Your 401k Abroad: The Expat Retirement Mistake That Costs $1M

The IRS doesn't send a warning letter. Your 401(k) custodian won't call. Zero. Nada. Thousands of expats don't know this rule.

The IRS doesn't send a warning letter. Your 401(k) custodian won't call. Zero. Nada. Thousands of expats don't know this rule.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Here's a number that will ruin your morning: the average American expat makes a retirement account mistake that costs them between $63,000 and $1,142,000 in lifetime wealth — and most of them never find out until it's far too late to fix it.

The IRS doesn't send a warning letter. Your 401(k) custodian won't call. And most general-purpose financial advisors have no idea that the rules change completely the moment you board a one-way flight out of the country.

Whether you're already living abroad, planning a move, or daydreaming about sipping coffee in Medellín while your portfolio compounds quietly, this guide covers exactly what happens to your 401(k) and IRA when you leave the US — and how to turn the expat tax code into one of the most powerful wealth-building tools available to anyone, anywhere on earth.

Related: Roth IRA expat guide

Let's start with the mistake that's already costing thousands of expats money right now.

The Hidden Rule That Kills Your IRA Contributions Abroad

Most expats who use the Foreign Earned Income Exclusion (FEIE) to eliminate their US tax bill are doing it right — it's one of the most valuable tax breaks in the IRS code. In 2025, the FEIE lets you exclude up to $130,000 of foreign earned income ($132,900 in 2026) from US federal taxation. Zero. Nada.

Here's the trap nobody tells you about: the same FEIE that zeros out your tax bill also zeros out your ability to contribute to an IRA.

The IRS requires you to have taxable earned income equal to or greater than your IRA contribution. If the FEIE has excluded all of your income, you have $0 of taxable earned income on your return — which means you legally cannot contribute a single dollar to a Traditional or Roth IRA that year.

Thousands of expats don't know this rule. They keep contributing anyway. The IRS calls that an excess contribution, and it triggers a 6% annual excise tax on the excess amount until you correct it by withdrawing the excess plus earnings. Leave it uncorrected for three years and you've effectively paid the entire contribution back in penalties. Leave it for ten years and you've paid 60% of the excess in penalties alone — on money that was never supposed to be in the account.

This isn't a gray area. It's the plain text of IRC §219(b)(1). And yet expat tax forums are full of people discovering this mistake years after the fact, scrambling to file amended returns and Form 5329.

The fix: you must choose between FEIE and IRA contributions. If you want to keep contributing to your IRA, you either need to earn income above the FEIE cap ($130,000), use the Foreign Tax Credit instead of FEIE, or have another source of US-taxable earned income. More on that below.

What Actually Happens to Your 401(k) When You Leave

The short answer: nothing, immediately. Your 401(k) doesn't disappear when you resign from a US job and move to Portugal. The money stays exactly where it is, growing tax-deferred, until you decide to move it or take distributions.

But "doing nothing" is rarely the right long-term call. You have three options.

Option 1: Leave It in the Plan

This works short-term. If you're on a two-year assignment in Singapore and plan to return to a US employer, leaving your 401(k) in place is completely reasonable. The plan keeps running, your investments keep growing, and you deal with it when you're back.

The problems start for long-term expats. Former employer 401(k) plans are administratively cumbersome from abroad. Some custodians require US addresses for certain documents. You have fewer investment options than in a self-directed IRA. And you're locked into the plan's fee structure, which averages 0.5%–1.5% — several multiples higher than a low-cost IRA at a major custodian.

Option 2: Cash It Out (Almost Never Do This)

This is the million-dollar mistake.

