Peru for US Expats: Taxes, Visas & the $1,200/Month Life

10 min read · 2,415 words

There are roughly 9 million Americans living abroad. Fewer than 80,000 of them live in Peru — which is exactly why you should pay attention. While everyone else chases the same Lisbon apartment or Medellín loft, Peru sits there with a $1,200/month comfortable lifestyle, a fast-track residency visa that costs almost nothing to qualify for, and a tax situation that’s genuinely workable for US expats who structure it right.

The country is the world’s second-largest silver producer, home to one of the fastest-growing middle classes in South America, and has clocked average GDP growth above 4% annually for the past decade. Lima’s Miraflores district is genuinely world-class — walkable oceanfront promenade, Michelin-recognized restaurants, and fiber internet in apartments that rent for a third of what you’d pay in Miami. That’s geographic arbitrage at scale.

Here’s everything you need to know to actually move there.

Why Peru Is Being Slept On

The expat conversation always gravitates toward the same short list: Portugal, Mexico, Colombia, Thailand. Peru doesn’t make that list often, and the gap between reputation and reality is stark.

Lima is a city of 11 million with a food scene that routinely places multiple restaurants in the World’s 50 Best rankings (Central has held a top-5 spot). It has direct flights to Miami in under 6 hours, a currency that holds value better than most of its neighbors, and neighborhoods that feel legitimately safe and walkable. Cusco offers a completely different tempo — Andean altitude, colonial architecture, an ever-present international crowd, and monthly rents under $600 for a furnished apartment.

Peru’s economy is also effectively dollarized in practice. Bank accounts can be denominated in USD, prices in tourist and expat areas are often quoted in dollars, and the sol (PEN) has been remarkably stable compared to, say, the Argentine peso or Colombian peso. Your purchasing power doesn’t get eroded by surprise devaluations.

The counterintuitive part: Lima is cheaper than Medellín for equivalent quality of life, yet gets far less attention from the geographic arbitrage crowd. That gap is closing — but it hasn’t closed yet.

Visa Options for US Citizens

US citizens can enter Peru without a visa and stay for up to 183 days per 12-month period on a tourist stamp. No advance application, no appointment, no fee — just a valid US passport. For longer stays or actual residency, Peru has three primary routes.

