Student Loans Abroad: The FEIE Zero-Payment Strategy

FEIE can legally cut your federal student loan payment to $0 abroad. Here's how income-driven repayment + the foreign earned income exclusion work together.

FEIE can cut your federal student loan payment to $0 legally. How IDR + foreign income exclusion work together for US expats.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Here's a number that should make any expat with student loans sit down: the average American has $38,787 in federal student loan debt, and millions of them are quietly making payments every month when, under the Foreign Earned Income Exclusion, they could legally owe $0.

Not $50. Not $80. Zero.

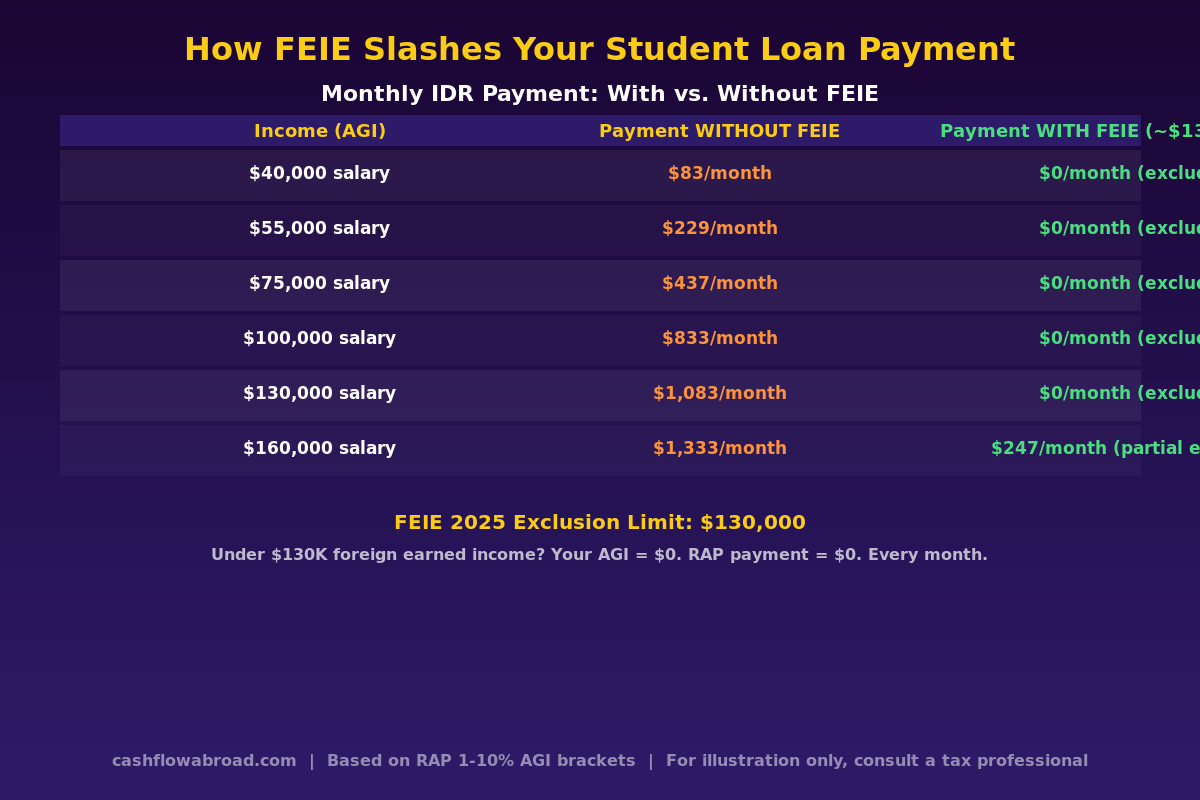

This isn't a loophole in the shadowy sense—it's a straightforward consequence of how income-driven repayment plans calculate your monthly bill. Your payment is based on your adjusted gross income. FEIE legally reduces that income. Do the math, and for most expats earning under $130,000 abroad, the result is a monthly student loan payment of absolutely nothing.