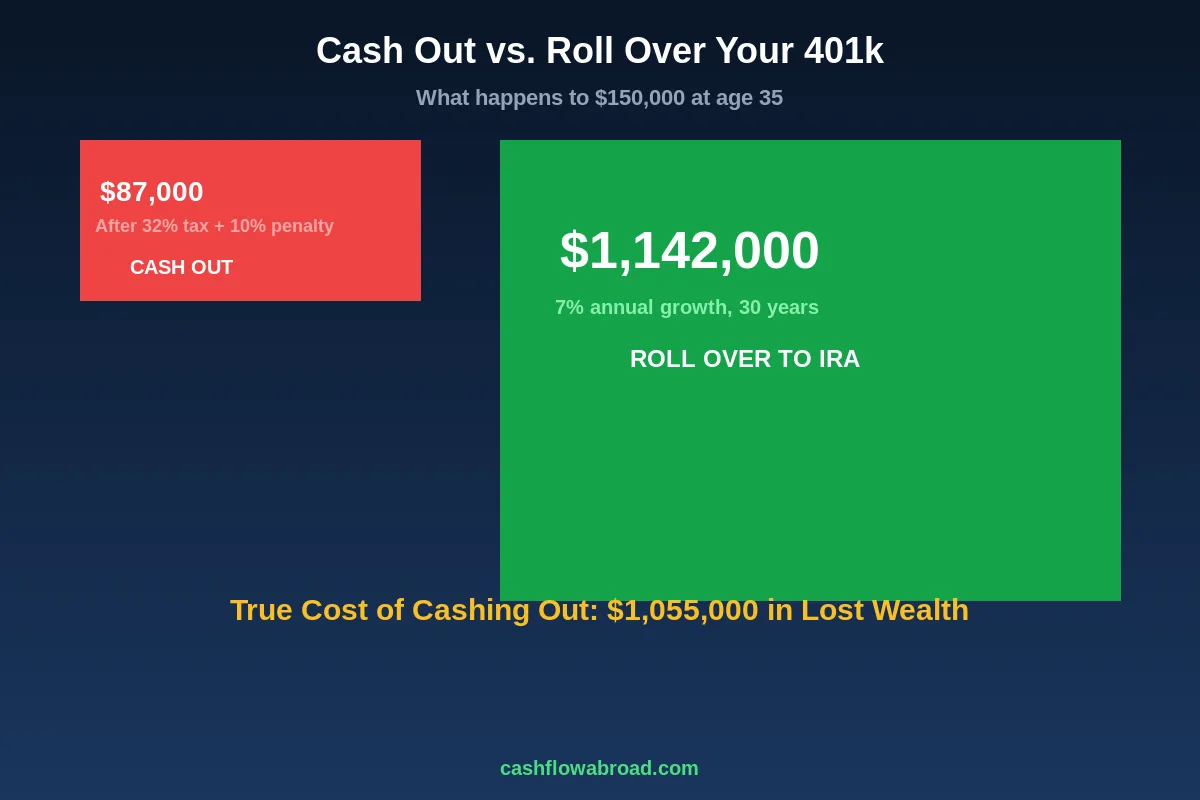

If you're under 59½ and you cash out your 401(k), you pay ordinary income tax on the entire amount plus a 10% early withdrawal penalty. At a 32% federal bracket, on a $150,000 balance, that's approximately $63,000 going straight to the IRS. You walk away with $87,000.

Roll that same $150,000 into an IRA instead, pay nothing now, let it grow at 7% annually for 30 years: you retire with $1,142,000. The cash-out decision didn't just cost you $63,000 in taxes. It cost you over $1 million in retirement wealth.

The only scenario where cashing out makes partial sense is genuine liquidity emergency with no other options — and even then, exhaust every alternative first. A 401(k) loan (if still employed), a personal loan, or a HELOC all have lower effective costs than the cash-out tax bomb.

Option 3: Roll Over to a Traditional IRA (Usually the Right Move)

A direct custodian-to-custodian rollover from your 401(k) to a Traditional IRA is a completely tax-free event. Nothing owed. The money transfers, continues growing tax-deferred, and you gain several important advantages:

- Lower fees: A self-directed IRA at a major custodian like Charles Schwab International often runs near-zero in expense ratios vs. 0.5%–1.5% for 401(k) plans

- Broader investment choices: Any publicly traded stock, ETF, or fund — not just the curated options in your former employer's menu

- Roth conversion flexibility: Rolling to a Traditional IRA unlocks the zero-tax Roth conversion strategy that most expats never learn about (more below)

- No US mailing address required with most major custodians if accounts are properly established before you leave

Note: A Roth 401(k) should roll directly to a Roth IRA — same logic, still tax-free, maintains after-tax treatment throughout.

