The Foreign Housing Exclusion Most Expats Forget to Claim

The Form 2555 foreign housing exclusion or deduction can reduce taxable foreign earned income above a base amount, subject to general and high-cost-location limits. Here is the 2026 calculation and filing sequence.

- For 2026, the maximum Foreign Earned Income Exclusion is $132,900 and the full-year base housing amount is $21,264, or 16% of that limit.

- The general full-year housing-expense limit is $39,870 before subtracting the base amount; IRS Notice 2026-25 lists higher limits for qualifying high-cost locations.

- Employees generally claim a foreign housing exclusion, while self-employed taxpayers calculate a foreign housing deduction on Form 2555.

- The housing calculation is completed before the Foreign Earned Income Exclusion, and excluded income cannot also support a foreign tax credit.

- Neither the FEIE nor the foreign housing exclusion or deduction reduces self-employment tax.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Short answer: qualifying employees abroad can use Form 2555 to exclude eligible housing costs above the annual base amount, subject to the general or location-specific limit. Self-employed taxpayers calculate a foreign housing deduction instead. The housing amount is calculated before the Foreign Earned Income Exclusion, and neither benefit reduces self-employment tax.

Use the IRS's current foreign housing exclusion or deduction guidance together with Notice 2026-25. The amount depends on qualifying days, employer-provided amounts, eligible expenses, and the location where you incurred them.

What Is the Foreign Housing Exclusion?

The Foreign Housing Exclusion lives in IRC §911(c) and is filed on Form 2555 (Part VI for employees; Part IX for the self-employed, where it becomes a deduction instead). It works on top of — not instead of — the standard FEIE.

The formula is simple:

Excludable Housing Amount = Qualified Housing Expenses − Base Amount

(subject to a city-specific annual cap)

For 2025, the base amount is $20,800 (16% of the $130,000 FEIE). That base represents what the IRS considers a "normal" US housing cost. Every dollar of qualified foreign housing expense above that threshold — up to your city's annual cap — gets excluded from gross income, on top of your standard $130,000 FEIE.

So if you're renting in London for $48,000/year and utilities add $4,000 more, your qualifying expenses total $52,000. Subtract the $20,800 base, and you get a $31,200 housing exclusion. Stack that on your $130,000 FEIE and you've effectively excluded $161,200 from federal income tax before touching a single deduction.

The 2025 Numbers You Need

| Metric | 2024 | 2025 | 2026 |

|---|---|---|---|

| FEIE Max Exclusion | $126,500 | $130,000 | $132,900 |

| Housing Base Amount (16%) | $20,240 | $20,800 | $21,264 |

| Standard City Cap | $37,950 | $39,000 | $39,870 |

| Combined Max (standard city) | $164,450 | $169,000 | $172,770 |

The caps increase annually with inflation. Married couples who both qualify can each claim a full exclusion: $260,000 in combined FEIE for 2025, plus each spouse's housing costs.

