Capital Gains Tax: The FEIE Blind Spot Expats Pay For

The FEIE excludes your salary from US taxes—but does nothing for capital gains. Worse, the stacking effect can push your gains into a higher bracket.

The FEIE shields your salary but not your stock gains. Learn how NIIT, the stacking rule, and Section 865(g) affect US expat capital gains taxes.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Most US expats spend weeks hunting down the right tax software, filing an FEIE claim, and congratulating themselves on legally excluding $130,000 of foreign earnings from US taxation. Then they sell $80,000 of Apple stock and get a tax bill they weren't expecting. The Foreign Earned Income Exclusion is one of the most powerful tools in expat tax law — and one of the most misunderstood. It excludes earned income. Period. Capital gains, dividends, interest, and rental income are invisible to it. If you hold a US brokerage account and haven't accounted for this, you're walking into a trap that costs expats billions of dollars collectively every filing season.

What the FEIE Actually Covers (And Doesn't)

The Foreign Earned Income Exclusion (Form 2555) lets qualifying US citizens and green card holders exclude up to $130,000 of foreign earned income in 2025 (rising to $132,900 in 2026) from US federal income tax. This is real money. For a remote worker earning $130K living in Lisbon, it often means a federal tax bill of approximately zero on their paycheck.

But the IRS defines "foreign earned income" with surgical precision. Earned income means wages, salaries, professional fees, and net self-employment income — money you received in exchange for personal services performed in a foreign country. That's it. The exclusion does not apply to:

- Capital gains from selling stocks, ETFs, or mutual funds

- Dividends from US or foreign companies

- Interest income from savings, bonds, or CDs

- Rental income from property you own

- Royalties and licensing fees

- Pension and retirement distributions

This is codified in IRC Section 911 and confirmed repeatedly in IRS guidance. Your investment portfolio generates unearned income under the tax code. FEIE does not touch it.

If you've been assuming your portfolio gains are shielded because you live abroad — they're not. The IRS wants their cut regardless of which time zone you're filing from.

The Stacking Effect: FEIE Can Actually Raise Your Capital Gains Tax

Here's where it gets counterintuitive. The FEIE doesn't just fail to protect your capital gains — it can actively increase the rate at which those gains are taxed.

When you claim the FEIE, the IRS calculates tax on your remaining income as though the excluded amount still occupies the bottom of your income stack. This is the "stacking rule" under the regulations, and it means your capital gains get pushed into higher brackets than they would be otherwise.

