Australian Super & US Taxes: The Trap Nobody Warns You About

Australian superannuation has a treaty gap that exposes US expats to 0,000/year IRS penalties on money they cannot touch. Here is what you need to know.

The US-Australia treaty gap exposes your super to annual IRS taxation and 0,000/yr penalties. What every US expat in Australia must know.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

You move to Australia for work. Your employer deposits 12% of your salary into a superannuation fund every payday. You ignore it — that money is locked up until you're 60, and you're focused on the next few years abroad. Then, five years later, your US tax attorney drops a bill that makes your coffee go cold: you owe $50,000 in back taxes, interest, and automatic IRS penalties — on money you've never touched, in an account you couldn't access if you tried.

This isn't a hypothetical. It's the scenario playing out for thousands of American expats in Australia who made the same reasonable assumption: that Australian superannuation works like a 401(k). It does not. The US-Australia tax treaty contains a specific gap that leaves super contributions and growth fully exposed to US taxation — and the penalty structure for non-compliance is brutal enough to turn a well-funded retirement account into a liability.

How Australian Super Works (If You're Not American)

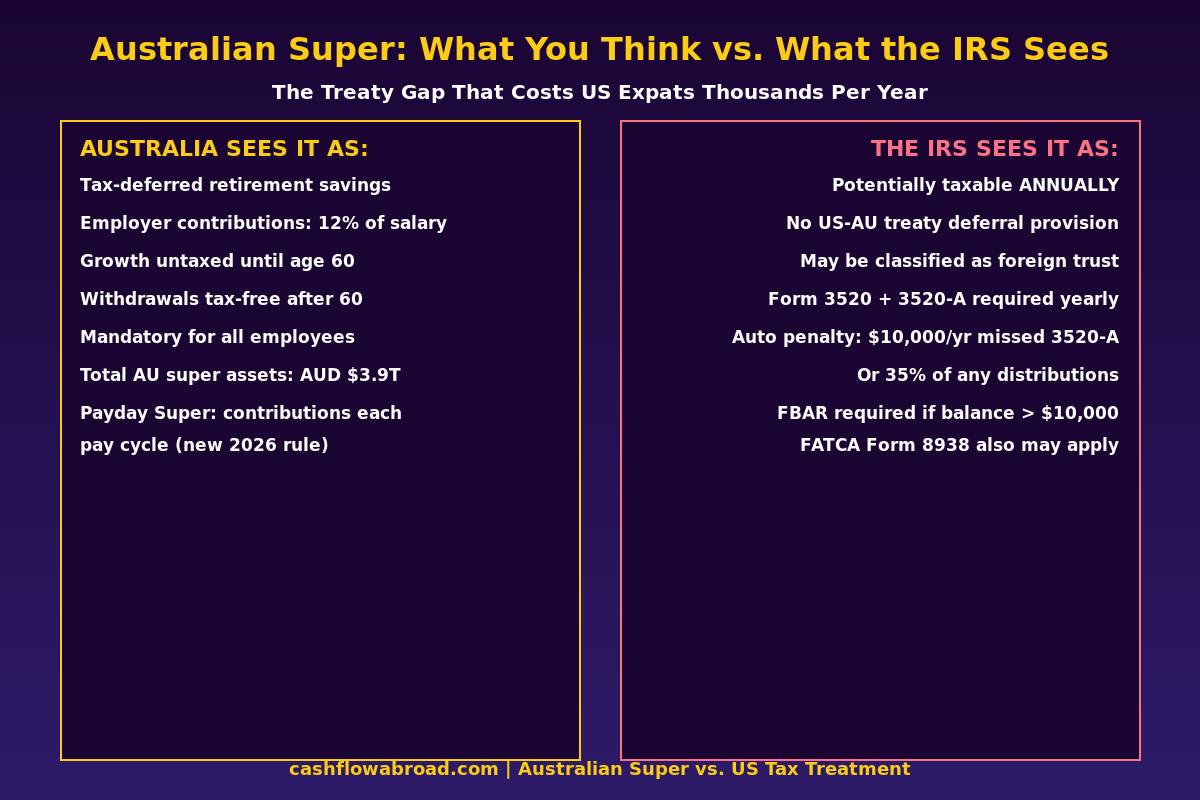

For every Australian — and most expats working legally in the country — superannuation is mandatory. Under the Superannuation Guarantee, employers must contribute a minimum of 12% of ordinary time earnings into a super fund starting from the 2025–2026 financial year. That rate has been climbing: it was 10.5% in 2022–2023, and it hit the legislated ceiling of 12% in July 2025.

