The Expat Investor's Playbook: Build Wealth Abroad Without PFICs

Here's a number that should terrify every American living abroad: if you invest in the wrong fund — even a perfectly reasonable index fund — the IRS...

Here's a number that should terrify every American living abroad: if you invest in the wrong fund — even a perfectly reasonable index fund — the IRS...

Here's a number that should terrify every American living abroad: if you invest in the wrong fund — even a perfectly reasonable index fund — the IRS can tax your gains at effectively 50%.

Not 15%. Not 20%. Fifty percent. Sometimes more.

It's called the PFIC trap, and it destroys expat portfolios every single year. The worst part? Most expats don't find out until they file their taxes and their accountant delivers the bad news.

Related: Roth IRA expat guide

I've watched smart, financially literate Americans move abroad, keep investing through their local bank (seems logical, right?), and then get absolutely hammered when the IRS classifies every foreign-domiciled fund as a "Passive Foreign Investment Company." Suddenly that sensible European index fund triggers a tax rate that would make a Wall Street hedge fund manager wince.

But here's the thing — this is entirely avoidable. With the right brokerage, the right fund selection, and a basic understanding of how US tax law treats overseas investors, you can build a seven-figure portfolio from anywhere in the world while paying less in taxes than you would back in the States.

This is the guide I wish existed when I started investing from abroad. Every strategy, every brokerage option, every tax trap — laid out so you can build real wealth without the IRS taking half of it.

Why Investing as an Expat Is Fundamentally Different

If you're a US citizen living abroad, you exist in a financial no-man's-land that most investment advice completely ignores.

Stateside financial advisors don't understand the PFIC rules, the FBAR implications, or the FATCA reporting requirements. Foreign financial advisors don't understand why you can't just open a local brokerage account like everyone else. And the internet is full of generic "just buy index funds" advice that's technically correct but practically dangerous if you buy the wrong index funds.

Here's what makes expat investing uniquely challenging:

- US brokerages may freeze your account when you update your address to a foreign country. Fidelity, Vanguard, and TD Ameritrade have all been known to restrict accounts for overseas residents.

- Foreign brokerages create tax nightmares. Any fund registered outside the US is likely a PFIC, triggering punitive taxation.

- You're taxed on worldwide income regardless of where you live. The US is one of only two countries (along with Eritrea) that taxes citizens on global income.

- FATCA means your foreign bank reports your balances to the IRS. Over 300,000 foreign financial institutions now report American account holders' data.

- The FEIE ($132,900 in 2026) only covers earned income — not dividends, capital gains, or interest. Your investment returns are always taxable.

If you haven't already, read our complete guide to US expat banking and taxes for the full picture on FBAR, FATCA, and FEIE. What follows here is specifically about how to invest without getting wrecked.

The PFIC Trap: The #1 Portfolio Killer for Americans Abroad

This is the single most important concept for any American investing overseas. Get this wrong, and everything else becomes irrelevant.

What Is a PFIC?

A Passive Foreign Investment Company (PFIC) is any foreign corporation where either:

- 75% or more of gross income is passive (dividends, interest, rents, royalties), OR

- 50% or more of assets produce passive income

In practical terms, virtually every mutual fund, ETF, or investment fund registered outside the United States is a PFIC. That Vanguard fund you bought through your UK brokerage? PFIC. That German index fund your Deutsche Bank advisor recommended? PFIC. That Canadian mutual fund you kept from when you lived in Toronto? PFIC.

