An estimated 9 million Americans live outside the United States. Fewer than 2 million file US expat tax returns each year. That gap doesn't mean the rest are exempt — it means millions of people are quietly racking up exposure to penalties they don't know exist.

FBAR and FATCA are two separate foreign account reporting requirements that trip up even financially sophisticated expats. They have different thresholds, different forms, different filing agencies, and wildly different penalties. Miss one — or both — and the IRS doesn't send a gentle reminder. It sends a penalty notice.

Here's the complete breakdown of what you actually need to file, when, and what happens if you don't.

What Is FBAR — And Why It Has Nothing to Do With Your Tax Return

FBAR stands for Report of Foreign Bank and Financial Accounts. It's filed on FinCEN Form 114 with the Financial Crimes Enforcement Network — a bureau of the US Treasury Department, not the IRS. That distinction matters: your accountant can file your tax return perfectly and still miss your FBAR if they don't specifically ask about foreign accounts.

The rule is blunt: if you are a US person (citizen, green card holder, or resident alien) and you have a financial interest in or signature authority over foreign financial accounts totaling more than $10,000 at any point during the calendar year, you must file an FBAR.

Note what that says: at any point. This isn't an end-of-year balance — it's a peak balance threshold. Wire $15,000 to a foreign account in January, spend it down to $3,000 by December, and you still triggered the filing requirement in January. The rule catches people constantly.

The $10,000 threshold is also aggregate across all foreign accounts. Five accounts with $3,000 each totals $15,000 — all five must be reported.

What Counts as a Foreign Account

- Foreign bank checking and savings accounts

- Foreign brokerage and investment accounts

- Foreign mutual funds

- Foreign pension and retirement funds (in most cases)

- Foreign insurance policies with a cash surrender value

- Accounts you have signature authority over, even if you don't own them (e.g., your employer's foreign account if you're a signatory)

How to Actually File the FBAR

FinCEN Form 114 is filed electronically through the BSA E-Filing System. It cannot be filed on paper. Most expat tax software and accountants handle this as part of the standard service — but verify, because it's not automatic.

Deadline: April 15, with an automatic extension to October 15. No request is needed — you don't file an extension form. If you miss April 15, you're still fine through October 15.

The FBAR reports the maximum value held in each account during the year, the account number, and the name and address of the foreign bank. It's an information return — you're not paying taxes on what you report. You're just telling FinCEN the money exists.

What Is FATCA — The IRS's Global Surveillance Network

FATCA stands for the Foreign Account Tax Compliance Act, passed in 2010. While FBAR is about telling FinCEN you have accounts, FATCA is about telling the IRS what those accounts are worth — and it's backed by a global data-sharing infrastructure that now covers over 110 countries and 300,000 foreign financial institutions.

Every major bank in the UK, Germany, Singapore, Mexico, Colombia, Australia, and most of the developed world is now required to report US account holders' balances directly to the IRS. That means the IRS often knows your foreign account exists before you file. FATCA just makes sure you confirm it.

The taxpayer-side of FATCA compliance is Form 8938 (Statement of Specified Foreign Financial Assets), filed with your regular tax return (Form 1040).

Form 8938 Thresholds: Much Higher Than FBAR

Unlike FBAR's $10,000 threshold, Form 8938 has much higher reporting thresholds — and they differ depending on where you live:

| Filing Status | Living Abroad — Year-End Balance | Living Abroad — Peak Balance | US Resident — Year-End | US Resident — Peak |

|---|---|---|---|---|

| Single / MFS | $200,000 | $300,000 | $50,000 | $75,000 |

| Married Filing Jointly | $400,000 | $600,000 | $100,000 | $150,000 |

Most expats with one or two foreign bank accounts won't hit Form 8938 thresholds. But if you have a foreign investment portfolio, foreign pension, or property held through a foreign entity — the numbers add up quickly.