One critical rule that catches many expats off-guard: you cannot roll a US 401(k) directly into a foreign pension plan. The IRS does not recognize most foreign pension plans as qualified accounts, even in countries with robust US tax treaties. Attempting this triggers a full taxable distribution plus potential penalties. Always roll into a US IRA; manage the foreign side separately.

Related: best retirement countries guide

The Zero-Tax Roth Conversion: The Expat's Most Powerful Retirement Move

This is the part of the expat tax code that should be taught in every financial planning course. It's legal, it's well-documented by the IRS, and it's being used right now by savvy expats to build six- and seven-figure tax-free retirement accounts while paying the federal government absolutely nothing.

Here's the mechanism.

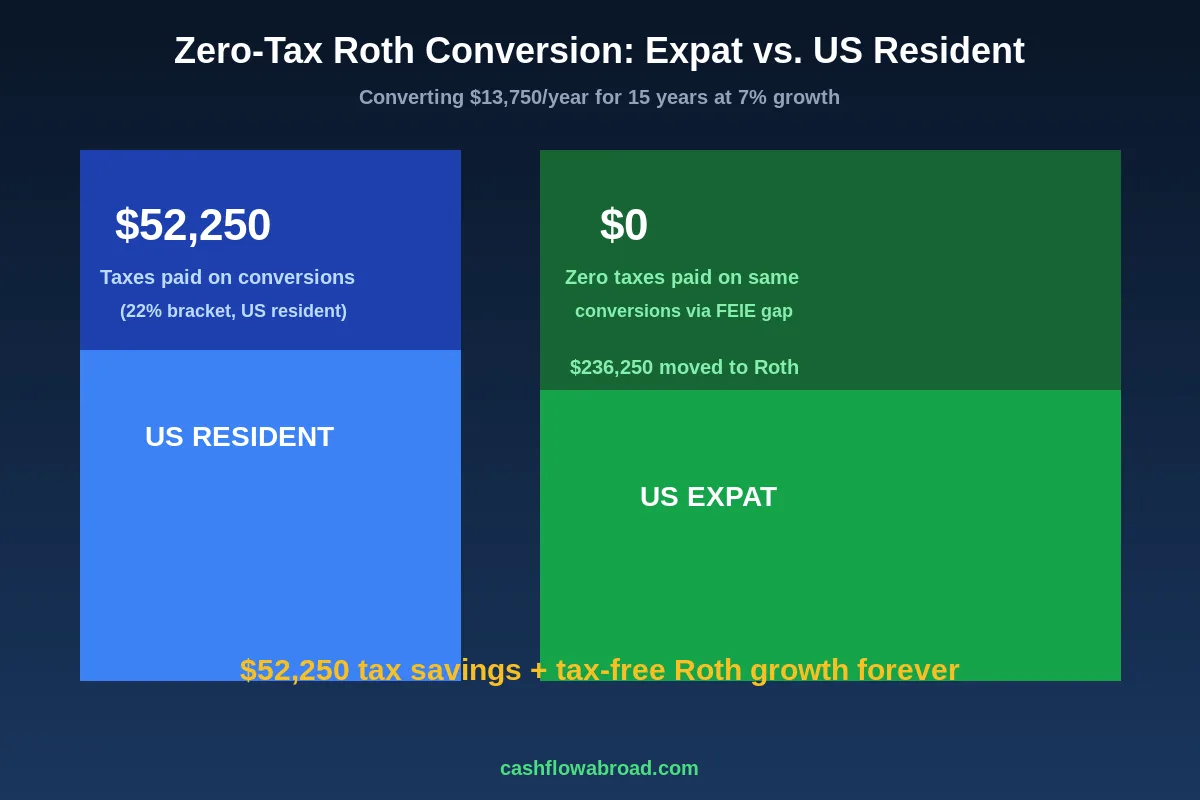

When you use the FEIE to exclude all of your earned income from US taxation, your taxable income on your US return is $0 (or close to it). But you still get to claim the standard deduction — $15,750 for single filers in 2025, $31,500 for married couples filing jointly.

