Federal Student Loans Abroad: The Zero-Payment Playbook

Living abroad can legally drop your federal student loan payment to $0. Here’s how FEIE + IBR works together—and the 2026 tax bomb you must plan for.

Use FEIE + IBR to pay $0/month on federal student loans while living abroad. Plus: the 2026 forgiveness tax bomb and how to plan for it.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

There are 43 million Americans carrying federal student debt totaling $1.77 trillion. A growing share of them have discovered something counterintuitive: leaving the country can drop their monthly payment to $0 — legally, permanently, while the forgiveness clock keeps running.

When a US expat combines the Foreign Earned Income Exclusion (FEIE) with an Income-Based Repayment (IBR) plan, their Adjusted Gross Income can fall to zero. And when your AGI is $0, your federal student loan payment under IBR is also $0. Not deferred. Not in forbearance. Officially $0 per month — while the 20-to-25-year forgiveness timeline continues accruing.

But 2026 brought changes that most expats haven't processed. The SAVE plan is gone. Loan forgiveness is now taxable for the first time since 2021. A new plan called RAP is reshaping the IDR landscape. If you're managing federal loans from abroad — or considering leaving the US while carrying debt — this is what you need to know.

The Core Strategy: FEIE + IBR = $0 Monthly Payment

The mechanics are straightforward once you understand how IBR calculates payments. Under Income-Based Repayment, your monthly bill equals 10% of your discretionary income divided by 12. Discretionary income is your AGI minus 150% of the federal poverty line for your household size.

For a single person in 2026, the federal poverty line is $15,060. At 150%, that's $22,590. If your AGI falls below that threshold, your IBR payment is $0.

The FEIE is what drives the AGI down. For tax year 2026, Americans living abroad can exclude up to $132,900 of foreign-earned income from US federal taxes. That exclusion reduces your AGI dollar-for-dollar. An expat earning $100,000 in Lisbon, Medellín, or Chiang Mai has an AGI of $0 after the exclusion — well below the $22,590 IBR threshold.

To qualify, you need to pass either the Physical Presence Test (330 days outside the US in a 12-month period) or the Bona Fide Residence Test (established residence in a foreign country). Once you elect the exclusion on Form 2555, your AGI drops and your IBR payment follows. Our complete FEIE guide covers the qualification tests and how to file in detail.