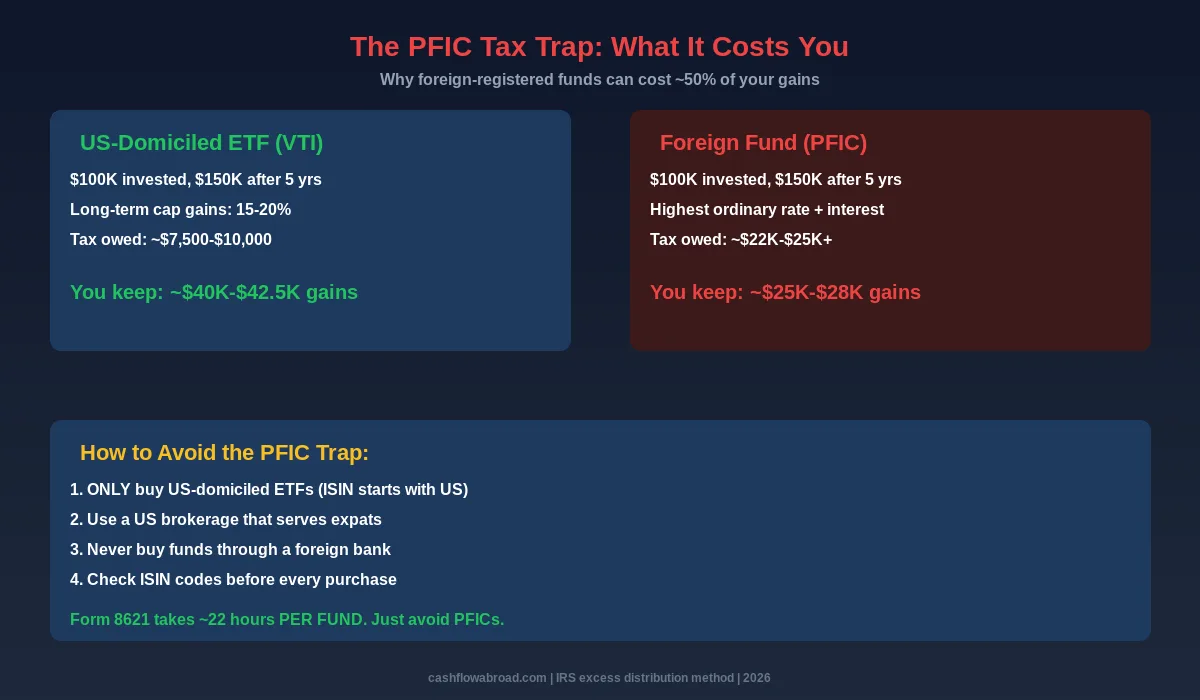

Why PFIC Taxation Is Devastating

Under the default "excess distribution" method, PFIC gains are:

- Allocated across your entire holding period — the IRS pretends you earned the gains equally across every year you held the fund

- Taxed at the highest marginal rate for each year — currently 37% federal, regardless of your actual bracket

- Hit with an interest charge — as if you had underpaid taxes in each prior year

The combined effect? Effective tax rates of 40-50% on your gains, sometimes higher. Compare that to the 15-20% long-term capital gains rate you'd pay on a US-domiciled fund.

The Compliance Nightmare

Even if you could stomach the tax rate, the reporting burden is absurd. Form 8621 (the PFIC reporting form) is required for each PFIC you own. The IRS estimates each form takes approximately 22 hours to complete. Own five foreign funds? That's 110 hours of tax preparation — for investments that are being taxed at punitive rates anyway.

How to Check If a Fund Is a PFIC

The simplest test: check the ISIN (International Securities Identification Number). If it starts with "US," it's a US-domiciled fund and you're safe. If it starts with anything else (IE for Ireland, LU for Luxembourg, GB for the UK), it's almost certainly a PFIC.

| ISIN Prefix | Country | PFIC Risk | Action |

|---|---|---|---|

| US | United States | Safe | Go ahead and invest |

| IE | Ireland | PFIC | Avoid — even Vanguard Ireland funds |

| LU | Luxembourg | PFIC | Avoid — common for European funds |

| GB | United Kingdom | PFIC | Avoid — includes UK ISA funds |

| CA | Canada | PFIC | Avoid — Canadian mutual funds included |

| KY | Cayman Islands | PFIC | Avoid — common for hedge funds |

The Best Brokerages for US Expats in 2026

Your brokerage choice is make-or-break. Pick the wrong one and you'll either lose access to your account, get locked out of trading, or be pushed into PFIC territory. Here are the options that actually work.

1. Interactive Brokers — The Gold Standard

If I had to recommend one brokerage for US expats, it's Interactive Brokers (IBKR). They operate in over 150 countries, offer access to 150+ global markets, charge as little as $0 commissions on US stocks, and they actually welcome expat clients.

