Puerto Rico Act 60: Keep Gains Tax-Free as a US Citizen

Most Americans pay up to 23.8% on capital gains. Puerto Rico Act 60 cuts that to 0%—without renouncing citizenship. Here's what it actually costs and how to qualify.

Puerto Rico Act 60 lets US citizens pay 0% capital gains without renouncing citizenship. Full breakdown of costs, requirements, and IRS audit risks.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

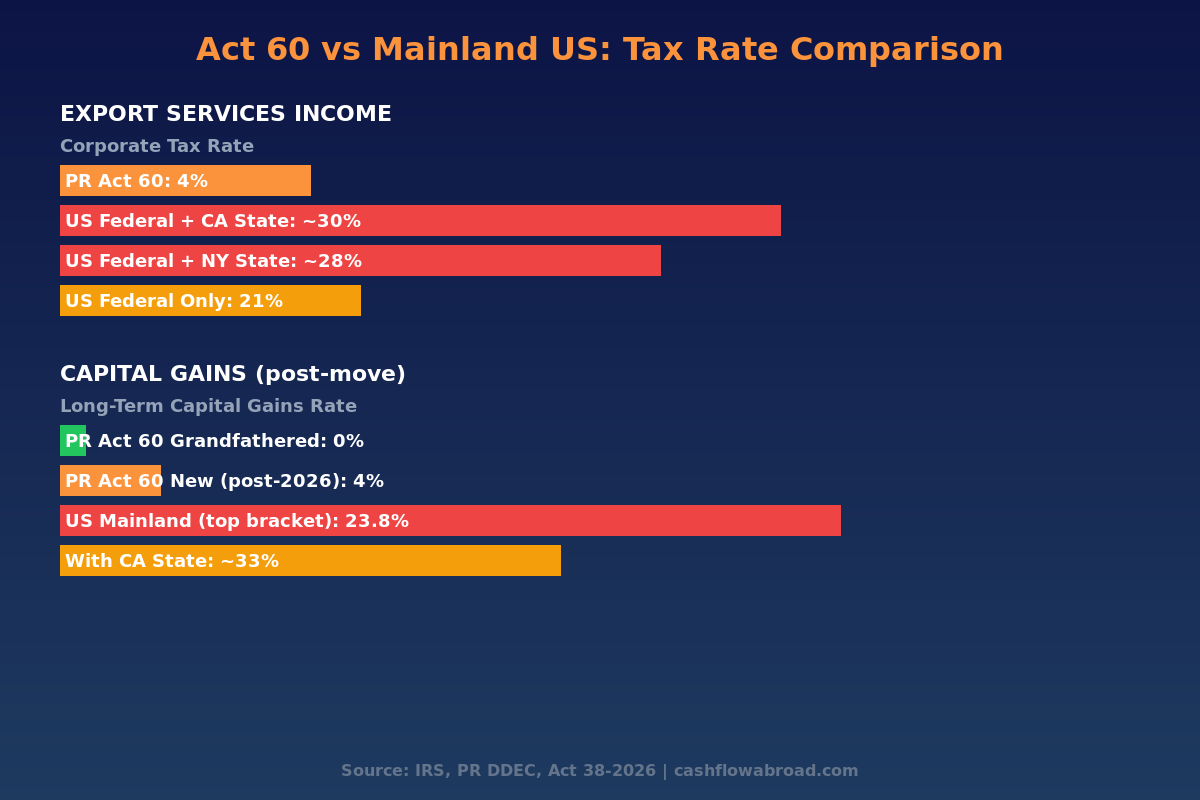

The United States taxes long-term capital gains at up to 23.8% federally — 20% base rate plus a 3.8% Net Investment Income Tax for high earners. Add California's 13.3% state rate and a profitable stock or crypto exit can cost you 37% before you see a dollar. Most people assume that's just the price of doing business as an American.

It doesn't have to be.

Puerto Rico Act 60, Chapter 2 allows bona fide Puerto Rico residents to pay 0% capital gains tax on gains accrued after their residency date. No citizenship renunciation. No offshore trust. No expatriation tax. You keep your US passport, your Social Security eligibility, your ability to live and work freely on the mainland — you just park your tax home 1,035 miles southeast of Miami.