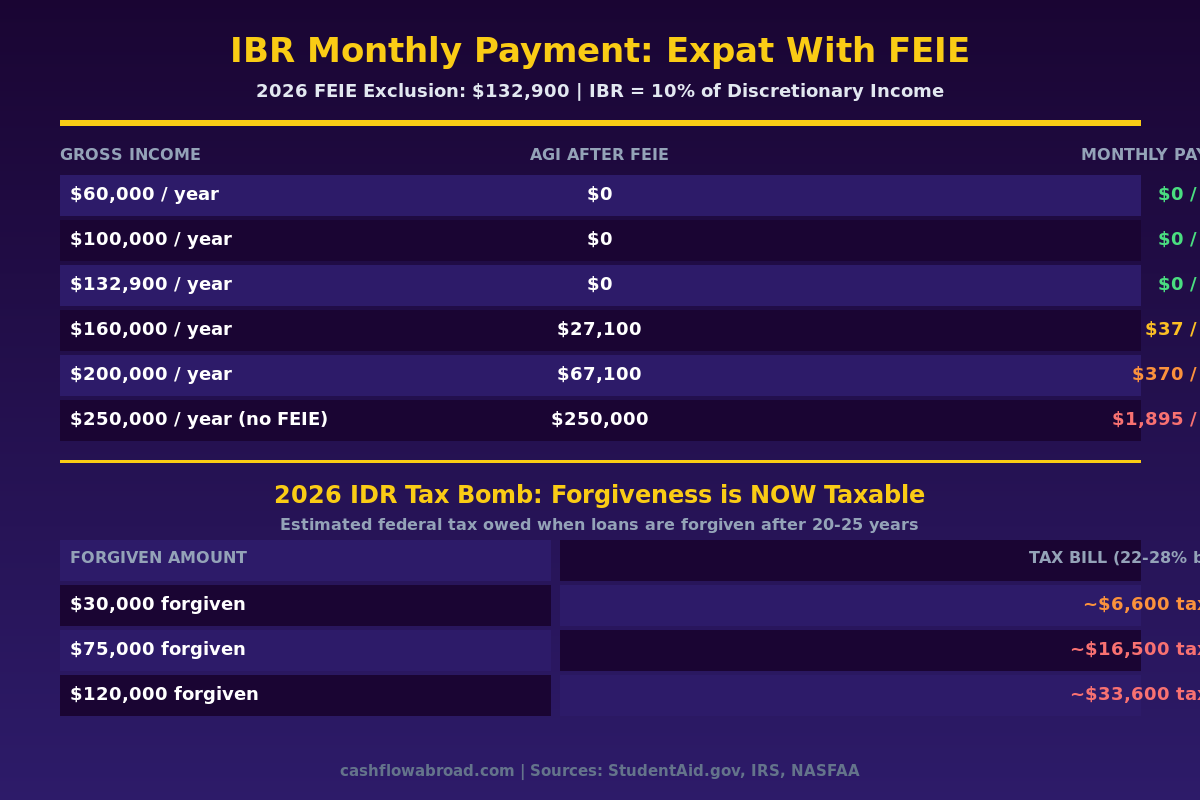

The Payment Math for Real Income Levels

| Gross Income (Earned Abroad) | AGI After FEIE ($132,900 exclusion) | IBR Monthly Payment |

|---|---|---|

| $60,000 | $0 | $0 |

| $100,000 | $0 | $0 |

| $132,900 | $0 | $0 |

| $160,000 | $27,100 | ~$37/month |

| $200,000 | $67,100 | ~$370/month |

| $250,000 (no FEIE) | $250,000 | ~$1,895/month |

Important caveat: the FEIE covers only earned income — salary, self-employment income, freelance wages. Passive income such as dividends, capital gains, and rental proceeds still flows through to AGI. If your $100k income is primarily investment returns, this strategy won't produce the same result. Our FEIE vs. Foreign Tax Credit breakdown covers which income types each provision addresses.

The SAVE Plan Is Dead. Here's What to Do Now.

For borrowers currently on SAVE: your plan is finished. A federal court blocked its core provisions in 2025, and the Trump administration reached a formal settlement with Missouri to wind it down completely. No new enrollments are accepted. The 7.7 million borrowers on SAVE must migrate to a new plan by July 2028.

There's a 90-day window starting July 1, 2026 to choose a replacement. Miss it and your servicer auto-enrolls you in Standard Repayment — which calculates payments based on your full loan balance and ignores AGI entirely. For a borrower expecting $0/month, that's a brutal outcome.

Two realistic options for expats:

Option 1: Income-Based Repayment (IBR) — Best for FEIE Users

IBR is the right plan for most expats relying on the FEIE strategy. Payments are 10% of discretionary income (AGI minus 150% of the poverty line), which means the FEIE can genuinely produce $0. The partial financial hardship requirement that used to gatekeep IBR enrollment was removed in 2025 — any borrower with eligible federal Direct Loans can now enroll regardless of current income. Forgiveness triggers after 20 years for undergraduate loans and 25 years for graduate loans.

Option 2: Repayment Assistance Plan (RAP) — New in 2026

The RAP plan launches July 1, 2026. Monthly payments range from 1% to 10% of earnings on a sliding scale, with 20-year forgiveness for all borrowers. The FEIE interaction with RAP is still being clarified by servicers — whether payments are based on gross income or AGI-after-exclusion hasn't been consistently implemented. Until official guidance is explicit, IBR is the more predictable default for expats depending on $0 payments.

PAYE and ICR are being phased out entirely by July 2028. If you're on either, begin the transition now.

Managing Federal Loans from Abroad: The Practical Side

The strategy itself is clean. The administration is where friction appears.

