Phantom Gains: The Hidden Tax on Foreign Property Sales

You sold your Spanish apartment for the exact same price you paid for it — €215,000 in, €215,000 out. Zero profit in euros.

You sold your Spanish apartment for the exact same price you paid for it — €215,000 in, €215,000 out. Zero profit in euros.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

You sold your Spanish apartment for the exact same price you paid for it — €215,000 in, €215,000 out. Zero profit in euros. Your Spanish neighbors pay zero capital gains tax. You get a letter from the IRS saying you owe $11,400.

Welcome to phantom gains — the most misunderstood (and most expensive) tax trap in the expat world. Because the United States taxes based on citizenship, not residence, every foreign property transaction runs through a dollar conversion. The IRS doesn't care what happened in euros, pounds, or pesos. It cares what happened in USD — and the difference between those two realities can be enormous.

This guide breaks down exactly how US tax applies when you sell property abroad, when you sell your US home from abroad, and what you can do to minimize the damage before you sign the papers.

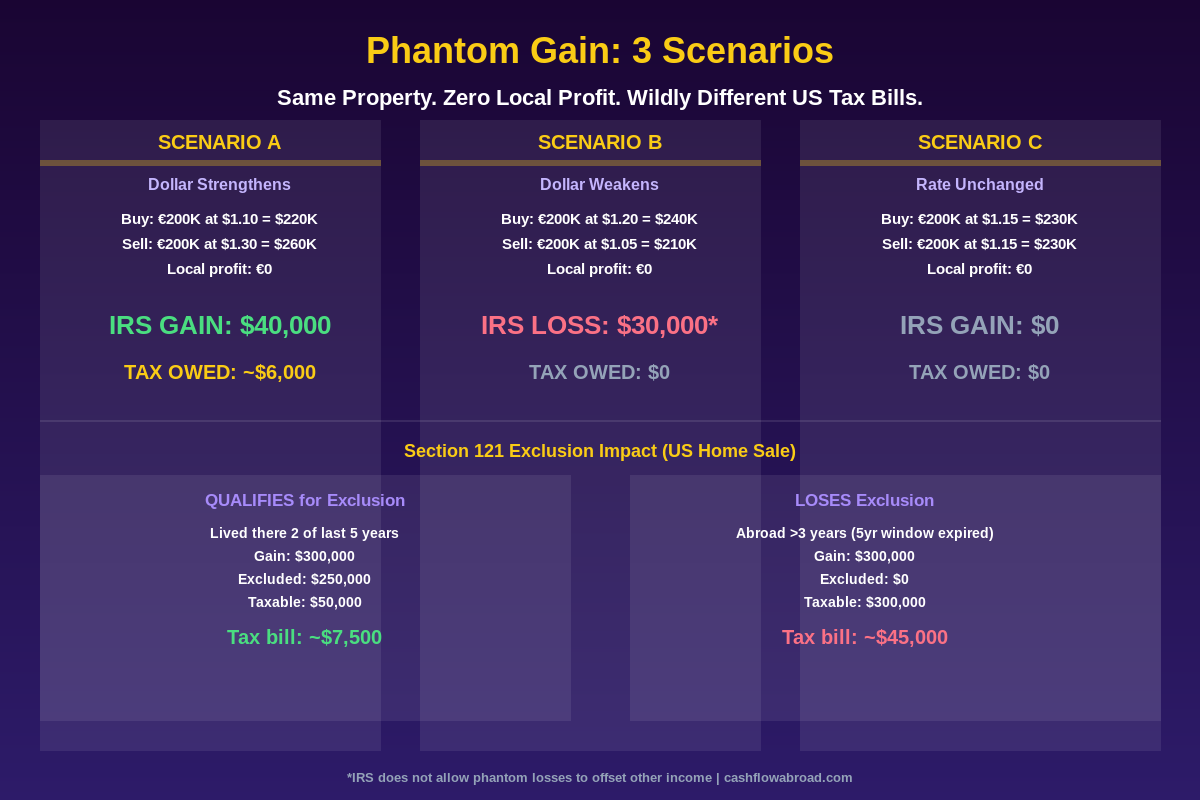

Why the IRS Sees Profit You Never Made

The core problem is simple: the US requires you to report all gains in US dollars, using the spot exchange rate on the date of each transaction. Buy in one exchange rate environment, sell in another, and a currency shift creates a "gain" that exists only on paper — in a currency you may not even hold.