Rentista Visa — The Sweet Spot

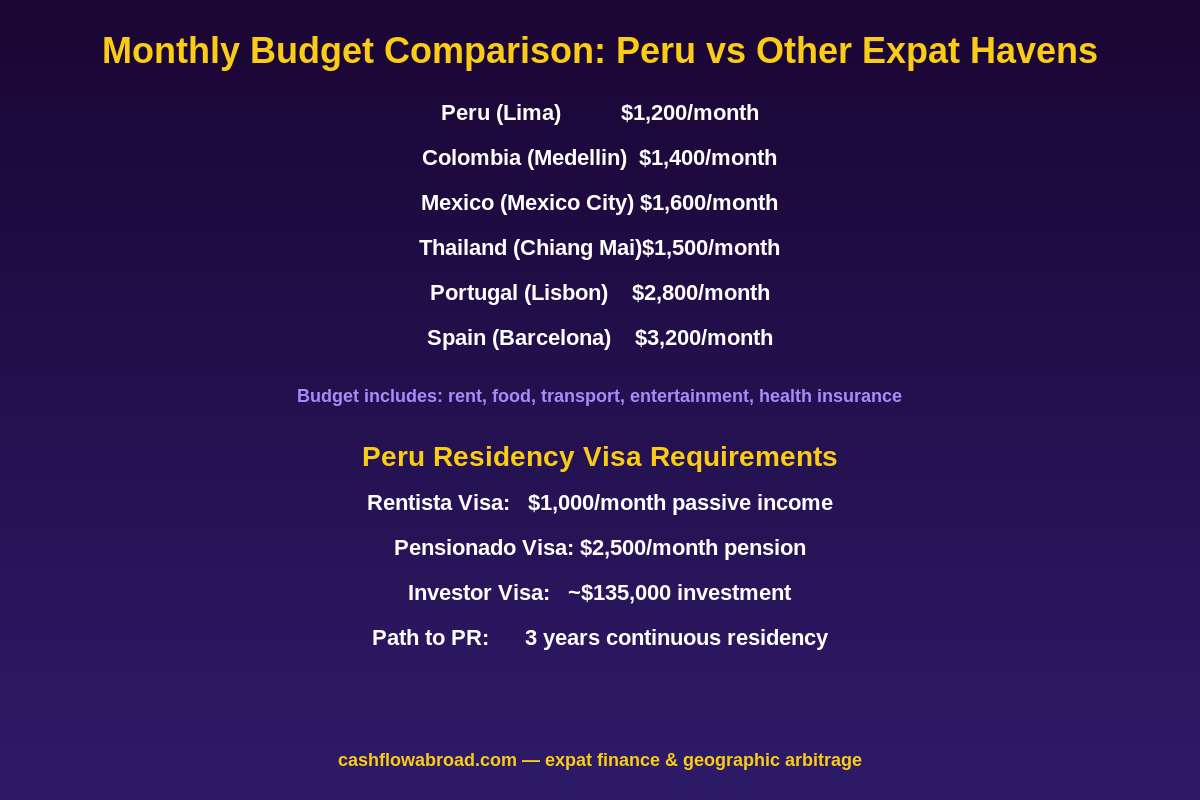

The Rentista visa is the path most expats take. It requires just $1,000/month in passive income — pension, dividends, rental income, royalties, annuities — with an additional $500/month per dependent. That’s an extraordinarily low bar compared to most countries’ passive income residency programs (Portugal’s D7 requires €760/month and has a growing waitlist; Panama’s Pensionado requires $1,000/month but involves more bureaucracy).

The visa has indefinite validity on renewal and creates a path to permanent residency after 3 years of continuous legal residence. Dual citizenship is recognized — you don’t give up your US passport.

Documents required: valid passport, proof of income (bank statements, pension letters, investment account statements), criminal background check apostilled from the US, and health insurance proof. Budget $300–$800 for an immigration lawyer to handle the application — errors cause 2–3 month delays.

Pensionado Visa

Specifically for retirees with $2,500/month in pension or social security income. Same process, same path to permanent residency. If your Social Security plus any pension or annuity clears that threshold, this is the cleanest route for older expats — you’re not trying to prove “passive income,” you’re presenting a government-guaranteed check.

Investor Visa

Requires a minimum investment of PEN 500,000 (~$135,000 USD) in a Peruvian company or real estate project. Faster PR pathway at 2 years rather than 3. Less common among lifestyle expats, more useful for entrepreneurs or those buying Lima rental property as part of their portfolio.

| Visa Type | Income/Asset Requirement | Path to PR | Best For |

|---|---|---|---|

| Rentista | $1,000/month passive income | 3 years | Investors, remote workers with investment income |

| Pensionado | $2,500/month pension | 3 years | Retirees on Social Security + pension |

| Investor | ~$135,000 USD investment | 2 years | Entrepreneurs, real estate investors |

| Tourist Stamp | None | None | Testing the waters, stays under 183 days |

Peru’s Tax System: What You Actually Owe

Peru runs a hybrid territorial/worldwide tax system, and the distinction matters depending on your residency status — which in turn depends on how much time you spend there.

If You Become a Peruvian Tax Resident

Spending more than 183 days in any 12-month period makes you a Peruvian tax resident, triggering worldwide income taxation. Progressive rates range from 8% on the lowest bracket up to 30% on income above roughly 45 UIT (the 2026 Tax Unit is PEN 5,500, or ~$1,480 USD). On a practical basis:

- Income up to ~$28,000 USD equivalent: 8%

- $28,000–$56,000: 14%

- $56,000–$84,000: 17%

- $84,000–$112,000: 20%

- Above $112,000: 30%

These rates are lower than top US marginal rates, but the critical point is that they stack on top of your US obligations unless properly offset.

If You Stay Non-Resident

Peruvian-sourced income is taxed at a flat 30% for non-residents, no deductions. Foreign income — US dividends, US rental income, US client payments — is not taxable in Peru for non-residents. This creates a clean planning window if you spend the first year as a tourist (under 183 days) testing the country before committing to full residency.

Your US Tax Obligations Don’t Disappear

Peru and the US have no bilateral tax treaty. That means you can’t lean on treaty tie-breakers to reduce your US tax burden — every tool you have is domestic: the Foreign Earned Income Exclusion (FEIE) and the Foreign Tax Credit (FTC).

The FEIE lets you exclude up to $126,500 in 2024 earned income if you meet the physical presence test (330 days outside the US). The FTC offsets US taxes dollar-for-dollar against Peruvian taxes paid on the same income. For most expats earning below six figures, properly structured FEIE + FTC brings the combined tax bill well below what they’d owe living in the US. Read our complete US expat tax guide before making any moves.

FBAR and FATCA reporting still apply — Peruvian bank accounts exceeding $10,000 in aggregate require FinCEN 114 filing.