And with 7.5 million borrowers now scrambling after the SAVE plan was dismantled in 2026, understanding this strategy has become more urgent than ever.

How Income-Driven Repayment Plans Actually Work

Before getting to the FEIE angle, it helps to understand why your payment can drop so dramatically. Under income-driven repayment (IDR), the government doesn't care how much you borrowed. Your monthly bill is calculated from your income and family size, not your balance.

The surviving IDR plans all start from the same basic premise: take your adjusted gross income (AGI), subtract a poverty-line threshold, and charge you a percentage of what's left. The key variable is your AGI—and that's exactly what FEIE attacks.

Under IBR (Income-Based Repayment), your payment is 10% of discretionary income, defined as AGI minus 150% of the federal poverty guideline. For a single person in 2025, 150% of the poverty line is roughly $22,590. If your AGI is $22,590 or less, your payment is $0.

The new Repayment Assistance Plan (RAP), launching July 1, 2026, takes a more direct approach: payments range from 1% to 10% of total AGI across 11 income brackets, with a flat $10 minimum. If your AGI is $0, your payment is $10 per month—the minimum floor. If your AGI under the FEIE calculation still comes out above zero but below the threshold for a meaningful payment, you could still see dramatically lower bills.

What FEIE Does to Your AGI—and Your Loan Payment

The Foreign Earned Income Exclusion lets Americans living and working abroad exclude up to $130,000 of foreign-earned wages from US federal income tax (2025 amount; it adjusts annually for inflation). You claim it by filing Form 2555 with your tax return.

Here's the part that surprises most people: the excluded income also disappears from your AGI calculation. For IDR purposes, the IRS bases your payment on your AGI as reported—not on what you actually earned. So if you make $80,000 as a developer working remotely from Medellín, and you qualify for FEIE, your AGI for IDR purposes becomes $0. Or close enough to it that your payment floors out.

The math is blunt:

- You earn $80,000 abroad

- FEIE excludes $80,000 (you're under the $130K limit)

- AGI = $0

- IDR payment = $0 (or $10/month under RAP's floor)

While your colleagues back in Chicago are cutting checks for $400+ per month on their loans, you're effectively paying nothing—and the interest may not even accrue on some plans thanks to interest subsidies.

The SAVE Plan Is Dead: What Replaced It

If you've been on SAVE, this year was a rude awakening. The Biden-era Saving on a Valuable Education plan—which offered the lowest discretionary income threshold in history—was ruled unlawful and killed by the Trump administration. All 7.5 million SAVE borrowers were directed to exit the plan immediately.

The replacement options as of mid-2026:

| Plan | Payment Formula | Forgiveness Timeline | Available Now? |

|---|---|---|---|

| IBR (original) | 10% discretionary income (150% poverty line threshold) | 20 years (new borrowers: 25 years) | Yes |

| IBR (2014+) | 10% discretionary income | 20 years | Yes (if borrowed after July 2014) |

| RAP (new) | 1%–10% of total AGI by bracket; $10 minimum | 30 years | July 1, 2026 |

| Standard | Fixed monthly based on balance | 10 years | Yes |

| PAYE | 10% discretionary income | 20 years | Being phased out |

For expats using FEIE, the choice between IBR and RAP (once available) will depend on your specific situation. IBR's discretionary income formula hits $0 when your AGI is at or below 150% of the poverty line. RAP hits a $10/month floor regardless. For most expats with a true FEIE-zeroed AGI, both options result in negligible or no payments.

The Forgiveness Tax Bomb: A 2026 Trap Nobody's Talking About

Here's where the strategy gets complicated—and where most expats planning to "ride out" IDR for 20-25 years need to recalibrate.

The American Rescue Plan Act (ARPA) temporarily made IDR forgiveness tax-free from 2021 through December 31, 2025. That exemption has now expired. Starting with forgiveness received in 2026 and beyond, any balance wiped out at the end of your IDR term is added to your taxable income for that year.

