The FEIE Self-Employment Tax Trap for Expat Freelancers

FEIE zeroes your income tax — but not SE tax. Expat freelancers still owe up to $21k on $150k income. Here's how to reduce or eliminate it.

FEIE won't save expat freelancers from SE tax. Learn what you actually owe, which countries offer exemptions, and 3 strategies to reduce the bill.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

You moved abroad, claimed the Foreign Earned Income Exclusion, and watched your federal income tax bill drop to zero. You're a genius. Then the IRS sends you a bill for $14,130. On the exact same $100,000 you just excluded.

Welcome to the self-employment tax trap — the most expensive blind spot in expat freelancer tax planning. FEIE is real, it's powerful, and it works exactly as advertised for income tax. But self-employment tax (SE tax) is not income tax. It's a parallel levy with its own rules, its own calculation, and its own immunity to Form 2555. Every year, thousands of freelancers and consultants living abroad file confidently with FEIE and still owe five figures they didn't budget for.

Here's everything you need to understand — including three strategies that can actually reduce or eliminate it.

What the FEIE Actually Does (And Doesn't Do)

The Foreign Earned Income Exclusion lets qualifying US citizens exclude up to $130,000 (2025) or $132,900 (2026) of foreign-earned income from federal income tax. That's it. Not total tax. Not all federal tax. Income tax specifically.

Self-employment tax is a separate line on your return — Schedule SE — that funds Social Security and Medicare. The IRS treats it as distinct from income tax, and Form 2555 has exactly zero effect on it. The instructions are unambiguous: "The exclusion of income under the FEIE does not reduce your self-employment tax."

This distinction matters enormously when you're a freelancer, independent contractor, or sole proprietor working abroad. W-2 employees at foreign companies have a different situation — their employer pays half the payroll taxes locally. Self-employed workers are paying both the employer and employee portions themselves, at 15.3% combined.