There's a deadline: applications submitted after December 31, 2026 will face a 4% rate instead of 0%. If you're evaluating this strategy, 2026 is the decision year.

What Is Puerto Rico Act 60, Chapter 2?

Puerto Rico is a US territory. Its residents are American citizens, but under IRC § 933, bona fide residents of Puerto Rico are exempt from US federal income tax on Puerto Rico-sourced income. Puerto Rico can legislate its own tax rates on that income — and it does.

Act 60 (enacted 2019, consolidating the original Act 20 and Act 22) is the island's tax incentive code. Chapter 2 targets "Individual Resident Investors" — people who relocate to Puerto Rico and generate investment income: capital gains, dividends, and interest. Under a Chapter 2 decree, qualifying investment income is taxed at 0% by Puerto Rico. Combined with the federal IRC § 933 exemption, total tax on qualifying gains is zero.

The gains must be new — appreciated after the date you established PR residency. Gains that accrued before you moved are still subject to US tax (more on the 10-year lookback rule below).

The Four Tests the IRS Actually Checks

Most people hear "183 days" and stop reading. That's a trap. The IRS applies four conjunctive tests for bona fide Puerto Rico residency, and failing any single one eliminates the exemption.

Test 1: Physical Presence

You must spend at least 183 days per year in Puerto Rico. The IRS counts partial days, passport stamps, credit card records, cell phone pings, and flight data. People who fly to PR for a long weekend 30 times a year get flagged. People who genuinely live there don't.

Test 2: Tax Home

Your principal place of business must be in Puerto Rico. If you run a hedge fund from a New York office, work for a US employer that pays your salary, or maintain a law practice on the mainland — Puerto Rico is not your tax home. Remote founders who can genuinely relocate their operations pass this test. Corporate executives who want to keep their Midtown office don't.

Test 3: Closer Connection

Puerto Rico must be where your life is anchored: your bank accounts, car registration, professional licenses, club memberships, family, and social ties. IRS auditors specifically check voter registration, gym memberships, where your kids go to school, and where your doctors are.

Test 4: Residential Property

You must purchase a home in Puerto Rico within two years of your decree grant. Renting indefinitely while maintaining a house in California doesn't meet this requirement. You need to buy.

The Real Cost Breakdown

Act 60 is not cheap to set up or maintain. The tax savings are enormous at scale, but there's real overhead. Here's what you're actually paying:

| Cost Item | Year 1 | Ongoing/Year |

|---|---|---|

| DDEC application fee | $5,000 | — |

| PR attorney + CPA (decree setup) | $10,000–$25,000 | — |

| Mandatory annual charitable donation | $10,000 | $10,000 |

| Annual compliance (CPA + DDEC reporting) | $5,000–$10,000 | $3,000–$8,000 |

| PR qualifying residential property (rent or buy) | $30,000–$120,000+ | $30,000–$120,000+ |

| Total Year 1 costs (conservative) | ~$60,000–$170,000+ | |

| Non-housing ongoing costs | ~$13,000–$18,000/year | |

The Puerto Rico housing market has appreciated 38–65% since 2020, driven significantly by Act 60 relocatees. Condado beachfront properties run $800–$1,500 per square foot. Dorado luxury estates start at $2 million and go to $15 million and beyond. You don't need to buy at the top tier, but you do need to buy — and PR real estate is no longer inexpensive.

The economic breakeven is approximately $500,000 in expected capital gains over five years, accounting for compliance overhead, housing costs, and audit risk. Below that threshold, FEIE and other strategies are simpler and less expensive. Above $1 million in annual gains, Act 60 deserves serious analysis.

On $2 million in capital gains, the federal tax savings alone exceed $476,000 (at the 23.8% long-term rate). Annual compliance costs of $15,000 look negligible against that figure.

The 2026 Deadline Is Structural, Not Marketing

New legislation extended Act 60 through 2055 — but changed the rate for new applicants. Applications submitted on or after January 1, 2027 receive a 4% Puerto Rico rate on capital gains instead of 0%, locked in through 2055.

Grandfathered applicants — those who file their decree applications by December 31, 2026 — keep the legacy 0% structure through December 31, 2035. That's roughly nine years of zero-rate qualifying gains.

