Cyprus Non-Dom: Zero Tax on Dividends for 17 Years

11 min read · 2,658 words

Most expats hunting for low-tax EU residency fixate on Portugal (dead), Italy (now €300,000/year), or Malta. Meanwhile, Cyprus has been sitting there offering something arguably better than all three — and it doesn’t get half the attention it deserves.

Here’s the number that stops people mid-sentence: €4,770. That’s the maximum you pay in Cyprus personal taxes on dividends and interest income — no matter how much you earn. Receive €50,000 in dividends? €4,770. Receive €5,000,000 in dividends? Still €4,770. For 17 years.

This is Cyprus’s Non-Domicile (Non-Dom) regime, and it’s one of the most underrated tax structures in the developed world. The 2026 tax reform just officially secured it for another decade-plus. It survived intact. Here’s exactly how it works.

What Is Cyprus Non-Dom Status?

Cyprus tax law separates two concepts that most countries conflate: tax residency and domicile. You can be a tax resident of Cyprus — legally paying taxes there — without being considered domiciled there. Non-dom status is the default for any foreign national who relocates to Cyprus.

Domicile in Cyprus is established by one of two routes: you were born to a Cypriot-domiciled parent (domicile of origin), or you’ve been a Cyprus tax resident for 17 out of the last 20 years (deemed domicile). A freshly arrived American, British, German, or Brazilian relocating to Cyprus starts with non-dom status automatically — no application required, no fees to the government.

The 17-year deemed domicile clock is rolling, not absolute. If you spend a year or two outside Cyprus as a tax non-resident at any point, the 20-year window shifts forward and your non-dom runway extends. With deliberate planning, some advisors argue the status can be maintained for well beyond the standard horizon.

The SDC Exemption: Why the Math Is Shocking

Cyprus levies a separate tax called the Special Defence Contribution (SDC) on passive income. For domiciled Cyprus residents, the rates hit hard: 17% on dividends (dropping to 5% from 2026 under the new reform), 30% on interest. For non-doms, the SDC rate on all of these is exactly 0%.

Dividends and interest are also exempt from Cyprus’s regular progressive income tax. They’re only exposed to two things: the SDC (0% for non-doms) and the General Healthcare System (GHS) levy at 2.65%.

That 2.65% GHS sounds like a catch, but there’s a ceiling: contributions cap at €4,770 per year, applying to the first €180,000 of income. Beyond €180,000, no additional GHS applies. So whether you earn €200,000 in dividends or €2,000,000, your Cyprus personal tax bill on that income is capped at €4,770.

This isn’t a niche loophole. It’s written directly into Cypriot law, administered by PwC, KPMG, and Deloitte for international clients, and it survived the December 2025 tax reform — Cyprus’s most comprehensive tax overhaul in 20 years — completely intact.

The 60-Day Rule: Minimum Residency You’ve Ever Seen in the EU

Most EU residency programs require 183 days per year. Cyprus doesn’t. Under the 60-day rule, you become a Cyprus tax resident with just 60 days in-country annually, provided you meet all of these:

- You are not a tax resident in any other country

- You don’t spend more than 183 days in any single other country during the year

- You maintain a permanent address in Cyprus — rented or owned

- You have some economic connection to Cyprus: employment, a business, or a directorship of a Cyprus-registered company

The economic tie is easier than it sounds. Holding a directorship in a Cyprus company — even a holding company you form yourself — typically qualifies. You don’t need to be employed by anyone; a properly structured Cyprus company with you as director satisfies the requirement.

Day counting follows standard rules: arrival day counts as a Cyprus day; departure day counts as a day abroad. Sixty genuine days per year — two months split across two or three trips — is the minimum to establish residency.

This makes Cyprus uniquely attractive to investors, fund managers, and business owners who travel constantly. You can spend the bulk of your year in Dubai, Singapore, or across Europe without losing your Cyprus tax residency, as long as no single country clocks more than 183 of your days.