That standard deduction creates a "zero-tax window." You can convert up to $15,750 per year from a Traditional IRA or rolled-over 401(k) into a Roth IRA — and pay zero federal income tax on the conversion.

In a Roth IRA, that converted money grows tax-free forever. When you withdraw it in retirement (after meeting the 5-year rule and age 59½), you pay zero tax. No required minimum distributions during your lifetime. No state income tax if you're domiciled in Florida, Texas, Nevada, or Wyoming.

The math for a single expat earning $90,000 abroad, using FEIE, living in Medellín:

- Earned income: $90,000 → excluded via FEIE → $0 US taxable earned income

- Passive income (dividends, interest): assume $2,000

- Standard deduction: $15,750 minus $2,000 passive income = $13,750 available for zero-tax conversion

- Convert $13,750 from Traditional IRA to Roth → $0 US federal tax owed

Over 15 years, that's approximately $206,250 converted to Roth tax-free. At 7% annual growth, that compounds to roughly $450,000–$500,000 in tax-free Roth assets by retirement. If you were doing the same conversions as a US resident in the 22% bracket, you'd have paid $45,375 in taxes on those same conversions — before accounting for state income tax if you're domiciled somewhere like California (up to 13.3%).

For married couples, the math is even better: $31,500/year in potential zero-tax conversions (minus passive income). Over 15 years: $470,000+ moved to Roth without a dollar of federal tax.

State domicile is not optional. Establish domicile in a no-income-tax state — Florida, Texas, Nevada, South Dakota, Wyoming — before you leave the US. California, New York, and several other states will continue pursuing you for state income taxes even after you've moved abroad if you haven't formally cut ties. California is particularly aggressive. Conversions done while California-domiciled get hit with state tax at up to 13.3%, even if you're sitting in a Chiang Mai coffee shop when you execute them.

One timing rule: conversions must be completed by December 31 of the tax year. You need a reasonable estimate of your full-year income before you convert, to avoid converting so much that you overshoot the zero-tax window and trigger an unexpected bill.

FEIE vs. Foreign Tax Credit: Which Preserves More Retirement Wealth?

The FEIE isn't the only way to handle US taxes abroad. The Foreign Tax Credit (FTC) gives you a dollar-for-dollar credit against your US tax liability for income taxes paid to a foreign government. In many situations, the FTC is actually the better choice — especially for expats in high-tax countries who want to maintain IRA contribution eligibility.

| Factor | FEIE (Form 2555) | Foreign Tax Credit (Form 1116) |

|---|---|---|

| IRA contribution eligibility | Destroyed if income fully excluded | Preserved (income stays "taxable" in US) |

| Best for | Low/no-tax countries (UAE, Panama, Cayman) | High-tax countries (Germany, France, UK) |

| Roth conversion opportunity | Yes — creates zero-tax window | Limited — income remains on return |

| Covers passive income? | No (earned income only) | Yes (earned and passive) |

| Unused credits? | N/A | Carry forward 10 years, back 1 year |

| Self-employment tax relief? | No | No |

| Switching flexibility? | 5-year lockout if you revoke | No election — use or skip annually |

Consider an expat earning $105,000 in Germany. German income tax at roughly 42% means approximately $44,100 in German taxes paid. Their US tax liability on $105,000 would be approximately $18,000–$20,000. Using the FTC, those German taxes wipe out the US bill entirely — with excess credits to carry forward for 10 years.

Now run the same scenario using FEIE instead: they exclude $105,000, owe approximately zero US tax — but lose all IRA contribution eligibility. Over 20 years, that's $7,000/year in forgone IRA contributions, growing at 7% annually: $295,000 in forgone retirement wealth versus the FTC approach.

The decision rule: if your effective foreign tax rate approaches or exceeds your equivalent US rate, use the FTC and keep contributing to your IRA. If you're in a low/no-tax country (UAE, Panama, Paraguay, Georgia), FEIE almost certainly wins and Roth conversions fill the gap. For the full FEIE strategy breakdown, see Zero Federal Income Tax as a US Expat: The FEIE Guide.