The math is brutal:

| Balance Forgiven | Tax Bracket | Estimated Federal Tax Bill |

|---|---|---|

| $30,000 | 22% | ~$6,600 |

| $50,000 | 22% | ~$11,000 |

| $80,000 | 24% | ~$19,200 |

| $120,000 | 32% | ~$38,400 |

That's not a surprise you want to face in your 40s or 50s. The one major exception: Public Service Loan Forgiveness (PSLF) remains permanently tax-free.

This changes the calculus for expats on a pure IDR-to-forgiveness plan. If you're 8 years into a 20-year forgiveness track and your balance has ballooned due to years of $0 payments, you need to model whether the forgiveness tax bomb is bigger than just aggressively paying down the loan over the next decade. In many cases, investing those "saved" payments in a brokerage account while abroad builds more wealth than either option.

PSLF from Abroad: Who Qualifies

If you're working for a US-based employer while living abroad, Public Service Loan Forgiveness might be the best deal in the room. PSLF forgives your remaining balance after 120 qualifying payments (10 years)—and it does so tax-free, permanently.

The catch: your employer must be a qualifying public service organization under US law. Working for a foreign government or local NGO doesn't count, no matter how much good you're doing. Here's how it breaks down:

| Employment Type | PSLF Eligible? |

|---|---|

| US Federal Government employee working abroad | Yes |

| US 501(c)(3) nonprofit with remote foreign employees | Yes |

| Foreign government | No |

| Foreign private employer | No |

| Foreign NGO (not US 501(c)(3)) | No |

| Self-employed / freelance | No |

| US for-profit employer with remote work abroad | No |

Note that as of July 1, 2026, a new PSLF rule also excludes employers that engage in illegal activities with a "substantial illegal purpose" (specifically targeting organizations involved in terrorism or aiding illegal immigration). For the vast majority of expats working for US nonprofits or government, nothing changes.

If you work for a US nonprofit or government agency from abroad, PSLF plus FEIE is a powerful combination: $0 monthly payments on IDR plans plus tax-free forgiveness after 10 years. Aggressively pursue this route if it applies to you.

The Real Strategy: Pay Down or Ride It Out?

There's no universal right answer here. The $0 IDR payment is valuable not just for the savings—it's capital that can be deployed somewhere more productive. Let's look at the realistic options:

Option A: IDR + Invest the Difference

If your IDR payment would be $300/month in the US and is $0 abroad, that's $3,600/year freed up. Invested in a diversified portfolio with an 8% average return over 20 years, you're looking at roughly $178,000—likely more than the original loan balance. When forgiveness arrives (and the tax bill with it), you have the assets to cover it.

This approach works best when your loan balance is large relative to income, and you're likely to have a significant balance left at forgiveness time. See our expat investing guide to understand which account structures to use when investing from abroad—PFIC rules apply and can bite hard if you use foreign funds.

Option B: Aggressive Payoff

If your loan balance is moderate (under $40,000) and you have strong income abroad, sometimes the cleanest move is to direct 12-18 months of savings toward killing the loans entirely. With the FEIE reducing your tax burden, your cash flow abroad is often higher than it would be in the US—use that asymmetry. This eliminates the forgiveness tax bomb entirely.

Option C: PSLF Route (Best if Eligible)

If you work for a qualifying US employer, put every spare dollar elsewhere and make only your IDR-required payments (even $0) for 10 years. You'll be paid back in tax-free forgiveness. This is the unambiguous winner if you qualify.

How to Keep Your $0 Payment Going: The Practical Side

The IDR payment system is set up for people who are present in the US and filing simple tax returns. Managing it from abroad requires some intentional systems:

Annual Income Certification

Every IDR plan requires you to certify your income annually. Miss the deadline, and your payment jumps to the standard amount instantly—no grace period. Set a calendar reminder for 60 days before your certification due date. You'll submit your prior-year tax return (Form 1040 + Form 2555) showing your FEIE exclusion, which is your documentation that your AGI is low or zero.