What Income IS Actually Taxed

Non-dom status is not a blanket exemption from everything. Here’s the complete picture:

| Income Type | Tax Treatment for Non-Doms |

|---|---|

| Dividends (worldwide) | 0% SDC + 0% income tax + 2.65% GHS capped at €4,770 |

| Interest income | Same as dividends — capped at €4,770 GHS |

| Capital gains on shares/securities | 0% — blanket exemption for all Cyprus residents regardless of domicile |

| Employment income (Cyprus-source) | Progressive 0–35%; 50% exemption available if salary >€55,000 and new to Cyprus |

| Self-employment income | Progressive 0–35% income tax |

| Rental income (Cyprus property) | Progressive income tax rates (SDC on rentals abolished from 2026) |

| Foreign pension income | 5% flat rate (first €3,420/year exempt); progressive rates if lower |

| Capital gains on Cyprus real estate | 20% CGT (€17,086 lifetime primary residence exemption) |

Cyprus personal income tax brackets, for context:

| Taxable Income (EUR) | Rate |

|---|---|

| 0 – 19,500 | 0% |

| 19,501 – 28,000 | 20% |

| 28,001 – 36,300 | 25% |

| 36,301 – 60,000 | 30% |

| Above 60,000 | 35% |

Employment and self-employment income carries an additional 8.8% social insurance contribution up to a wage ceiling. Non-doms with purely passive income — dividends, interest, securities gains — avoid this contribution entirely.

