US Citizenship Renunciation: The Exit Tax Trap

Renouncing US citizenship triggers a brutal exit tax — ,350 fee, mark-to-market on all assets, IRA deemed distributions, and a new 40% inheritance tax on US heirs.

The real cost of renouncing US citizenship: ,350 fee, mark-to-market exit tax, IRA deemed distributions, and Section 2801 inheritance tax on US heirs.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

The State Department charges you $2,350 just to fill out a form. Then the IRS arrives. For roughly 4,820 Americans who renounced their citizenship in 2024 — a 48% jump from 2023 — the exit was far more expensive than they anticipated. The dirty secret: renouncing US citizenship doesn't set you free from US taxes. It triggers one of the most aggressive exit tax regimes in the developed world, and most people only find out after it's too late to restructure.

This is not a guide about whether you should renounce. That's your call. This is about the financial mechanics — the IRS rules, the dollar thresholds, and the traps that turn what looks like a clean break into a six-figure tax event.

Who Qualifies as a "Covered Expatriate"

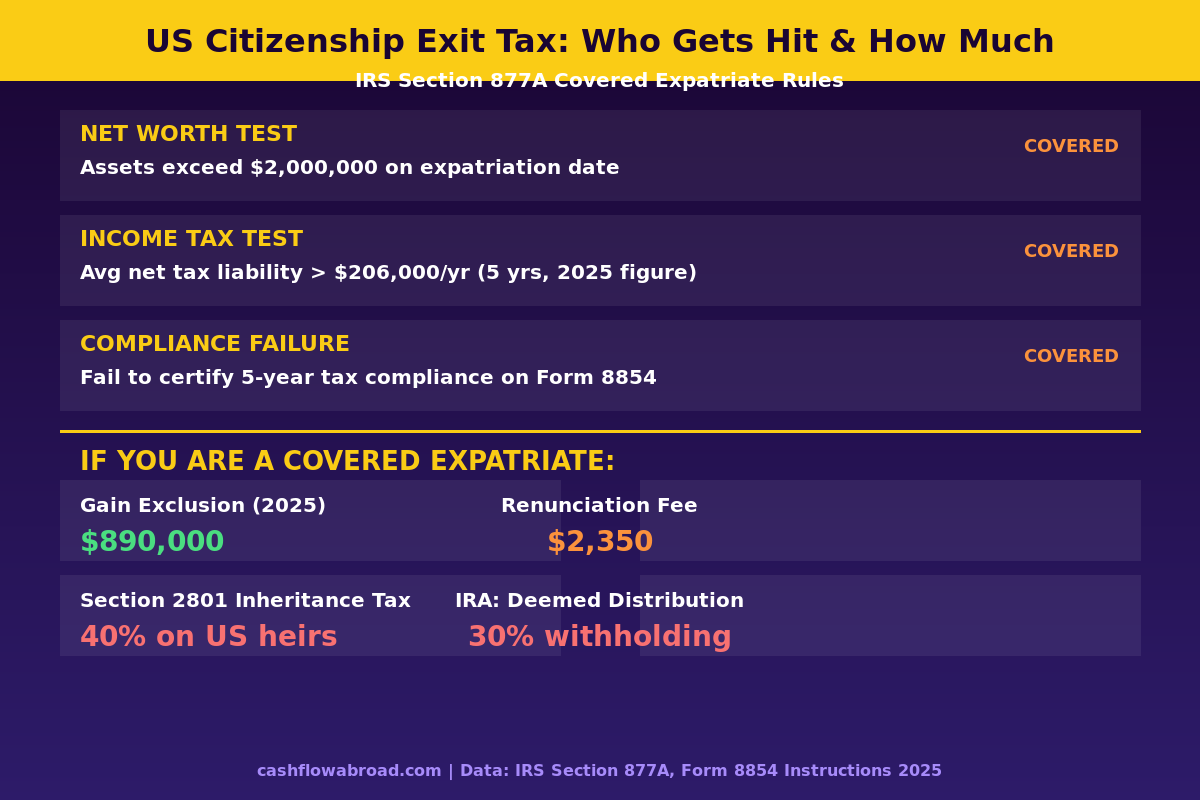

The IRS doesn't impose the exit tax on everyone who renounces or abandons a green card. It only hits covered expatriates — a legal designation under Section 877A of the Internal Revenue Code. You become a covered expatriate if you meet any one of three tests:

| Test | Threshold (2025) | What Counts |

|---|---|---|

| Net Worth Test | $2,000,000+ | All worldwide assets at fair market value on expatriation date |

| Income Tax Test | Avg $206,000/yr net tax liability over prior 5 years | Average annual US net income tax — inflation-adjusts each year |

| Compliance Failure | N/A | Failure to certify 5-year tax compliance on Form 8854 |