Pros:

- Available in virtually every country

- Access to US-domiciled ETFs (avoiding PFICs)

- Multi-currency accounts — hold and trade in 27 currencies

- Margin rates starting at 5.33%

- Full suite: stocks, options, futures, bonds, forex

- IRA accounts available for US citizens abroad

Cons:

- Interface isn't beginner-friendly (Trader Workstation is built for pros)

- $0 inactivity fee was only removed recently — check current terms

- Customer service can be hit or miss

Best for: Serious investors who want full market access from any country.

2. Charles Schwab International

Schwab expanded their expat-eligible countries significantly and now serves US citizens in 30+ countries. Their international account is designed specifically for Americans living overseas.

Pros:

- Zero-commission US stock and ETF trades

- Strong research and educational resources

- US-based customer service that understands expat needs

- Easy account opening process for overseas Americans

- Checking account with no foreign ATM fees worldwide

Cons:

- Not available in every country (check eligibility)

- More limited product range than IBKR

- No options trading in some expat accounts

Best for: Buy-and-hold investors who want a straightforward, reliable platform with integrated banking — the Schwab Visa debit card with unlimited worldwide ATM fee rebates is a game-changer for expats who need to access cash in local currency.

👉 Open a Schwab International Account

3. tastytrade — For the Active Trader

If you're trading options, futures, or commodities from abroad, tastytrade deserves serious consideration. Their platform is built for active traders with some of the lowest options commissions in the industry ($1.00 per contract to open, $0 to close).

We covered tastytrade extensively in our silver and commodity trading guide — if you're trading Section 1256 contracts with the 60/40 tax advantage, this is where you want to be.

Caveat: tastytrade's expat eligibility varies by country. Check their current country list before applying.

4. SoFi Invest — For Maintaining a US Footprint

If you maintain a US address (many expats do for banking purposes), SoFi offers a solid all-in-one platform with automated investing, individual stock trading, and banking — all with zero commissions. Their automated portfolios make it easy to stay invested without active management.

Keep in mind: SoFi is designed for US-based customers. If you update your address internationally, access may be restricted. Many expats maintain a US address specifically for platforms like this.

5. ARQ Finance — Stablecoin-Powered Dollar Access for Latin America

If you live in Latin America, ARQ Finance (formerly DolarApp) gives you dollar and euro access through stablecoins. Your balance is held in USDc and EURc — Circle-issued stablecoins pegged 1:1 to real dollars and euros. You can deposit USDC or USDT from any external wallet (Ethereum, Polygon, or Tron), swap stablecoins to local currency (MXN, COP, ARS, BRL) at real market rates, and withdraw to your local bank instantly. On top of that, you earn up to 4% APY on USDc balances, get a Mastercard with up to 4% cashback, and can invest in stocks and ETFs. Available in Mexico, Colombia, Argentina, and Brazil.

Best for: Expats and remote workers in Latin America who want stable-currency accounts, stablecoin on/off ramps, and yield on dollar holdings — all without a US bank account.

What to Actually Invest In (And What to Avoid)

The Core Portfolio: US-Domiciled ETFs

The safest, most tax-efficient approach for US expats is building a portfolio entirely from US-domiciled ETFs. These trade on US exchanges, have ISINs starting with "US," and are never classified as PFICs.

| Asset Class | ETF | Expense Ratio | Why It Works for Expats |

|---|---|---|---|

| US Total Market | VTI | 0.03% | Broadest US exposure, ultra-low cost |

| International (ex-US) | VXUS | 0.07% | Global diversification WITHOUT PFIC risk |

| US Bonds | BND | 0.03% | Stability, income, all US-domiciled |

| Emerging Markets | VWO | 0.08% | LATAM, Asia exposure via US ETF |

| REITs | VNQ | 0.12% | Real estate exposure without buying property |

| S&P 500 | VOO | 0.03% | Large-cap US, legendary track record |

The critical insight: You can get full global diversification — US stocks, international stocks, emerging markets, bonds, real estate — using only US-domiciled ETFs. There is zero reason to buy a foreign fund. Vanguard's VXUS gives you international stock exposure through a US-registered ETF. Same global diversification, zero PFIC risk.