The Real Numbers: What You Actually Save

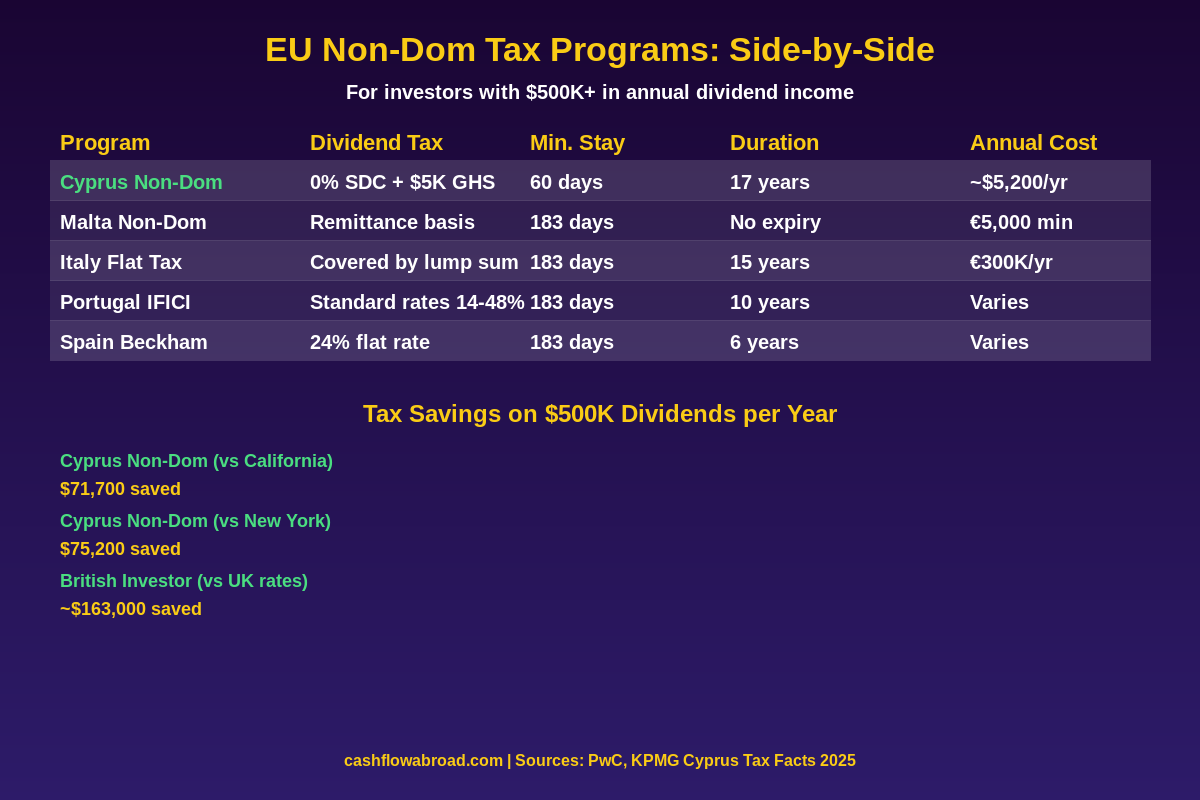

Consider an investor with €500,000 in annual dividend income from a globally diversified portfolio held personally (not through a company). What does Cyprus non-dom status mean versus staying home?

| Jurisdiction | Tax on €500K Dividends | Annual Savings vs. Cyprus |

|---|---|---|

| Cyprus Non-Dom | €4,770 (GHS cap) | — |

| Germany | ~€131,875 (26.375% Abgeltungsteuer) | €127,105/year |

| United Kingdom | ~€168,750 (33.75% higher rate) | €163,980/year |

| France | ~€150,000 (30% prélèvement forfaitaire unique) | €145,230/year |

| Italy (new flat tax) | €300,000 (flat annual lump sum) | €295,230/year |

Over a 17-year non-dom horizon, a British investor receiving €500,000/year in dividends saves approximately €2.79 million in taxes compared to staying in the UK — before any growth on those invested savings. Even accounting for Limassol rent, accounting fees, and legal costs over the full 17 years (~€100,000 in total), the net benefit exceeds €2.6 million.

Initial setup costs are modest: approximately €1,500–3,000 in legal fees, €1,800–3,500/year in accounting, and €800–1,800/month for a Limassol apartment during your 60-day stays. Break-even on those costs against a high-tax European country typically happens in the first 30–60 days of Year 1.

The Corporate Layer: How Business Owners Stack the Advantage

Cyprus non-dom status combines with Cyprus’s corporate tax regime for a powerful stack. The corporate rate moved from 12.5% to 15% in January 2026 to satisfy the OECD Pillar Two minimum, but three major exemptions survived unchanged:

- Dividends received by a Cyprus company from subsidiaries: generally 100% exempt from corporate tax

- Capital gains on securities at the corporate level: 0% — a Cyprus holding company can sell shares in any company, anywhere in the world, with zero Cyprus corporate tax on the gain. No minimum holding period required.

- IP Box: 80% deduction on qualifying IP income, bringing the effective IP profit rate down to 2.5%

The full structure: your operating business pays 15% Cyprus corporate tax on active profits. The company distributes dividends to you, the non-dom individual shareholder. You pay 0% SDC + 2.65% GHS (capped at €4,770) on those dividends. Total effective rate: 15% at the company level, then €4,770 maximum personally — regardless of how large the distribution.

The December 2025 reform also abolished the Deemed Dividend Distribution (DDD) rule, which previously required Cyprus companies to distribute 70% of profits within two years or face SDC charges. This is gone for profits from 2026 onward, giving business owners flexibility to time distributions strategically.

Cyprus vs. The Alternatives

Portugal’s NHR for investors is effectively dead as of March 2025, replaced by IFICI — a narrowly targeted program for scientists, researchers, and qualifying tech professionals. Standard passive investors no longer qualify.

Italy’s flat tax landed at €300,000/year in 2026, having jumped from €100,000 to €200,000 in August 2024 and then again. Over 15 years, that’s €4.5 million to participate. The math only works for investors generating tens of millions annually in foreign income.

Malta’s non-dom regime operates on a remittance basis — income and assets kept offshore aren’t taxed, with a minimum €5,000/year tax. It’s workable but requires the operational complexity of keeping income genuinely outside Malta, and the country’s banking and business environment is smaller than Cyprus’s.