The math: a 2026 application means 0% for nine years. A 2027 application means 4% for 29 years. For an investor with $3 million in positions to exit over that window, the difference is substantial. Grant Thornton's Puerto Rico practice flagged this as the most significant Act 60 structural change in the program's history.

IRS Scrutiny Has Reached a New Level

Act 60 is legal. It's also the most aggressively audited tax strategy in the current IRS enforcement landscape.

A December 2025 Government Accountability Office report found that only about half of Act 60 Individual Investor decree holders filed Form 8898 — the required IRS disclosure for US citizens changing residency to a US territory. That's not a compliance nuance. It signals that a large portion of Act 60 participants haven't been treating the transition with the rigor the IRS requires.

IRS Campaign 685 is the active enforcement initiative targeting Puerto Rico residency claims. Investigators use flight records, credit card transactions, passport stamps, cell tower data, and subpoenas to law firms to reconstruct where taxpayers actually lived. In 2025, the Senate Finance Committee opened an investigation into cryptocurrency investor Dan Morehead for allegedly misrepresenting Puerto Rico residency to avoid more than $100 million in federal taxes.

Three patterns trigger scrutiny most consistently:

- Maintaining a primary home in New York or California while renting in San Juan

- Flying to PR specifically to hit 183 days, then returning to a mainland-based business and social life

- A US-headquartered business or employer that hasn't operationally relocated to Puerto Rico

The IRS is pursuing criminal referrals in flagrant cases. If you're treating Act 60 as a technicality to technically satisfy rather than a genuine relocation, the risk profile is not favorable.

The Crypto Opportunity — and the Trap

Act 60 became famous largely through the crypto community. The rules are specific and unforgiving.

The IRS treats cryptocurrency as property under Revenue Ruling 2019-24, and income sourcing follows IRC § 865.

Crypto purchased after your Puerto Rico residency date: 100% of the gain is Puerto Rico-sourced. Sell under your Act 60 decree → 0% tax. Clean and straightforward.

Crypto purchased before your move: The gain is split. Appreciation that accrued before your residency date is US-sourced — still taxable by the IRS. Appreciation that accrues after your residency date is Puerto Rico-sourced → 0%.

Concrete example: You bought 10 BTC at $30,000 ($300,000 total). You established Puerto Rico residency when BTC was trading at $80,000. By the time you sell, it's at $150,000. The $50,000-per-coin gain from before your move is US-sourced and fully taxable. The $70,000-per-coin gain from after your move is PR-sourced at 0%.

The IRS expects wallet address disclosure, complete transaction histories, and clear proof of acquisition dates. Exchanges like Kraken provide this. If you're managing complex DeFi positions across chains, CoinTracking aggregates your transaction history into IRS-ready reports — essential documentation if your Act 60 decree ever gets audited.

For the broader US expat crypto tax picture, our crypto taxes guide covers FBAR, Form 8938, and how foreign exchanges interact with US reporting.

Pre-Move Gains: The 10-Year Lookback Rule

IRC § 937(b) and Treasury Regulation § 1.937-2 include a rule designed to prevent day-before-liquidity-event games: the 10-year lookback.

If you sell appreciated assets within 10 years of establishing Puerto Rico residency, the pre-residency appreciation is treated as US-sourced income. Still subject to IRS tax. The rule is intentional — it closes the obvious loophole of moving to PR the week before a major exit.

After 10 years as a bona fide PR resident, however, even gains that appreciated before your move become Puerto Rico-sourced, taxed at 5% under Act 60 (not 0%, but dramatically less than 23.8% federal plus state).

The implication is clear: Act 60 rewards long-term commitment. Investors willing to hold existing positions for a decade post-move and exit in Puerto Rico get the best outcome. Investors deploying fresh capital into new positions after establishing PR residency get the clean 0% case immediately.

Act 60 vs. FEIE: Which Strategy Fits

| Factor | Act 60 (Puerto Rico) | FEIE (Living Abroad) |

|---|---|---|

| Capital gains excluded? | Yes — 0% on post-move gains | No — FEIE covers earned income only |

| Earned income excluded? | Partially (PR-source income exempt) | Yes — up to $126,500 (2024) |

| Must leave the US? | No — PR is a US territory | Yes — 330+ days abroad or foreign residence |

| State income tax avoided? | Yes — PR replaces prior state | Depends on prior state domicile |

| IRS audit risk | High (active Campaign 685) | Moderate (330-day test scrutiny) |

| Best income type | Capital gains, dividends, trading | Salary, consulting, freelance |

| Annual compliance cost | $13,000–$18,000+ | $3,000–$6,000 |

The two strategies serve fundamentally different income profiles. Our FEIE guide covers the earned income exclusion in detail. Act 60 is designed for investors whose wealth comes from capital appreciation — not paychecks.