Maintain a US Address

Loan servicers, the IRS, and your bank all need a US mailing address on file. This isn't optional—missed correspondence has tanked repayment plans for expats who didn't realize they needed it. A virtual mailbox like Traveling Mailbox gives you a real US street address, scans your mail, and forwards critical documents. For the $15/month cost, it's essential infrastructure for any expat managing US financial accounts.

Keep a US Bank Account Active

Your loan servicer will attempt to debit your US bank account for payments—even $0 or $10 payments generate a transaction. Keep a US account funded with enough to cover any minimum. Mercury works well for this if you're running a US business from abroad. For personal banking, Charles Schwab International remains the gold standard for expats—no foreign transaction fees, free ATM withdrawals worldwide, and a brokerage account under the same roof.

File US Taxes Every Year—On Time

This one should be obvious, but it bears stating: the FEIE only works if you file. Many expats believe that if they owe nothing, they don't need to file. Wrong. You need Form 2555 on record for income certification to work. Our full expat banking and tax guide covers the filing timeline and key forms in detail.

Who This Strategy Is For—and Who It Isn't

The FEIE zero-payment strategy makes the most sense when:

- Your foreign-earned income is under $130,000 and you qualify as a bona fide resident or pass the physical presence test

- Your loan balance is large enough that forgiveness is a realistic outcome (generally $50,000+)

- You're investing the "saved" payments rather than spending them

- You have a plan for the forgiveness tax bill (either PSLF or a brokerage account to cover it)

It's less compelling when:

- Your balance is under $25,000—aggressive payoff may be cleaner

- Your income is over $130,000 and you'd only qualify for partial FEIE exclusion

- You're close to PSLF eligibility but using a non-qualifying employer—in which case, switch employers or at least model the numbers

- You plan to return to the US within 2-3 years and the IDR payment will revert to a normal (possibly high) amount anyway

One important note: this strategy interacts with your eligibility for the Roth IRA. FEIE reduces your "earned income" for purposes of Roth contributions. If your entire income is excluded, you can't contribute to a Roth that year. There are workarounds (a backdoor Roth conversion doesn't require earned income), but it's a trade-off worth understanding before you commit to full FEIE exclusion.

The Bottom Line

Most Americans with student loans never connect the dots between FEIE and their loan servicer's payment calculation. These two systems—international tax law and federal student aid—don't talk to each other. But the numbers do. If you're earning under $130,000 abroad, filing Form 2555, and enrolled in an income-driven repayment plan, you have a legal, IRS-sanctioned path to a $0 monthly student loan payment.

That's not a loophole. It's a feature. Use it intentionally: model your forgiveness timeline, account for the tax bomb, and put the savings to work in a brokerage account rather than letting them evaporate into lifestyle inflation. The SAVE plan is gone, but the underlying math of FEIE + IDR is very much alive.

Financial Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Student loan regulations change frequently—consult a qualified tax professional or student loan advisor before making decisions about your repayment strategy. FEIE eligibility depends on your specific facts and circumstances.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 26, 2026

Expat Tax & FinanceMay 26, 2026

How Expats Legally Pay $0/Month on Student Loans

Use the FEIE + IBR combination to reduce student loan payments to $0/month while living abroad. SAVE is dead — here is what works in 2026.

Expat Tax & FinanceMay 17, 2026

Expat Tax & FinanceMay 17, 2026

Federal Student Loans Abroad: The Zero-Payment Playbook

Use FEIE + IBR to pay $0/month on federal student loans while living abroad. Plus: the 2026 forgiveness tax bomb and how to plan for it.

Expat Tax & FinanceJuly 14, 2026

Expat Tax & FinanceJuly 14, 2026

Expat State Taxes: Which US States Won't Let You Go

Move abroad and California may still tax you 13.3%. Learn which five states chase expats, how domicile works, and how to sever state ties legally.