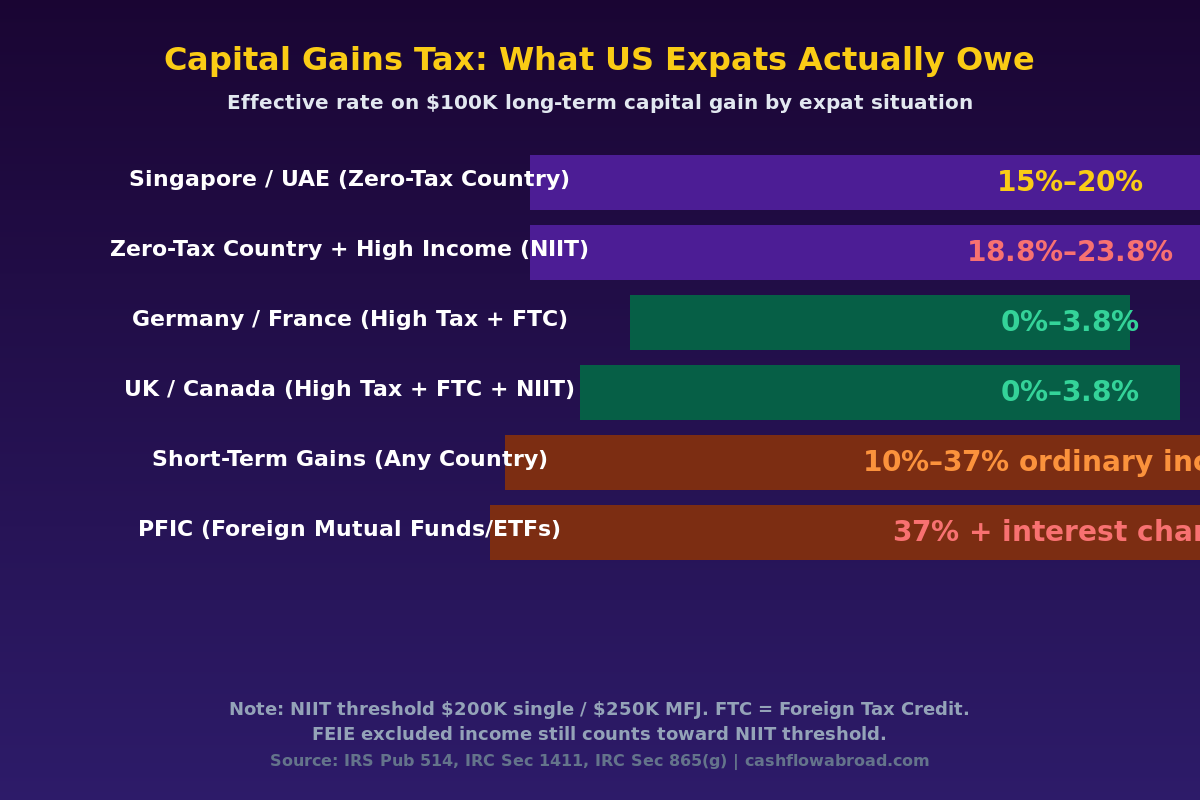

Consider this example: A US expat living in Singapore earns $180,000 in wages and excludes $130,000 under FEIE. She also sells stock for a $60,000 long-term capital gain. Without FEIE, her taxable income is $50,000 in wages plus $60,000 in gains — much of those gains might be taxed at 0% or 15%. With FEIE, the IRS treats her as if she earned $130,000 before the remaining $50,000 — so her capital gains sit on top of a $180,000 stack. Every dollar of those gains gets taxed at 20%, not 0%.

The 2025 long-term capital gains brackets for a single filer look like this:

| Rate | Single Filer Taxable Income | Married Filing Jointly |

|---|---|---|

| 0% | Up to $48,350 | Up to $96,700 |

| 15% | $48,351 – $533,400 | $96,701 – $600,050 |

| 20% | Over $533,400 | Over $600,050 |

Because the stacking rule fills the lower brackets with your excluded income first, even a moderate-earning expat can end up with capital gains taxed at 15% or 20% when — without the FEIE — those same gains would have been taxed at 0%. Short-term capital gains (assets held under 12 months) are taxed as ordinary income at rates from 10% to 37%, with no preferential rate and no FEIE protection.

NIIT: The 3.8% Nobody Warned You About

On top of standard capital gains rates sits the Net Investment Income Tax — a 3.8% surtax on investment income that very few expats plan for. Enacted in 2013 under the Affordable Care Act (IRC Section 1411), NIIT applies to single filers with Modified Adjusted Gross Income above $200,000, or married filers above $250,000.

Combined with the 20% long-term rate, the maximum federal tax rate on capital gains for high-earning expats is 23.8%.

Here's the trap that catches even sophisticated expats: the FEIE exclusion does NOT reduce your MAGI for NIIT purposes. The IRS explicitly excludes the FEIE from modifying MAGI in the NIIT calculation. So if you earn $150,000 abroad and exclude $130,000, your MAGI is still $150,000 — not $20,000. Add $80,000 in capital gains and your MAGI hits $230,000 — above the $200,000 threshold. NIIT fires on the lesser of net investment income ($80,000) or the excess over the threshold ($30,000), meaning you owe $30,000 × 3.8% = $1,140 in NIIT with no credit available to offset it.

There's another critical point: the Foreign Tax Credit cannot offset NIIT. Even if you paid capital gains taxes to Germany, the UK, or France, those foreign tax credits apply against your regular US capital gains tax — not the 3.8% surtax. The IRS confirmed this in regulations under Section 1411. NIIT is a separate tax with no foreign offset mechanism whatsoever.

For a comprehensive breakdown of the Foreign Tax Credit vs. FEIE tradeoffs, see our FEIE vs. Foreign Tax Credit guide.

Where the Foreign Tax Credit Actually Helps (and Where It Doesn't)

The Foreign Tax Credit (Form 1116) is the other major tool in the expat tax arsenal — and for investment income, it's often more powerful than the FEIE. The FTC allows a dollar-for-dollar reduction of your US tax bill for income taxes paid to a foreign country on the same income.

For capital gains, this falls in the "passive income basket." Whether the FTC applies depends on where the gains are sourced.

Section 865(g): The Critical Re-Sourcing Rule

Under US tax law, capital gains on securities are sourced to your country of residence. This seems straightforward — if you live in Germany and sell Apple stock, the gain is German-sourced, and German capital gains tax (Abgeltungsteuer at roughly 26.4% including the solidarity surcharge) should be creditable against US tax on those same gains.