What to Avoid Like the Plague

- Any fund your foreign bank recommends. They don't know (or care) about PFIC rules.

- Irish-domiciled ETFs (iShares, Vanguard Ireland). These are optimized for European investors' withholding tax treaties, not for Americans.

- UK ISA accounts. Tax-free for UK residents, PFIC nightmare for Americans.

- Foreign robo-advisors. Nutmeg, Wealthsimple (Canadian version), etc. All use foreign-domiciled funds.

- Offshore insurance wrappers. Isle of Man, Gibraltar products sold to expats. Complex, expensive, and PFIC city.

Tax-Advantaged Accounts That Work from Abroad

Just because you live overseas doesn't mean you lose access to tax-advantaged retirement accounts. But there are important nuances.

Related: expat 401k and IRA guide

Traditional and Roth IRAs

You can contribute to IRAs from abroad, but there's a catch: you need taxable compensation, and the FEIE can wipe it out.

If you exclude all your earned income under the Foreign Earned Income Exclusion ($132,900 in 2026), you technically have zero "taxable compensation" — which means zero IRA contribution eligibility. The workaround? Exclude slightly less than your full income, leaving enough taxable earned income to justify IRA contributions ($7,000 limit in 2026, $8,000 if 50+).

For the complete FEIE breakdown, see our step-by-step FEIE guide.

SEP-IRA for Self-Employed Expats

If you're running your own business abroad (and many of our readers are — see our guide to building a $100K online business from anywhere), the SEP-IRA is a powerhouse. You can contribute up to $70,000 in 2026 — significantly more than a traditional IRA.

The key: contributions are based on net self-employment income after the FEIE exclusion. If you earn $180,000 and exclude $132,900 under FEIE, you have $47,100 in taxable self-employment income that can fuel SEP-IRA contributions.

Solo 401(k)

For self-employed expats, the Solo 401(k) offers even more flexibility than a SEP-IRA — including Roth contributions and loan provisions. Combined employer/employee contribution limits reach $70,000 in 2026 ($77,500 if 50+).

Why the FEIE Doesn't Cover Investment Income (And What to Do About It)

This trips up so many expats. You file your FEIE, exclude your earned income, maybe even reduce your federal tax bill to zero — and then assume your investments are covered too.

They're not.

The Foreign Earned Income Exclusion only covers earned income — salary, wages, self-employment income. Investment income — dividends, capital gains, interest, rental income — is always taxable regardless of where you live.

This is why tax-efficient investing matters even more for expats. Strategies that minimize taxable events:

- Favor growth over dividends. Total market ETFs (VTI) over high-dividend ETFs (VYM) means fewer taxable distributions.

- Use tax-loss harvesting. Sell losers to offset winners. This works the same from abroad.

- Maximize retirement accounts. SEP-IRA and Solo 401(k) contributions shelter income from taxes.

- Hold for long-term gains. The 15-20% long-term capital gains rate beats the 37% short-term rate.

- Consider the Foreign Tax Credit. If your country of residence taxes investment income, you may be able to credit that against your US tax liability — avoiding double taxation.

We covered the FEIE vs. FTC decision in depth in our expat banking and taxes guide. For most expat investors, using the FTC on investment income while using the FEIE on earned income is the optimal strategy.

The Crypto Allocation Question

Should crypto be part of your expat portfolio? For many location-independent investors, the answer is a qualified yes — but the size and approach matter.

Crypto offers something uniquely valuable to expats: it's truly portable. No bank can freeze it because you moved countries. No brokerage can restrict access based on your residence. Your Bitcoin doesn't care whether you're in Medellín, Bangkok, or Lisbon.

That said, the IRS treats crypto as property, and every sale, trade, or exchange is a taxable event. We covered the full crypto tax picture in our crypto and taxes guide for US expats. Use a tool like CoinTracking to automate the reporting — it imports from every major exchange and generates IRS-ready forms.