Annual income recertification: Every IDR plan requires annual recertification of your income. Miss the deadline and your servicer recalculates using your original loan balance — generating a payment you don't want and potentially a gap in your forgiveness timeline. Set a calendar reminder 90 days before your recertification date, every year, without exception.

Documentation: To certify $0 or near-zero income as an expat, you submit your US tax return showing the FEIE election via Form 2555. The number your servicer uses is line 11 on Form 1040 — your AGI. Make sure the return is filed before recertification is due.

US mailing address: Loan servicers require a physical US address for correspondence, recertification notices, and legal documents. Using a family member's address creates complications; a virtual mailbox is cleaner. Traveling Mailbox gives you a real US street address in 50+ cities, scans incoming mail digitally, and deposits checks — for $15/month. It's the same infrastructure that solves the address problem for IRS correspondence, banking, and brokerage accounts simultaneously. We cover the full setup in our virtual mailbox guide for expats.

Making payments from abroad: When your IBR payment is $0, this doesn't matter. If you owe a small monthly amount, paying from a foreign bank can trigger wire fees that exceed the payment itself. Keep a US-based checking account active for loan payments. Mercury is free and works cleanly for expats maintaining US banking. When you need to move money internationally, Remitly offers competitive exchange rates without the inflated fees most US banks charge for international transfers. The full expat banking setup is in our US Expat Banking Guide.

The 2026 Tax Bomb: Forgiven Loans Are Now Taxable

This is the part most FEIE calculators and YouTube explainers skip over.

The American Rescue Plan Act of 2021 temporarily shielded forgiven student loan balances from federal income tax. That exemption expired December 31, 2025 and was not renewed. Starting January 1, 2026, any federal student loan balance forgiven under an IDR plan is treated as ordinary taxable income in the year of forgiveness.

The FEIE will not help you here. It covers earned income only — not debt cancellation income. The forgiven amount lands on your Form 1040 in full, in a single tax year. Estimated impact by balance:

| Forgiven Balance | Estimated Tax at 22–28% Bracket | Net Outcome vs. Paying in Full |

|---|---|---|

| $30,000 forgiven | ~$6,600–$8,400 | $21,600–$23,400 saved net |

| $60,000 forgiven | ~$13,200–$16,800 | $43,200–$46,800 saved net |

| $100,000 forgiven | ~$22,000–$28,000 | $72,000–$78,000 saved net |

| $150,000 forgiven | ~$33,000–$42,000 | $108,000–$117,000 saved net |

Even with the tax bill, IDR forgiveness wins mathematically for most high-balance borrowers. The problem isn't that the strategy is broken — it's that the tax bill arrives as a lump sum in the year of forgiveness, and unprepared borrowers get blindsided.

How to prepare: Start building a dedicated "tax bomb fund" now. If forgiveness is 10 years away, estimate your forgiven balance (accounting for interest accrual during $0-payment years) and reverse-engineer what you need to set aside annually. A taxable brokerage account in broad US-listed ETFs works well — liquid, growing, accessible when needed. Our Expat Investing Playbook explains which US-listed funds avoid the PFIC trap that foreign-domiciled ETFs trigger for American investors.

PSLF remains permanently tax-free. Public Service Loan Forgiveness — 10 years of qualifying payments while working for a US government or nonprofit employer — is exempt from federal income tax by statute. This path is not available to most expats since it requires active employment with a qualifying US employer. But if it applies to you, the forgiveness is clean.

When This Strategy Doesn't Apply

Worth naming the exceptions directly:

- Private loans: None of this applies to private student loans — SoFi refinanced debt, Sallie Mae, or any other private lender. Private loans have no IDR plans and no forgiveness pathway. If you refinanced federal loans to private to capture a lower rate, you permanently gave up IDR access and forgiveness eligibility. That trade-off may still make sense depending on your balance and income trajectory, but you need to know it exists.

- Passive income earners: If your income abroad is primarily dividends, rental proceeds, or capital gains, the FEIE doesn't reduce it. Your AGI remains elevated and IBR payments follow.