Roth IRA Abroad: What You Can and Can't Do

The Roth IRA is the most expat-friendly retirement account structure in existence. No required minimum distributions during your lifetime. Tax-free growth. Contributions (not earnings) always available without tax or penalty regardless of age. And it's accessible from anywhere in the world.

The 5-Year Rule

The clock starts January 1 of the tax year of your first-ever Roth IRA contribution. You must wait 5 years AND reach age 59½ for fully qualified distributions of earnings. This rule applies identically whether you live in Kansas City or Kuala Lumpur.

The practical implication: open a Roth IRA now, even with a $1 contribution, to start the 5-year clock. If you're already abroad and haven't contributed, start when you can. The clock doesn't care about account size — it only cares about the date of the first contribution.

How Your Host Country Taxes Roth Distributions

The US treats qualified Roth distributions as completely tax-free. Your country of residence may see things differently.

Related: expat investing playbook

| Country | Roth IRA Treatment | US Tax Treaty? | Notes |

|---|---|---|---|

| United Kingdom | Generally respected as tax-free | Yes | Pensions taxed only in country of residence; Roth treated favorably under treaty |

| Canada | Recognized with treaty election | Yes | No new contributions while Canadian resident; Form T1 treaty election required |

| Germany | Generally respected | Yes | Reciprocal pension treatment; Roth typically not taxed in Germany on qualified distributions |

| Australia | Taxed as ordinary income | Yes (limited) | Australia does not respect Roth tax-free status; distributions taxed as local income |

| Colombia | No treaty protection | No | No US-Colombia income tax treaty; distributions may be subject to local tax |

| UAE | Irrelevant — 0% income tax | No | No UAE income tax on any distributions; completely moot |

| Panama | Not locally taxed | No | Territorial tax system; foreign-source distributions not taxed in Panama |

| Portugal | Partially recognized | Yes | Standard rates up to 48%; IFICI/NHR 2.0 for qualifying innovation workers at 20% flat |

The pattern: for expats in treaty countries with favorable pension provisions (UK, Germany, Canada), Roth IRAs receive good treatment. For zero-tax countries like UAE and Panama, it's a non-issue. For countries without a US treaty, research local treatment carefully before building a heavy Roth distribution strategy.

The PFIC Trap: How Foreign Mutual Funds Can Destroy Your Investment Returns

If you've opened a local brokerage account in your host country and purchased any foreign mutual funds or ETFs — stop and consult a US expat tax professional before filing your next return.

The IRS classifies most non-US investment funds as Passive Foreign Investment Companies (PFICs). Any non-US corporation where 75%+ of gross income is passive (dividends, interest, rents, capital gains) or 50%+ of assets produce passive income qualifies. This catches virtually every foreign mutual fund and most foreign ETFs sold by local banks to expat clients.

The tax treatment is deliberately punitive. Distributions above 125% of the 3-year average are called "excess distributions" — taxed as ordinary income at the highest marginal rate, plus non-deductible interest charges compounding annually back to the year you first purchased. Effective total tax rates on PFIC excess distributions routinely exceed 50–60%.

The practical rule: hold US funds, not foreign ones. An S&P 500 ETF held in a US IRA or US brokerage account is completely exempt from PFIC rules. The equivalent S&P 500 tracker sold by a German bank through a German brokerage account is a PFIC. Same underlying assets, wildly different tax consequences.

For international exposure in your portfolio, use US-listed international ETFs: iShares MSCI EAFE (EFA), Vanguard FTSE All-World ex-US (VEU), or similar. These are not PFICs. They're fully compliant. Hold them through a US account at Charles Schwab International, Fidelity, or Vanguard — all of which are accessible from abroad and do not have the PFIC problem.

For expats who already own PFICs inadvertently, the Streamlined Foreign Offshore Procedures (SFOP) offer a path to catch up on Form 8621 (required for each PFIC held) without standard failure-to-file penalties. Missing PFIC reporting can suspend the statute of limitations on your entire tax return — the IRS can examine returns indefinitely when required forms are absent.