From Australia's perspective, super is essentially untouchable retirement savings:

- Growth inside the fund is taxed at just 15% within the fund — far below personal income tax rates.

- You can't withdraw until you reach your preservation age (generally 60) and retire.

- Once you hit 60 and meet a "condition of release," withdrawals are typically tax-free.

Starting in 2026, Australia's new Payday Super rules kicked in. Employers must now deposit super contributions on each payday — not quarterly as they historically could. The Australian Tax Office now has real-time visibility into contribution streams. For US expats, this means the compliance clock ticks faster than ever.

In total, Australia's superannuation system holds over AUD $3.9 trillion in assets. Tens of thousands of American citizens and green card holders have accounts in that pool. Many of them are filing their US taxes wrong — or not at all — for those accounts.

The Treaty Gap That Breaks Everything

Here's the core problem. The US has tax treaties with most major countries, and those treaties typically include provisions that allow pension and retirement account growth to be deferred — matching the home country's treatment. The US-Canada treaty covers RRSPs explicitly via Form 8833 election. The US-UK treaty covers UK pensions and SIPPs.

The US-Australia tax treaty, signed in 2001, has no comprehensive pension deferral provision for Australian superannuation.

Without that treaty protection, US persons with super funds are left with IRS default rules, which treat the fund as a foreign trust. The IRS's position — articulated in multiple private letter rulings and professional guidance — is that the growth inside an Australian super fund may be taxable to the US beneficiary annually, even though the money is locked up and the Australian government doesn't consider it taxable at all.

This is the phantom income problem. You're being taxed on growth in an account you cannot legally access. The tax is calculated on your US return, payable in US dollars, regardless of what's happening inside the fund.

The Reporting Requirements: Where the Real Damage Happens

Even if the tax liability on fund growth ends up being manageable (some practitioners argue the "accumulation phase" taxation is ambiguous enough to warrant a conservative reporting position), the reporting requirements are not ambiguous — and the penalties for missing them are automatic.

Form 3520 and Form 3520-A

If the IRS classifies your super fund as a foreign grantor trust — the dominant view among tax professionals — you're required to file:

- Form 3520: Annual return to report transactions with foreign trusts. Due with your tax return (April 15, or June 15 if abroad).

- Form 3520-A: Annual information return of the foreign trust itself. Due March 15 — earlier than your main return.

The penalty for a late or missing Form 3520-A is automatic: the greater of $10,000 or 5% of the gross value of the trust assets for each year. On a $200,000 super fund, that's $10,000 per year — whether you knew about the requirement or not. Miss five years and you're looking at $50,000 in penalties before the IRS has assessed a single dollar of actual tax.

Distributions from super — whether received as a US resident or as an expat — can trigger an additional penalty of 35% of the distribution amount if not reported correctly on Form 3520.

FBAR and FATCA

Australian super funds are almost certainly foreign financial accounts for FBAR purposes. If the total value of your foreign financial accounts — super plus anything else — exceeds $10,000 at any point during the calendar year, you must file FinCEN 114 (the FBAR) by April 15 (auto-extended to October 15).

Separately, if you're abroad and your super fund plus other foreign assets exceeds $200,000 at year-end or $300,000 at any point (single filer), or $400,000/$600,000 for married filing jointly, you also need to report on Form 8938 (FATCA reporting). Filing both Form 8938 and FBAR is required — they're not duplicates in the IRS's eyes.

FBAR penalties for non-willful violations run up to $10,000 per year per account. Willful violations: the greater of $100,000 or 50% of the account balance. For reference, if your super fund held $300,000 and the IRS determines willful non-filing over three years, the theoretical penalty exposure is $450,000 — 150% of the account value.