FATCA covers a broader set of assets than FBAR. It includes foreign partnership interests, foreign trusts, foreign stock and securities held directly (not through a US custodian), and interests in foreign pension plans and deferred compensation plans. This means your foreign rental property held through a Colombian S.A.S. or a Panamanian foundation may be reportable on 8938 but not on FBAR.

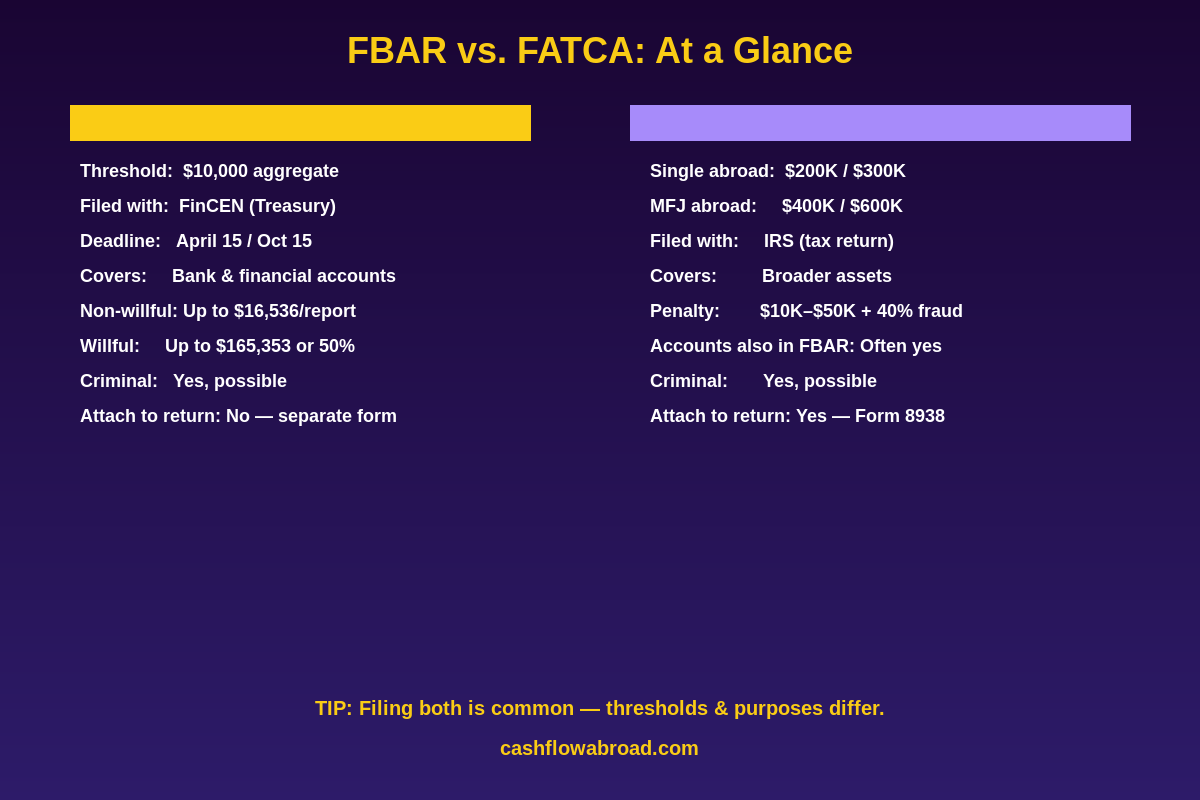

FBAR vs. FATCA: The Key Differences

| Feature | FBAR (FinCEN 114) | FATCA (Form 8938) |

|---|---|---|

| Filed with | FinCEN (Treasury) | IRS (attached to 1040) |

| Threshold (single, abroad) | $10,000 aggregate | $200K year-end / $300K peak |

| Deadline | April 15 (auto Oct 15) | Same as tax return |

| Covers | Bank and financial accounts | Broader — includes foreign entities, pensions, stock held directly |

| Non-willful penalty | Up to $16,536 per annual report | $10,000 initial + $10K/30 days (max $50K) |

| Willful penalty | $165,353 or 50% of balance | 40% penalty on unreported amounts |

| Criminal exposure | Yes | Yes |

| Statute of limitations | 6 years | 6 years (unlimited if >25% income omitted) |