RMDs Abroad: The 30% Withholding Trap Nobody Warns You About

Required Minimum Distributions arrive whether you live in Phoenix or Phuket. Under the SECURE 2.0 Act:

- Born 1951–1959: RMDs begin at age 73

- Born 1960 or later: RMDs begin at age 75 (effective 2033)

- Roth IRAs: No RMDs during your lifetime — one of the Roth's biggest structural advantages

- Penalty for missed RMD: 25% excise tax on the shortfall (enforced again by IRS starting 2025 after the 2021–2024 moratorium)

The withholding trap: if your custodian has a foreign address on file, they may automatically withhold up to 30% of your RMD as non-resident alien (NRA) withholding — even if a tax treaty reduces your actual rate to zero or 15%.

The fix: file Form W-8BEN with your custodian before distributions begin, claiming treaty benefits. Without it, you're giving the IRS an interest-free loan and waiting months for your refund via Form 1040-NR.

Treaty reduced withholding rates on pension distributions:

- UK: 0% (taxable only in UK under the treaty)

- Canada: 25% or lower under treaty provisions

- Germany: 15%

- Australia: 10% (reduced from statutory 30%)

- Colombia: 30% — no treaty, full withholding applies

- Panama: 30% — no treaty, full withholding; reclaim via Form 1040-NR

If you're retiring in a no-treaty country, heavy use of Roth IRA assets sidesteps this problem entirely — qualified Roth distributions have zero US withholding, full stop. This is one of the strongest arguments for maximizing Roth conversion during your working years abroad.

Self-Directed IRAs: Invest in Foreign Real Estate Tax-Sheltered

For expats who want to combine retirement account tax advantages with foreign real estate investing, the Self-Directed IRA (SDIRA) is worth understanding — though it comes with strict rules.

A SDIRA allows investment in non-traditional assets including:

- Foreign real estate (rental properties, raw land, condominiums)

- Physical gold and IRS-approved precious metals

- Private equity and private loans

- Cryptocurrency through specialized custodians

A typical foreign real estate structure through a SDIRA works like this:

- Open a SDIRA with a specialized custodian (standard brokerages like Fidelity and Schwab don't offer this product)

- The IRA custodian establishes a US LLC

- The US LLC holds ownership of a local entity in your target country (a Colombian SAS, a Mexican S.A. de C.V., etc.)

- The local entity owns the property

- All rental income and appreciation flow back to the IRA — tax-deferred in a Traditional SDIRA, tax-free in a Roth SDIRA

The prohibited transaction rules are absolute: you cannot live in or vacation in IRA-owned property, rent to yourself or family members, or perform personal labor on the property. Violating these rules converts the entire IRA into a taxable distribution instantly. All management must go through third parties.

The SDIRA wrapper doesn't eliminate local country taxes — your Colombian entity still has Colombian tax obligations. But it can dramatically reduce or eliminate US federal taxes on investment returns, especially in a Roth SDIRA where qualified distributions are completely tax-free. For more on expat investment structures, see the Expat Investor's Playbook.

The 5-Year Revocation Lockout: The Most Expensive Accidental Mistake in Expat Tax

This deserves its own section because it's catastrophically expensive and shockingly common among expats who switch countries or work with tax preparers unfamiliar with expat-specific rules.

Related: expat estate planning guide

Once you elect the FEIE (by filing Form 2555), you must continue claiming it unless you formally revoke it. If you revoke — either intentionally to switch to the FTC, or accidentally — you are barred from re-electing FEIE for five consecutive tax years.

Accidental revocation happens more often than you'd think:

- Simply omitting Form 2555 from a return while still eligible is treated as a revocation

- Claiming an FTC or deduction on income that could have been excluded with FEIE automatically revokes the election

- Using a tax preparer unfamiliar with expat rules who files incorrectly

If you accidentally revoke FEIE and then relocate to a zero-tax country like the UAE, you're locked out of FEIE for five years. At $22,000–$30,000 in annual FEIE-driven tax savings, the 5-year lockout costs you $110,000–$150,000 in avoidable taxes.

The only path to early reinstatement: apply for a Private Letter Ruling from the IRS. Cost: $43,700 for most filers ($3,450 if gross income is under $250,000). And the IRS can simply deny it.