High-Cost City Limits: Where the Exclusion Gets Serious

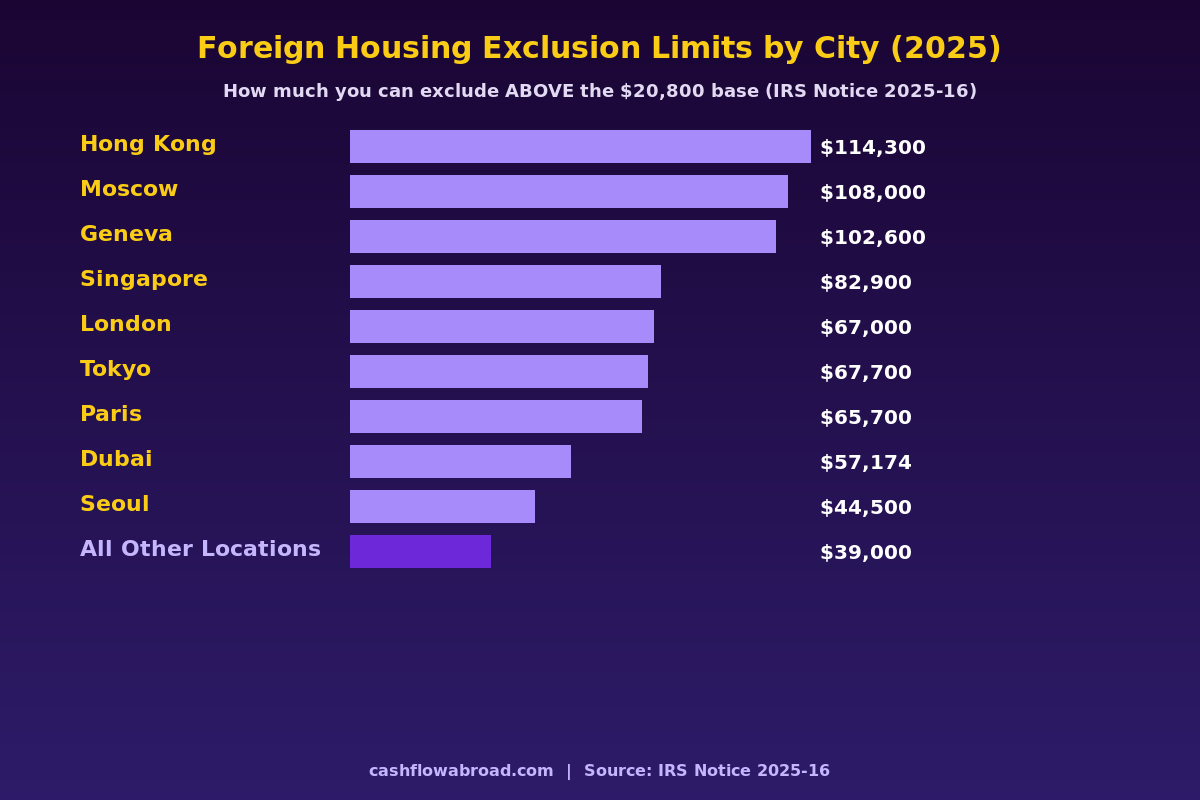

The IRS publishes elevated housing caps for 146 cities through annual notices. IRS Notice 2025-16 (released March 5, 2025) sets the following limits. These are the total annual housing cost caps — not the additional exclusion amount. Subtract the $20,800 base to find your maximum excludable housing benefit.

| City / Location | 2025 Annual Cap | Max Excludable Above Base |

|---|---|---|

| Hong Kong | $114,300 | $93,500 |

| Moscow, Russia | $108,000 | $87,200 |

| Geneva, Switzerland | $102,600 | $81,800 |

| Singapore | $82,900 | $62,100 |

| Tokyo, Japan | $67,700 | $46,900 |

| London, United Kingdom | $67,000 | $46,200 |

| Paris, France | $65,700 | $44,900 |

| Sydney, Australia | $62,300 | $41,500 |

| Dubai, UAE | ~$57,174 | ~$36,374 |

| Seoul, South Korea | $44,500 | $23,700 |

| All other locations | $39,000 | $18,200 |

A US employee in Hong Kong paying $90,000 in annual rent could exclude up to $93,500 in housing costs. Stack that on the $130,000 FEIE and you've excluded $223,500 from federal income tax in a single year — all from one form.

IRS Notice 2026-25 contains an unusual planning opportunity: for 60 locations where the 2026 cap is higher than the 2025 cap, taxpayers can retroactively apply the 2026 limits to their 2025 tax return. If you're filing in a qualifying city like Geneva or Singapore, verify whether your location qualifies before finalizing your 2025 return.

What Counts — and What Doesn't

The IRS is specific. Not everything you spend on housing qualifies.