Section 865(g) codifies this re-sourcing rule, but with a condition: foreign-source treatment only applies when your country of residence imposes a tax of at least 10% on the gain. For high-tax countries, this works in your favor. For zero-tax jurisdictions, there's no foreign tax to meet the threshold — and no FTC to apply.

| Country | Local Capital Gains Tax | FTC Available? | US Tax on $100K Gain (approx.) |

|---|---|---|---|

| Germany | ~26.4% (incl. surcharge) | Yes — Sec. 865(g) applies | ~$0 federal (FTC offsets fully) |

| France | 30% flat (PFU tax) | Yes | ~$0 federal |

| United Kingdom | 10%–20% on non-property assets | Yes | ~$0–$5,000 federal |

| Singapore | 0% | No (nothing to credit) | $15,000–$20,000 federal |

| UAE / Dubai | 0% | No | $15,000–$20,000 federal |

| Panama | 0% on foreign-source gains | No | $15,000–$20,000 federal |

The implication is counterintuitive: expats in high-tax countries often pay less total US capital gains tax than expats in tax havens. An expat in Dubai who sells $100,000 in stock gains owes roughly $15,000–$20,000 to the IRS with no offset. An expat in Germany who sells the same position may owe nothing to the IRS — though they paid $26,400 to Germany. Both paid roughly the same total tax; the German expat just paid it to a different government.

Excess FTC credits in the passive basket can carry forward up to 10 years or back 1 year to offset future US taxes on dividends, interest, and additional capital gains. This makes tracking FTC carryforwards a meaningful optimization for expats with large investment portfolios.

See our PFIC and expat investing guide for a deeper breakdown of which investment structures work and which blow up on you.

The PFIC Trap: Foreign Mutual Funds Are a Tax Nightmare

If you've opened a local investment account abroad and bought into the country's equivalent of an index fund, you've very likely stumbled into a Passive Foreign Investment Company. Non-US mutual funds, ETFs, and unit trusts are almost universally classified as PFICs under IRC Sections 1291–1298.

The PFIC tax regime is deliberately punitive. Gains from PFIC shares are not eligible for long-term capital gains rates. Instead, they're taxed at the highest ordinary income rate (37% in 2025), plus an interest charge calculated as if you had owed the tax each year the gain accrued. The effective combined rate can exceed 50%.

The correct approach for global diversification: buy US-listed ETFs that hold international stocks (VT, VXUS, EFA) rather than owning foreign-domiciled funds directly. If you already own foreign ETFs, correcting this requires a mark-to-market election (Form 8621), a Qualified Electing Fund election if the fund supports it, or selling — and accepting the PFIC tax hit to start fresh.

Charles Schwab International actively supports US citizen expats, keeps accounts open for non-residents, and gives you access to the full range of US-listed ETFs and securities — plus free ATM withdrawals worldwide through their checking account. tastytrade is another expat-friendly platform focused on options and active trading.

Two More Hidden Traps Expats Miss

Currency Gains Are Taxable

Every gain or loss must be calculated in US dollars. This creates phantom gains when foreign currencies strengthen. If you bought a German stock for €10,000 when the euro was $1.10 (cost basis: $11,000) and sold for €10,000 when the euro reached $1.20 (proceeds: $12,000), you have a $1,000 taxable gain — even though the stock price in euros didn't budge. Report it on Form 8949 like any other capital transaction.

The same applies to foreign bank accounts. Holding euros or pounds that appreciate against the dollar generates taxable income when you convert. Many expats overlook this entirely.

State Capital Gains Taxes Don't Accept Foreign Credits

The Foreign Tax Credit is a federal mechanism. Most US states offer no equivalent credit for taxes paid to foreign governments. If you maintain legal domicile in California (capital gains taxed as ordinary income at up to 13.3%) or New York (up to 10.9%), the taxes you paid to Germany or Portugal don't reduce a single dollar of state liability.

Expats living in zero-tax countries with California domicile face the worst of all worlds: full federal capital gains tax (no FTC offset), plus full California state tax, with nothing to show for it in credits. This is why domicile strategy matters enormously. Our guide on state taxes for expats covers which states let you go cleanly and which follow you around the world.

Six Strategies to Reduce Capital Gains Tax as an Expat

1. Use FTC Instead of FEIE If You Have Significant Investment Income

If you live in a country with meaningful capital gains taxes and hold a substantial portfolio, the Foreign Tax Credit often beats the FEIE on total tax liability. FTC users avoid the stacking effect entirely — capital gains sit at the bottom of the income stack, potentially reaching the 0% bracket. And foreign taxes paid on gains can directly offset the US tax on those same gains under Section 865(g). Model both options with a qualified expat CPA before your return is filed.