By contrast, the Foreign Tax Credit has no equivalent election requirement. You can claim it one year, skip it the next, claim it again — no penalty. This flexibility is a meaningful advantage of the FTC for expats moving between countries with different tax regimes.

The practical rule: never file a return that omits Form 2555 if you're using FEIE. Never let a domestic-focused accountant touch your expat return without verifying they understand the revocation rules.

Strategy by Country: What Makes Sense Where You Are

UAE / Dubai: Maximum Accumulation

Zero UAE income tax. FEIE eliminates US tax on the first $130,000+. Self-employed Americans in Dubai still owe 15.3% self-employment tax (FEIE does nothing for SE tax — a costly surprise for many Dubai-based freelancers). But employees face a near-unprecedented tax efficiency window.

IRA strategy: FEIE kills contribution eligibility below the cap. Use the zero-tax Roth conversion window aggressively instead. Roll any existing 401(k) to a Traditional IRA before departing the US, then convert to Roth within the standard deduction gap every year you're in the UAE.

Germany / High-Tax Europe: FTC + Ongoing IRA Contributions

German income taxes at 40%+ routinely exceed equivalent US rates, meaning FTC eliminates your US tax bill while your income remains "taxable" in the US — preserving full IRA contribution eligibility. Contribute the maximum ($7,000 in 2025) to a Roth IRA annually. German tax treatment of Roth distributions is generally favorable under the US-Germany tax treaty.

Panama / Territorial Tax Countries: FEIE + Roth Conversions

Panama taxes only Panama-sourced income. Remote workers earning US-source income pay zero Panamanian income tax. Combined with FEIE, this is as close to a legally tax-free existence as most Americans can achieve. Maximize Roth conversions in the standard deduction gap every year. No US-Panama treaty means 30% withholding on Traditional IRA distributions unless you file Form W-8BEN and reconcile via 1040-NR — so weight your accounts toward Roth heavily.

Colombia / Latin America: Geographic Arbitrage + Capital Efficiency

The retirement math in Colombia is extraordinary. A couple living comfortably in Medellín spends $1,300–$2,000/month, requiring a nest egg of roughly $480,000 at a 4% withdrawal rate. The same lifestyle in a US city runs $6,000–$8,000/month — requiring $1.8–$2.4 million. That's 73–80% less capital needed.

Our colleagues at ColombiaMove.com have the full monthly budget breakdown for Medellín — granular numbers on groceries, utilities, restaurants, transport, and healthcare. If you're considering Colombia as a retirement base, it's required reading before you run your retirement projections.

No US-Colombia income tax treaty means IRA distribution planning requires extra attention. Lean toward Roth accounts where possible to avoid the 30% withholding issue on Traditional IRA and 401(k) distributions. See the full Geographic Arbitrage Playbook for 10-country comparisons.

The Expat Retirement Account Action Checklist

Before You Leave the US

- Establish domicile in a no-income-tax state (Florida, Texas, Nevada, South Dakota, Wyoming). Do this before you file your last US state return. California and New York will pursue state taxes even after you've left if domicile is not properly severed.

- Roll your 401(k) to a Traditional IRA if leaving your employer. Use a custodian with international-friendly policies — Charles Schwab International is the standard recommendation for expats, offering free global ATM withdrawals and no foreign account complications.

- Open a Roth IRA if you don't have one. Even a $1 contribution starts the 5-year clock. Don't leave the US without it.

- Decide: FEIE or FTC. Know your destination country's effective tax rate on your income type. If it's below ~20–22%, FEIE probably wins. If it's above ~30%, FTC probably wins. Get qualified expat CPA advice before filing the first return abroad.

- File Form W-8BEN with your IRA custodian to establish treaty-rate withholding on future distributions.

First Year Abroad

- Calculate your Roth conversion capacity. Estimate full-year income, subtract FEIE exclusion, subtract standard deduction, subtract passive income. That net figure is your zero-tax conversion window.

- Execute Roth conversions by December 31 — they cannot be backdated to the prior year.

- Stop IRA contributions if using FEIE and your income is entirely below the cap. Continuing creates 6% annual penalties requiring Form 5329 corrections.