For portfolio allocation, consider:

- 5-10% allocation for moderate risk tolerance

- Bitcoin and Ethereum as core holdings (not memecoins)

- Use a reputable exchange — Kraken operates in 190+ countries and has proven reliability for expat investors. They offer staking, futures, and a solid mobile app.

- Self-custody for long-term holdings — hardware wallets (Ledger, Trezor) for anything you're holding more than a year

- Don't forget FBAR reporting — foreign exchange accounts over $10,000 may need reporting

Managing Your Business Treasury from Abroad

If you're running a US business while living overseas (as many readers of our guide to running a US business from Colombia are doing), your business treasury needs a home.

Mercury has become the go-to banking platform for location-independent entrepreneurs. Here's why it matters for investing:

- Treasury accounts earning 4%+ APY on idle business cash

- No foreign address restrictions — Mercury serves US-entity businesses regardless of where the founder lives

- API integrations for automated bookkeeping (critical for FBAR and FATCA compliance)

- FDIC-insured through partner banks, up to $5M with sweep accounts

Keep your business treasury separate from your personal investment portfolio. Business cash should be liquid and safe. Personal investments are where you take calculated risks for growth.

Three Expat Portfolio Models

Here are three portfolio frameworks depending on your risk tolerance and situation. All use only US-domiciled funds to avoid PFICs.

Model 1: The Conservative Expat (Capital Preservation)

Best for: Retirees abroad, people living on savings, those within 5 years of retirement

| Allocation | ETF | Percentage |

|---|---|---|

| US Bonds | BND | 40% |

| US Total Market | VTI | 30% |

| International | VXUS | 15% |

| TIPS (Inflation) | VTIP | 10% |

| Cash / Money Market | SGOV | 5% |

If you're already retired abroad and stretching Social Security, our guide to countries where Social Security goes 5x further pairs perfectly with this conservative approach.

Model 2: The Balanced Builder (Growth + Stability)

Best for: Mid-career expats, dual-income households, 10+ year time horizon

| Allocation | ETF | Percentage |

|---|---|---|

| US Total Market | VTI | 40% |

| International | VXUS | 20% |

| US Bonds | BND | 15% |

| Emerging Markets | VWO | 10% |

| REITs | VNQ | 10% |

| Crypto (BTC/ETH) | — | 5% |

Model 3: The Aggressive Nomad (Maximum Growth)

Best for: Young expats (20s-30s), high earners with no dependents, 15+ year horizon, high risk tolerance

| Allocation | ETF | Percentage |

|---|---|---|

| US Total Market | VTI | 45% |

| International | VXUS | 20% |

| Emerging Markets | VWO | 15% |

| Crypto (BTC/ETH) | — | 10% |

| Options/Commodities | — | 10% |

For the options and commodities slice, tastytrade remains my top pick for Section 1256 contracts — the 60/40 tax treatment (60% long-term, 40% short-term regardless of holding period) is a genuine edge. We broke down the full strategy in our commodity trading from abroad guide.

Protecting Your Financial Life from Anywhere

When you're managing a six- or seven-figure portfolio from a café in Medellín or a coworking space in Lisbon, security isn't optional — it's existential.

Digital Security Essentials

- VPN for financial transactions: Always use a VPN when accessing brokerage accounts on public WiFi. NordVPN is what I use — they have servers in 60+ countries and a strict no-logs policy. This isn't just about privacy; some brokerages will flag or freeze accounts that log in from unexpected foreign IP addresses.

- Hardware security keys (YubiKey) for two-factor authentication on brokerage accounts

- Dedicated email for financial accounts — not the same one you use for newsletters and social media

- Password manager with unique, random passwords for every financial platform

Health Insurance: The Overlooked Investment

This isn't directly an investment strategy, but medical bankruptcy can destroy any portfolio. If you're living abroad without employer-sponsored coverage, you need a plan.

SafetyWing offers global health insurance starting at around $120/month — covering 185+ countries with no deductible for doctor visits. We did a deep comparison in our expat health insurance guide. The point is: protecting your health protects your wealth.