A concrete example:

- You buy a French apartment in 2018: €200,000 at $1.18/€ → cost basis $236,000

- You sell in 2024: €200,000 at $1.30/€ → sale proceeds $260,000

- Local gain: €0

- IRS gain: $24,000 — taxed at long-term capital gains rates (up to 20%)

At the 15% long-term rate, that phantom gain costs you $3,600 in real money on a sale where you earned nothing. Flip it: if the dollar strengthened since you bought, you might have a USD loss on a local break-even — but as we'll get to shortly, the IRS handles gains and losses asymmetrically.

The Asymmetry That Makes This Worse

The IRS taxes phantom gains but largely does not give you the mirror benefit on phantom losses. If dollar strengthening reduces your converted proceeds below your converted basis, you technically have a capital loss — but that loss can only offset other capital gains. It cannot reduce your W-2, your self-employment income, or your rental income. If you have no gains to offset in that year, the loss carries forward and you chip off $3,000/year against ordinary income indefinitely.

Meanwhile, a phantom gain is fully taxable in the year of sale. The asymmetry is real and one-sided.

The Holding Period Math

Same rules apply as US property. Hold more than 12 months → long-term capital gains rates (0%, 15%, or 20% federally). Hold 12 months or less → short-term, taxed as ordinary income up to 37%.

For 2025 income (filed in 2026), the long-term rate thresholds are:

| Filing Status | 0% Rate Up To | 15% Rate Up To | 20% Above |

|---|---|---|---|

| Single | $48,350 | $533,400 | $533,400+ |

| Married Filing Jointly | $96,700 | $600,050 | $600,050+ |

One thing expats frequently get wrong: the Foreign Earned Income Exclusion shields earned income (wages, freelance, self-employment) — it does nothing for capital gains or rental income. If you're using FEIE and excluding $120,000 in salary, your property gain is still taxed in full. The FEIE is also "stacked" against capital gains for rate purposes, meaning it can push your gains into higher brackets even though you excluded the income underneath it.

The Section 988 Trap: Foreign Currency Mortgages

If you financed the foreign property with a local mortgage, you're dealing with a second layer of phantom gain under IRC Section 988. The IRS treats a foreign-currency debt as a separate financial position from the property itself — effectively a currency trade.

Here's how it bites: you take out a €150,000 mortgage when the euro is at $1.25/€ (dollar liability: $187,500). By the time you sell and pay off the mortgage, the dollar has strengthened to $1.08/€. Your remaining €100,000 balance only costs $108,000 to discharge — saving you $17,500 in dollar terms. The IRS taxes that $17,500 savings as ordinary income under Section 988, not a capital gain. It doesn't get the preferential long-term rate. At a 32% marginal rate, that's $5,600 of additional tax on a currency move that had nothing to do with your property's performance.

If the dollar weakens and your mortgage becomes more expensive in dollar terms, you get a Section 988 loss that can offset other ordinary income. But most expats only find out about either calculation at tax time — usually the year they sell.

Selling Your US Home From Abroad: The Section 121 Minefield

This is the big one for expats who still own a home in the States. Section 121 lets you exclude up to $250,000 in capital gains ($500,000 married filing jointly) on the sale of your primary residence — but only if you pass the ownership test (owned 2 of last 5 years) and the use test (lived there 2 of last 5 years).