- Avoid foreign mutual funds in local brokerage accounts. Hold international exposure through US-listed ETFs in your US accounts only.

Annually, Every Year Abroad

- Repeat Roth conversions within the zero-tax window

- File FBAR (FinCEN 114) if any foreign financial accounts exceed $10,000 aggregate at any point during the year

- File Form 8938 (FATCA Statement) if foreign financial assets exceed $200,000 single filer or $400,000 married filing jointly (thresholds for those residing abroad)

- Never omit Form 2555 if using FEIE — omission equals revocation

- File Form 8621 for any PFIC holdings, and stop buying new PFICs

The Accounts and Tools That Actually Work for Expats

A few practical recommendations for managing US retirement accounts from abroad:

- Charles Schwab International: The standard recommendation for long-term US expats. Free ATM withdrawals worldwide, no foreign transaction fees, and their IRA and brokerage accounts work smoothly from abroad. You can hold any US-listed ETF from any country.

- tastytrade: For active traders and options strategies, tastytrade offers competitive commissions and clean mobile access. Solid for managing a taxable brokerage account alongside your IRA strategy.

- Mercury: If you run a US-registered business from abroad, Mercury is the expat entrepreneur's banking layer — US business checking, no monthly fees, built for remote operations.

- Remitly: For moving money between US accounts and local bank accounts in your host country, Remitly consistently offers better exchange rates with transparent fees versus wire transfers through a traditional bank. Worth bookmarking alongside our full expat money transfer guide.

The Bottom Line

Your retirement accounts don't stop working when you move abroad. In many ways, they start working harder — because the expat tax code creates wealth-building opportunities that simply don't exist for people living in the US.

The zero-tax Roth conversion window can put $50,000–$200,000 in tax-free wealth into your retirement portfolio over a decade, compared to doing the same conversions as a US resident. The geographic arbitrage math means you need 50–75% less capital to retire comfortably in most of the world versus any major US metro. And avoiding the 401(k) cash-out mistake can preserve over $1 million in lifetime retirement wealth.

The catch is knowing the rules before you make the moves. The FEIE-IRA contribution interaction, the 5-year revocation lockout, the PFIC trap, the withholding rules on RMDs — these are all legally clear, well-documented, and consistently misunderstood by anyone who hasn't specifically studied expat tax law.

Hire a qualified US expat CPA for your first year abroad at minimum. The typical cost is $500–$2,000 annually. Given the mistakes described in this article and the strategies available to avoid or exploit them, the ROI on that advice is routinely 10x–50x or more. It is the highest-leverage money you will spend in your first year abroad.

For the broader expat investing framework, see the Expat Investor's Playbook. For banking, FBAR, and FATCA essentials, start with the US Expat Banking & Taxes guide. For the full FEIE vs. FTC decision breakdown, see Zero Federal Income Tax as a US Expat.

Financial Disclaimer: This article is for informational and educational purposes only and does not constitute financial, tax, or legal advice. US tax law is complex and individual circumstances vary significantly. Always consult a qualified US expat tax professional or CPA before making decisions about retirement accounts, FEIE elections, Roth conversions, or investment structures abroad. Rules referenced are based on information available as of the date of publication and are subject to change by the IRS or Congress.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Investing & Wealth BuildingJuly 3, 2026

Investing & Wealth BuildingJuly 3, 2026

REITs for US Expats: Income, Tax Rules, and PFIC Traps

US expats can earn 4%+ REIT yields at a 29.6% effective rate with the permanent Section 199A deduction. Know which funds are PFICs and which are not.

Investing & Wealth BuildingJune 26, 2026

Investing & Wealth BuildingJune 26, 2026

Options Trading for US Expats: Tax Rules and Traps

Section 1256 contracts cap US expat options traders at a 26.8% blended rate. Understand wash sales, NIIT traps, mark-to-market, and Form 6781 rules.

Investing & Wealth BuildingJune 24, 2026

Investing & Wealth BuildingJune 24, 2026

W-8BEN: How Expats Cut US Withholding on Dividends

Nonresident aliens can halve 30% US dividend withholding with Form W-8BEN. See treaty rates by country, the portfolio interest exemption, and REIT