The compliance failure test catches more people than the other two combined. If you don't file Form 8854 — or file it late, or check the wrong box — you are automatically deemed a covered expatriate regardless of your net worth or income. Many expats who were otherwise below the thresholds have tripped this wire simply through paperwork errors.

The $2 million net worth threshold also catches people who consider themselves middle-class. A paid-off house in San Francisco or Boston, a 401(k), some index funds, and a small business equity stake can easily cross $2 million without you thinking of yourself as "wealthy."

The Mark-to-Market Deemed Sale: Your Biggest Surprise

Here's the mechanism that generates the actual tax bill. On the day before your expatriation date, the IRS treats you as having sold every asset you own worldwide at fair market value. Stocks, real estate, business interests, foreign investment accounts — all of it is deemed sold at once.

You then owe capital gains or ordinary income tax on any net gain above the exclusion amount. In 2025, that exclusion is $890,000. Gain above that threshold is taxed at applicable rates (0%, 15%, or 20% for long-term capital gains, up to 37% for short-term or ordinary income items).

Practical example: you've built up $1.5 million in appreciated stock since your original cost basis of $200,000. The deemed sale triggers a $1.3 million gain. After the $890,000 exclusion, $410,000 is taxable. At the 20% long-term rate, that's $82,000 owed on the day you renounce — before you've sold a single share.

Real estate held abroad gets particularly complicated because the IRS uses USD values throughout. If the foreign currency appreciated against the dollar during your holding period, you can owe US tax on gains that are purely attributable to exchange rate movements — the "phantom gain" problem that affects many expats.

What Happens to Your IRA and 401(k)

Retirement accounts don't get mark-to-market treatment. They get something worse: they're treated as fully distributed on the day before expatriation. The entire balance of your traditional IRA is deemed withdrawn at once, subject to income tax (not capital gains rates) — though notably without the 10% early withdrawal penalty.

For employer-sponsored deferred compensation plans (pension, 401k distributions, stock options), the IRS imposes a flat 30% withholding tax on future payments made after expatriation. If you have a pension from a former US employer that will pay $5,000/month starting at age 65, 30% of every payment goes to the IRS indefinitely.

The only partial relief: if you have a deferred compensation plan and can elect a lump-sum distribution before you renounce, that amount gets folded into the mark-to-market calculation with the $890,000 exclusion available. Timing matters enormously here, and the difference between acting before versus after can easily exceed six figures. This is where a tax attorney who specializes in expatriation becomes essential.

For expats still building their retirement accounts, the expat 401k and IRA playbook covers how these accounts work while you're abroad — and why your strategy shifts dramatically if renunciation is on the table long-term.

The $2,350 Fee and Form 8854

Before any tax bill, you pay $2,350 to the US State Department just to begin the renunciation process. This fee, introduced in 2014 (up from $450 — a 422% increase), is non-refundable even if you change your mind during the process. The State Department typically requires an appointment at a US embassy or consulate, and wait times in popular expat destinations run six to eighteen months in many locations.

After the consular appointment, the tax obligations kick in:

- Form 8854 — "Initial and Annual Expatriation Statement" — must be filed with your final year's tax return. Missing this form = automatic covered expatriate status. If you're a covered expatriate and file Form 8854 after the due date, you may owe the exit tax anyway.

- Form 1040-NR — used for the year of expatriation (part-year resident, part-year non-resident).

- FBAR and FATCA compliance — you must certify 5 years of compliance on Form 8854, which means 5 years of FBARs (FinCEN 114) and FATCA (Form 8938) if applicable. Many expats discover outstanding filing obligations at this stage.