Colombia-Specific Note

If you're based in Colombia (or considering it), our sister site ColombiaMove.com covers the banking landscape in detail — including the best banks for foreigners in 2026 and how the local healthcare system works. For cost of living specifics, their Medellín budget breakdown is worth bookmarking.

Your 30-Day Expat Investor Action Plan

Stop reading and start doing. Here's exactly what to do in the next 30 days:

Week 1: Audit and Account Setup

- Audit your current holdings. Check every ISIN. If anything doesn't start with "US," you need a plan to exit those positions.

- Open an Interactive Brokers or Schwab International account. Applications take 1-3 business days to process.

- Set up a VPN. Get NordVPN configured on all your devices before you start moving money.

Week 2: Portfolio Construction

- Choose your portfolio model (Conservative, Balanced, or Aggressive) based on your age, risk tolerance, and time horizon.

- Fund your account and make your first purchases — VTI, VXUS, and BND are the core three.

- Set up automatic contributions if your brokerage supports it.

Week 3: Tax Optimization

- Evaluate FEIE vs. FTC for your specific situation (or use both strategically).

- Open a SEP-IRA or Solo 401(k) if you're self-employed.

- Set up a system for tracking cost basis — you'll need this for capital gains calculations.

Week 4: Protection and Automation

- Enable 2FA on every financial account (preferably hardware key, not SMS).

- Set up FBAR tracking — note all foreign accounts with balances exceeding $10,000 at any point during the year.

- Review your health insurance — check SafetyWing if you need global coverage.

- Build passive income streams alongside your portfolio — check our guide to passive income that works from any country.

The Bottom Line

Investing as a US expat isn't harder than investing at home — it's just different. The rules are different. The traps are different. The opportunities are different.

The Americans who build real wealth abroad are the ones who understand three things:

- Avoid PFICs at all costs. Stick to US-domiciled ETFs. Check the ISIN. Always.

- Use the right brokerage. Interactive Brokers and Schwab International actually want your business.

- Stack tax advantages. FEIE for earned income, FTC for investment income, SEP-IRA for retirement savings, Section 1256 for commodities. Each tool has a purpose.

The geographic arbitrage advantage — earning in strong currencies while living in low-cost countries — is the greatest wealth-building accelerator most Americans never discover. If you're already living abroad (or planning to), you're ahead of the game. Now make your money work as hard as you do.

If you're considering Colombia as your base, our sister site ColombiaMove.com has everything you need — from the digital nomad visa guide to the complete moving checklist. And if you want a plug-and-play relocation plan, grab our Colombia Relocation Kit on Gumroad.

What's your biggest investing challenge as an expat? Drop a comment below — I read every one and respond to questions about brokerage selection, PFIC avoidance, and tax strategy. And if you found this guide useful, share it with another expat who's probably investing in the wrong funds right now. They'll thank you later.

Want more content like this? We publish deep-dive guides on expat finance, geographic arbitrage, and building wealth from anywhere. Bookmark this site and check back — or follow us for updates.

Disclaimer: This article contains affiliate links. If you sign up through our links, we may earn a commission at no extra cost to you. We only recommend products and services we personally use or have thoroughly researched. This content is for informational purposes only and should not be considered financial, tax, or legal advice. Consult a qualified professional for advice specific to your situation.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Investing & Wealth BuildingJune 17, 2026

Investing & Wealth BuildingJune 17, 2026

Interactive Brokers for US Expats: What You Need to Know

IBKR accepts US citizens in 200+ countries. Learn which entity to choose, FBAR rules, and which investments trigger PFIC penalties when living abroad.

Investing & Wealth BuildingJuly 3, 2026

Investing & Wealth BuildingJuly 3, 2026

REITs for US Expats: Income, Tax Rules, and PFIC Traps

US expats can earn 4%+ REIT yields at a 29.6% effective rate with the permanent Section 199A deduction. Know which funds are PFICs and which are not.

Investing & Wealth BuildingJune 12, 2026

Investing & Wealth BuildingJune 12, 2026

Best Expat Brokerage: IBKR vs Schwab Compared

IBKR offers multi-currency accounts and 150+ exchanges; Schwab gives free worldwide ATM access. Which is better for US expats investing abroad?