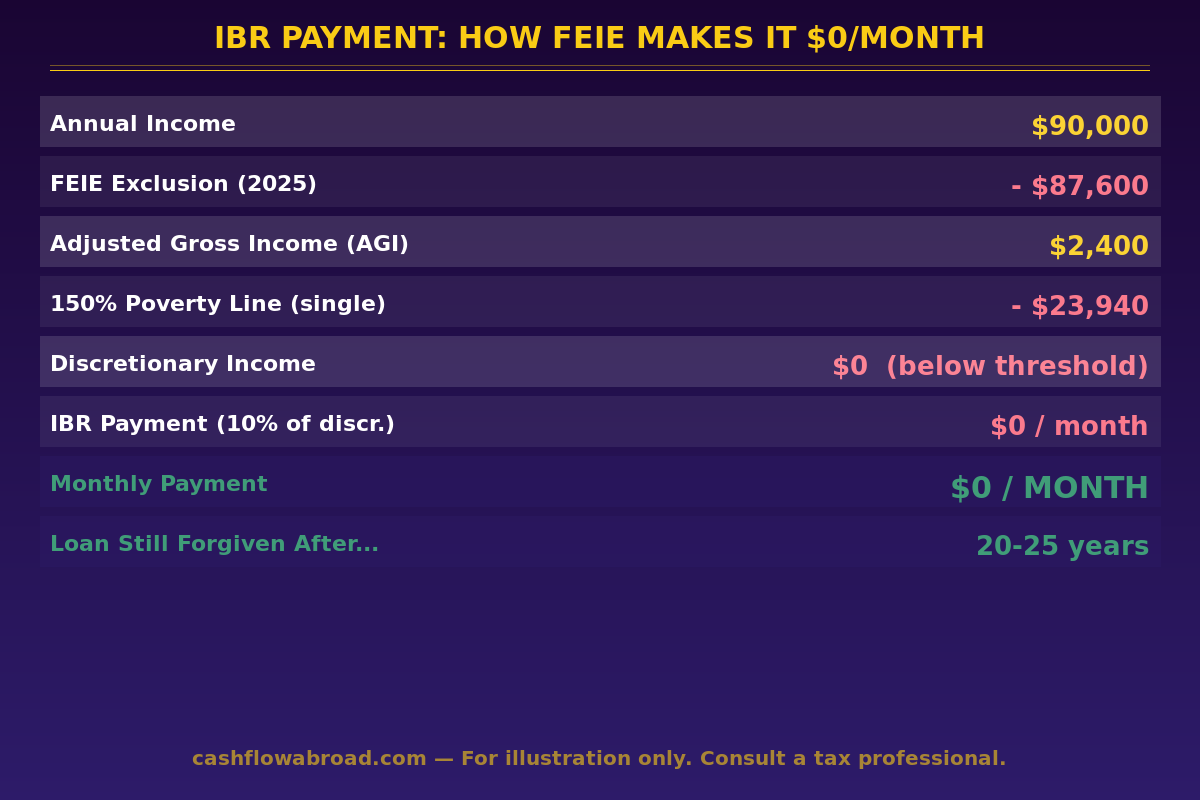

The FEIE for tax year 2025 allows you to exclude up to $130,000 of foreign-earned income from US federal taxes. If you earn under that threshold while living abroad, your federal AGI drops to roughly $0. When AGI ≤ 150% of the poverty line, discretionary income equals $0. Monthly payment equals $0.

| Step | Amount |

|---|---|

| Annual foreign income (salary or freelance) | $85,000 |

| Minus FEIE exclusion (2025 cap: $130,000) | −$85,000 |

| US Federal AGI after exclusion | $0 |

| Minus 150% poverty guideline (single, 2026) | −$23,940 |

| Discretionary income (floored at $0) | $0 |

| IBR monthly payment (10% ÷ 12) | $0 / month |

| Standard 10-year payment on $40,000 at 6.5% | ~$454 / month |

That is $5,448 per year you keep in your pocket — indefinitely — while each $0 payment counts as a qualifying payment toward IDR forgiveness. The average federal student loan balance is $39,547. Multiply 20 years of $0 payments against standard repayment and the gap exceeds $100,000 in payment avoidance before the forgiveness event.

How the Numbers Scale With Income

The strategy works most cleanly for borrowers earning under the FEIE cap. Above it, payments creep back up — but still far below standard repayment rates:

| Annual Foreign Income | FEIE Applied | AGI After FEIE | IBR Monthly Payment | Standard 10-yr ($40k loan) |

|---|---|---|---|---|

| $50,000 | $50,000 | $0 | $0 | $454 |

| $85,000 | $85,000 | $0 | $0 | $454 |

| $140,000 | $130,000 | $10,000 | $0* | $454 |

| $180,000 | $130,000 | $50,000 | $217 | $454 |

*$10,000 AGI still falls below the $23,940 poverty threshold — discretionary income floors at $0.