Qualifying expenses:

- Rent on your principal residence abroad

- Electricity, gas, water, and sewer utilities

- Renter's insurance premiums

- Furniture rental

- Residential parking

- Nonrefundable lease fees or deposits

- Reasonable household repairs

Not qualifying:

- Mortgage principal payments

- Mortgage interest (deductible separately, but excluded from the housing exclusion calculation)

- Home purchase costs or capital improvements

- Domestic help — housekeepers, nannies, gardeners

- Internet service and telephone

- Cable, streaming subscriptions

- Meals or groceries

- Second residence costs

If your employer pays rent directly or provides housing as a benefit, that amount may already be excluded under IRC §119. You cannot double-dip — the housing exclusion covers costs you personally bear above the base amount.

What This Actually Saves: A Real Calculation

US employee, $180,000 in foreign earned income, living in London, $52,000 in annual qualifying housing costs (rent plus utilities), single filer.

FEIE only:

- Exclude $130,000 via FEIE → taxable income: $50,000

- Federal income tax (2025 brackets): ~$6,617

FEIE + Housing Exclusion:

- Housing exclusion: $52,000 − $20,800 = $31,200 (under London's $67,000 cap)

- Taxable income drops to $18,800

- Federal income tax: ~$2,118

- Additional savings from housing exclusion: ~$4,499/year

At London's maximum cap ($46,200 excludable), the income tax savings reach roughly $10,164 per year at the 22% marginal rate. Over a 5-year corporate assignment, that's over $50,000 in additional tax savings — from checking one more box on a form you're already filing.

The Self-Employed Trap

If you're self-employed abroad, the mechanics shift — and not in your favor.

Self-employed expats claim a Foreign Housing Deduction (Form 2555, Part IX) rather than an exclusion. The housing amount still reduces your income tax liability, but here's what catches people: neither the FEIE nor the housing deduction reduces self-employment (SE) tax.

SE tax runs at 15.3% on net self-employment income (applied to 92.35% of net earnings). Even if you exclude the full $130,000 from income tax, you still owe SE tax on that income — approximately $18,370 per year at the full exclusion amount. The housing deduction adds no relief here.

That's why many self-employed expats explore structuring through a US S-corporation or look at whether a totalization agreement applies to their host country. For the full self-employment tax picture, see our guide on the self-employment tax trap for expat freelancers.

FEIE + Housing vs. Foreign Tax Credit: Which Strategy Wins?

The housing exclusion only works alongside the FEIE. You cannot claim both the FEIE and the Foreign Tax Credit (FTC) for the same income in the same year. These are mutually exclusive elections for any given dollar of foreign earned income.

The FEIE + housing exclusion wins when:

- Your host country has low or zero income tax (Dubai, Singapore, Hong Kong, Cayman Islands)

- Your effective local tax rate is below the US equivalent

- Most of your income is foreign earned income rather than passive income

The FTC tends to win in high-tax countries — France, Germany, Scandinavian countries — where local taxes already exceed the US amount. In those situations, the FTC can zero out your US tax bill without "using up" your exclusion. See the detailed breakdown in our FEIE vs. Foreign Tax Credit guide.

One important caveat: the FEIE election, once revoked, triggers a 5-year waiting period before you can re-elect it. Think carefully before switching strategies mid-career.

Record-Keeping and Banking Basics

Claiming the housing exclusion means documenting every qualifying expense: rent receipts, lease agreements, utility statements, insurance invoices. Keep records for at least 6 years given the extended statute of limitations that applies to certain foreign reporting situations.

A dedicated bank account for housing expenses simplifies substantiation significantly. Charles Schwab International remains a top choice for expats — no foreign transaction fees, fee-free ATM withdrawals worldwide, and their brokerage integrates seamlessly with your checking account for clean expense tracking.

You'll also need a verifiable US address for IRS correspondence while living abroad. Traveling Mailbox provides a real US street address in 50+ cities with mail scanning and check deposit capability for around $15/month — an easy way to maintain your IRS address, state domicile, and US banking access while overseas.