The FBAR rules alone are a landmine. A single non-willful violation can cost $16,536; willful violations run $165,353 or 50% of the account balance, whichever is greater, per violation per year. If you have unreported foreign accounts in your history, getting into full compliance before expatriating is essential — and the FBAR/FATCA reporting guide covers exactly how that process works.

Section 2801: The Tax Your US Family Pays After You're Gone

This is the provision that most renunciation guides skip entirely. Under Section 2801 of the Internal Revenue Code, if you are a covered expatriate and you give money or leave an inheritance to a US-citizen or US-resident family member, they owe a 40% tax on what they receive.

This rule existed on paper since the HEART Act of 2008, but the IRS had never issued implementing regulations — so many practitioners treated it as unenforceable. That changed on January 14, 2025, when Treasury finalized the Section 2801 regulations. They are now fully enforceable and apply to covered gifts and bequests received on or after January 1, 2025.

The mechanics:

| Scenario | Amount | Annual Exclusion | Tax Owed by US Recipient |

|---|---|---|---|

| Gift from covered expatriate parent to US-citizen child | $500,000 | $19,000 (2025) | $192,400 (40% × $481,000) |

| Inheritance from covered expatriate parent | $1,000,000 | $19,000 (2025) | $392,400 (40% × $981,000) |

| Gift below annual exclusion | $18,000 | $19,000 (2025) | $0 |

Note what's absent: the donor's unified gift/estate tax credit does not offset this tax. The covered expatriate's estate may also owe taxes in their new country of residence. The result is potential double-taxation on the same transfer — once in the foreign country, once by the US recipient paying Section 2801 tax.

If you have US-citizen children and are considering renouncing, this is no longer a theoretical problem. The Section 2801 tax is fully in effect. Estate planning needs to account for it explicitly — the expat estate planning guide covers strategies for cross-border wealth transfer in this new environment.

Why 4,820 Americans Renounced in 2024 Anyway

Despite the costs, renunciation is accelerating. The 2024 figure of 4,820 was the third-highest annual total on record, up 48% from 3,253 in 2023. The surge in Q3 2024 alone — 2,123 renunciations in a single quarter — was the highest quarterly figure since late 2016.

The primary driver isn't wealthy people dodging taxes. Most renunciations are driven by ordinary Americans living abroad who are unable to maintain basic financial services because of US reporting burdens. FATCA, the 2010 law that forces foreign banks to report US account holders to the IRS, has caused thousands of non-US banks to simply refuse American clients. Opening a bank account, getting a mortgage, or investing in local funds has become impossible or severely restricted in many countries for US passport holders.

The cost-benefit calculation shifts once you're living permanently in a country where you can't get a mortgage or a brokerage account because of your US citizenship — especially if you have no US income and owe zero US tax anyway. For those people, renunciation is about functionality, not tax evasion.

For expats who want to stay American but reduce their tax exposure, the alternatives are meaningful. The Foreign Earned Income Exclusion eliminates federal tax on up to $126,500 of foreign-earned income (2024 figure). Territorial tax countries let you structure your life so that offshore income isn't taxed by your country of residence either — a dramatically lower-cost alternative to renunciation for many people.

Who Should Actually Consider Renouncing

The exit tax math often makes renunciation more expensive than staying American for most people. But there are scenarios where it's worth the analysis:

- Permanent non-resident with no US income: If you've lived abroad for 10+ years, have no US-source income, and pay full taxes in a country with a US tax treaty, you may be filing US returns every year to report zero tax owed — paying thousands in accounting fees for paperwork that means nothing.

- Below the exit tax thresholds: If your net worth is well under $2 million and your historical US tax liability was below $206,000/year, you won't be a covered expatriate. The exit tax doesn't apply. Your cost is $2,350 plus accounting fees, and you're done with the IRS forever.

- Dual citizens by birth: People who acquired US citizenship at birth but grew up in another country often have stronger ties to their other citizenship and minimal US connections. For them, renouncing can be largely an administrative act with limited financial impact if the asset and income thresholds aren't met.