How the Penalty Math Stacks Up

| Violation | Penalty (Non-Willful) | Penalty (Willful) |

|---|---|---|

| Missing Form 3520-A (per year) | $10,000 or 5% of fund value | 35% of distribution + $10,000 |

| Missing FBAR (per account, per year) | Up to $10,000 | Greater of $100,000 or 50% of account |

| Missing Form 8938 (per year) | $10,000 to $50,000 | $10,000 to $50,000 + accuracy penalties |

| Unreported super fund income (growth) | 20% accuracy penalty + interest | 75% civil fraud penalty + interest |

These penalties compound. A US citizen who worked in Sydney for five years, accumulated $180,000 in super, and never filed any of the required forms faces — theoretically — well over six figures in penalties before the IRS considers a dollar of underlying tax. The penalties often exceed the tax itself.

Self-Managed Super Funds: An Even Bigger Trap

Some high-earning expats or long-term residents hold a Self-Managed Super Fund (SMSF), which gives them direct control over fund investments. From a US tax perspective, SMSFs are almost universally classified as foreign grantor trusts — the same reporting burden as regular industry funds, but with significantly more complexity because the US person directly controls investment decisions.

If you're a US citizen and the trustee of an SMSF, expect to file both Forms 3520 and 3520-A every year, reporting the trust's assets, income, and distributions in detail. US-based tax attorneys specializing in Australian cross-border matters typically charge $3,000–$8,000 per year for SMSF compliance alone — before any underlying tax is paid. If you don't already have an SMSF, this is not the structure to set up while holding US citizenship.

How Other Countries' Pensions Compare

| Country | Pension Plan | US Treaty Deferral? | Trust Forms Required? | Employer Contribution Rate |

|---|---|---|---|---|

| Australia | Superannuation | No — treaty gap | Yes (3520/3520-A) | 12% of salary |

| Canada | RRSP | Yes — Form 8833 election | Typically no | Voluntary (employer varies) |

| United Kingdom | SIPP / Workplace Pension | Yes — qualifying plans covered | Often yes if SIPP | Min 3% employer, 5% employee |

| Germany | Gesetzliche Rentenversicherung | Partial | Generally no (statutory scheme) | 9.3% employer |

| Netherlands | Pensioen (pillar 2) | Partial treaty coverage | Generally no | Varies by sector |

Canada solved its pension deferral problem via explicit treaty language updated in 1984. The UK's 2001 treaty with the US included pension provisions. Australia's 2001 treaty simply didn't address superannuation — and renegotiating bilateral tax treaties requires years of government-to-government diplomacy. There is no fix on the near-term horizon.

What You Can Actually Do

If You're Currently Non-Compliant

If you've been in Australia and haven't been filing Forms 3520/3520-A, you have options. The IRS's Streamlined Foreign Offshore Procedures allow non-willful non-filers to catch up with dramatically reduced penalties. The program requires:

- Filing 3 years of amended or delinquent tax returns

- Filing 6 years of FBARs for all unreported foreign accounts

- Paying any back tax owed plus interest

- Certifying non-willfulness — that you genuinely didn't know about the requirement

Under Streamlined Offshore, FBAR and Form 3520 penalties are waived if the certification is accepted. The critical word is "non-willful." Once you know about the requirement and don't file, you've crossed into willful territory. If you're reading this article, the clock has started on your knowledge cutoff.

Engage a CPA or tax attorney with specific Australian-US cross-border experience before filing any amended returns. Firms like Greenback Tax Services, Bright!Tax, and Golding & Golding all have super-specific expertise. The compliance cost is real, but far cheaper than willful penalty exposure.

If You're Currently Working in Australia

You cannot opt out of super contributions for employed workers — they are legally mandatory. But you can:

- Choose a simple fund type. Industry funds (like AustralianSuper or Hostplus) and retail funds are far easier to report than SMSFs. If you don't already have an SMSF, don't establish one while you're a US person.

- File correctly from year one. Once you know about the requirement, Forms 3520 and 3520-A must be filed annually. The compliance cost ($1,000–$3,000/year for a straightforward industry fund) is real but a fraction of the penalty exposure for non-filing.

- Think about the post-Australia situation. When you return to the US, your super account becomes a foreign account you'll continue reporting on until you take distributions after age 60. Some expats explore rolling funds into other structures before leaving Australia; your options are limited by preservation rules, but worth discussing with a dual-qualified advisor.