Cyprus stands as the most scalable EU option: costs stay fixed at ~€4,770/year regardless of income above €180,000, the minimum stay is the lowest in the EU, and the program is now legislatively extended to 27 years for those who need it.

The US Expat Caveat: Read This Before Booking Your Flight

The IRS taxes US citizens on worldwide income, regardless of where they live. Cyprus non-dom status eliminates your Cyprus tax bill on passive income — but it does nothing to your IRS obligation.

The Foreign Tax Credit only credits taxes actually paid to a foreign government. If you pay €4,770 in Cyprus on €500,000 of dividend income, that’s all you can credit against US liability. The remaining federal tax applies in full. Without a US-Cyprus tax treaty (one doesn’t exist), there’s no bilateral mechanism to prevent double taxation on passive income.

This makes Cyprus non-dom significantly less valuable for US citizens receiving US-source dividends than for citizens of high-tax countries. The value shows up differently for Americans:

- Business owners who restructure through a Cyprus company create a 15% corporate-level tax that’s creditable on the US return. The non-dom regime then shelters distributions beyond that.

- High earners using FEIE can exclude up to $126,500 (2024 figure, indexed annually) of foreign earned income — Cyprus residency satisfies the bona fide residence test — while keeping passive income taxes capped at €4,770.

- Anyone seriously considering renunciation who wants a clean, tax-efficient EU landing spot. Cyprus non-dom is one of the more attractive post-renunciation setups in Europe.

Before making any structural moves, understand how the FEIE and Foreign Tax Credit interact with your specific income profile. The full US expat tax guide covers FBAR, FATCA, and residency obligations that continue regardless of where you live.

One practical infrastructure note: if you move to Cyprus, you’ll still need a US mailing address for IRS correspondence, banking, and any ongoing US business. Traveling Mailbox provides real US street addresses in 50+ cities with mail scanning and check deposit capability for $15/month — standard infrastructure for serious expats maintaining US ties.

How to Set Up Cyprus Non-Dom Residency

There’s no government application for non-dom status. It’s your default as a foreign national establishing Cyprus tax residency. Here’s the actual process:

1. Establish a Cyprus address. Rent or buy a property. Limassol is the hub for international business and professional services — expect €800–1,800/month for a two-bedroom. Larnaca and Nicosia run cheaper (€600–1,200) but have fewer international resources.

2. Set up a Cyprus company or employment tie. The most common route is incorporating a Cyprus limited company and appointing yourself director. Setup costs: €1,500–3,000 through a local law firm. Annual maintenance (accounting, audit, registered office): €1,800–3,500. The company can be a pure holding company — it doesn’t need to operate commercially in Cyprus.

3. Register for a Tax Identification Number (TIN). Done in person or via a local representative at the Cyprus Tax Department. Free of charge.

4. Spend your 60 days. Split across two or three visits. Keep documentation: boarding passes, rental agreements, utility bills, mobile phone records. The 60-day count needs to be defensible.

5. File your annual Cyprus tax return. Deadline: July 31 for the prior calendar year. A local accountant handles this — expect €500–1,000/year for a simple personal return with primarily dividend income.

One note on banking: Cyprus banks run intensive KYC processes. About 19% of foreign applicants were rejected in 2024. Bring complete documentation — passport, proof of address, source-of-wealth statement, bank reference letter. Opening an account in person during one of your early visits is strongly recommended over attempting remote onboarding.

For investment accounts, most Cyprus non-doms keep brokerage accounts in the US, UK, or Ireland. Charles Schwab International is consistently expat-friendly — they don’t close accounts based on foreign residency, offer free ATM withdrawals globally, and support international account holders. For moving funds between jurisdictions, Remitly offers transparent rates on international transfers.

Health Coverage

Your GHS levy (€4,770/year maximum) entitles you to access Cyprus’s General Healthcare System — a universal scheme that covers primary care, specialists, and hospital stays. For non-doms who travel heavily and want worldwide coverage, supplementing with international health insurance is common. SafetyWing’s Nomad Health plan provides comprehensive global medical coverage, which pairs well with the multi-country lifestyle Cyprus non-dom naturally enables.