An important point: filing both is common. The forms overlap in some accounts but not others. An account reported on FBAR is often also reportable on Form 8938 (if you hit the thresholds), but Form 8938 can cover assets that don't appear on FBAR at all. Don't assume filing one covers the other — it doesn't.

The Real Penalty Picture — Including the Supreme Court Win

The penalty structure for FBAR used to be brutal. The IRS's position was that non-willful penalties applied per account, per year — meaning 10 accounts over 5 years of non-filing could mean 50 separate penalty charges at up to $10,000 each. The government tried to hit one taxpayer, Alexandru Bittner, with $2.72 million in non-willful penalties across 61 accounts held over five years.

In February 2023, the Supreme Court ruled 5-4 in Bittner v. United States that non-willful FBAR penalties apply on a per-form basis — one penalty per annual report, regardless of how many accounts are included. Bittner's liability dropped from $2.72 million to roughly $50,000–$60,000. That's still significant, but the ruling ended the IRS's strategy of weaponizing multi-account penalties against people who simply didn't know the rules.

Current penalty structure, adjusted for inflation:

- Non-willful FBAR violation: Up to $16,536 per annual report

- Willful FBAR violation: The greater of $165,353 or 50% of the account's highest balance during the year — per account, per year. This one is still devastating.

- Criminal FBAR: Up to $250,000 fine and 5 years in prison for willful violations

- FATCA (Form 8938) non-filing: $10,000 initial penalty, then $10,000 for each 30-day period after IRS notice — capped at $50,000

- FATCA underpayment: 40% accuracy-related penalty on underpayments tied to undisclosed foreign assets

The line between willful and non-willful is everything. Willful means you knew about the requirement and intentionally ignored it. Non-willful means you didn't know or made a mistake. If you've been reading this and haven't filed, you are now informed — act before that classification changes.

How to Catch Up If You've Never Filed

The IRS has formal catch-up programs for people who didn't know about these requirements. The key is acting before the IRS contacts you — once they reach out first, your options narrow significantly.

Streamlined Filing Compliance Procedures

The IRS's Streamlined Compliance Procedures are the standard solution for non-willful non-filers. Two tracks:

Streamlined Foreign Offshore Procedure (SFOP) — for expats who meet the physical presence or bona fide residence test:

- File 3 years of amended or delinquent tax returns

- File 6 years of FBARs

- Pay any taxes and interest owed

- Zero percent offshore penalty — this is as close to amnesty as the IRS offers

Streamlined Domestic Offshore Procedure (SDOP) — for US residents who should have been reporting:

- Same return and FBAR filing requirements

- Pay a 5% miscellaneous offshore penalty on the highest aggregate balance of unreported accounts

For most expats, the SFOP is essentially a penalty-free amnesty — you catch up, pay taxes owed (often zero if you're using the FEIE or foreign tax credits — see the full FEIE breakdown), and move forward with a clean slate.

Delinquent FBAR Submission Procedures

If you have no unreported income — just unfiled FBARs — you may qualify for the Delinquent FBAR Submission Procedures. File the late FBARs with an explanation of why you didn't file. When there's no unreported income and no prior IRS contact, penalties are generally not imposed. Many expats who use local accounts purely for living expenses (no income flowing through them) qualify here and walk away with no penalty at all.