- Track your Foreign Tax Credit. The 15% tax paid inside the fund on investment income may partially offset US liability via the Foreign Tax Credit, depending on how the income is characterized. This doesn't work automatically — it requires proper structuring on your return.

Banking and Money Transfers

While managing Australian super compliance, US expats in Australia also need reliable ways to move money across the Pacific. For international transfers from Australia to US accounts, Remitly consistently offers competitive rates with transparent fees — far better than bank wire rates. For maintaining a US banking presence — critical for IRS correspondence and keeping stateside accounts active — Mercury works well for US LLCs and business accounts, while Charles Schwab International covers personal banking and brokerage with fee-free ATM withdrawals globally.

If you're in Australia long-term, a Traveling Mailbox virtual US address (~$15/month) keeps your IRS mailing address current, maintains your state domicile claim, and ensures you receive IRS notices promptly — which you don't want sitting unread in a forwarding queue. See our virtual mailbox guide for the full setup walkthrough.

Health Coverage While in Australia

Medicare in Australia covers residents — but as a US citizen on a temporary visa, your coverage depends on whether you hold a Medicare card under the Reciprocal Health Care Agreement. That agreement is limited; it covers medically necessary care but not everything. If you're on a subclass 482 or similar work visa long-term, supplemental international health insurance fills the gaps. SafetyWing's Nomad Insurance starts at $56/month for US expats under 40 and works globally — including Australia. For a detailed comparison of coverage options, see our expat health insurance guide.

The Broader Pattern: Foreign Investment Traps

Australian super is one instance of a consistent IRS pattern: foreign investment vehicles receive harsher treatment than their US equivalents, often without treaty protections to equalize the burden. Foreign ETFs and mutual funds face the PFIC rules — passive foreign investment company rules that can result in top ordinary income rates plus punitive interest on fund gains. Foreign pension plans, as we've seen, trigger trust reporting with automatic penalties. The IRS presumes foreign = worse until a specific treaty says otherwise.

The practical upshot: don't wait for something to go wrong before getting compliant. The Australian Tax Office shares financial data with the IRS under FATCA intergovernmental agreements and the Common Reporting Standard. Your super fund balance is not invisible — it's just invisible to Americans who assume no news means no problem.

Bottom Line

Australian superannuation is one of the most generous mandatory retirement systems in the world — and one of the most dangerous tax traps for US citizens living abroad. The combination of no treaty deferral, automatic $10,000/year penalties, and phantom income taxation on locked-up funds creates a compliance burden that catches even financially sophisticated expats off guard.

The good news: if you're non-compliant and it was genuinely non-willful, the Streamlined Offshore Procedures offer a real exit ramp. But that window narrows the longer you wait — and the new 2026 Payday Super rules mean the ATO's real-time data sharing with the IRS just got more current.

Get a dual-qualified US-Australian tax professional involved before your first Australian tax return. The cost of proactive compliance is measured in hundreds to low thousands per year. The cost of ignoring it is measured in multiples of your account balance.

Disclaimer: This article is for educational purposes only and does not constitute legal, tax, or financial advice. Tax laws, treaty interpretations, and IRS guidance change frequently. Consult a qualified US-Australian cross-border tax professional before making decisions about superannuation compliance, Form 3520 obligations, or international investment strategy. Penalty figures and thresholds cited reflect IRS published guidance and professional commentary as of the publication date.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 30, 2026

Expat Tax & FinanceMay 30, 2026

FBAR vs FATCA: What Every Expat Must Know

FBAR and FATCA are two separate foreign account reporting requirements with different penalties and thresholds. Learn what every US expat must file.

Expat Tax & FinanceJune 23, 2026

Expat Tax & FinanceJune 23, 2026

FBAR vs Form 8938: Expat Reporting Guide

US expats with foreign accounts over $10,000 must file FBAR. Learn how Form 8938 differs, current penalty amounts, and how to catch up.

Expat Tax & FinanceJune 13, 2026

Expat Tax & FinanceJune 13, 2026

WEP and GPO Repealed: Expats With Foreign Pensions Win

WEP and GPO ended in January 2025, giving expats with foreign pensions their full SS benefits. Average retroactive payout: $6,710. Here is the tax