Cost of Living: The Real Numbers

Peru’s cost advantage is most pronounced in housing and food — two line items that account for roughly 65% of most expats’ monthly budgets. Both are dramatically cheaper than equivalent-quality options in Europe, Southeast Asia’s tourist hotspots, or even Mexico City.

Housing Costs by City

| City / Neighborhood | 1BR Furnished | 2BR Furnished | Notes |

|---|---|---|---|

| Lima – Miraflores | $700–$1,100/month | $1,100–$1,600/month | Ocean views, safest district, walkable |

| Lima – Barranco | $500–$900/month | $900–$1,350/month | Bohemian, arts scene, slightly cheaper |

| Lima – San Isidro | $800–$1,200/month | $1,200–$1,800/month | Business/embassy district, quiet |

| Arequipa | $350–$650/month | $600–$950/month | “White City,” 7,500 ft altitude, mild climate |

| Cusco | $300–$600/month | $500–$900/month | 11,000 ft altitude, colonial, tourist hub |

Food is where Peru’s value becomes almost embarrassing. A full three-course menú meal at a local restaurant — soup, main, dessert with juice — runs $3–$6. Weekly groceries at local markets for a single person: $55–$80. Even dining out regularly at mid-range restaurants, most Lima expats spend $300–$450/month on food. In Arequipa or Cusco, subtract another 20%.

Single expat monthly budget in Lima (Miraflores):

- Rent (1BR furnished): $750–$950

- Groceries + dining out: $350–$500

- Transportation (Uber + taxis): $80–$120

- Utilities + internet: $70–$100

- Health insurance: $120–$200

- Entertainment + misc: $100–$200

- Total: $1,470–$2,070/month

In Arequipa or Cusco, the same lifestyle runs $900–$1,400/month. That’s not poverty-level frugality — that’s a full, comfortable life with nice restaurants, a gym membership, and weekend travel to Machu Picchu for under $100 round trip.

Healthcare: Better Than Expected

Lima’s private hospital network is legitimately good. Clínica Anglo Americana in San Isidro is the top expat-oriented facility — English-speaking staff, modern equipment, and costs that would make a US patient weep with relief. A specialist consultation runs $40–$80. A full blood panel: under $50. The San Pablo Group of clinics and Clínica Ricardo Palma are also strong options with English-language services.

Private health insurance from local providers like Rímac Seguros or Pacífico Seguros starts at $120–$250/month and provides comprehensive coverage at Lima’s top private facilities. International coverage from SafetyWing is accepted at major Lima private clinics and costs as little as $45/month for their nomad plan — a solid option while you’re still in the 183-day tourist window before committing to residency.

One important practical note: Peruvian clinics typically expect payment upfront regardless of insurance status. Keep a credit card with adequate limits, pay at the desk, and submit for reimbursement. Since 2024, all private pharmacies are legally required to offer generic alternatives before brand-name drugs — a rule that makes prescription costs surprisingly affordable. For a full comparison of expat health insurance options, see our expat health insurance guide.

Healthcare quality drops sharply outside major cities. If you’re planning to base yourself in rural Andes or the Amazon basin, factor in medical evacuation insurance and plan for Lima or Arequipa as your treatment destination for anything serious.

Banking in Peru

Peru has a strong, stable banking sector. The four main options for expats are BCP (Banco de Crédito del Perú), Interbank, BBVA Perú, and Scotiabank — all of which accept foreign residents and offer accounts in both PEN and USD.

Dollar-denominated accounts are the move for expats living on US-earned income. You hold USD locally, convert to soles at your discretion, and avoid exposure to any future PEN fluctuation. BCP’s Cuenta Experta account includes free online banking with an English-language interface. Interbank and Scotiabank can open accounts for people with just a tourist visa — you don’t need to wait for your Carné de Extranjería (foreigner ID card) to arrive.

For your US-side banking, Charles Schwab’s international checking account remains the gold standard — no foreign transaction fees, unlimited ATM fee rebates worldwide, and no account minimums. Withdraw soles from any Lima ATM at the interbank rate, no fee.

For moving money between your US account and Peru, Remitly offers competitive rates on USD-to-PEN transfers, typically beating bank wire rates by 1–2% on the exchange. On a $3,000/month transfer, that’s $30–$60 saved every single month. Our expat money transfer guide breaks down the full comparison.

Best Neighborhoods for Expats in Lima

Lima is massive and spread-out. Neighborhood selection is the most important decision you’ll make — quality of life varies enormously across the city’s 43 districts.