The years don't need to be consecutive. You can live there year 1 and year 3, rent it out years 2, 4, and 5, and still pass the use test as long as you hit 730 total days of personal use within the 5-year window ending on the sale date.

The expat clock problem: once you've been abroad more than 3 years without returning to live in the property, the 5-year window expires on the use test. You may still pass ownership, but failing use means zero exclusion. The difference between selling at year 2.5 abroad and year 3.5 abroad can be $37,500+ in federal tax on the same property.

| Years Abroad at Sale | Use Test | Gain | Excluded | Taxable Amount | Approx. Federal Tax |

|---|---|---|---|---|---|

| 2 years | Passes | $300,000 | $250,000 | $50,000 | ~$7,500 |

| 3 years | Passes (barely) | $300,000 | $250,000 | $50,000 | ~$7,500 |

| 3.5 years | Partial (count days) | $300,000 | $175,000* | $125,000 | ~$18,750 |

| 4+ years | Fails | $300,000 | $0 | $300,000 | ~$45,000 |

*Partial exclusion available when use requirements are partially met.

Non-Qualified Use: How Renting Reduces Your Exclusion

Even if you qualify for the exclusion, renting the home before you sell reduces what you can exclude. Any period after January 1, 2009 where the property wasn't your primary residence is "non-qualified use" — and gain is allocated to that period proportionally.

The formula: Gain × (non-qualified use months ÷ total ownership months) = gain that cannot be excluded, even if total gain is under $250K.

Example: 10-year ownership (120 months). Rented 36 months while abroad (30% non-qualified use). Total gain: $220,000. Non-excludable portion: $220,000 × 30% = $66,000. You pay tax on $66,000 even though total gain is well below the $250K exclusion cap.

Depreciation Recapture: The 25% Nobody Escapes

If you rented the US home and took depreciation deductions on Schedule E, those deductions come back to bite at sale. Depreciation recapture is taxed at 25% — no exclusion possible under Section 121, no FTC offset (unless you also paid tax on a rental gain locally, which is rare for a US property). Every dollar of depreciation claimed after May 6, 1997 is "unrecaptured Section 1250 gain" subject to the 25% rate.

A simple example: 5 years of renting, $45,000 in claimed depreciation. At sale, $45,000 of gain is taxed at 25% = $11,250 of tax that cannot be avoided through any exclusion or foreign tax credit strategy. This is the number that surprises expat homeowners most at closing.

The Foreign Tax Credit: Your Best Offset Tool

Most countries tax property gains locally — Spain, France, Germany, Portugal, Mexico, and dozens of others have their own capital gains regimes. When you pay tax locally on the same gain, you claim a Foreign Tax Credit (Form 1116) to offset your US tax dollar for dollar.

This is often the best available defense. Spain taxes non-resident property gains at 19–23%. If Spain takes 19% and the US would charge 15%, your FTC fully wipes out the US liability — you owe nothing additional. If the US rate exceeds the foreign rate (possible in low-tax jurisdictions), you pay only the difference.

Critical nuances:

- Passive basket rules mean FTC from capital gains can only offset US tax on other passive income, not earned income

- Phantom gains have no local tax attached — no FTC to claim, full US tax owed

- You cannot use both FEIE and FTC on the same dollars — the choice between them on rental income and gains should be modeled before the tax year of the sale, not after

The Filing Checklist

Selling foreign property generates obligations beyond your 1040:

- Form 8949 + Schedule D: Report the sale in USD, including cost basis at historical exchange rate and proceeds at sale-date rate

- FBAR (FinCEN 114): If proceeds land in a foreign account that ever exceeds $10,000 during the year — minimum $16,536/year penalty for non-filing

- Form 8938 (FATCA): Applies if foreign financial assets exceed $200K single/$400K married at year-end, or $300K/$600K at any point. Foreign property itself is generally not a specified foreign financial asset, but the bank account holding the proceeds usually is

- Form 4797: Required when a property had rental use — handles depreciation recapture calculation

For the complete FBAR, FATCA, and expat tax filing stack, see our full compliance guide.