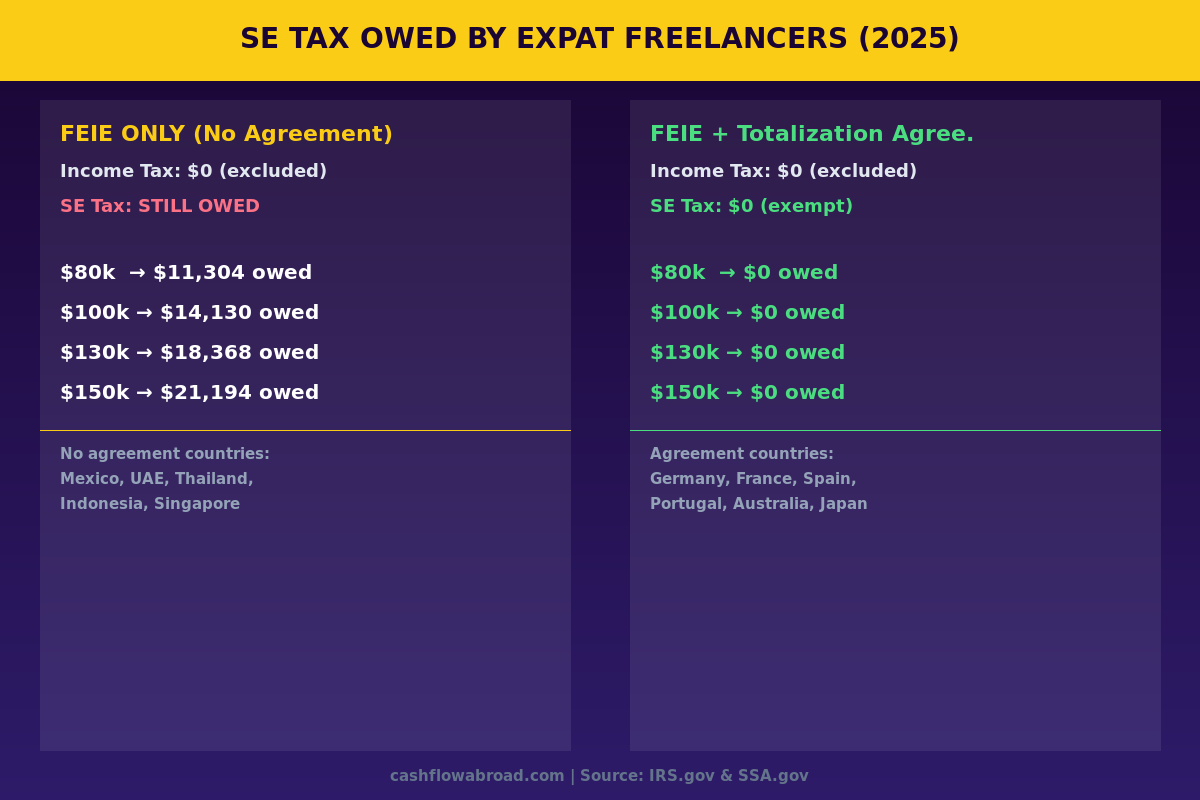

The Exact Math: What You Actually Owe

SE tax doesn't apply to 100% of your net income — the IRS gives you a slight adjustment. You multiply net self-employment earnings by 92.35% first (this accounts for the deductible "employer half"), then apply the 15.3% rate to that figure. Social Security kicks in at 12.4% up to the wage base ($176,100 for 2025, $184,500 for 2026), and Medicare runs at 2.9% on everything.

| Gross Self-Employment Income | After 92.35% Factor | SE Tax Owed (15.3%) | Federal Income Tax with FEIE |

|---|---|---|---|

| $80,000 | $73,880 | $11,304 | $0 |

| $100,000 | $92,350 | $14,130 | $0 |

| $130,000 | $120,055 | $18,368 | $0 |

| $150,000 | $138,525 | $21,194 | $0 (on first $130k) |

These numbers assume 100% of income qualifies as foreign-earned income and you pass either the bona fide residence or physical presence test. The core point stands: FEIE zeros out your income tax and leaves your SE tax completely intact.

The one partial offset: half of your SE tax (the "employer half") is deductible from your adjusted gross income on Form 1040. On a $14,130 bill, that's a ~$7,065 deduction — but since FEIE already wiped out your taxable income, this deduction is often worthless. You can't deduct against zero.

The Totalization Agreement Escape Hatch

Here's the biggest relief mechanism most expat freelancers never hear about: totalization agreements. The US has signed these bilateral Social Security treaties with approximately 30 countries. If you're self-employed in a country with one, you pay into that country's social security system and are fully exempt from US SE tax.

To claim the exemption, get a Certificate of Coverage from your host country's social security authority and attach it to your US return. The SE tax line goes to zero.

| Countries WITH US Totalization Agreements | Popular Expat Destinations WITHOUT Agreements |

|---|---|

| Germany, France, Spain, Portugal, Italy | Mexico, Thailand, Indonesia |

| Australia, Japan, South Korea | UAE, Singapore, India |

| Brazil, Chile, Uruguay | China, Vietnam, Philippines |

| Canada, Netherlands, Sweden | Colombia, Panama, Costa Rica |

| Poland, Czech Republic, Hungary | Malaysia, Georgia, Albania |

Notice the painful irony: the most popular digital nomad destinations — Thailand, Mexico, UAE, Bali — have no totalization agreement with the US. Portugal is one of the few European-style expat magnets on the agreement list. If SE tax elimination is a priority, Portugal, Germany, Spain, and Australia are structurally better situations than Chiang Mai or Mexico City.

One critical nuance: even with a totalization agreement, you still need to be contributing to the local social security system — not every country's system automatically covers self-employed foreigners. Verify with a local accountant before assuming the exemption applies.

Strategy 1: The S-Corp Election

If you're incorporated as a US LLC, you can elect S-Corporation tax treatment by filing Form 2553. As an S-Corp shareholder-employee, you pay yourself a "reasonable salary" — that salary is subject to payroll taxes. The remaining profits come out as distributions, which are not subject to payroll taxes at all.

Example: You earn $120,000 net. You set your reasonable salary at $55,000. SE tax applies only to the $55,000 salary (~$8,415) rather than the full $120,000 (~$16,940). You save roughly $8,500 in one move. That salary is also potentially excludable under FEIE, further compressing your bill.

The catch: "reasonable salary" is an IRS requirement, not a suggestion. The IRS has challenged S-Corp arrangements where owners paid themselves suspiciously low wages. You need to pay something in line with what someone would earn for similar work. And S-Corp compliance — payroll processing, quarterly deposits, Form 1120-S — costs money. The breakeven point is typically $60,000–$80,000 in net income before the savings justify the overhead.

If you're running a US-based business while living abroad, read our guide to operating a US business from overseas — entity structure decisions here compound quickly.

Strategy 2: Solo 401(k) Contributions

A Solo 401(k) doesn't exempt income from SE tax directly — but it reduces your net self-employment income, which is what SE tax is calculated on. Every dollar in employer contributions reduces your SE tax base dollar for dollar.

In 2025, you can contribute up to $69,000 total to a Solo 401(k) ($23,500 as employee deferral, plus employer contributions up to 25% of net earnings). Contribute $20,000 in employer contributions and your SE tax base drops by $20,000 — saving $3,060 in SE tax.