2. Time Large Sales for Low-Income Years

Freelancers, consultants, or anyone with variable income can harvest gains in years when total taxable income (modeled without the FEIE stacking distortion) stays below the 0% capital gains threshold — $48,350 for single filers, $96,700 for married couples in 2025. A $40,000 gain realized in a lean year can cost exactly zero dollars in federal capital gains tax.

3. Tax-Loss Harvest Aggressively

Losses offset gains dollar-for-dollar, with up to $3,000 annually applying against ordinary income. Unused losses carry forward indefinitely. Note: as of 2025, crypto is now subject to wash-sale rules — you must wait 31 days before rebuying any sold crypto position to preserve the loss deduction. CoinTracking handles cost basis tracking across exchanges and generates the IRS-required reports; Kraken is one of the few major exchanges that still operates for US citizens living abroad.

4. Invest Through Qualified Opportunity Zones

Capital gains proceeds reinvested in a Qualified Opportunity Fund within 180 days of the triggering sale can be deferred — and if the QOF investment is held for 10+ years, all appreciation inside the fund is permanently excluded from federal tax. The program was made permanent in 2025, with enhanced step-ups for rural opportunity zones. Best suited for large capital events: business sales, concentrated stock positions, or property disposals.

5. Maximize Roth Contributions

Capital gains inside a Roth IRA grow and distribute tax-free, permanently. FTC users who retain earned income on their return typically preserve Roth contribution eligibility. Even when direct contributions aren't available (due to income limits or FEIE wiping out earned income), the backdoor Roth conversion is usually still available. Every dollar of growth shifted into a Roth is one less dollar subject to future capital gains tax.

6. Track and Deploy FTC Carryforwards

When foreign taxes paid on capital gains exceed your US liability in a given year, you generate carryforward credits in the passive basket. These credits offset future US taxes on dividends, interest, and additional capital gains for up to 10 years. Letting these expire unused is leaving money on the table. A proper FTC tracking spreadsheet — or a CPA who maintains one — pays for itself many times over for any expat with substantial investment income.

Set Up Your Infrastructure First

None of this works if your brokerage account gets closed because you updated your foreign address. Many major US brokers — Fidelity, Vanguard, E*TRADE — have restricted or closed accounts for expats with foreign addresses. Charles Schwab International is the most reliable option for US citizens abroad, with explicit support for expat clients and global ATM access through their checking account.

You'll also need a real US mailing address. The IRS, brokerages, and most financial institutions require one. A virtual mailbox through Traveling Mailbox ($15/month) gives you a real US street address in 50+ cities with mail scanning, check deposit, and forwarding. It's the infrastructure that keeps everything else working. Our virtual mailbox guide walks through the setup in detail.

For a complete look at managing US retirement accounts from abroad, see our expat 401k and IRA guide and our crypto taxes guide for US expats.

The Bottom Line

The FEIE is one of the most powerful tax breaks in the US code for citizens living abroad — but it operates in a specific lane. The moment your wealth starts generating capital gains, dividends, or interest, you're back in full US taxation territory. And because of the stacking effect and the non-creditable NIIT, many expats find their investment income taxed at higher effective rates than it would be for a stateside investor.

The solution is planning: understand which elections optimize your specific income mix, avoid PFIC traps by holding US-listed funds, time large sales around your income levels, and maintain the right financial infrastructure to keep accounts open and address compliant. Expats who treat capital gains as an afterthought will eventually pay for that assumption. Those who plan around it come out consistently ahead.

Financial disclaimer: This post is for informational and educational purposes only and does not constitute tax or financial advice. Tax rules for US expats are complex and subject to change. Consult a qualified international tax professional — ideally a CPA specializing in expat taxation — before making decisions about your filing strategy, FEIE vs. FTC election, or investment structure. Individual circumstances including residency status, income composition, treaty country, and state domicile significantly affect outcomes.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageJune 21, 2026

Geographic ArbitrageJune 21, 2026

Hong Kong for US Expats: Tax and Visa Guide

US citizens living in Hong Kong pay 15% salaries tax with no US-HK treaty. Learn FEIE vs FTC, Top Talent Pass visas, FBAR rules, and monthly costs.

Expat Tax & FinanceMay 29, 2026

Expat Tax & FinanceMay 29, 2026

Moving Abroad Mid-Year: Maximize Your Tax Benefits

Moving in Q4 instead of Q1 costs you up to $30K in FEIE exclusions. Learn how pro-ration works, state tax traps, and FBAR obligations in year one.

Expat Tax & FinanceMay 16, 2026

Expat Tax & FinanceMay 16, 2026

The FEIE-Roth IRA Trap Costing Expats $500K at Retirement

The FEIE excludes income from U.S. tax — but blocks Roth IRA contributions. Learn the 5-year trap and preserve retirement savings abroad.