You would need to earn more than roughly $153,940 abroad before IBR payments break above $0 for a single filer. Even then, $217/month instead of $454/month is a material difference compounded over two decades.

Which Repayment Plans Work in 2026

The SAVE plan is gone. A federal appeals court issued its final ruling on March 10, 2026, officially vacating the Biden-era plan. Borrowers currently on SAVE must switch to an eligible repayment plan by July 1, 2026 — or they will be automatically placed on the Standard Plan, eliminating any payment reduction.

| Plan | Payment Rate | Poverty Threshold | Forgiveness | Works With FEIE Strategy? |

|---|---|---|---|---|

| New IBR (loans after 7/1/2014) | 10% | 150% FPL | 20 yrs undergrad / 25 yrs grad | Yes |

| Old IBR (loans before 7/1/2014) | 15% | 150% FPL | 25 years | Yes (slightly higher payment) |

| PAYE | 10% | 150% FPL | 20 years | Yes |

| ICR | 20% | 100% FPL | 25 years | Yes (only option for consolidated Parent PLUS) |

| SAVE | Vacated March 2026 | — | — | No — switch immediately |

| RAP (July 2026) | Variable | 100–150% FPL | 20–25 years | Likely yes — confirm when live |

As of July 4, 2025, the partial financial hardship requirement for IBR eligibility was removed, meaning essentially all federal loan borrowers can now enroll regardless of income. Log in to studentaid.gov, select "Change Repayment Plan," and request IBR. Servicers are required to process the switch.

The Income Verification Trap

IDR plans require annual recertification. Most borrowers use the IRS Data Link on StudentAid.gov, which pulls your AGI directly from your last filed return — where the FEIE exclusion has already been applied. Your servicer sees zero AGI and sets payment to $0.

The problem: some servicers request alternative income documentation — pay stubs, employer letters, or bank statements. If you hand over documents showing $85,000 in gross earnings, your servicer may calculate your payment based on gross income rather than AGI, wiping out the FEIE benefit entirely.

Your legal position is strong. The governing regulation (34 CFR 685.209) bases IDR payments on AGI from your most recent federal tax return. FEIE-excluded income is not taxable and does not appear in AGI by definition. If a servicer calculates a higher payment using alternative docs, file a complaint with the Federal Student Aid Ombudsman Group at studentaid.gov/feedback-center.

Best practice: always use the IRS Data Link for recertification — never manually enter income figures. If your servicer asks for additional documentation, provide only your official IRS tax transcript.

The Forgiveness Tax Bomb

IDR forgiveness is not free money. After 20–25 years, the cancelled balance becomes taxable as ordinary federal income — starting with forgiveness events in 2026 onward. The American Rescue Plan Act tax exemption expired December 31, 2025, and Congress did not extend it.

Realistic scenario: you borrow $40,000, pay $0/month for 20 years. Unpaid interest compounds on the principal throughout. At year 20, your outstanding balance might be $70,000 to $90,000. That balance is forgiven and added to your federal taxable income for that calendar year. At a 22% marginal rate on $80,000 in forgiven debt: a $17,600 tax bill due in a single year.

Mitigation options:

- Occasional lump-sum principal payments reduce the forgiven balance without losing $0/month status on regular billing

- A dedicated tax bomb fund — invest a fixed monthly amount in a taxable brokerage account earmarked for year-20 tax liability

- Income management before forgiveness — if you return to the US years before the forgiveness date, higher domestic AGI means higher IBR payments that pay down the balance before forgiveness

PSLF for Expats: What Qualifies

Public Service Loan Forgiveness — forgiveness after 10 years, no tax bill — is available to US expats under specific conditions. Your employer must be a US-based government entity or a US-registered 501(c)(3). Working for a foreign nonprofit, the UN, NATO, or an international organization does not qualify. The check-issuer's legal domicile determines eligibility, not where you perform the work.

Qualifying overseas situations:

- Peace Corps and AmeriCorps assignments (treated as US federal employment)

- US State Department foreign service positions

- Overseas branches of US universities where the US parent institution is the legal employer

- Remote employees of qualifying US nonprofits (physical location irrelevant — employer qualification is what matters)

Beginning July 1, 2026, the DOE can disqualify certain employers from PSLF eligibility based on evidence of "substantial illegal purpose" — a new political risk factor worth monitoring. If PSLF doesn't apply, IDR forgiveness at 20–25 years remains the backstop, with the tax exposure described above.

The US Infrastructure You Need

Federal loan servicers only accept payments from US bank accounts in US dollars. Two things must be in place before you can execute this strategy from abroad:

A US bank account that stays open while abroad. Most major retail banks close accounts for non-resident address holders. Mercury and Charles Schwab International both remain accessible to expats without requiring US presence, accept international wire transfers, and work seamlessly with loan servicer autopay. Schwab's debit card also reimburses worldwide ATM fees — useful when you're transferring funds between international accounts and your US servicer.