The Real Downsides

Cyprus non-dom is genuinely attractive, but the marketing version often omits a few things worth knowing:

The 17-year clock is rolling. Once you’ve been a Cyprus tax resident for 17 out of any 20-year rolling window, deemed domicile kicks in and you lose non-dom status. Strategic breaks — genuinely leaving Cyprus tax residency for a year or two — push the window forward. But it requires active management, not passive assumption that it lasts forever.

No US-Cyprus tax treaty. This is the single biggest limitation for Americans. There’s no comprehensive bilateral agreement to prevent double taxation or reduce withholding on US-source income paid to Cyprus entities. The 30% US withholding on interest and dividends paid to a Cyprus company (without treaty relief) can undermine the structure if not managed properly.

Cyprus is not Schengen — yet. EU membership without Schengen membership means non-EU expats in Cyprus still use passports at borders with Schengen countries. Cyprus has secured EU backing for Schengen accession in 2026; the accession process was in technical review as of early 2026. EU citizens are unaffected.

Rental income on Cyprus property is still taxed. Non-dom status doesn’t shelter Cyprus-source rental income from progressive rates. If you buy a property in Limassol and rent it out while traveling, that income goes through the standard tax brackets.

Banking history carries weight. The 2013 bail-in is part of institutional memory. For large sums, most sophisticated Cyprus non-doms keep significant assets in EU banks outside Cyprus rather than concentrating in Cypriot institutions — even with the €100,000 EU deposit guarantee.

Who Cyprus Non-Dom Is Actually Built For

The clearest beneficiaries:

- Non-US investors with large dividend or interest portfolios. British, Australian, Canadian, and European citizens paying 25–40% on passive income can collapse that bill to €4,770/year.

- Business owners distributing profits from an international holding structure. The 15% corporate + €4,770 personal cap is among the most efficient in the EU for non-US persons.

- Crypto-active investors. Cyprus treats individual crypto gains the same as securities gains — exempt. Non-dom status further shelters dividends from Cyprus crypto companies. Combined with the 60-day minimum stay, it’s hard to beat in the EU.

- High-travel professionals and fund managers who can satisfy the 60-day rule without significantly changing their lifestyle.

- US citizens with restructured business income who can generate creditable corporate tax to offset US liability while sheltering personal distributions.

If you’re mapping out the full geographic arbitrage playbook — where to live to maximize what your income buys — Cyprus belongs in any serious comparison. The expat investing playbook covers what happens to your US investment accounts when you relocate abroad, which is a prerequisite read before making any structural moves involving foreign residency.

The Bottom Line

The EU’s best-kept tax secret for passive income investors is sitting on an island in the Eastern Mediterranean with beaches, English as a working language, and a regulatory regime that says: your dividends, your interest, your securities gains — we want almost none of it.

For non-US investors, the math is nearly impossible to argue with at scale. €4,770/year on seven-figure passive income, EU membership, 60-day minimum stay, and a regime that survived the most comprehensive tax reform in Cyprus’s modern history. Italy charges €300,000/year for less flexibility. Portugal closed the door. Cyprus is open.

The caveats for Americans are real and worth planning around — but they don’t make Cyprus unworkable. They make it a structure that requires genuine advice from someone who knows both Cypriot and US international tax law, rather than a simple plug-and-play relocation. Get that advice before you move. The regime’s value is substantial enough that the cost of a proper consultation is trivial by comparison.

Financial Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations change frequently; specific rules may have been updated after publication. Cyprus non-dom status involves significant legal and tax planning that varies by individual circumstances, country of citizenship, and income structure. US citizens should specifically consult a tax professional with expertise in US international tax law — including FBAR, FATCA, FEIE, and Foreign Tax Credit rules — before making any tax residency decisions. Nothing in this article should be construed as a recommendation to restructure assets or establish residency in any jurisdiction.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.