- Near-term homebuyers: $0 loan payments look clean on a tax return but create friction on mortgage applications. Conventional lenders typically use 0.5%–1% of your outstanding loan balance as a monthly obligation in their debt-to-income calculation, regardless of actual IDR payments. If you're buying property within two to three years, model your DTI with this in mind.

- Standard Repayment borrowers: This strategy requires enrollment in an IDR plan. Standard 10-year repayment is fixed and payment-blind to AGI. You must be on IBR (or RAP once its FEIE interaction is confirmed) for the $0 scenario to work.

- High earners above the FEIE cap: Once your foreign earned income exceeds $132,900, additional income flows directly to AGI and increases IBR payments. At $200,000 in foreign earned income, your monthly payment is still ~$370 — meaningful, but far below what it would be on Standard Repayment.

5-Step Action Plan for Expats With Federal Loans

- Confirm your loans are federal Direct Loans. Log into studentaid.gov to verify loan types, servicer, and outstanding balances. Only federal Direct Loans qualify for IBR enrollment and IDR forgiveness. FFEL loans may need to be consolidated first.

- Switch to IBR now if you're on SAVE. Don't wait for the July 2026 window. Log into your servicer's portal and request IBR enrollment immediately. Processing can take 30–60 days, and the window is narrower than it looks.

- Elect the FEIE on your US tax return. File Form 2555 with your Form 1040. This is an affirmative election — it doesn't apply automatically. If you've been abroad and haven't been claiming it, you may be able to file amended returns for prior years to recapture missed benefits.

- Recertify annually using your FEIE-reduced AGI. When your servicer requests recertification, submit documentation reflecting your AGI after the FEIE exclusion. Your $0 or near-$0 AGI produces your $0 or near-$0 payment. Never let recertification lapse.

- Fund a tax bomb account starting now. Open a US brokerage account and direct what you would have paid toward loans into broad-market US ETFs. Let it compound for 15–20 years. When forgiveness arrives, the tax bill is covered — and you likely have surplus growth on top of it.

The Bottom Line

The $0 monthly payment strategy is real, legal, and operating exactly as the tax code was written. An expat who earns $80,000 in Barcelona and pays $0/month on their federal loans while the IBR forgiveness clock runs isn't gaming anything — they're using a provision Congress designed. The FEIE was created to prevent double taxation for Americans living and working abroad. Its side effect on IDR payments is a feature of how the calculations interact, not a loophole.

What changed in 2026 is the back-end tax treatment. The forgiven balance is now a taxable event, and planning for it — not ignoring it for 20 years — is the difference between a strategy that works and one that produces an expensive surprise. The math still favors IDR forgiveness for most high-balance borrowers, but only if you build for the tax bill and keep the recertification calendar intact.

Know the mechanism. Work the calendar. Keep a US address. Those three things are the entire operational requirement for making this work.

This post is for informational purposes only and does not constitute financial, tax, legal, or student loan advice. Student loan regulations and income-driven repayment rules change frequently — the SAVE plan wind-down, RAP launch, and forgiveness taxability are all active policy areas. Consult a qualified expat tax professional or student loan attorney before making repayment decisions. Tax treatment varies by individual circumstances, income type, and jurisdiction.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 26, 2026

Expat Tax & FinanceMay 26, 2026

How Expats Legally Pay $0/Month on Student Loans

Use the FEIE + IBR combination to reduce student loan payments to $0/month while living abroad. SAVE is dead — here is what works in 2026.

Expat Tax & FinanceMay 11, 2026

Expat Tax & FinanceMay 11, 2026

Student Loans Abroad: The FEIE Zero-Payment Strategy

FEIE can cut your federal student loan payment to $0 legally. How IDR + foreign income exclusion work together for US expats.

Expat Tax & FinanceMay 29, 2026

Expat Tax & FinanceMay 29, 2026

Self-Employment Tax: The Expat Freelancer’s Hidden Bill

FEIE zeroes your income tax abroad—but SE tax still applies. See the exact numbers and legal ways to reduce your bill as a US expat freelancer.