If you're also managing foreign investment accounts and want to understand how they interact with PFIC rules and foreign tax reporting, our expat investing playbook covers the full compliance picture.

Three Mistakes That Cost Expats the Exclusion

1. Not checking the city-specific cap. Some expats conservatively estimate their housing costs to "play it safe" — and claim far less than their city's actual cap allows. Run the numbers against IRS Notice 2025-16 before you file.

2. Including non-qualifying expenses. Internet, cable, domestic help, and purchased furniture are the most common mistaken inclusions. Each is specifically excluded in the Form 2555 instructions. Including them creates an audit exposure that isn't worth the risk.

3. Revoking the FEIE election without understanding the consequences. Switching from FEIE + housing to FTC seems appealing when your host country's tax rate rises — but the 5-year lockout after revocation can create a painful gap if circumstances change again. The FEIE deep-dive on this site covers the election and revocation mechanics in full.

Don't Leave $10,000+ on the Table

The Foreign Housing Exclusion isn't a gray area or aggressive position — it's a statutory benefit Congress wrote into the tax code specifically for Americans living and working abroad. The IRS publishes updated city caps every spring. The form is the same one you're already filing. The only reason most expats miss it is that nobody told them it exists.

If you're in a high-cost city, paying rent abroad, and already claiming the FEIE, add Part VI to your Form 2555 this year. Bring the numbers to a tax professional who specializes in international returns. At $10,000 or more in potential annual savings, the CPA fee pays for itself in the first year — often by the second invoice.

For the complete expat financial compliance picture — banking, brokerage, FBAR, and tax treaties — see our US expat banking and taxes guide.

Financial disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws are complex and subject to change. The FEIE, foreign housing exclusion, and Foreign Tax Credit involve nuanced trade-offs that depend on your specific income, filing status, country of residence, and host-country tax situation. Consult a qualified tax professional with US international tax expertise before making any filing decisions.

Frequently asked questions

What is the 2026 foreign housing base amount?

For a full qualifying year, the 2026 base housing amount is $21,264, equal to 16% of the $132,900 maximum Foreign Earned Income Exclusion. A partial-year base is calculated daily for qualifying days.

What is the general 2026 housing-expense limit?

The general full-year limit on eligible housing expenses is $39,870, or 30% of the 2026 FEIE maximum. The potential housing amount is eligible expenses up to the applicable limit minus the base amount. High-cost locations can have higher limits under IRS Notice 2026-25.

Do self-employed expats claim the housing exclusion?

Self-employed taxpayers generally calculate a foreign housing deduction rather than an exclusion. Someone who is both an employee and self-employed during the year may have both components, subject to the Form 2555 rules.

Can I claim a foreign tax credit on income excluded by Form 2555?

No. Foreign taxes allocable to income excluded under the FEIE or foreign housing exclusion cannot also be claimed as a foreign tax credit or deduction. The allocation can be complex when only part of income is excluded.

Does the foreign housing exclusion reduce self-employment tax?

No. The IRS states that the foreign housing exclusion or deduction can reduce regular income tax but does not reduce self-employment tax.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 1, 2026

Expat Tax & FinanceMay 1, 2026

The $75K Tax Break US Expats Leave on the Table

Most US expats claim the FEIE and stop — missing a second IRS shelter that can shield up to $93K more in cities like Hong Kong or Singapore.

Expat Tax & FinanceJuly 14, 2026

Expat Tax & FinanceJuly 14, 2026

Expat State Taxes: Which US States Won't Let You Go

Move abroad and California may still tax you 13.3%. Learn which five states chase expats, how domicile works, and how to sever state ties legally.

Expat Tax & FinanceMay 29, 2026

Expat Tax & FinanceMay 29, 2026

Self-Employment Tax: The Expat Freelancer’s Hidden Bill

FEIE zeroes your income tax abroad—but SE tax still applies. See the exact numbers and legal ways to reduce your bill as a US expat freelancer.