The major limitation: Solo 401(k) contributions require taxable earned income. If FEIE has excluded 100% of your foreign-earned income, you technically have no taxable earned income remaining to base contributions on. This is one area where earning above the FEIE limit ($130,000+) creates an unexpected advantage — you have taxable income to anchor retirement contributions, and a Solo 401(k) then meaningfully reduces both your income tax and SE tax on that excess.

For freelancers earning under $130,000 who fully exclude all income under FEIE, Solo 401(k) produces limited SE tax savings. Fix the structure first.

Living in a Non-Agreement Country? Do This

If you're in Thailand, Mexico, UAE, or any expat hotspot without a US totalization agreement, and you're not ready to restructure as an S-Corp, here's the pragmatic approach:

Budget for it correctly. Set aside 15.3% of net self-employment income into a separate account every month. Most freelancers who get stung by SE tax were treating their post-FEIE income as take-home pay. Make estimated quarterly payments using Form 1040-ES — the underpayment penalty threshold is 90% of current-year tax or 100% of prior-year tax. Missing quarterly payments adds penalty interest on top of what you already owe.

Maximize deductible business expenses. SE tax applies to net self-employment income. Every legitimate business deduction — home office, equipment, professional subscriptions, business travel, health insurance premiums (100% deductible for self-employed individuals) — reduces your SE tax base dollar for dollar. A $5,000 reduction saves $765 in SE tax.

Maintain your US infrastructure. SE tax payments, estimated taxes, and IRS notices require functional US banking and a real US address. A Mercury business account handles the banking side. For the IRS address, a Traveling Mailbox gives you a real US street address in 50+ cities for $15/month, scans your mail digitally, and ensures you actually receive IRS correspondence — critical when you're living across time zones from your tax authority.

For the complete picture of managing US tax obligations from abroad, our US expat banking and taxes guide covers the full infrastructure stack.

The $130k Ceiling Problem for High Earners

The 2025 FEIE limit is $130,000. If you earn $180,000 as a self-employed expat, $50,000 is exposed to ordinary income tax — at 22–24% — on top of SE tax on the entire $180,000 ($25,439 before adjustment). You're now paying income tax on the excess and SE tax on everything.

At this income level, the S-Corp election stops being optional. A well-structured arrangement at $180,000 saves $12,000–$15,000 annually in SE tax alone — easily justifying $2,000–$3,000 in additional accounting fees. The math is hard to argue with.

High-earning expat freelancers should also consider the investing implications of foreign entity structures. How you hold investments abroad interacts directly with your SE tax and entity planning decisions — our expat investing and PFIC guide covers these intersections.

The Bottom Line

FEIE is one of the most powerful tools in US international tax law — it genuinely eliminates federal income tax on up to $130,000 of foreign-earned income. What it doesn't do is touch self-employment tax, which runs at 15.3% and applies to every dollar of net freelance income regardless of where you live or how you file. A freelancer earning $100,000 abroad with full FEIE exclusion still owes $14,130 to the IRS — and thousands of expats discover this only when the bill arrives.

The fixes are real: live in a totalization agreement country and contribute to local social security, elect S-Corp status and pay yourself a reasonable salary, or build deductible expenses aggressively to reduce net SE income. None of these require leaving the US tax system — just understanding which parts of it actually apply to you.

Plan around the full tax picture, not just the income tax line.

Financial disclaimer: This article is for educational purposes only and does not constitute tax or legal advice. Tax laws change frequently and individual circumstances vary significantly. Consult a qualified CPA or tax attorney with international experience before making decisions about entity elections, retirement contributions, or your overall tax structure. SE tax calculations use 2025 IRS figures and are simplified for illustration purposes.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 29, 2026

Expat Tax & FinanceMay 29, 2026

Self-Employment Tax: The Expat Freelancer’s Hidden Bill

FEIE zeroes your income tax abroad—but SE tax still applies. See the exact numbers and legal ways to reduce your bill as a US expat freelancer.

Expat Tax & FinanceJuly 14, 2026

Expat Tax & FinanceJuly 14, 2026

Expat State Taxes: Which US States Won't Let You Go

Move abroad and California may still tax you 13.3%. Learn which five states chase expats, how domicile works, and how to sever state ties legally.

Expat Tax & FinanceMay 29, 2026

Expat Tax & FinanceMay 29, 2026

Moving Abroad Mid-Year: Maximize Your Tax Benefits

Moving in Q4 instead of Q1 costs you up to $30K in FEIE exclusions. Learn how pro-ration works, state tax traps, and FBAR obligations in year one.