What Doesn't Trigger FBAR Filing

Not every foreign-adjacent account requires an FBAR:

- US military banking facilities abroad

- Accounts held at US branches of foreign banks (those are US accounts)

- Accounts in US territories like Puerto Rico and Guam (with US-chartered institutions)

- IRAs — you don't report the IRA itself on FBAR, though foreign assets inside it may be a different story

- Correspondent or nostro accounts

Foreign pension treatment is one of the more complicated areas. Some foreign pension plans are exempt based on tax treaties; others must be reported. The UK-US treaty provides specific treatment for UK pension schemes; other countries have no such protection. This is where a qualified expat tax professional earns their fee — the wrong call here can mean a missed filing or an unnecessary one.

Getting Your Account Stack Right as an Expat

The practical approach: keep your core financial life in the US with institutions that support expats. Charles Schwab International is the standard recommendation — no foreign transaction fees, free ATM withdrawals globally, no account minimums, and they don't close accounts when you move abroad. Their brokerage is also one of the few that actively supports expat clients (detailed in the expat brokerage guide).

For business banking with strong international wire capability, Mercury is a solid option — no fees, great ACH and wire support, and no complaints about foreign IP addresses.

If you need a physical US address for IRS correspondence, banking, or state domicile purposes, Traveling Mailbox is the practical solution — a real US street address in 50+ cities, mail scanning, and check deposit capability for $15/month. Essential for anyone maintaining US banking ties while abroad. See the full virtual mailbox guide for the full breakdown.

For moving money internationally, Remitly offers competitive rates without the spread that banks quietly take on wire transfers.

The 5 Most Common FBAR/FATCA Mistakes

- Missing signature authority accounts. If you can control a foreign account — even if you don't own it — you may need to report it. US employees with signing authority on a company's overseas operating account overlook this constantly.

- Using year-end balance instead of peak balance. FBAR triggers on the highest balance at any point during the year, not what's there on December 31.

- Assuming FBAR covers FATCA. Two separate forms, two separate agencies. Filing one doesn't satisfy the other.

- Not reporting foreign pensions. Mandatory pension contributions like CPF (Singapore), IMSS (Mexico), or Superannuation (Australia) often require reporting under FBAR and sometimes Form 8938, depending on treaty provisions.

- Filing late without using the formal catch-up programs. A late FBAR filed ad hoc — without a reasonable cause statement or a formal procedure — can trigger penalties even for non-willful failures. Use the Streamlined or Delinquent procedures, not a wing-and-a-prayer amended filing.

Record-Keeping: What to Keep and How Long

FBAR statute of limitations: 6 years from the filing deadline. A 2019 tax year FBAR was due October 15, 2020 — the government generally has until 2026 to assess penalties on it. For FATCA/Form 8938, it's also 6 years, but unlimited if you omit more than 25% of gross income.

Keep these for at least 7 years:

- Foreign account statements showing monthly and year-end balances

- Account opening and closing dates

- Copies of all filed FBARs and Form 8938s with confirmation receipts

- Any correspondence with foreign banks or financial institutions

For the broader picture on what the IRS knows about your foreign income and how global data sharing has changed enforcement, the post on CARF and global data sharing covers the surveillance architecture in detail.

The Bottom Line

FBAR and FATCA are not going away — if anything, enforcement is increasing as FATCA's data-sharing network matures. With 110+ countries automatically feeding US account holder data to the IRS, the gap between what you report and what they know is shrinking every year.

The good news: if you've been non-compliant through ignorance rather than intent, the catch-up path is genuinely reasonable. The Streamlined Foreign Offshore Procedure offers a near-penalty-free way to get current. The window for using it closes the moment the IRS initiates contact. Act first.

Next reads: the complete expat banking and taxes guide covers the full picture, and the FEIE vs. foreign tax credit breakdown will show you how to calculate what, if anything, you actually owe after catching up.

Financial disclaimer: This article is for informational purposes only and does not constitute legal or tax advice. FBAR and FATCA rules are complex and situation-specific. Consult a qualified expat tax attorney or CPA before taking any action on foreign account reporting or compliance procedures.