Miraflores

The default expat hub. Cliff-top oceanfront promenade (Malecón de la Reserva), the Larcomar open-air shopping center, walkable streets with good coffee shops, and the highest concentration of international restaurants in the city. Safe enough to walk at night in the main commercial areas. Rents are the highest in Lima but still well below comparable US neighborhoods.

Barranco

Lima’s creative district — artists, galleries, hip bars, colonial architecture, and a young professional social scene. The iconic Puente de los Suspiros bridge makes you remember you’re actually living abroad, not just working remotely from a coworking space. Rents run 15–25% below Miraflores. Best for under-40 expats who want a social life built in.

San Isidro

The financial and embassy district. Quieter than Miraflores, greener, with Lima’s top private hospitals and international schools nearby. Better for families or older expats who prioritize calm over nightlife. Slightly more expensive than Barranco, roughly on par with Miraflores.

Outside Lima

Arequipa — Peru’s second city, nicknamed the “White City” for its colonial volcanic-stone architecture. Consistently mild climate year-round (60–75°F), 30–50% cheaper than Lima for equivalent housing, a strong and growing expat community, and a genuinely excellent food scene. Altitude at 7,500 feet is noticeable but manageable for most people within a week.

Cusco — 11,000 feet of altitude makes this a challenging permanent base. Acclimatization takes 2–4 weeks, and some people never fully adjust. For those who can handle it: extraordinary colonial architecture, a perpetual international crowd, cheap rents, and proximity to some of the most spectacular landscapes in South America.

Moving Checklist: What to Handle Before and After Arrival

- Virtual US mailbox: Maintain a US address for IRS correspondence, brokerage accounts, and state domicile. Traveling Mailbox provides a real US street address in 50+ cities, scans all mail digitally, and handles check deposits — about $15/month. Essential for keeping your US financial infrastructure intact. See the full guide to virtual mailboxes for expats.

- eSIM for arrival: Saily offers affordable eSIM data plans for Peru so you have connectivity from the moment you land — no hunting for a local SIM at the airport.

- Immigration lawyer: Budget $300–$800 for a Lima-based immigration attorney. Paperwork errors cause 2–3 month delays that can affect your 183-day count.

- Health insurance before departure: Don’t arrive uninsured. SafetyWing is the easiest starting point; upgrade to a local Peruvian plan once residency is established for comprehensive in-network access.

- Pre-move tax consultation: With no US-Peru tax treaty, a one-hour consultation with a US expat CPA before you go is worth far more than it costs. The FEIE/FTC interaction is manageable but needs to be structured correctly from day one.

Who Peru Is Right For (And Who It Isn’t)

Peru works best for expats who prioritize low cost of living and authentic cultural immersion over western-European-style infrastructure. Lima’s Miraflores is legitimately comfortable — but it’s not Lisbon. Internet speeds are solid (20–100 Mbps for $20–$50/month in major cities), but power outages happen occasionally outside the top districts. Healthcare is excellent in Lima and good in Arequipa; anywhere else, you’re relying on basic care for anything serious.

It’s a strong fit for:

- Early retirees who want $1,500–$2,000/month to feel like $5,000 in purchasing power

- Remote workers earning in USD and spending in soles

- Anyone combining serious geographic arbitrage with world-class cuisine — Lima’s food scene genuinely competes globally

- Investors interested in Lima Miraflores real estate (consistent USD-denominated appreciation with a dollarized rental market)

It’s a poor fit if you need consistent tropical warmth (Lima is overcast and gray roughly half the year due to the Humboldt Current), or if you want the turnkey expat-bubble comfort of Medellín’s El Poblado or Lisbon’s Príncipe Real with their established infrastructure and peer communities. For a broader comparison of geographic arbitrage destinations, the Geographic Arbitrage Playbook runs the numbers on 10 countries side by side.

The Bottom Line

Peru’s combination of a $1,000/month Rentista visa, workable tax structure, world-class private healthcare at a fraction of US prices, and cost of living that makes $2,000/month feel genuinely wealthy puts it in the top tier of underappreciated expat destinations. The 9 million Americans living abroad have mostly overlooked it — which is exactly your window before the crowd catches on and rents follow.

Structure your residency correctly, stay compliant with both the IRS and Peru’s SUNAT tax authority, and you’re looking at a lifestyle upgrade that costs less than your current US rent.

Financial Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently and individual circumstances vary. Consult a qualified US expat CPA and a licensed Peruvian immigration attorney before making any relocation or financial decisions. FBAR and FATCA reporting obligations apply to all US citizens and green card holders regardless of where they live.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.