Strategies That Actually Work

Time the Sale Before the 3-Year Use Test Cliff

If you're within 3 years of moving abroad and still qualify under the use test, selling before that window expires is the highest-leverage move available. On a home with $300,000 of gain, selling in year 2 abroad vs. year 4 abroad could mean the difference between $7,500 in tax and $45,000. That's $37,500 of pure planning value.

Move Back In Before Selling

If the window has already expired, re-establishing primary residency for two years resets the use test. Non-qualified use from the rental period still reduces the exclusion proportionally — but you recover the basic 2-of-5-year qualification. Often worth it for large gains.

Use a 1031 Exchange on US Rental Properties

Section 1031 lets you defer capital gains indefinitely by rolling proceeds from one US investment property into another. It does not apply to foreign property — you can't exchange a Spanish apartment for a Texas duplex. But if you're selling a US rental while abroad, 1031 defers all gains: you must identify a replacement property within 45 days and close within 180 days of your sale.

Keep a Clean Cost Basis Record from Day One

Your cost basis for a foreign property includes the purchase price, closing costs, capital improvements, and legal fees — all converted to USD at the exchange rate on the day each cost was incurred, not the rate on a single date. Many expats use a blended estimate at tax time; the correct method is transaction-by-transaction. The difference matters when gains are large.

Maintain a US Address for Tax and Financial Continuity

When selling US property from abroad, you need a valid US address for IRS correspondence, escrow documentation, and — critically — keeping brokerage and banking accounts open to receive proceeds. A virtual mailbox like Traveling Mailbox gives you a real US street address in over 50 cities with mail scanning and check deposit capability for $15/month. It's the cleanest way to maintain your IRS address, state domicile, and financial address while actually living abroad. See our full virtual mailbox guide for options and setup.

Use an Expat-Friendly Brokerage for Reinvestment

If you're selling US property and redeploying into US brokerage accounts, don't assume your existing custodian will cooperate. Fidelity and Vanguard are known to restrict or close accounts when they detect foreign addresses. Charles Schwab International is built for Americans abroad: no foreign address restrictions, worldwide ATM fee reimbursement, and full investment account access from any country. For a detailed breakdown of which institutions actually serve expats, see our expat investing guide.

The Bottom Line

Phantom gains are not a planning failure — they're a structural feature of citizenship-based taxation. The only way to avoid them entirely is to sell when exchange rates are in your favor, or to avoid foreign currency transactions altogether. What you can control is the Section 121 math: track your 730-day use count obsessively, model the sale date against the 3-year cliff, account for non-qualified use periods, and know exactly how much depreciation you've claimed. The strategies that work are front-loaded. Once you've signed at closing and the proceeds are in an account somewhere, the tax is fixed. Plan before you sell, not after.

This post is for informational purposes only and does not constitute tax or financial advice. US tax rules for international real property transactions are complex and highly fact-specific. Consult a qualified international tax professional before making any decisions regarding foreign property, capital gains strategy, or expat tax planning.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJuly 29, 2026

Expat Tax & FinanceJuly 29, 2026

Form 4868 vs 2350 for Expats

Compare Form 4868 and Form 2350 for expats, choose the right extension, and protect cash flow before claiming Form 2555.

Expat Tax & FinanceJuly 28, 2026

Expat Tax & FinanceJuly 28, 2026

US Mortgage as an Expat: Document Checklist

Prepare the income, asset, credit, translation, and closing documents lenders ask for when expats apply for a U.S. mortgage.

Expat Tax & FinanceJuly 27, 2026

Expat Tax & FinanceJuly 27, 2026

EU VAT for US Ecommerce Sellers

Learn when U.S. ecommerce sellers need EU VAT, OSS, or IOSS, and fix checkout rules before taxes erase profit margins overseas.