For anyone near or above the thresholds, the analysis requires a qualified tax attorney — not a CPA and not a DIY calculation. The interplay between mark-to-market timing, IRA treatment elections, Section 2801 planning, and state-level implications (some states impose their own exit taxes) is genuinely complex.

Practical Checklist Before You Start the Process

- Audit 5 years of US tax filings — ensure all returns are filed and accurate. Missing years must be amended before you can certify compliance on Form 8854.

- File all outstanding FBARs — 6 years of FinCEN 114 are required for the Streamlined Filing Compliance Procedures if you have unreported accounts.

- Calculate your net worth precisely — include all worldwide assets: foreign real estate at current FMV, business interests, cryptocurrency holdings, life insurance cash value. If you're near $2 million, get a professional appraisal.

- Model the IRA/retirement account decision — determine whether a pre-renunciation lump-sum election saves more than the deemed-distribution treatment.

- Consider Section 2801 implications — if you have US-citizen heirs who will inherit, factor the 40% inheritance tax into your estate planning now.

- Book your consular appointment early — wait times at busy embassies in London, Paris, and Zurich run 6–18 months. Your planning window is long.

- Maintain a US address during transition — a virtual mailbox service keeps your US address current for banking and IRS correspondence during the multi-year wind-down process.

If you're below the covered expatriate thresholds and your US compliance is clean, renunciation can genuinely be a straightforward process. If you're above the thresholds, it requires the same level of planning as a major corporate transaction — because that's essentially what it is.

The Alternative: Stay American, Pay Less

Renunciation gets attention because it's dramatic, but it's rarely the best financial move for someone primarily motivated by tax savings. The IRS allows Americans living abroad to eliminate most of their US tax liability without renouncing:

- The FEIE eliminates federal income tax on up to $126,500 of foreign-earned income (2024)

- The Foreign Tax Credit offsets US tax liability dollar-for-dollar against taxes paid to a foreign government

- Living in a territorial tax country (Panama, Georgia, Paraguay, Costa Rica) means your local government doesn't tax your foreign income either

- Properly structured US investments held through a PFIC-compliant brokerage like Charles Schwab International remain available to Americans abroad without triggering punitive PFIC rules

The combination of FEIE, Foreign Tax Credit, and a low-tax country of residence can get many expats to an effective US tax rate near zero — without the $2,350 fee, the exit tax, or the Section 2801 exposure for their heirs.

The Bottom Line

Renouncing US citizenship is a legitimate choice, and for some people it genuinely makes sense. But the marketing around it — "cut the cord," "stop paying US taxes forever" — glosses over a gauntlet that can cost hundreds of thousands of dollars if approached carelessly.

The key risks: automatic covered expatriate status from a paperwork error, a deemed-sale tax event on appreciated assets, full income-tax treatment of IRA balances, and a new 40% inheritance tax on US-citizen heirs that only became enforceable in January 2025. Each of these is avoidable with planning. None are avoidable if you show up at the consulate without understanding them first.

If you're serious about exploring this path, start with a consultation from a tax attorney who specializes in expatriation — not as a formality, but as the first real step in the process.

Financial disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. Tax laws change frequently, and individual circumstances vary significantly. Consult a qualified international tax attorney and CPA before making any decisions about expatriation, citizenship renunciation, or related tax matters. Nothing here should be construed as a recommendation to renounce or retain US citizenship.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJune 11, 2026

Expat Tax & FinanceJune 11, 2026

US Expatriation Tax: Section 877A Rules Explained

A $2M net worth triggers Section 877A mark-to-market tax on departure. Learn how covered expatriates are taxed and what to plan before you leave.

Expat Tax & FinanceJune 19, 2026

Expat Tax & FinanceJune 19, 2026

IRC 877A: Deemed Sale Rules for Departing Americans

IRC 877A deems all worldwide assets sold before departure. Learn the 2026 exclusion, IRA deemed-distribution rules, and Form 8854 filing deadline.

Expat Tax & FinanceJune 14, 2026

Expat Tax & FinanceJune 14, 2026

US Exit Tax: What Covered Expatriates Actually Owe

The US Exit Tax hits covered expatriates with a deemed sale of all worldwide assets. Learn the 3 tests, the 90K exclusion, IRA traps, and planning