A valid US mailing address. Loan servicers, the IRS, and US financial institutions require a real US street address — PO boxes are frequently rejected. Traveling Mailbox provides a real street address in 50+ US cities, scans your mail digitally on demand, and handles check deposits for $15/month. It covers expat banking compliance, IRS correspondence, state domicile maintenance, and servicer mailing requirements simultaneously. The site owner uses it personally.

Set up autopay from your US account. Beyond the 0.25% interest rate reduction most servicers offer for autopay enrollment, it eliminates the risk of missing a recertification notice from abroad and accidentally triggering a payment reset.

For the full tax infrastructure, the FEIE strategy guide covers eligibility tests and Form 2555 mechanics in depth. Your state domicile situation matters too — several states do not recognize the FEIE for state income tax purposes, meaning your state-level AGI for state-administered loan programs may differ from your federal AGI. And for the full expat banking picture, the US expat banking and taxes guide covers the complete account stack.

Annual Recertification From Abroad

Recertification is fully digital and takes under 15 minutes. Missing it resets your payment to the Standard Plan amount until you re-certify — prior qualifying months are not lost, but the temporary overpayment won't be refunded.

- Log in to StudentAid.gov (a VPN may be needed in some countries — NordVPN is reliable for US government sites)

- Select "Manage Loans" → "Recertify Income" and use the IRS Data Link to pull your AGI automatically from your filed return

- Confirm family size and submit

- Servicer processes within 7–10 business days

File your US tax return before recertifying. If you're on extension (October deadline), recertify using the prior year return and update when the current year is processed. Set a calendar reminder 60 days before your annual deadline — servicer requests for documentation occasionally arrive, and you need time to respond without missing the window.

6 Steps to Implement This

- Confirm FEIE eligibility. Pass either the Physical Presence Test (330 days outside the US in a 12-month period) or the Bona Fide Residence Test. File Form 2555 with your annual return.

- Switch to IBR immediately if you're on SAVE — the July 1, 2026 deadline is firm. If you're on Standard or Graduated repayment, switch to IBR. No penalty; you can switch back if circumstances change.

- Open a Schwab or Mercury account (or confirm your existing US account remains accessible abroad). Enable autopay for student loan payments from it.

- Get a virtual US mailbox like Traveling Mailbox. Update your servicer, StudentAid.gov, and the IRS with the new address before leaving.

- File taxes first, then recertify. Use only the IRS Data Link — never manually enter income. FEIE will already be reflected in your AGI from the return.

- Build a tax bomb fund. Contribute a fixed monthly amount to a taxable brokerage account — tastytrade or SoFi both work well for US expats. This is not optional — the forgiveness tax bill is real and 20 years arrives faster than expected.

Bottom Line

The US tax code creates friction for expats in a dozen ways. The FEIE + IDR combination is one of the rare cases where the mechanics accidentally work in your favor. IDR plans were calibrated around domestic poverty thresholds; expats who qualify for the FEIE end up with artificially low AGI, and the payment formula responds to that mechanically.

The median federal student loan balance is $24,109. The average is $39,547. If you're carrying either of those balances, living abroad, earning under $130,000, and still on Standard repayment — you are likely sending thousands of dollars annually to your servicer that the law does not require you to pay. If you're on SAVE, switch to IBR before July 1, 2026. Then automate recertification each fall, and build the fund for the eventual forgiveness tax bill.

The balance will be forgiven. The payment savings are real. The tax event is coming. Plan for all three.

Financial Disclaimer: This article is for informational and educational purposes only and does not constitute legal, tax, or financial advice. Student loan repayment rules, FEIE eligibility requirements, income-driven repayment calculations, and applicable laws can change, and individual circumstances vary significantly. Consult a qualified US expat tax attorney or CPA before making changes to your repayment plan or tax filing strategy. Nothing in this article constitutes a guarantee of $0 payments, loan forgiveness, or specific tax outcomes.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 17, 2026

Expat Tax & FinanceMay 17, 2026

Federal Student Loans Abroad: The Zero-Payment Playbook

Use FEIE + IBR to pay $0/month on federal student loans while living abroad. Plus: the 2026 forgiveness tax bomb and how to plan for it.

Expat Tax & FinanceMay 11, 2026

Expat Tax & FinanceMay 11, 2026

Student Loans Abroad: The FEIE Zero-Payment Strategy

FEIE can cut your federal student loan payment to $0 legally. How IDR + foreign income exclusion work together for US expats.

Expat Tax & FinanceJuly 14, 2026

Expat Tax & FinanceJuly 14, 2026

Expat State Taxes: Which US States Won't Let You Go

Move abroad and California may still tax you 13.3%. Learn which five states chase expats, how domicile works, and how to sever state ties legally.