How to Apply: The Process

- Confirm eligibility. You cannot have been a Puerto Rico resident at any point between January 17, 2006 and January 17, 2012. If you were, you're ineligible for Chapter 2.

- Genuinely move to Puerto Rico. Establish 183+ days of physical presence. Not a paper move — an actual one.

- Hire a Puerto Rico-based attorney and CPA with Act 60 specialization. Budget $10,000–$25,000 for the initial engagement.

- File the Act 60 Chapter 2 application with DDEC. Pay the $5,000 filing fee. Receive your signed decree, valid 15 years and renewable for 15 more.

- File Form 8898 with the IRS immediately. This is the required disclosure for US citizens changing possession residency. Roughly 50% of Act 60 holders skip it. Don't be in that group.

- Purchase qualifying Puerto Rico residential property within two years of your decree grant.

- File both Puerto Rico and US tax returns annually. You still file a US Form 1040, but exclude Puerto Rico-source income under IRC § 933.

- Make the annual $10,000 charitable contribution to qualifying PR nonprofits. Half must go to organizations addressing child poverty.

You'll still want a US address for IRS correspondence, brokerage accounts, and financial institution requirements. A virtual mailbox through Traveling Mailbox provides a real US street address in 50+ cities with mail scanning and check deposits — useful while your tax home is Puerto Rico. For brokerage, Charles Schwab International is one of the cleaner setups for investors who move frequently, with free worldwide ATM reimbursement and no foreign transaction fees.

The Verdict

Puerto Rico Act 60 is among the most powerful legal tax reduction tools available to US citizens — and it works precisely because it requires genuinely relocating your life. The IRS will not let you maintain a Manhattan apartment, work from a New York office, and claim Puerto Rico residency based on 184 nights at a San Juan vacation rental. The GAO report, Campaign 685, and the Dan Morehead investigation all confirm that enforcement is real and getting more sophisticated.

But for investors willing to actually relocate — who want to live in a warm, ocean-surrounded US territory while paying 0% on capital gains through 2035 — the economics are compelling. On $5 million in investment gains over the next nine years, the difference between a well-executed Act 60 move and staying on the mainland exceeds $1 million in saved taxes after all compliance costs.

The 2026 deadline for the legacy 0% rate makes this a genuine decision point in 2026. For high-net-worth investors above the $500,000 gains threshold who are open to relocation, the conversation with an Act 60-specialist attorney is worth having before year-end.

For the broader picture of how expat investors structure their financial lives across borders, see our Expat Investing Playbook and Geographic Arbitrage guide.

Financial Disclaimer: This article is for informational and educational purposes only and does not constitute legal, tax, or financial advice. Puerto Rico Act 60 involves significant legal, compliance, and IRS audit considerations that vary based on individual circumstances. Tax laws change frequently. Consult a qualified US tax attorney and CPA with specific Act 60 experience before making any decisions. Nothing in this article should be construed as a recommendation to relocate, restructure investments, or take any specific financial action.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 30, 2026

Expat Tax & FinanceMay 30, 2026

FBAR vs FATCA: What Every Expat Must Know

FBAR and FATCA are two separate foreign account reporting requirements with different penalties and thresholds. Learn what every US expat must file.

Expat Tax & FinanceMay 6, 2026

Expat Tax & FinanceMay 6, 2026

Capital Gains Tax: The FEIE Blind Spot Expats Pay For

The FEIE shields your salary but not your stock gains. Learn how NIIT, the stacking rule, and Section 865(g) affect US expat capital gains taxes.

Expat Tax & FinanceMay 5, 2026

Expat Tax & FinanceMay 5, 2026

Australian Super & US Taxes: The Trap Nobody Warns You About

The US-Australia treaty gap exposes your super to annual IRS taxation and 0,000/yr penalties. What every US expat in Australia must know.